Charts of the Week

Charts of the week from 24 October to 4 November 2022: consumer prices, natural gas consumption, electricity consumption and other charts

The year-on-year consumer price inflation slowed slightly in October (to 9.9%), mainly due to a higher base of last year and also month-on-month lower oil derivatives prices. The year-on-year price increase of food and non-alcoholic beverages was 17.2%. In the period from the beginning of August to the beginning of November, gas consumption was about 17% lower than the comparable average consumption over the last five years, which is related to the measures taken to reduce gas consumption, the adjustment of industry to rising gas prices and the warmer than average weather in October. Mainly due to lower industrial consumption, electricity consumption in October was also significantly lower year-on-year. According to the seasonally adjusted data, the decline in the number of registered unemployed was similar to previous months, and the number of long-term unemployed also continued to fall. After a one-month interruption, turnover in market services increased again in August, supported by transportation and information and communication activities. Turnover in trade declined in September, but in the third quarter as a whole it remained similar to the second quarter in most trade sectors. The strengthening of the year-on-year growth in the nominal value of fiscally verified invoices in the second half of October has been largely influenced by the low base effect since mid-September. Trade in goods with EU Member States increased in the third quarter and was more favourable than expected given the situation in the international environment and deteriorating confidence indicators. In the face of high inflation, the average gross wage fell year-on-year again in real terms in August. The decline was more pronounced in the public sector due to the still present base effect of last year.

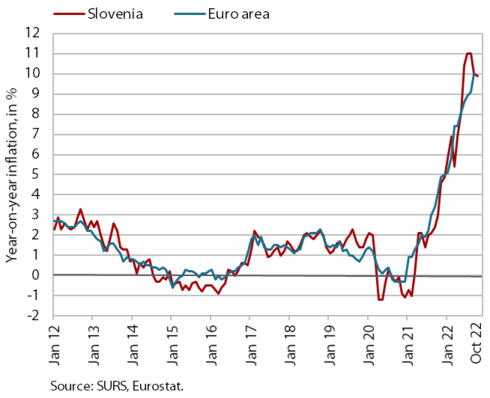

Consumer prices, October 2022

The year-on-year increase in consumer prices continued to slow slightly in October (to 9.9%). The increase in energy prices slowed further to 18.7% year-on-year, the lowest level in six months. Energy contributed 2.2 p.p. to year-on-year inflation. The slower growth was mainly the result of a higher base of last year and also the monthly decline in oil derivatives prices, which still largely exclude the 25 October price hike. In terms of energy prices, solid fuel prices continue to rise rapidly. In the last two months alone, they rose by more than 30%, and year-on-year they were up by almost 125%. The year-on-year increase in food and non-alcoholic beverage prices continued to strengthen in October, already reaching 17.2% (the highest in two decades) and contributing 2.8 p.p. to inflation. The monthly increase in food and non-alcoholic beverage prices was 2.5%, the second highest this year. Year-on-year growth in durable goods prices, which had been just over 10% since the end of the first half of the year, fell to 9.8% in October. The year-on-year increase in prices of semi-durable goods was still relatively subdued at 4%. Service prices rose by almost 6% year-on-year.

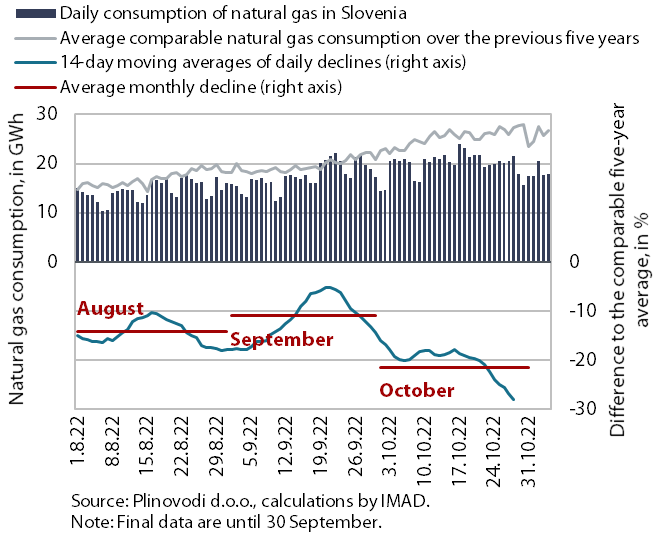

Natural gas consumption, August–October 2022

Natural gas consumption in August and September was below the comparable average consumption over the last five years (by 14% and 11% respectively), and based on available data, the decline in October is expected to be more than 20% as the weather was warmer than average. According to Eurostat, the average decline in gas consumption in EU Member States in August was the same as in Slovenia, and in September it was 15%. The decrease is driven by various measures taken by EU Member States to reduce gas consumption and adjustment of industry to rising prices of gas by reducing its consumption. The warm weather in October also contributed to lower consumption compared to previous years and helped to ensure that European gas storage facilities are almost full. According to preliminary data, gas consumption in Slovenia from 1 August to 4 November 2022 was about 17% lower than the comparable average consumption over the last five years.

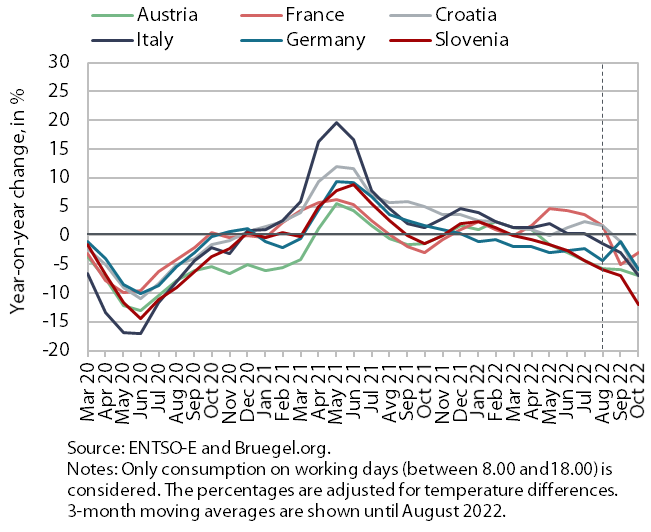

Electricity consumption, October 2022

Electricity consumption was 12% lower year-on-year in October. We estimate that this was mainly due to lower industrial consumption. This is related to a reduction in production activity, especially in some energy-intensive companies due to high energy prices, and to a more efficient energy consumption. Slovenia’s main trading partners also recorded a year-on-year decline in consumption in October (France by 3%, and Austria, Italy, Germany and Croatia by 7%).

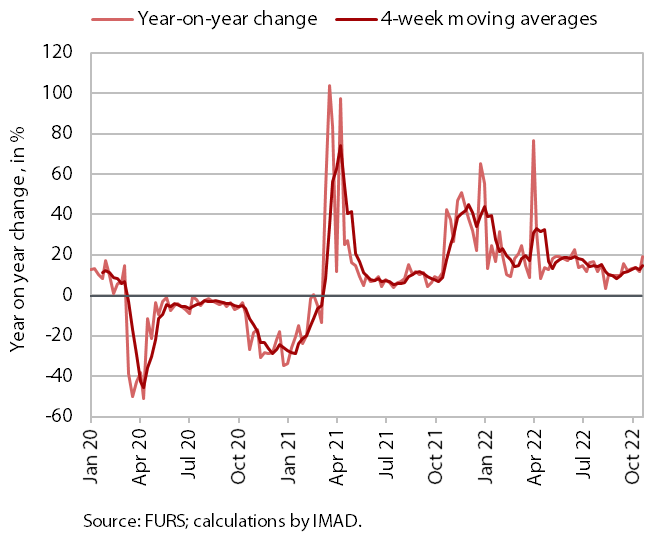

Value of fiscally verified invoices, in nominal terms, 16–29 October 2022

Amid high price growth, the value of fiscally verified invoices between 16 and 29 October 2022 was 16% higher year-on-year in nominal terms and 23% higher than in the same period of 2019. Year-on-year growth, which has strengthened since mid-September mainly due to last year’s lower base (in mid-September last year, the recovered/vaccinated/tested rule was extended to users of most services), was slightly higher than in the previous two weeks. This was mainly due to a stronger nominal growth in trade (16%), where turnover growth was higher in all three main sectors (retail, wholesale, motor vehicles). After rising in recent weeks, year-on-year growth of turnover in accommodation and food service activities more than halved (to 9%), due to more than a tenth lower turnover in accommodation establishments, partly as a result of the redemption of vouchers in October last year. Turnover in food and beverage service activities was up by a fifth.

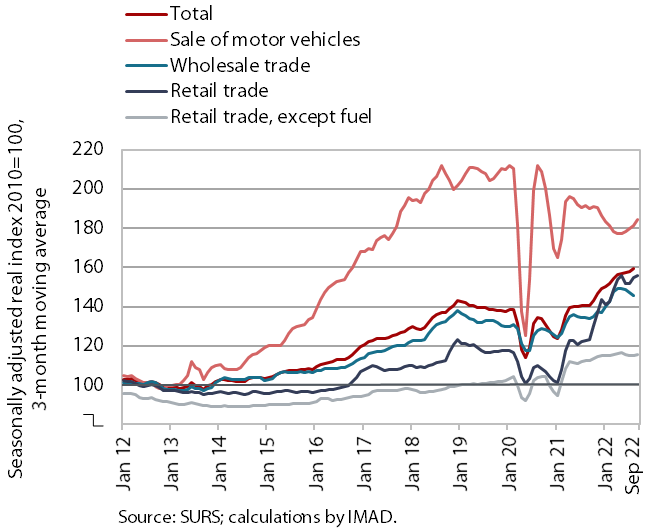

Turnover in trade, August–September 2022

According to preliminary data, turnover in trade declined in September after growth in August, but in the third quarter as a whole it remained similar to the second quarter in most sectors. The exception was turnover in wholesale trade, which recorded a significant drop, and turnover in the sale of motor vehicles, which increased significantly. Despite the increase, this was the only major trade segment to fall far short of pre-epidemic turnover; turnover was also lower than in the third quarter last year. In the third quarter, turnover in retail sales of food, beverages and tobacco products also remained lower year-on-year. In other sectors, year-on-year turnover growth continued to weaken.

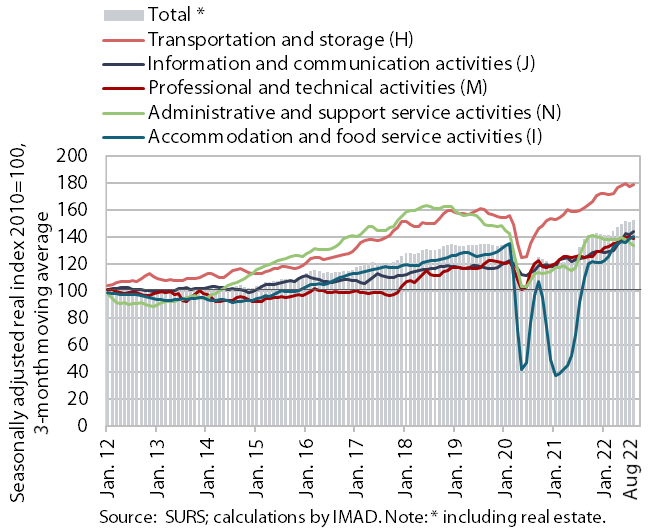

Turnover in market services, August 2022

After falling in July, real turnover in market services rose again in August, by 3.2% in current terms and by 7.8% year-on-year. After several months of decline, turnover in transportation, especially in storage, rose strongly again in current terms. Turnover also rose again in information and communication activities, with all services contributing to growth. Turnover continued to decline in administrative and support service activities, mainly due to its significant drop in travel agency activities. With the decline in current terms of overnight stays by domestic and foreign tourists, turnover in accommodation and food service activities also fell slightly. Turnover in professional and technical activities declined again, due to a decrease in consultancy activities.

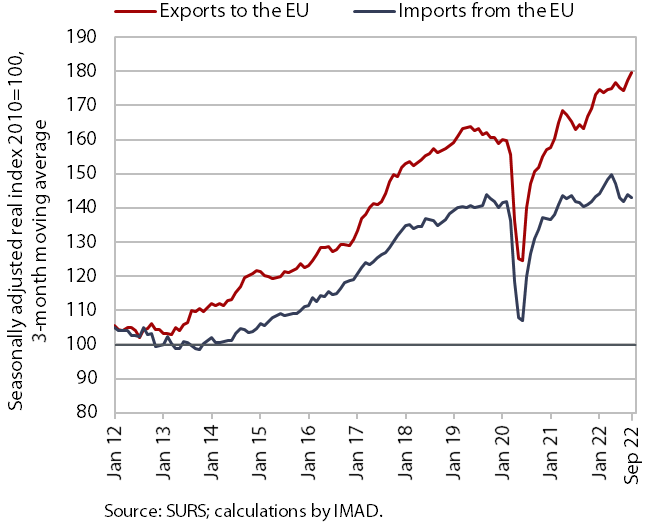

Trade in goods – in real terms, September 2022

Trade with EU Member States increased quarter-on-quarter in the third quarter; sentiment in export-oriented sectors deteriorated further in October. Amid considerable monthly fluctuations, real exports of goods to EU Member States rose by 2.6% compared to the previous quarter, while real imports of goods from EU Member States remained at the level reached (seasonally adjusted). Year-on-year growth in trade with EU Member States remained high in the third quarter (exports 8.5%, imports 0.5%). The high level of uncertainty in the international environment has had a significant impact on sentiment in export-oriented activities in recent months, as export orders continued to decline in October, reaching the lowest level since the end of 2020. According to the survey data, companies expect their competitive position in EU and non-EU markets to deteriorate in the last quarter and the volume of new orders to decline further.

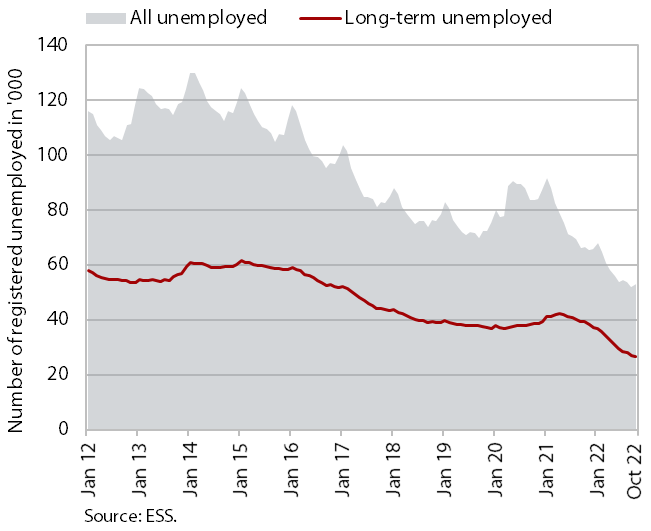

Number of registered unemployed persons, October 2022

According to seasonally adjusted data, the decline in the number of registered unemployed was similar as in previous months (-1.2%). According to original data, 52,991 persons were unemployed at the end of October, which is 1.8% more than at the end of September. This is mainly due to seasonal trends related to a higher inflow of first-time job seekers into unemployment. Year-on-year, unemployment was down 20.5%. Under conditions of high demand for labour, which is also reflected in the high vacancy rate, the number of long-term unemployed has also been declining since May last year – their number was almost a third lower year-on-year in October. The number of unemployed people over 50, who, like the long-term unemployed, are harder-to-place, is also declining – in October, their number was a good fifth lower than a year ago.

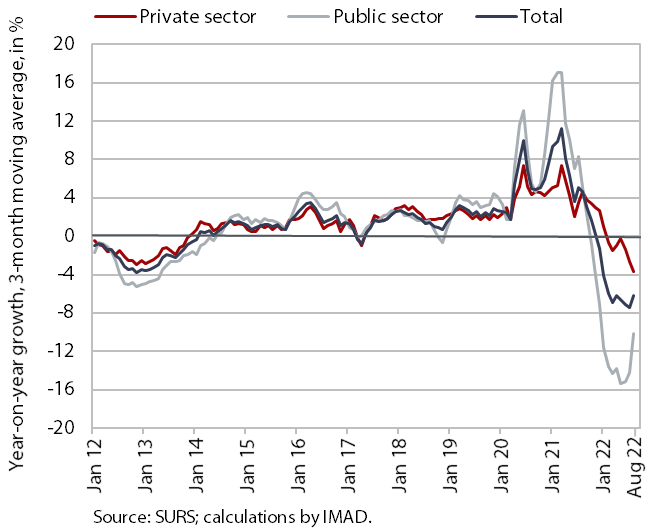

Average gross wage per employee, August 2022

Amid high inflation, the average gross wage fell by 4.8% year-on-year in real terms in August; due to the base effect of last year, the decline was more pronounced in the public sector (-7.2%) than in the private sector (-3.4%). In the private sector, the year-on-year decline was somewhat smaller in real terms than in July, but stronger than in other months this year. In the public sector, however, the year-on-year decline in real terms was smaller than in previous months, which is related to the year-on-year effect of the cessation of payment of most COVID-19 bonuses in July last year.