Charts of the Week

Current economic trends from 23 March to 3 April 2020: economic sentiment, prices, oil prices, bond yields and others

Some of the commented data do not yet cover the period when the coronavirus broke out in Slovenia and other EU countries and mostly indicate favourable developments in service activities at the beginning of this year. According to the first data available for March, confidence in the Slovenian economy deteriorated strongly due to the consequences of the COVID-19 epidemic, particularly in retail trade and in service and manufacturing activities. Year-on-year consumer price growth also slowed markedly in March. Electricity prices fell sharply, as did liquid fuel prices amid record low prices of oil on world markets.

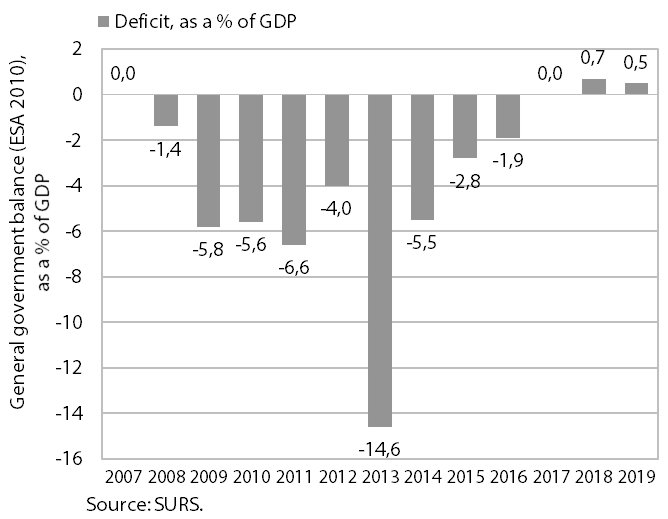

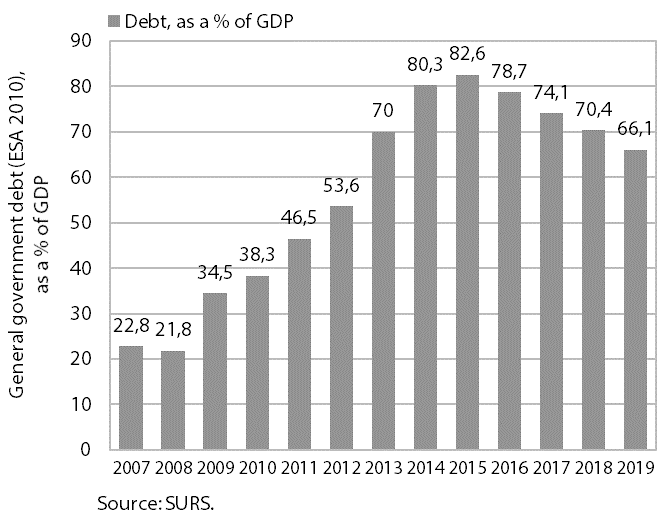

We also comment the past situation in public finances, which had improved significantly by 2019. The improvement in the general government balance in circumstances of high economic growth contributed to a rapid decline in the general government debt as a share of GDP in 2015–2019, which amounted to 66.1% last year.

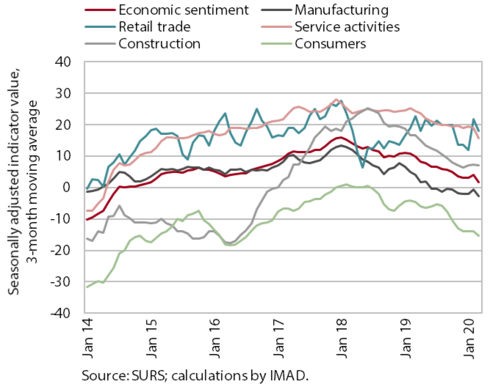

Economic sentiment, March 2020

Confidence in the economy dropped sharply in March. Confidence indicators fell in all sectors of the economy. The decline was the most pronounced in retail trade and in service and manufacturing activities, while the indicators of confidence in construction and among consumers were only slightly lower than in February. Confidence in manufacturing deteriorated mainly due to lower production expectations. However, as the survey was conducted in the first half of March, the March indicators do not yet fully reflect companies’ and consumers’ response to the negative consequences of the coronavirus outbreak in Slovenia and Europe. The situation has since changed significantly due to the rapid spread of the virus and the strict containment measures.

Prices, March 2020

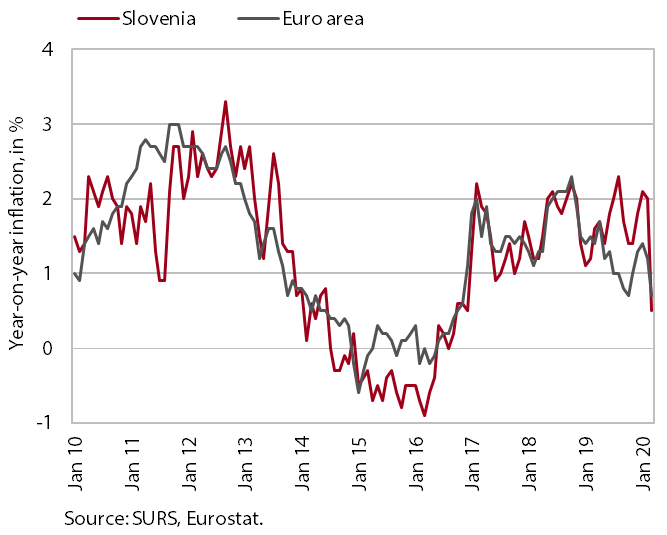

Year-on-year consumer price growth slowed notably in March, largely owing to lower prices of goods. Electricity prices dropped by 27.6% as a consequence of the measures to mitigate the consequences of the COVID-19 epidemic. Amid record low oil prices on world markets, prices of liquid fuels (7.3%) also dropped more markedly due to the pandemic. Year-on-year growth in food prices strengthened further, which can be partly attributed to higher demand at the outbreak of the epidemic. Moderate growth in prices of semi-durable goods continued, while the decline in durable goods prices slowed somewhat. Growth in prices of services eased in March. At 1.8%, it was at the lowest level since April.

Oil prices, March 2020

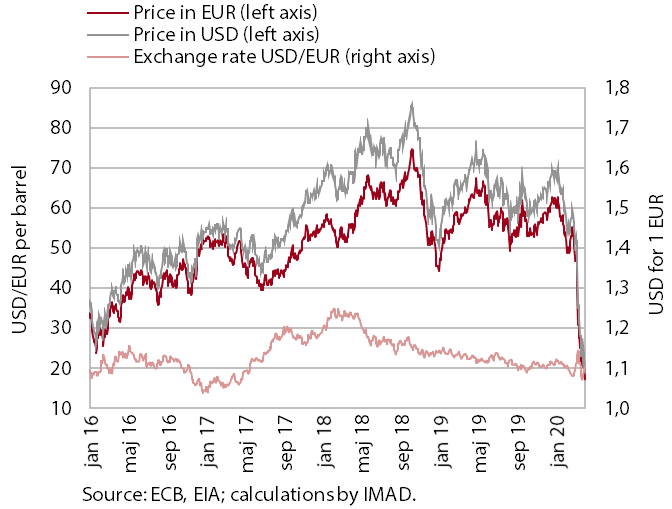

Oil prices reached record lows in March. The average dollar price for a barrel of Brent crude fell by 40% at the monthly level, to USD 33. The lowest March value slipped below USD 20, which is a 20-year low. Owing to a higher value of the euro against the US dollar, euro prices fell even somewhat more. Dollar prices of oil were down 51% year on year. A marked decline was a consequence of lower demand due to measures to contain the COVID-19 pandemic, but also the price war between Saudi Arabia and Russia.

Bond yields, Q1 2020

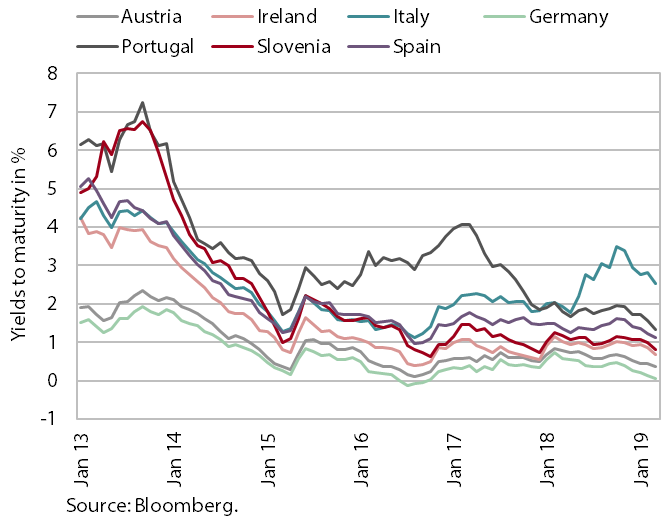

As a result of the COVID-19 epidemic, euro area bond markets were fairly volatile in the first quarter. The yields to maturity of most countries increased; without the ECB’s comprehensive package of measures to mitigate the consequences of the pandemic, the increase would have been even more pronounced. Particularly the yields of peripheral countries were higher, while the yields of some core countries actually declined. This is largely due to investment in safer assets according to our estimate. The spread of the Slovenian bond against the German bond rose to 60 basis points in the first quarter of this year.

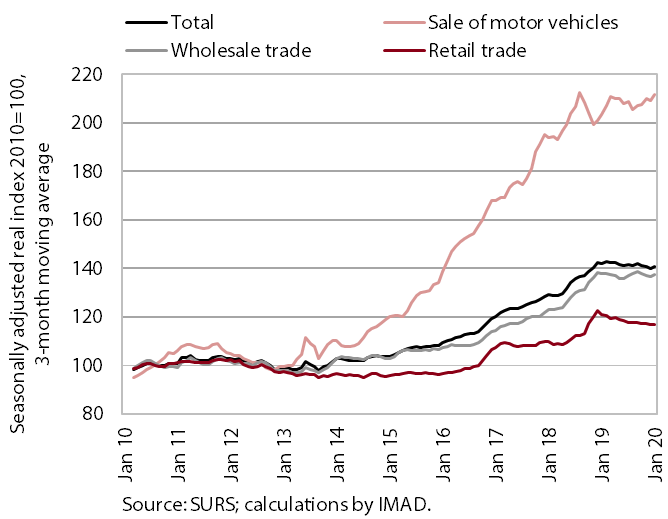

Turnover in trade, January 2020

Turnover in trade increased in January, following a decline at the end of last year. Turnover rose in all three main segments, under the impact of a further moderation of private consumption growth and increased activity in some sectors related to trade (manufacturing, construction, transport, etc.). With the spread of the coronavirus epidemic, the situation in trade changed. Turnover in food stores rose considerably in February according to preliminary data. Similar developments are also expected for March. Turnover growth in the sale of non-food products also continued in February according to preliminary data, which is however not expected for March due to the closure of such stores due to the epidemic.

Market services, January 2020

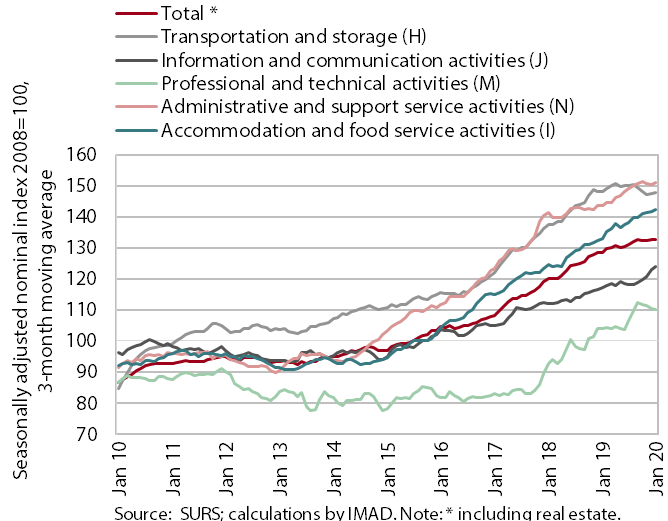

In January, the growth of turnover in market services continued in most services, after decelerating towards the end of last year. In accommodation and food service activities it accelerated as a result of the contribution from both accommodation activities and the sale of food and beverages. Strong growth was also recorded for transportation, which is mainly attributable to road freight transport and harbour transport. Strong turnover growth also continued in administrative and support service activities, mostly as a result of travel agency activities, which significantly contribute to the total turnover. With further growth in export revenues in computer services, turnover growth in information and communication activities slowed slightly. Turnover in professional and technical activities maintained the high level reached in the second half of last year.

Real estate, Q4 2019

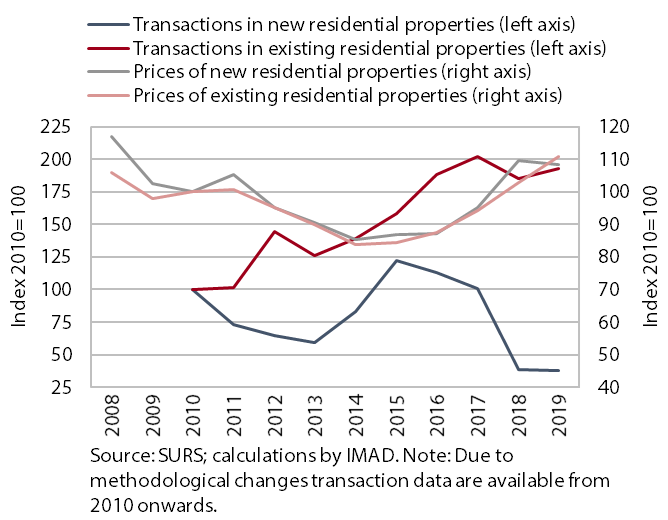

The average residential property price increased further in 2019, but growth moderated slightly. On average, it was 6.9% higher year on year (8.0% and 9.8% in the previous two years). The increase was a consequence of higher prices for existing dwellings, which last year exceeded 2008 prices for the first time. Prices of existing flats outside Ljubljana rose by more than a tenth for the second consecutive year, exceeding the average 2008 price by 13.3%. The growth of the average price of existing flats in Ljubljana, which started earlier than in the rest of Slovenia, eased to 2.5% last year (exceeding the 2008 price by 3.6%). Meanwhile, the average price of new dwellings dropped somewhat in 2019 (amid the lowest number of transactions in the last decade), after rising in the last four years.

General government balance

The public finance position had improved significantly by 2019. This was a consequence of the economic recovery after the financial crisis and fiscal stabilisation measures. The improvement in the fiscal position in 2018–2019 could have been even greater, but even this continuous improvement of several years enabled more fiscal space for the adoption of urgent measures. Revenue growth moderated last year due to lower economic growth, the easing of the tax burden on holiday allowance and a decline in property income, which until 2018 had been rising. Growth in expenditure on social benefits and transfers and on employee compensation, which had accounted for the bulk of the increase in total expenditure in 2015–2019, strengthened further in 2019 with the adoption of new measures. In 2018–2019 investment activity also rose more strongly. Last year total expenditure growth thus exceeded revenue growth for the first time since 2013. Interest payments dropped notably in the 2015–2019 period. At 1.7%, they were among the lowest in ten years.

Consolidated general government debt

The improvement in the general government balance in circumstances of high economic growth was reflected in a rapid decline in the general government debt as a share of GDP in the 2015–2019 period. The share of debt, which had increased strongly after the financial crisis and many years of general government deficits, fell by 16.5 pps to 66.1% of GDP between 2015 and 2019. The decline was larger than required in the Stability and Growth Pact. The share of debt also dropped notably in international comparison. Among EU Member States it was higher only in Ireland. In 2019 the debt-to-GDP ratio was around 20 pps lower than the euro area average. Its decline reflected the improvement in the primary balance, which has been in surplus since 2015; the contribution of economic growth was also favourable, but in 2019 it declined.