Charts of the Week

Current economic trends from 27 June to 1 July: inflation, bond, value of fiscally verified invoices, turnover in trade and turnover in market services

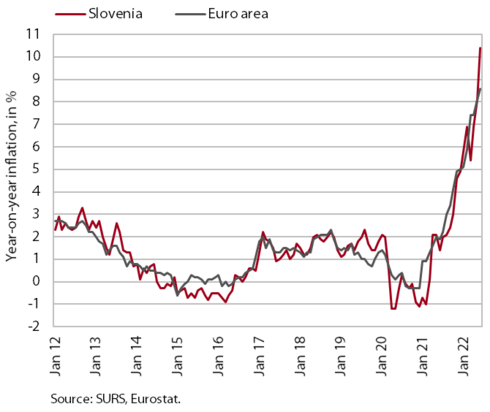

Year-on-year inflation continued to strengthen significantly in June; prices were one-tenth higher than a year earlier. Growth was mainly driven by more than one-third higher prices of energy. Growth of food prices was also slightly above average. Stronger inflation in the euro area and the announcement by ECB to accelerate monetary policy normalisation are the reasons for the rise in yields to maturity of euro area government bonds. The yield on the Slovenian bond reached its highest value since 2014 in the second quarter. Amid high growth of prices and turnover, the value of fiscally verified invoices in mid-June was about one-fifth higher in nominal terms than the value in the same periods of 2019 and 2021. Data on real income for April and partly for May show that growth in trade and other market services continued.

Inflation, June 2022

Inflation rose sharply again in June, to 10.4% year-on-year (2.7% month-on-month). This was mainly due to the expiry of the temporary exemption from the payment of certain electricity charges, which had been adopted in February to cushion the impact of high energy prices. As these charges were imposed again, the electricity price in June was more than 50% higher month-on-month. Energy prices have been on the rise since March last year and have been given an additional boost by the aggravation of the situation in Ukraine. According to our estimates, they were already about 35% higher year-on-year in June, contributing more than 4 p.p. to inflation. This does not yet take into account the impact of the change in the regulation of oil product prices on 21 June, which will be fully reflected in July’s inflation. Higher energy and food commodity prices, which to some extent are also due to geopolitical tensions, are increasingly affecting final food prices, which were 12.8% higher year-on-year in June. A significant contribution to growth came from higher prices of bread, cereal products, oils and meat. The price of services continued to rise by around 5%, especially due to higher prices for food service activities, rents, package holidays and accommodation. Price increases were high across most groups of goods and services. Only in education and communication was the price increase below 2% (0.4% and -5.3% respectively).

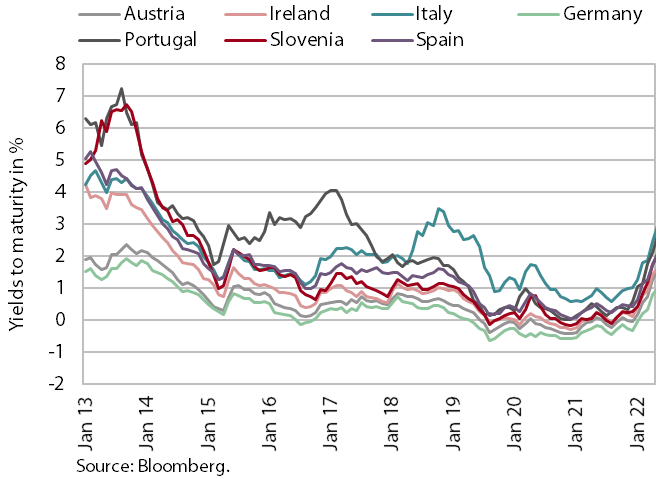

Bond, Q2 2022

Yields to maturity of euro area government bonds rose significantly in the second quarter. The decisive factors were the rise in inflation in the euro area and the announcement by the ECB to accelerate monetary policy normalisation. Yields to maturity of government bonds of peripheral countries are increasing more markedly. The yield to maturity of the Slovenian government bond was thus 2.11% in the second quarter, which is the highest since 2014. The spread to the German bond was 102 basis points, about 40 basis points higher than in the previous quarter and twice as high as before the epidemic.

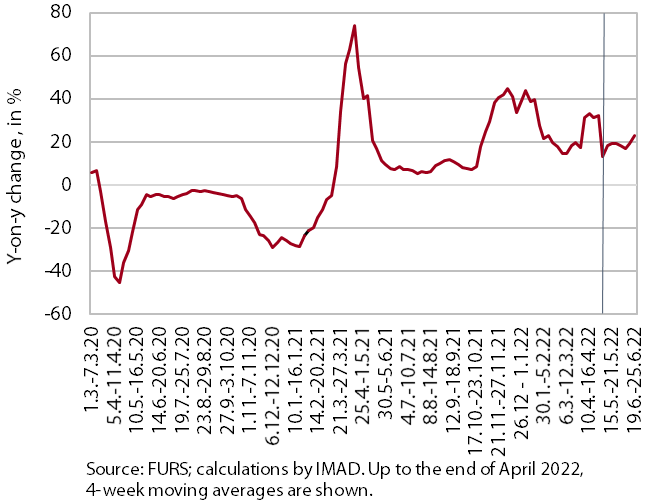

Value of fiscally verified invoices, in nominal terms, 12–25 June 2022

Amid high price growth, the value of fiscally verified invoices between 12 and 25 June 2022 was about one-fifth higher than in the same periods of 2019 and 2021. The 17% nominal growth of turnover in trade, where about three-quarters of the total value of fiscally verified invoices is issued, contributed most to the slightly higher year-on-year growth compared to the growth in the previous two weeks. Another significant growth factor was also 64% nominal growth of turnover in accommodation and food service activities (mainly due to high growth in accommodation), which was significantly lower than in previous months due to the continued lifting of operating restrictions last June.

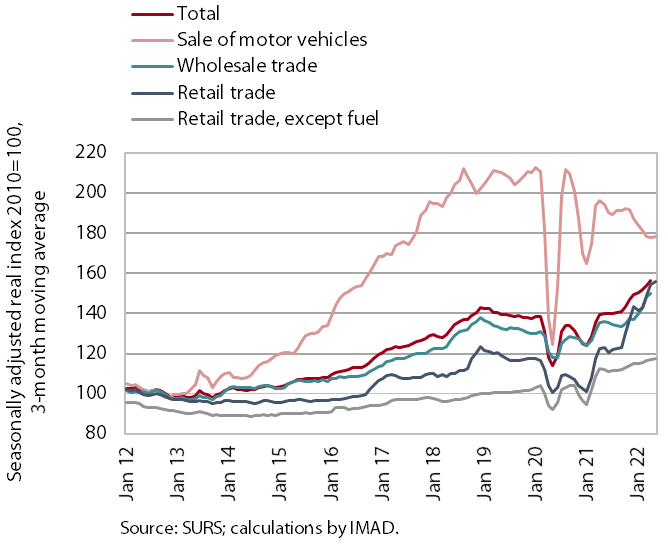

Turnover in trade, April–May 2022

Growth of turnover in trade continues. In April, growth was strongest in trade of motor vehicles, where turnover rose sharply again in May, according to preliminary data. Despite the growth, this was the only major trade segment that lagged behind pre-epidemic levels due to low sales in previous months. After the high growth in the first quarter, turnover further increased in wholesale trade. It fell in retail trade, which, in addition to lower turnover in the trade of automotive fuel (where real turnover fluctuated sharply in recent months), is also affected by lower turnover in the sale of food, beverages and tobacco. Turnover increased (in April and also in May, according to preliminary data) in retail trade of non-food products. Given a low base last year (due to the lockdown in the first third of April), it achieved high year-on-year growth of 12.5% in April.

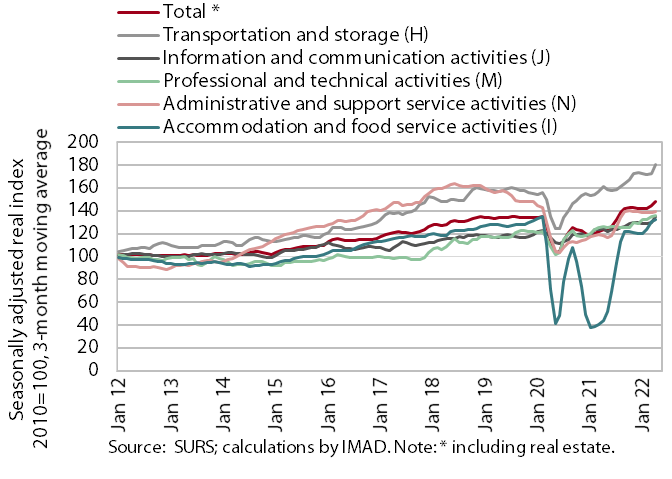

Turnover in market services, April 2022

Real turnover growth in market services continued in April. Total real turnover increased by 2.5% month-on-month and by 23.5% year-on-year, given the low base in April 2021. In current terms, growth accelerated in information and communication activities and transportation and storage. In the former group, this was mainly due to the resumption of significant turnover growth in telecommunication services, where turnover has mostly increased since December last year, and the continued favourable trend in computer services in the domestic and foreign markets. In the latter group, growth was mainly driven by land transport and postal activities. Turnover in professional and technical activities and administrative and support service activities stagnated. After high growth in the previous months, turnover only decreased in accommodation and food service activities. The lag compared to pre-epidemic turnover (April 2019) was only noticeable in travel and employment agencies (by 40% and by 28% respectively).