Charts of the Week

Current economic trends from 11 to 15 October 2021: electricity consumption by consumption group, construction, production volume in manufacturing, current account of the balance of payments and other data

Some indicators suggest that growth in the Slovenian economy slowed in the third quarter. After a sharp increase in the second quarter (2%), manufacturing output did not increase significantly on average in July and August compared to the previous quarter (0.5%), mainly due to disruptions in the supply of raw materials in the automotive industry. Industrial electricity consumption also points to a slowdown in growth. Construction activity fluctuates strongly on a monthly basis and remains below the comparable 2020 level, mainly due to unfavourable trends in non-residential construction.

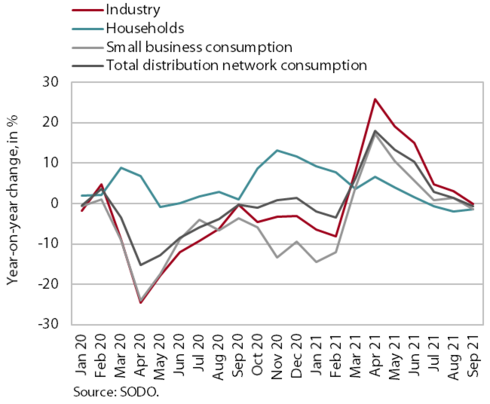

Electricity consumption by consumption group, September 2021

Industrial electricity consumption in September was similar to the same period in 2019 and 2020, while small business consumption lagged behind. Industrial electricity consumption, which had fallen in July and August (by 4.9% and 3.4% respectively) compared to the same periods of 2019, was again close to the level of the same period of 2019 in September, as was household consumption. Small business consumption, which has lagged behind the same period of 2019 since the start of the epidemic, fell by 4.9% in September (by 3.3% in July and by 5.3% in August). Compared to September last year, industrial consumption remained about the same, while small business and household consumption fell by 1.4%.

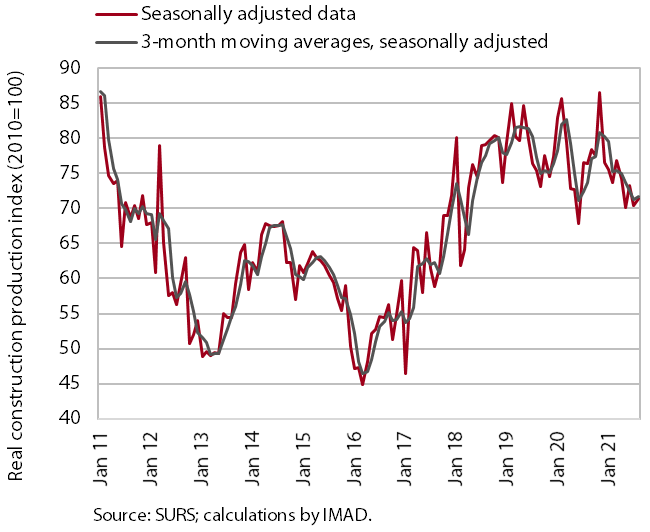

Construction, August 2021

Construction activity increased slightly in August but was still lower than a year ago. At the monthly level, the value of construction output increased by 1.4% but was down 6.8% year-on-year. Despite considerable monthly fluctuations, activity in civil engineering works and specialised construction remains at the levels reached at the beginning of the year, as does residential construction. However, activity in the non-residential construction is declining. The stock of contracts increased in the first half of the year and exceeded the previous year's level, while it fell sharply in August and was also lower year-on-year.

Construction prices continued to rise due to rising commodity prices and labour shortage. The implicit deflator of the value of completed construction works used to measure prices in the construction sector was 8% in August, its highest level since 2005.

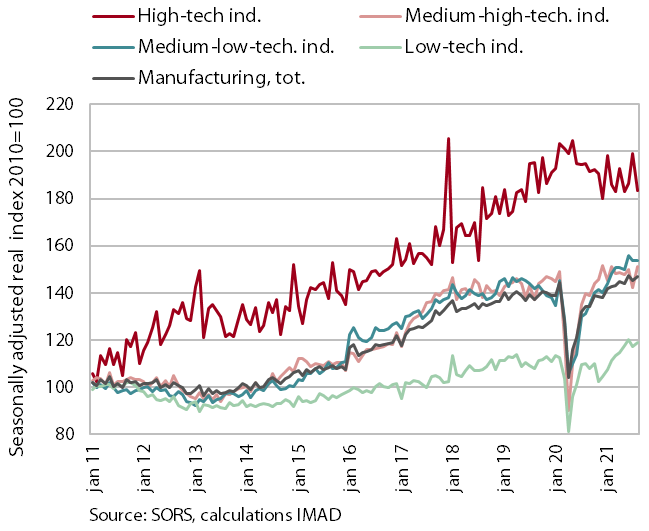

Production volume in manufacturing, August 2021

Manufacturing output has not changed significantly in recent months. Manufacturing production recorded significant year-on-year growth and was also higher than in the pre-epidemic period. Year-on-year growth was the highest in medium-low-technology industries, mainly underpinned by the manufacture of fabricated metal products. Growth was also high in medium-high-technology industries, which had declined the most in the first half of last year as the epidemic spread. Only the output of high-technology industries declined year-on-year, performing slightly worse than in the same period of 2019.

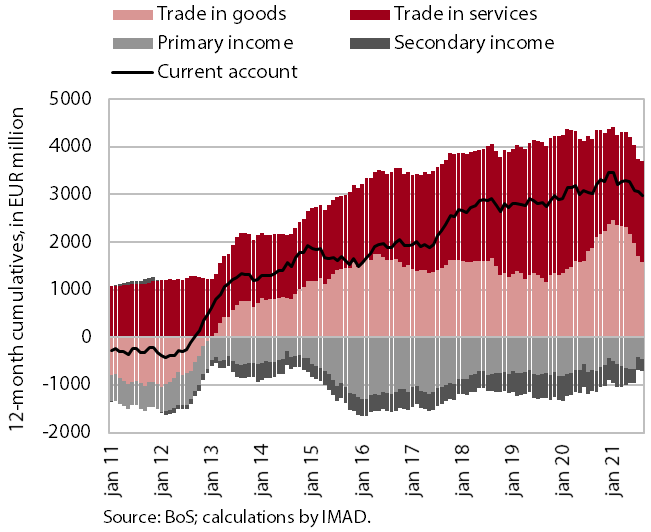

Current account of the balance of payments, August 2021

The current account surplus fell again in August. In the last 12 months, it totalled EUR 3 billion, which is 5.9% of GDP. The main reason for the year-on-year decline was the lower surplus in trade in goods under the impact of deteriorating terms of trade (higher increase in import than export prices). The surplus in trade in services also remained lower year-on-year, mainly due to a lower surplus in travel. The surplus in technical, trade-related services, R&D services and construction services continues to increase. The primary income deficit decreased year-on-year, mainly due to higher subsidies from the EU budget for the agricultural and fisheries policies. In primary income, net payments of interest on external debt and net payments of income on equity were also lower. The secondary income deficit was also lower as the government received more funds from the European Social Fund and inflows of current transfers from the private sector increased.

Road and rail freight transport – Q2 2021

The volume of road freight transport continued to increase in the second quarter of 2021 and was significantly higher than in the same period in 2019, while the volume of rail transport decreased slightly. Compared to the previous quarter, the volume of road transport performed by Slovenian road freight operators abroad increased by 4% and the volume of road transport performed at least partially on Slovenian territory (exports, imports and domestic transport combined) increased by 8%. Due to last year's low base, the volume of road transport increased by almost three tenths year-on-year. Rail freight transport was also higher year-on-year (by almost a tenth) but was down by a few percent compared to the same period in 2019.