Charts of the Week

Current economic trends from 24 to 28 January 2022: economic sentiment, wages, turnover in trade, turnover in market services and other charts

Economic sentiment improved slightly again in January despite the negative impact of supply chain disruptions and uncertainty surrounding the development of the epidemic. Year-on-year growth in average gross wages in the private sector remains high, which we estimate could also be due to labour shortages in some activities (manufacturing, construction and accommodation and food service activities). Due to the cessation of epidemic-related bonus payments, year-on-year public sector wage growth slowed significantly in the second half of the last year and was already negative in November. Turnover based on fiscal verification of invoices was 19% higher year-on-year in the first half of January and was slightly higher than the same period in 2019. Turnover in trade continued to increase last November. After a decline in October, turnover in market services increased again, with only travel and employment agencies falling below pre-epidemic levels.

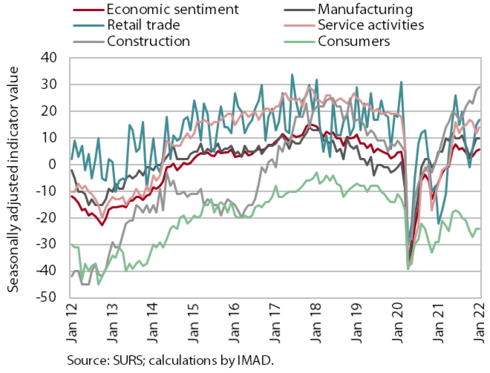

Economic sentiment, January 2022

The economic sentiment indicator rose in January for the third month in a row and remains well above the long-term average. On a monthly basis, confidence rose in most activities, while in manufacturing and among consumers it remained at the same level as last December. Confidence was significantly higher in January than in the same period last year, when stringent measures to contain the spread of the epidemic were still in place (confidence was particularly low in retail trade and among consumers). Confidence in manufacturing and construction was also higher than in the same period in 2019. Confidence was also well above the long-term average in construction (up 39 p.p.) and in manufacturing (up 10 p.p.). Despite the improvement in economic sentiment, there are still some limiting factors present. The deterioration in manufacturing is the result of the current situation in the international environment (supply bottlenecks, rising non-energy commodity and energy prices), while the deterioration in the retail trade and among consumers is related to uncertainty about the epidemic situation and the measures taken.

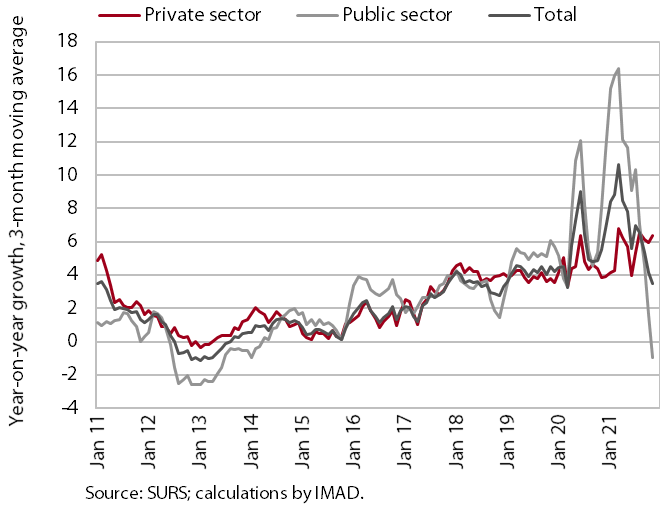

Wages, November 2021

In November 2021, average wages in the public sector were 4.1% lower year-on-year, while they were 7.2% higher in the private sector. Due to the cessation of epidemic-related bonus payments, year-on-year wage growth in the public sector slowed significantly in the second half of last year and already turned negative last November. In the first eleven months of 2021, these wages were 7.8% higher than in the same period of 2020. In the private sector, average wages increased by 5.9% year-on-year in the first eleven months, mainly due to the impact of the minimum wage increase at the beginning of the year, but also to the return to employment of workers who had participated in job retention measures. According to our estimates, wage growth in some private sector activities (manufacturing, construction and accommodation and food service activities) could also be the result of labour shortages. The year-on-year increase in private sector wage growth last November was also influenced by extraordinary payments (13th salary and Christmas bonus), which were higher than in the same periods of 2020 and 2019, given the good performance of companies.

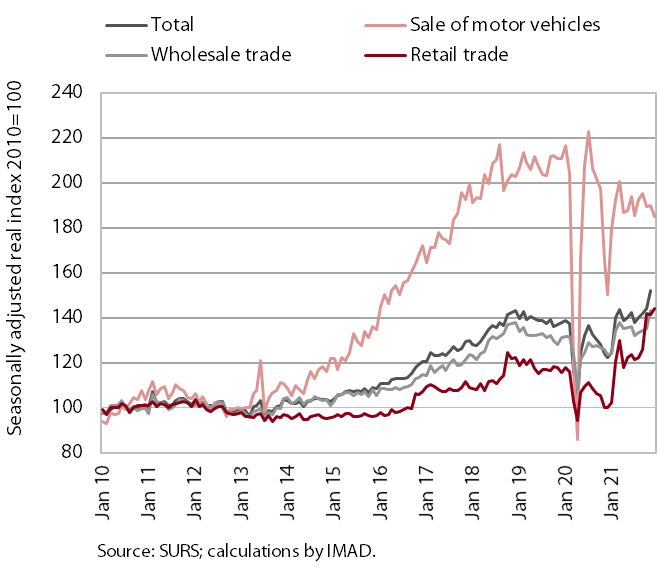

Turnover in trade, November–December 2021

Turnover in trade increased further last November. The monthly growth was mainly due to growth in wholesale trade. Turnover in the sale of motor vehicles remained at the (low) level reached and, due to delays in the delivery of vehicles, this was the only main segment that fell short of 2019 turnover. Turnover in retail sales also remained at the level reached, with further growth in turnover in the sale of non-food products and a decline in the sale of automotive fuels after high growth in the previous month. Turnover in the sales of food, beverages and tobacco was also lower, declining further last December, according to preliminary data. After stagnating in 2020, turnover in the latter increased by 7.9% year-on-year in 2021 and by 18.8% in the retail sector as a whole, with even higher growth in the sale of automotive fuels and non-food products.

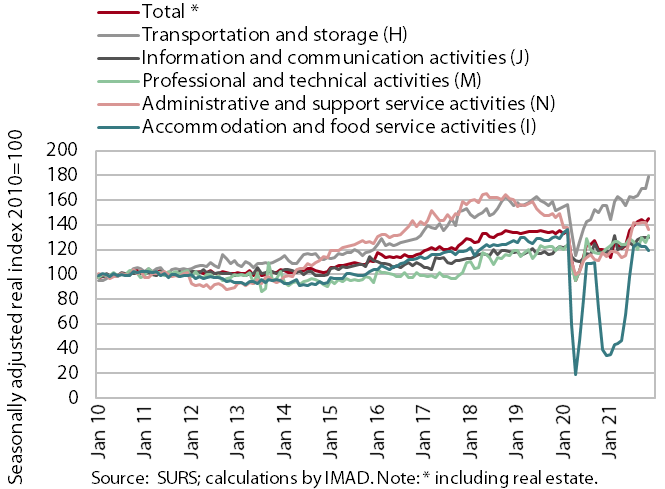

Turnover in market services, November 2021

Real turnover in market services rose again last November. It was up by 2% compared to the previous month and by 18.9% year-on-year. Turnover grew strongly in transportation and storage and professional and technical activities, mainly due to renewed strong growth in land transport and architectural and engineering services. Turnover in information and communication activities remained at the high previous month’s level. After stagnating in the previous months, the sharpest decline in turnover was recorded in administrative and support service activities, mainly due to a further decline in turnover in employment agencies. With the further worsening of the epidemic situation and the restrictions on business operations, turnover further declined in accommodation and food service activities. Turnover in November 2021 was higher year-on-year in all market services, but compared to the same month in 2019, only travel and employment agencies saw significantly lower turnover (by 46% and by 22% respectively).

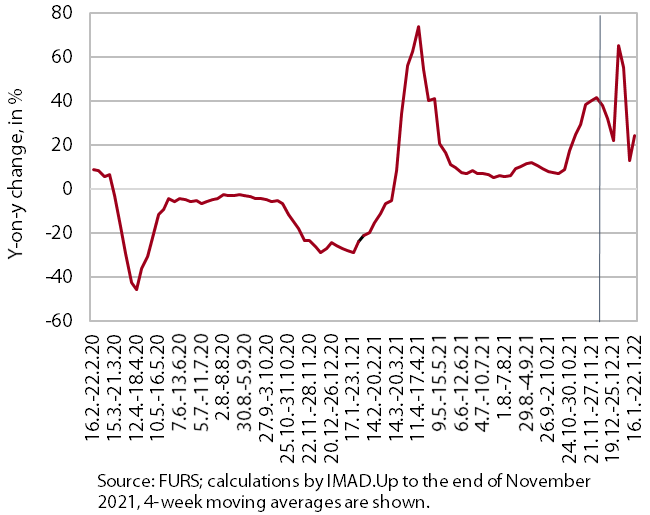

Turnover based on fiscal verification of invoices, 9–22 January 2022

According to data on fiscal verification of invoices, total turnover between 9 and 22 January 2022 was 19% higher year-on-year and 1% higher than in the same period of 2019. Year-on-year growth has fallen sharply compared to growth in the last two weeks, partly due to the worsening epidemiological situation. As a result, the number of people in quarantine, isolation and self-isolation increased, which was reflected in lower year-on-year turnover growth across all sectors. Although growth was lower, it remained very high year-on-year in the activities that were still almost completely shut down at the beginning of 2021 – mainly in tourism-related services. Growth in total turnover was also significantly lower than in the previous two weeks compared to turnover in the same period of 2019. Growth in trade fell to 1% (turnover in retail sales was lower than in 2019); most other sectors have widened the gap with pre-crisis levels.