Charts of the Week

Charts of the week from 20 to 24 March 2023: economic sentiment, value of fiscally verified invoices, slovenian industrial producer prices and other charts

In March, the value of the economic sentiment indicator remained similar to that in February, while it was lower year-on-year. Confidence deteriorated month-on-month and year-on-year in retail trade, construction and manufacturing, while it improved in services and among consumers. In the first half of March, the year-on-year turnover growth more than halved according to the nominal value of fiscally verified invoices, mainly due to the high base from last year, with growth in trade declining significantly. The year-on-year growth of Slovenian industrial producer prices slowed to 14.9% in February. This was entirely due to the high base from last year, as prices increased significantly month-on-month (by 1.5%). In January, the average gross wage was 1.3% higher year-on-year in real terms, mainly due to a considerable increase in the minimum wage at the beginning of the year and a relatively low base from last year. The growth of dwelling prices moderated in Q4 2022 amid a further decline in turnover, but remained high year-on-year, especially of existing dwellings.

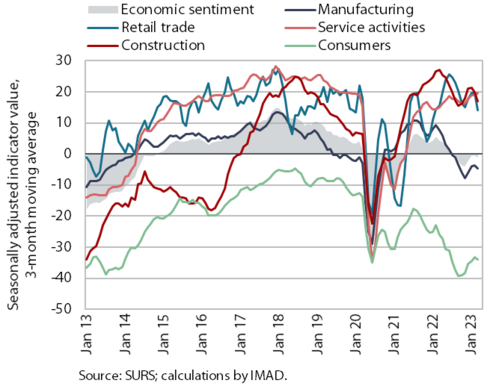

Economic sentiment, March 2023

In March, the value of the economic sentiment indicator remained similar to that in February (-0.3 p.p.), while it fell by 2.7 p.p. year-on-year. Compared to the previous month, confidence fell in retail trade, construction and manufacturing, while it rose slightly in services and among consumers. According to the original data, the same confidence indicators deteriorated year-on-year and month-on-month, while confidence improved in services and among consumers. The rise in consumer confidence was driven by more optimistic expectations about the country’s economic situation and the financial situation of households, while service providers assessed their business situation improved and expected higher demand. The economic climate improved in the first quarter compared to the last quarter of last year, but deteriorated compared to the same quarter of 2022.

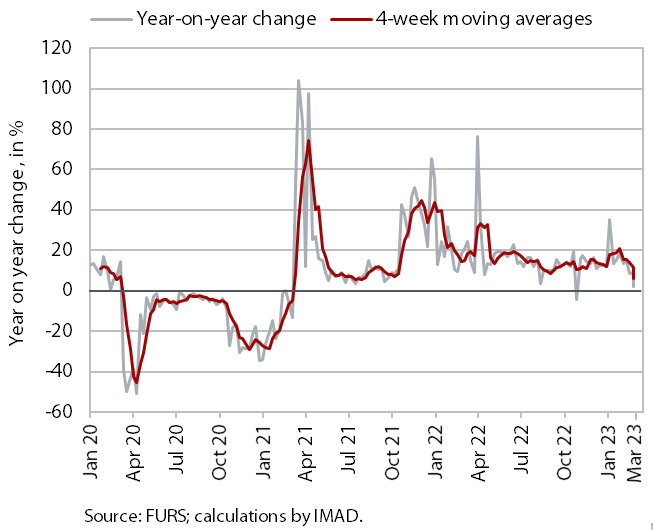

Value of fiscally verified invoices, in nominal terms, 5–18 March 2023

Amid high price growth and high base from last year, the nominal value of fiscally verified invoices between 5 and 18 March 2023 was 3% higher year-on-year. Year-on-year turnover growth more than halved due to the high base, with a particularly marked decline in trade (from 9% to 2%). Turnover in retail trade, which accounted for almost half of the total value of fiscally verified invoices, was similar to last year in nominal terms; the value of the sale of automotive fuels fell by a fifth year-on-year. The value of turnover in wholesale trade also declined year-on-year, while sales of motor vehicles increased by 17%. Turnover growth in accommodation and food service activities, certain creative, arts, entertainment and sports activities, and gambling and betting activities remained similar to the previous 14-day period (between 10% and 15%), when it more than halved due to a changed base.

Slovenian industrial producer prices, February 2023

The year-on-year growth of Slovenian industrial producer prices slowed further in February, falling to 14.9%, the lowest level since January 2022. The slowdown was entirely due to the high base from last year, as prices increased significantly (by 1.5%) compared to the previous month. They rose in all industrial groups, with only prices of durable consumer goods declining (by 2.2%). Price growth slowed year-on-year in both domestic (18.6%) and foreign markets (11.2%). Growth of intermediate goods prices slowed further (13.1%), while growth of capital goods (9.1%) and consumer goods (14.2%) prices remained broadly unchanged. Domestic energy prices, which rose by almost 15% month-on-month (while they remained unchanged in foreign markets due to stable conditions), were still significantly higher year-on-year (49.7%).

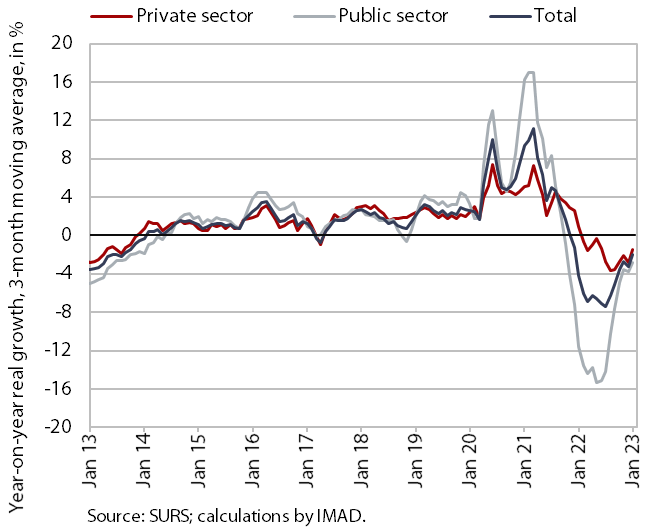

Average gross wage per employee, January 2023

Despite high inflation, the average gross wage increased by 1.3% year-on-year in real terms in January. This was mainly due to the sharp increase in the minimum wage at the beginning of the year and the relatively low base from January 2022. In the private sector, the average gross wage was up 2.2% year-on-year in real terms. Growth was strongest in accommodation and food service activities, which is facing a major labour shortage. In the public sector, gross wages fell by 0.1% year-on-year in real terms, which is a much smaller decline than in previous months. Compared to January last year, the average gross wage increased by 11.5% in nominal terms – by 9.9% in the public sector and by 12.4% in the private sector.

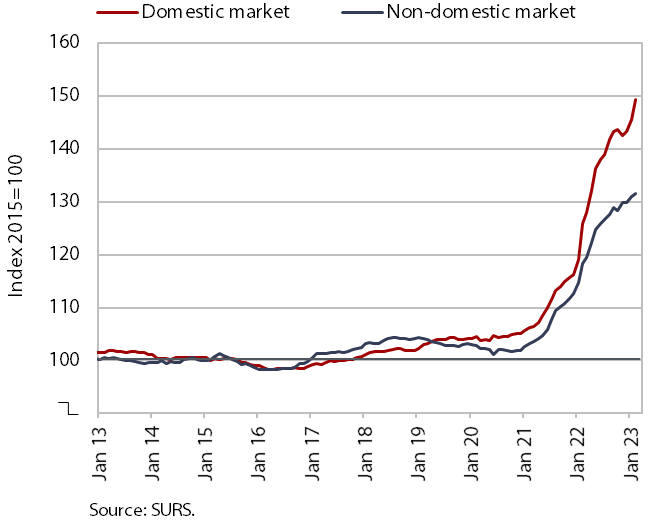

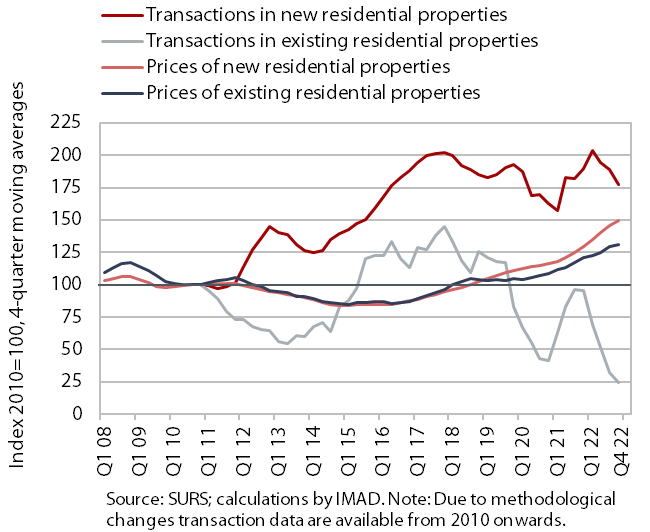

Residential real estate – Q4 2022

The growth of dwelling prices moderated in Q4 2022 amid a further decline in the number of transactions, but remained high year-on-year. Prices were 1% higher than in Q3 2022 and 11.3% higher than in Q4 2021. The still high year-on-year growth was mainly due to higher prices of existing dwellings (by 12%), where the number of transactions was almost a quarter lower year-on-year. Prices of newly built dwellings were also higher (by 5.1%), but these dwellings accounted for only 2% of all transactions. After an increase of 11.5% in 2021, prices rose by 14.7% year-on-year in 2022 as a whole. They were 34.3% higher in nominal terms than in 2008, with prices of existing dwellings rising by 41.1% (by 38.1% in Ljubljana and by 59.9% elsewhere) and prices of newly built dwellings by 11.8%.