Charts of the Week

Charts of the week from 14 to 18 November 2022: gross domestic product, natural gas consumption, electricity consumption by consumption group and other charts

In the third quarter, GDP fell compared to the second quarter (by 1.4%) and year-on-year growth (3.4%, not seasonally adjusted) was lower than in the first half of the year. After a deficit in the first half of the year, the current account returned to surplus in the third quarter. The terms of trade deteriorated for the seventh consecutive quarter. Uncertainty regarding the availability and prices of energy remains high. At the same time, the consumption of natural gas in Slovenia (and in the EU) has decreased significantly in recent months. This was due to favourable weather conditions and measures to reduce gas consumption and adjust production. Electricity consumption in the distribution network was lower year-on-year in October in all consumption groups. According to data on fiscal verification of invoices, turnover in the first half of November was 6% higher year-on-year in nominal terms, with growth slowing in recent weeks. Amid record employment, the rise in the number of people in employment slowed somewhat in September. It remained high especially in construction, which is characterised by a high share of foreign workers and a large labour shortage.

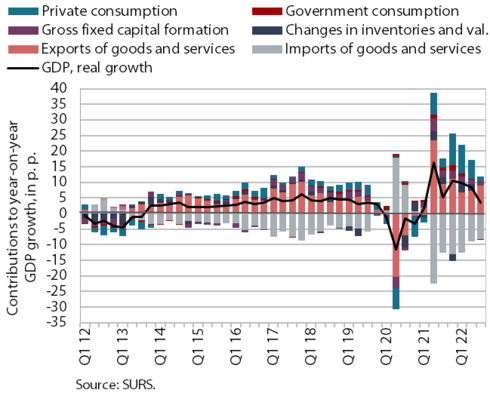

Gross domestic product, Q3 2022

In the third quarter, GDP fell by 1.4% compared to the second quarter, and the year-on-year growth (3.4%) was lower than in the first half of the year and in line with IMAD’s expectations in its Autumn Forecast. Household expenditure growth moderated to 2.6% year-on-year in the summer months as consumer confidence fell and real income declined. Growth was underpinned by the sale of non-food products and services. Investment remained strong in the third quarter, especially in construction. The deterioration in export expectations has not yet had a more pronounced impact on the growth of goods exports, where steady growth continued in the third quarter. This segment has been subject to strong monthly fluctuations since the spring, which are related to the great uncertainty in the international environment. Growth in trade in services also continued, albeit at a somewhat slower pace. The overall growth of exports exceeded the growth of imports, which contributed to a positive external trade balance. General government consumption declined year-on-year after a period of increased growth, with lower expenditure on containment measures and lower state budget expenditure on certain types of goods and services. The contribution from the change in inventories, after high positive values in the first half of the year, was neutral in the third quarter compared to the same period last year.

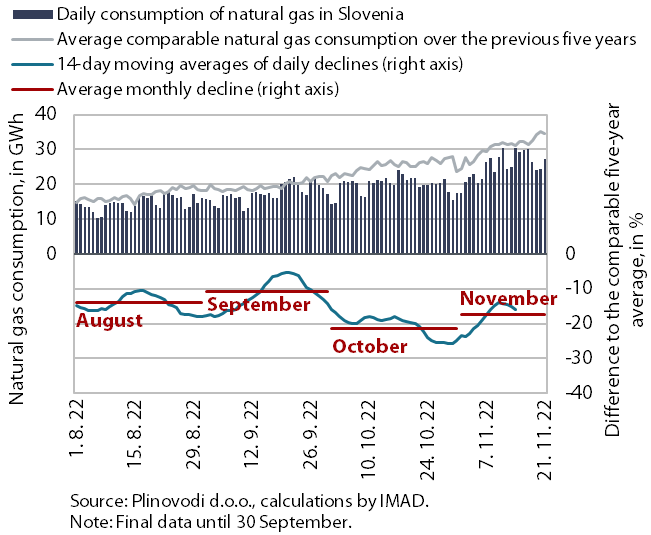

Natural gas consumption, August–November 2022

Natural gas consumption in August and September was below the comparable average consumption of the last five years (by 14% and 11% respectively), while the decline in October (22%) and November was even more pronounced due to this year’s warm autumn. According to Eurostat, the average decline in gas consumption in EU Member States in August was the same as in Slovenia, and in September it was slightly higher (13%). Lower consumption is underpinned by various measures taken by EU Member States to reduce gas consumption and by adaptation of various industries to rising prices of gas by reducing its consumption. The warmer-than-average weather in the last two months has also contributed to lower consumption and to the fact that European gas storage capacities were almost completely filled during this period. According to preliminary data, gas consumption in Slovenia from 1 August to 21 November 2022 (including the announced consumption for the last few days) was more than 16% lower than the comparable average consumption over the last five years.

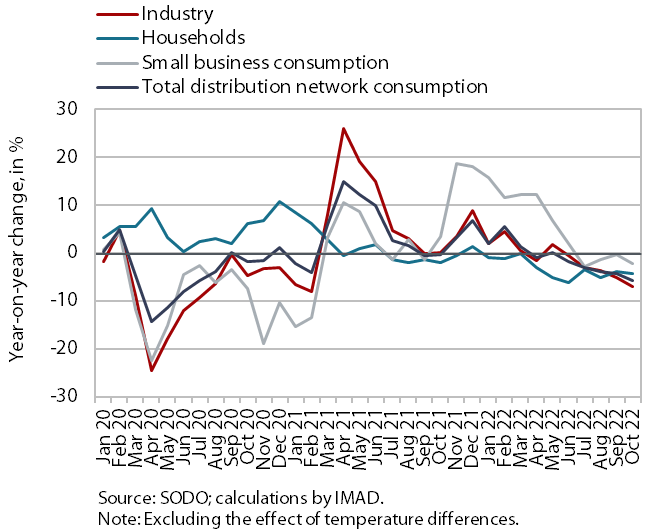

Electricity consumption by consumption group, October 2022

In October, electricity consumption in the distribution network was lower year-on-year in all consumption groups. The strongest decrease was in industrial consumption (by 7.1%). This is mainly due to the lower consumption by some energy-intensive companies, which reduced their production volume due to high electricity prices, but were also able to reorganise their production processes and introduce more modern technologies, which made them more energy efficient. Due to a more rational use of energy, household consumption and small business consumption were also lower year-on-year in October (by 4.3% and 2.2% respectively).

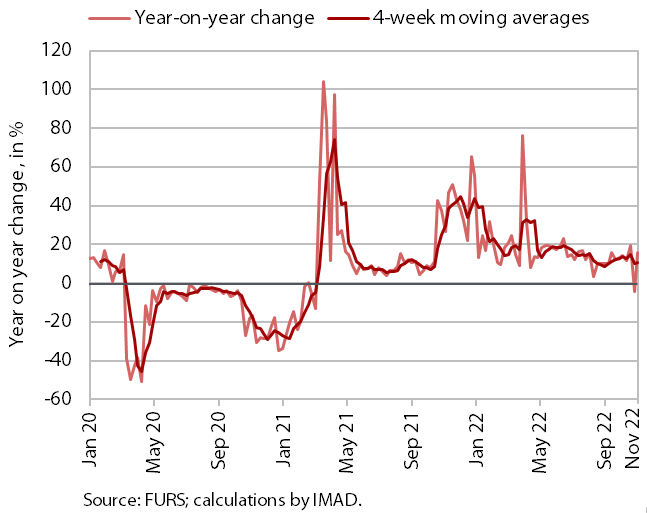

Value of fiscally verified invoices, in nominal terms, 30 October–12 November 2022

The value of fiscally verified invoices between 30 October and 12 November 2022, which was marked by high price growth and had one less working day compared to the same period last year, was 6% higher year-on-year in nominal terms and 12% higher than in the same period of 2019. Year-on-year growth, which has strengthened since mid-September mainly due to last year’s lower base, has more than halved in the last two weeks. This was mainly due to the timing of public holidays and one fewer working day this year, which was reflected in particular in lower nominal growth in turnover in trade, which accounted for slightly more than three quarters of the total value of fiscally verified invoices. Nominal growth of turnover in accommodation and food service activities strengthened significantly (to 23%), due to more than a tenth higher year-on-year turnover in accommodation establishments and the 29% increase in year-on-year turnover in the service of food and beverages due to stricter COVID-19 restrictions in the same period last year (recovered/vaccinated/tested rule).

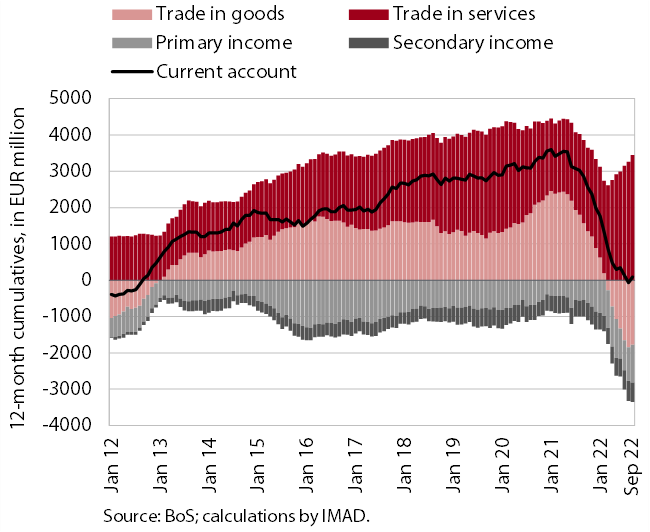

Current account of the balance of payments, September 2022

After a deficit in the first half of the year, the current account balance recorded a surplus again in the third quarter; the terms of trade deteriorated for the seventh consecutive quarter. The surplus amounted to EUR 304.7 million and was significantly lower compared to the same quarter last year (EUR 559.5 million). This was mainly due to trade in goods, as the real increase in imports of goods was higher than that in exports, given the deteriorating terms of trade. The terms of trade deteriorated year-on-year in the third quarter by 1.9%, which is less than in previous quarters, and contributed about one fifth to the change in the nominal trade balance (by EUR 443 million). The services surplus was higher than a year ago, especially in travel and transportation services. Net outflows of primary and secondary income were higher than a year ago. The primary income deficit was higher year-on-year in the third quarter due to larger payments of income on equity, direct investments and more customs duties paid to the EU budget due to the import of electric vehicles for the EU market (via the port of Koper), while the secondary income deficit was due to higher private sector transfers abroad. In the first nine months of this year, the current account was close to a balance (deficit of EUR 4 million).

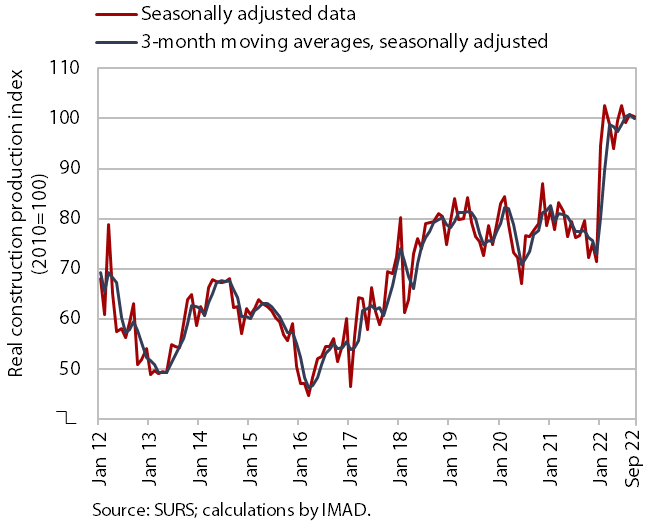

Activity in construction, September 2022

According to figures on the value of construction work put in place, construction activity in September was considerably higher year-on-year. After a strong upturn at the beginning of the year, the value of construction work remained at a high level during the rest of the year and was 26.1% higher in September than a year ago. Compared to previous years, construction of buildings stands out; activity was also high in civil engineering, while it was lower in specialised construction work (installation works and building completion). The implicit deflator of the value of completed construction works (used to measure prices in the construction sector) was 18% in September, which is slightly less than in previous months.

However, data on VAT suggest a significantly lower construction activity. According to these data, the activity of construction companies in the first nine months was 6% higher than last year. Based on data on the value of construction put in place, the difference in the growth of activity was 20 p.p.

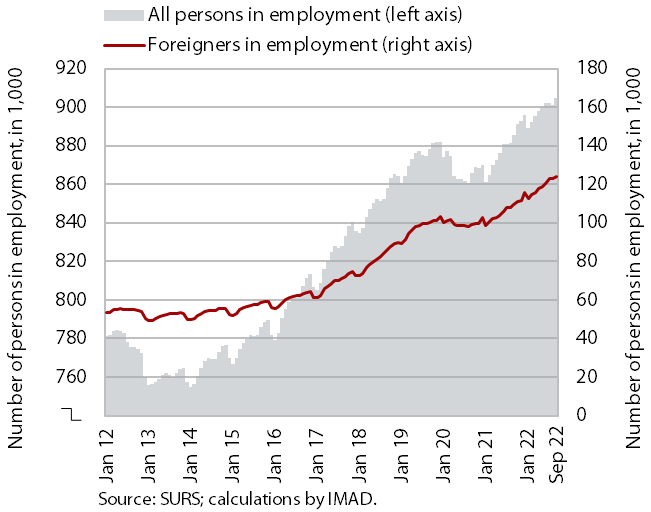

Number of persons in employment, September 2022

As the number of people in employment reached record high, year-on-year growth in September was 2.2%, slightly lower than in previous months. It remained high in construction, which faces major labour shortages. Employment of foreign workers has recently been increasingly contributing to overall growth in the number of people in employment – in September, foreign workers contributed 76% to year-on-year employment growth. Consequently, the share of foreign nationals among all persons in employment is also increasing, up 1.4 p.p. to 13.7% in the last year. Activities with the largest share of foreign workers are construction (47%), transportation and storage (32%) and administrative and support service activities (26%). In the first nine months, the number of people in employment rose by an average of 2.7% year-on-year.