Charts of the Week

Charts of the week from 13 to 17 March 2023: activity in construction, number of persons in employment, current account of the balance of payments and other charts

Construction activity continued to increase in January and was 27% higher year-on-year, with the construction of residential buildings in particular standing out compared to previous years. The construction sector recorded strong year-on-year growth in the number of persons in employment in January, the highest of all activities. Year-on-year, total employment grew at a similar rate to previous months (1.9%), again mainly due to the employment of foreigners. Gas consumption in the first half of March was about 13% lower than the average consumption in the same period in the last five years. The slightly wider gap with the average consumption is related to milder weather. Between August last year and January this year, gas consumption fell by 14% compared to same period in the last five years, and by a fifth in the EU. Electricity consumption was down in all consumer groups in February, most markedly in industry. The current account balance showed a deficit of EUR 218.9 million in the last 12 months, mainly due to the goods trade balance.

Activity in construction, January 2023

According to data on the value of construction work put in place, construction activity in January further increased. After a sharp upturn at the beginning of 2022, the value of construction work remained roughly unchanged throughout the year before rising sharply towards the end of last year and the beginning of this year. In January, it was 27% higher year-on-year. Compared to previous years, construction of buildings stood out in terms of the level of activity. The implicit deflator of the value of construction work put in place used to measure prices in the construction sector was 12% in January, which was slightly below the 2022 average.

However, some other data suggest significantly lower construction activity. According to VAT data, the activity of construction companies in January was 10% higher than last year. Based on data on the value of construction put in place, the difference in the activity growth was 17 p.p. Data on the value of industrial production in two activities traditionally strongly linked to construction also do not point to such high growth. Production in other mining and quarrying was 1% lower in January than in the same month of 2022, while it was 3 % lower in the manufacture of other non-metallic mineral products.

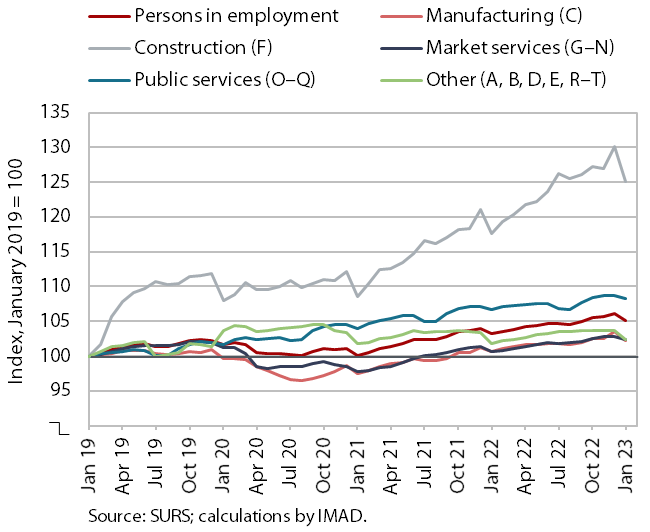

Number of persons in employment, January 2023

In January, year-on-year growth in the number of persons in employment was similar to the previous months (1.9%). The strongest growth was seen in construction, which is facing a major labour shortage and saw the largest increase in the number of persons in employment compared to the same period in 2019. Employment of foreign workers has been the largest contributor to the overall growth in the number of persons in employment for quite some time – its contribution was 78% year-on-year in January, which is slightly more than in the previous months. Foreigners accounted for 14% of total employment, up 1.3 p.p. from the previous year. The sectors with the highest share of foreigners were construction (47%), transportation and storage (32%), and administrative and support service activities (26%), in the latter due the employment of foreigners by employment agencies.

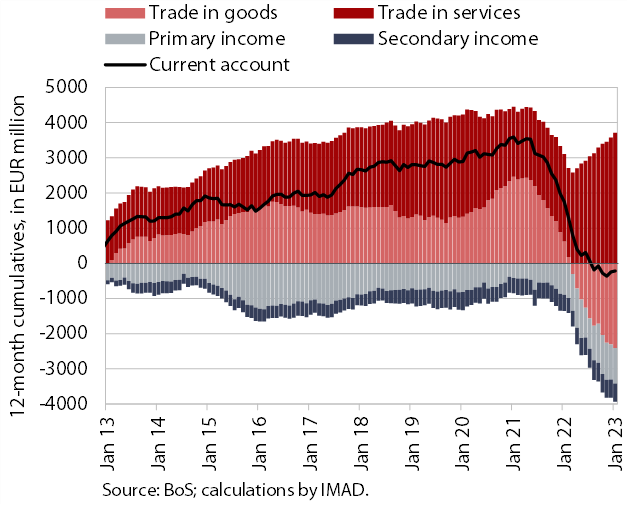

Current account of the balance of payments, January 2023

The current account of the balance of payments in the last 12 months recorded a deficit of EUR 218.9 million, compared to a surplus of EUR 1.7 billion in the same period a year earlier. Lower surplus and change to a deficit was mainly due to goods trade balance (the annual deficit in goods balance has increased since March last year), as imports of goods grew faster than exports. Net outflows of primary and secondary income increased. The primary income deficit increased year-on-year, mainly due to lower subsidies from the EU budget for the agricultural and fisheries policies and more customs duties paid into the EU budget, while the secondary income deficit was due to lower government revenue from abroad. The surplus in trade in services continued to increase, especially in trade in travel and transportation services.

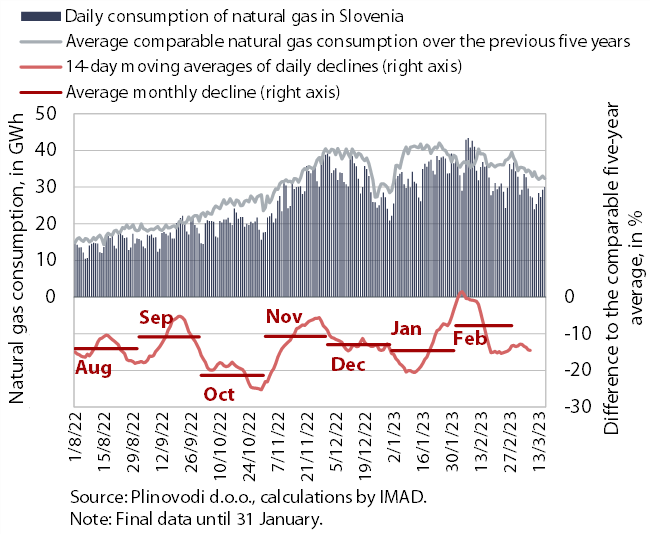

Natural gas consumption, March 2023

Gas consumption in the first half of March was about 13% below the average consumption in the same period in the last five years. Lower gas consumption was due to lower production in some industries as a result of high gas prices and government measures to encourage more rational consumption, while mild weather also widened the gap with average gas consumption compared to February. According to the preliminary data, gas consumption also decreased by 13% in the period from 1 August 2022 to 16 March 2023 compared to the comparable average of the previous five years. By 31 March (entire reduction period according to the EU Regulation), the reduction in consumption is likely to be only slightly below the EU recommendation to reduce gas consumption by at least 15%. Gas consumption in Slovenia between August last year and January this year was 14% lower than in the same period of the previous five years, while in the EU as a whole it was one-fifth lower.

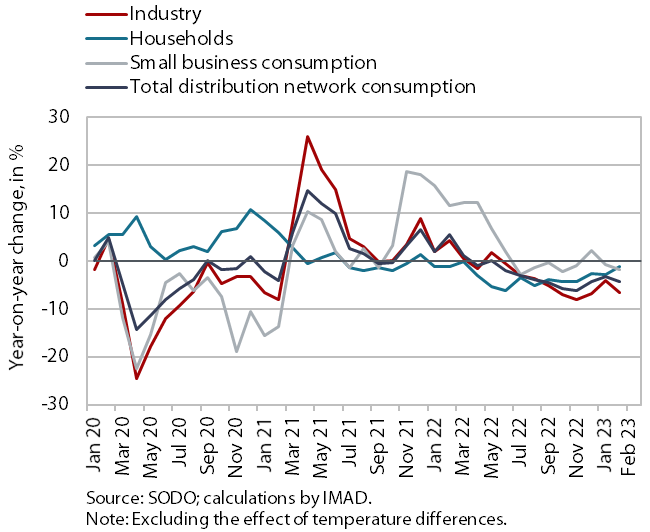

Electricity consumption by consumption group, February 2023

Electricity consumption in the distribution network was lower year-on-year in February in all consumption groups. The largest decrease was seen in industrial consumption (by 6.7%), according to our estimates due to lower consumption by the energy-intensive part of the economy as a result of high electricity prices. Household consumption was also lower year-on-year in February (by 1.1%). We estimate that this is due to more rational use of energy and also because fewer people stayed at home than in the same period last year, when the number of COVID-19 infections increased and containment measures were in place. Small business consumption was also slightly lower year-on-year in February (by 1.8%).