Charts of the Week

Current economic trends from 10 to 14 October 2022: natural gas consumption, electricity consumption by consumption group, production volume in manufacturing and other charts

Manufacturing output rose in August. Only the manufacture of motor vehicles and production in less technology-intensive and generally more energy-intensive industries were lower than a year ago. In September, most companies expected production to decline until the end of the year. This is also indicated by electricity consumption, which was significantly lower in September than in the same period last year. Natural gas consumption has also decreased significantly in recent months (by about 15%) compared to the same period in the previous five years, which, as with electricity, is related to rising prices and lower energy consumption. According to data on the value of construction work put in place, construction activity in August was significantly higher than last year. Compared to previous years, the construction of buildings stands out, and activity in civil engineering is also high. Amid rising domestic consumption and deteriorated terms of trade, the current account surplus in the last 12 months was significantly lower year-on-year and a deficit of EUR 212.5 million was recorded in the first eight months of 2022.

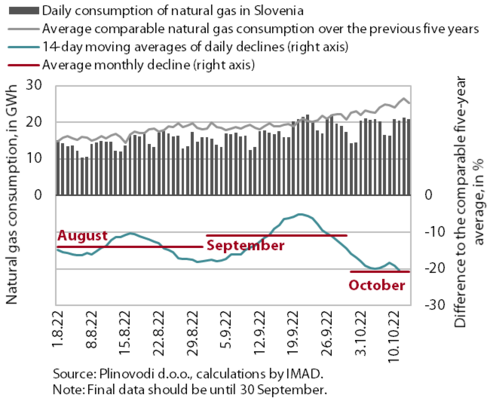

Natural gas consumption, August–September 2022

Natural gas consumption in August and September was lower than the comparable average consumption in the previous five years (by 14% and 11% respectively); according to available data consumption will be even lower in October. Compared to the previous five-year period, gas consumption has fallen by more than a tenth since the beginning of the year, which we associate with rising gas prices related to the energy crisis and lower consumption, especially in industry. Gas consumption usually increases significantly in October with the start of the heating season, and despite the government’s measure to limit the increase in gas prices, households are expected to use gas more rationally during the energy crisis. According to the Council Regulation, all Member States shall reduce their gas consumption in the period from 1 August 2022 to 31 March 2023 by at least 15% compared to their average gas consumption in the same period during the five preceding years. In Slovenia, consumption fell by 14.8% from the beginning of August this year to 18 October 2022, according to preliminary data.

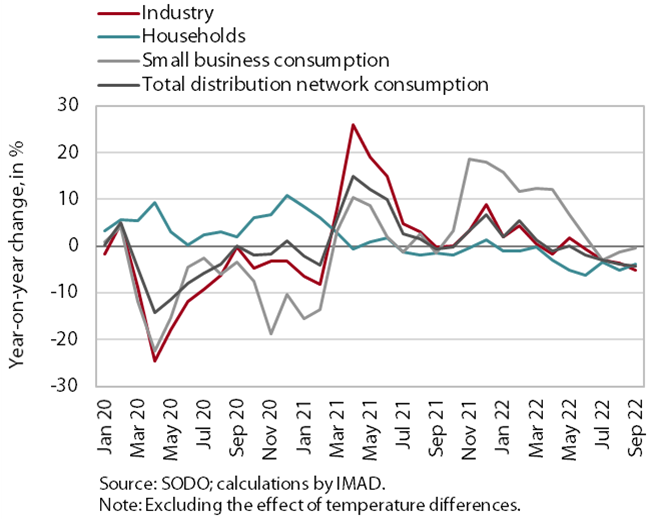

Electricity consumption by consumption group, September 2022

In September, electricity consumption in the distribution network was 4.4% lower year-on-year. The main reason for this was lower industrial consumption (-5.1%), which, according to our estimates, is mainly the consequence of lower consumption by some energy-intensive companies, which reduced their production volume due to the high electricity prices, but probably also improved their energy efficiency. Household consumption was also lower in September than a year ago (by -3.9%), while small business consumption remained about the same.

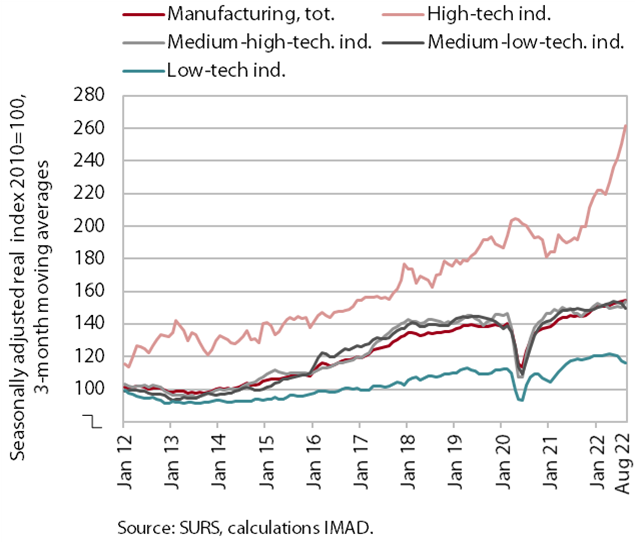

Production volume in manufacturing, August 2022

Manufacturing output increased in August. It continued to rise in high-technology industries and was also much higher in medium-high-technology industries. Manufacturing output in less technology intensive industries has mostly slowed since the middle of the year. In the first eight months of the year, manufacturing output was on average 6.2% higher year-on-year. It remained lower in the manufacture of motor vehicles (supply chain disruptions, "green" structural change) and in some less technology intensive industries (repair and installation of machinery and equipment, leather industry), including more energy-intensive industries (paper and rubber).

The outlook until the end of the year deteriorated further in September. Export expectations worsened, with most of the companies surveyed expecting a decline in production until the end of the year.

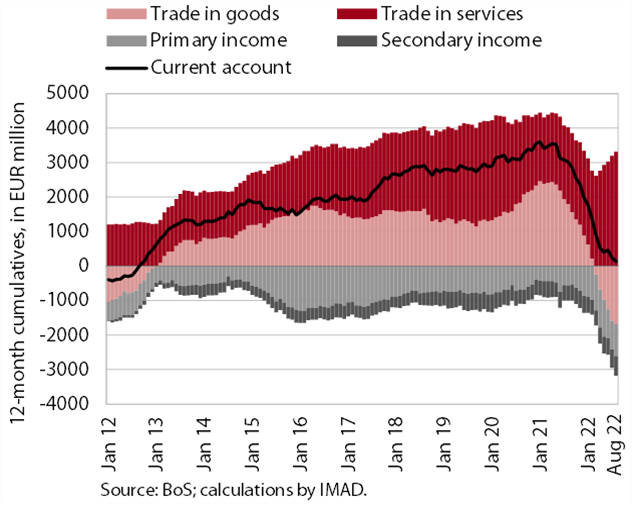

Current account of the balance of payments, August 2022

The current account surplus in the last 12 months was significantly lower year-on-year (EUR 137.3 million compared to EUR 3 billion) and a deficit of EUR 212.5 million was recorded in the first eight months of 2022. Lower surplus was mainly due to goods trade balance (the surplus turned into a deficit), as imports of goods grew faster than exports in the face of stronger domestic consumption and deteriorated terms of trade. Net outflows of primary and secondary income were also higher year-on-year. The primary income deficit was higher due to lower subsidies from the EU budget and more customs duties paid to the EU budget this year related to the import of electric vehicles for the entire EU market (Luka Koper). The higher secondary income deficit was arising from higher private sector transfers abroad. The services surplus increased, especially in trade in travel (easing of COVID-19 restrictions) and in trade in transport services related to the growth of international trade in goods.

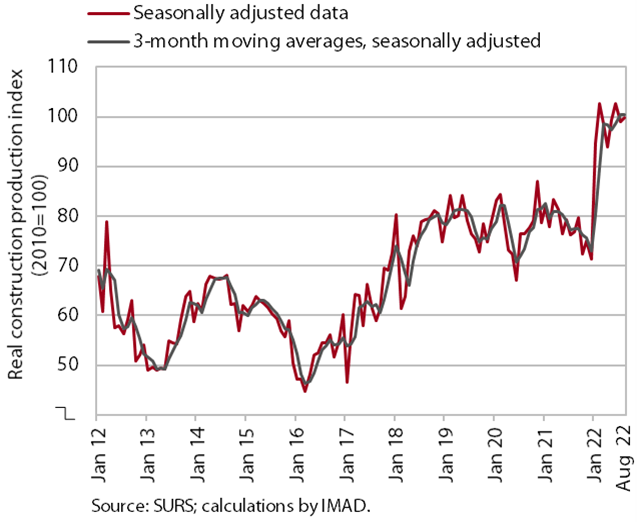

Activity in construction, August 2022

According to figures on the value of construction work put in place, construction activity in August was considerably higher than last year. After a strong upturn in activity at the beginning of this year, the value of construction work remained at this level during the rest of the year and was 30.2% higher in August than in the same month of 2021. Compared to previous years, construction of buildings stands out; activity was also high in civil engineering, while it was lower in specialised construction work (installation works and building completion). The implicit deflator of the value of completed construction works (used to measure prices in the construction sector) was 18% in August, which is slightly less than in previous months.

Some other data suggest a significantly lower construction activity. According to the data on VAT, the activity of construction companies in the first seven months was 7% higher than last year. Based on data on the value of construction put in place, the difference in the growth of activity was 17 p.p.

Road and rail freight transport – Q2 2022

The volume of road freight transport decreased significantly in the second quarter of 2022, while the volume of rail transport stagnated. The volume of road transport performed by Slovenian vehicles decreased significantly quarter-on-quarter and was only 2% higher than in the same quarter of 2019 (cross-trade was 10% lower and other road transport was 13% higher). The sharp quarter-on-quarter decline in the second quarter was more related to the decline in transport volume, which takes place at least partly in Slovenia (exports, imports and national transport combined). Nevertheless, the share of cross-trade transport performed by Slovenian vehicles in total transport remains much lower than in the same period before the epidemic (it decreased from 50% to 44%), while the share of foreign vehicle traffic on Slovenian motorways (according to DARS data) has not changed noticeably. Rail freight transport, already declining before the epidemic, was 2% lower than in the same quarter of 2019.