Charts of the Week

Current economic trends from 14 to 18 February 2022: labour market, construction, current account of the balance of payments and electricity consumption by consumption group

Labour market conditions remained favourable in December as employment reached new highs. In 2021 as a whole, the number of employed persons was 1.4% higher than in 2020 and 0.6% higher than in 2019. Due to the shortage of domestic labour, employment of foreign workers is increasing, especially of labourers in accommodation and food service activities, and in construction. Activity in construction was lower last year than a year earlier, mainly due to a sharp decline in the construction of non-residential buildings. However, VAT on an accrual basis in construction increased significantly in real terms last year, as did the number of employees. The current account surplus fell significantly last year, mainly due to the lower trade surplus as domestic demand recovered faster than foreign demand and the terms of trade deteriorated. The beginning of 2022 was marked by a new wave of infections. Industrial electricity consumption and small business electricity consumption were higher year-on-year in January and lower than in January 2020, most likely as a result of supply chain problems and increased staff absences caused by the rapid spread of the Omicron variant.

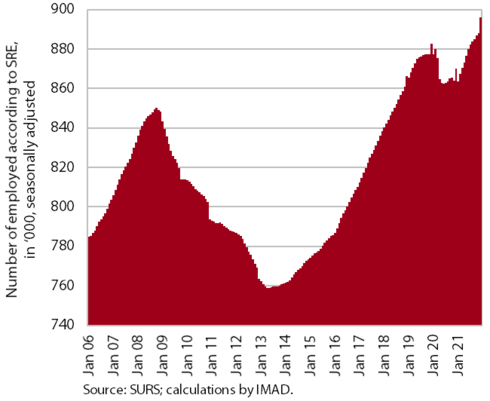

Labour market, December 2021

Employment continued to rise in December, reaching the highest level measured to date. The highest year-on-year increases at the end of last year were recorded in accommodation and food service activities and construction, with employment in the latter significantly higher than at the end of 2019, while employment in the former remained below the level of two years ago. Employment in manufacturing and administrative and support service activities was significantly lower than in December 2019. In 2021 as a whole, employment was 1.4% higher than in 2020 and 0.6% higher than in 2019. Amid the rapid economic recovery, employment growth is still largely dependent on the hiring of foreign workers (their contribution to total employment growth was almost 50% in December). Such high share of foreign workers is also related to the shortage of domestic labour, which is most pronounced in the accommodation and food service activities and in construction (both having a high job vacancy rate). The economic sectors with the highest share of employed foreign workers in 2021 as a whole were construction (43%), transportation and storage (31%), and administrative and support service activities (24%).

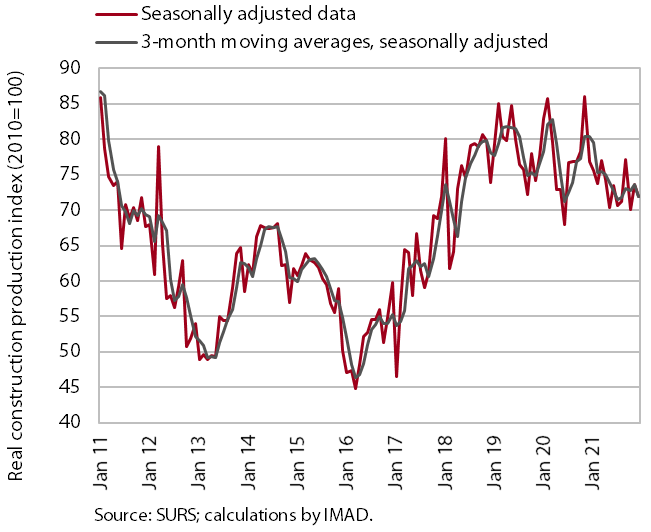

Construction, December 2021

According to figures on the value of construction work completed, activity in construction fell by 1.5% in the last quarter of 2021, while for the whole of 2021 it was 6% lower than the previous year. According to these data, construction activity fell sharply last year in non-residential construction (-37%), remained roughly unchanged in specialised construction, while it increased in civil engineering works and residential construction (by 4% and 15% respectively). Construction prices rose sharply last year under the pressure of rising commodity prices and labour shortages. The implicit deflator of the value of completed construction works (used to measure prices in the construction sector) was 13% in December 2021, the highest level in the last 20 years.

Some other data for 2021 show a better picture. According to data on VAT on an accrual basis, turnover in construction increased by 13% in real terms last year (taking into account the deflator for the value of completed construction works), and employment in construction rose by 4.4% on average, exceeding 70,000 in December for the first time in a decade. Confidence indicator in construction also improved significantly last year, reaching its highest level in 20 years.

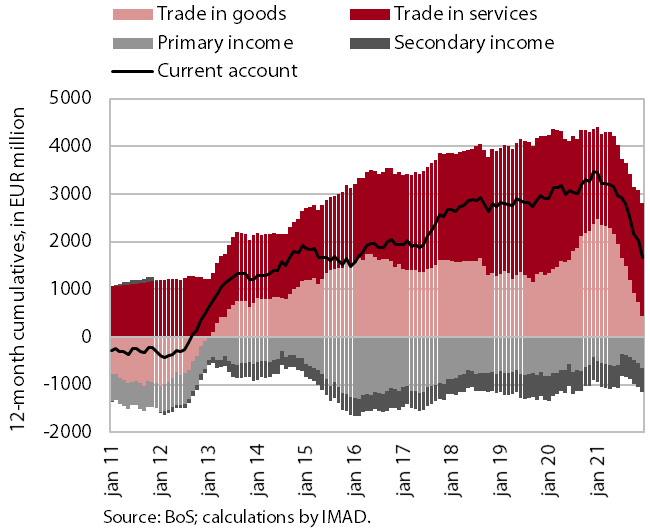

Current account of the balance of payments, December 2021

The current account surplus narrowed significantly in 2021 to EUR 1.7 billion (3.3% of GDP). Given the faster recovery in domestic demand than foreign demand and the deteriorating terms of trade, the lower current account surplus was largely due to a lower trade surplus. The surplus in services trade was higher, especially in trade in construction services and trade in higher value-added services (research and development services and telecommunications, computer and information services). Net outflows of primary income increased due to higher net outflows of income on equity (dividends and distributed profits) associated with a pick-up in economic activity at home and abroad. Net outflows of secondary income were also higher, mainly due to higher VAT- and GNI-based contributions to the EU budget. The narrowing of the savings/investment gap in the economy as a whole was mainly due to a decline in net household savings and an increase in net investment by non-financial corporations. However, the lower deficit in current transactions of the government sector was mainly due to a reduction in the general government deficit.

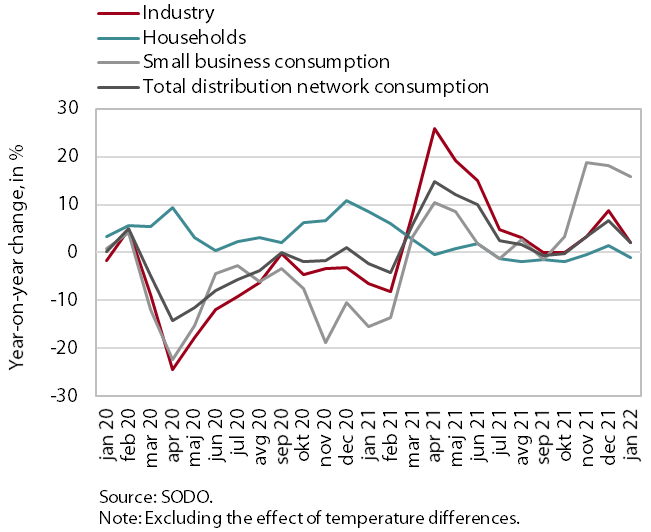

Electricity consumption by consumption group, January 2022

Industrial electricity consumption and small business electricity consumption were higher year-on-year in January and lower than in January 2020. Industrial electricity consumption was 2% higher year-on-year in January and small business electricity consumption was 15.8% higher. An important reason for the latter was last year's low base, as containment measures were in place last January, restricting mainly trade and services activities. Household consumption was slightly lower year-on-year in January (-1.4%). Compared to January 2020, industrial consumption was 4.7% lower and small business consumption was 2% lower. Lower business electricity consumption compared to the pre-epidemic period is most likely related to supply chain problems and increased staff absences due to the rapid spread of the Omicron variant. Household consumption was 7.4% higher in January than in January 2020 due to quarantine, isolation and work from home.