Slovenian Economic Mirror

Slovenian Economic Mirror 4/2018

Economic growth in the euro area slowed in the first quarter; owing to uncertainties in the international environment, prospects are less optimistic than in the autumn. Economic growth in Slovenia also eased at the beginning of the year, largely on account of slower growth in foreign demand and unfavourable weather impacts on construction. The labour market situation continues to improve. Inflation has increased in the last two months. Growth in loans to domestic non-banking sectors remains low. The general government balance on a cash basis was positive in the first four months.

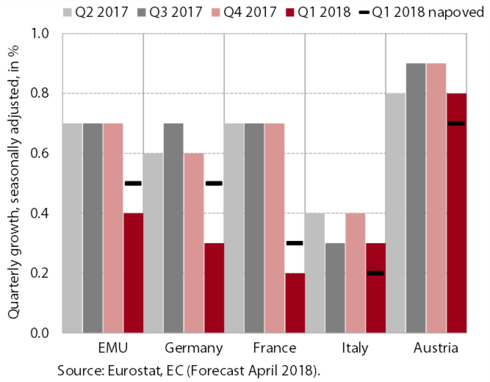

Economic growth in the euro area eased in the first quarter. GDP rose by 0.4% (seasonally adjusted, 0.4% in the EU) and was 2.5% higher year on year (2.4% in the EU). The moderation of quarterly growth was significantly affected by foreign demand, as the volume of euro area exports fell relative to the previous quarter. The main factor of GDP growth remained domestic consumption, where growth continued primarily in private consumption and investment. Among Slovenia’s main trading partners, GDP growth slowed the most in Germany and France, while in Italy and Austria it remained similar to previous quarters.

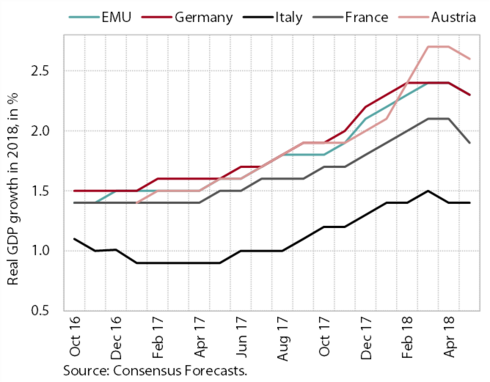

The prospects for euro area growth are less optimistic than early in the year. Following a considerable fall in the first three months, the values of business confidence indicators (ESI, PMI) declined further at the beginning of the second quarter. Business confidence was mainly affected by increased uncertainties internationally, especially the announcement (and introduction) of some anti-trade measures by the US and the elevated geopolitical risks in the Middle East. This showed particularly in the lowering of Consensus forecasts for 2018 GDP growth in Slovenia’s trading partners in the euro area (relative to March when they were highest). EC and OECD forecasts are slightly higher than in the autumn, but both point to rising downside risks.

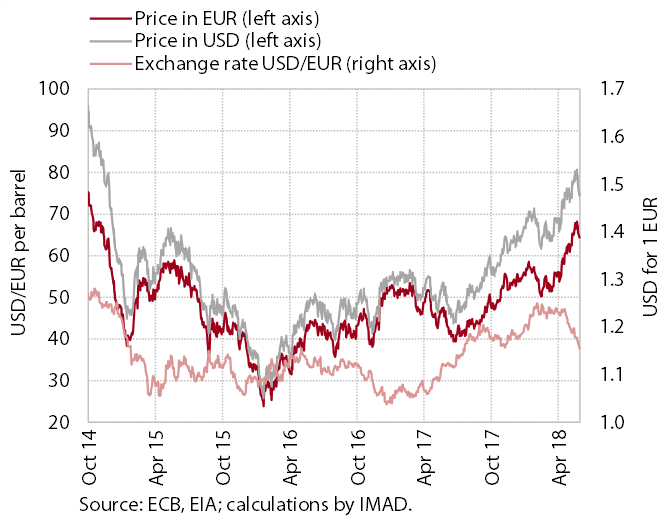

Oil prices have risen in recent months, reaching the highest levels since the end of 2014. The dollar price of Brent crude oil, at USD 65 at the beginning of the year, approached USD 80 in May. Year on year, oil prices were around 50% higher. According to the IEA, prices are rising largely due to increased uncertainties on oil markets related to the announced US sanctions on Iran. Euro price growth is also influenced by the depreciation of the euro relative to the US dollar in the last month.

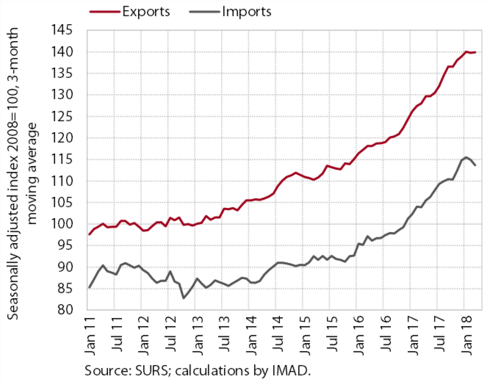

After last year's considerable growth, real exports and imports of goods have declined slightly in the last few months, but remain high year on year. Amid a moderation of growth in main trading partners, exports fell by 0.4% in the first quarter. Nevertheless, they remain higher year on year, primarily on account of vehicle exports, which represent around one fifth of Slovenian exports of goods. Imports have also dropped since the beginning of the year, particularly for intermediate consumption, which is partly related to the stagnation in manufacturing.

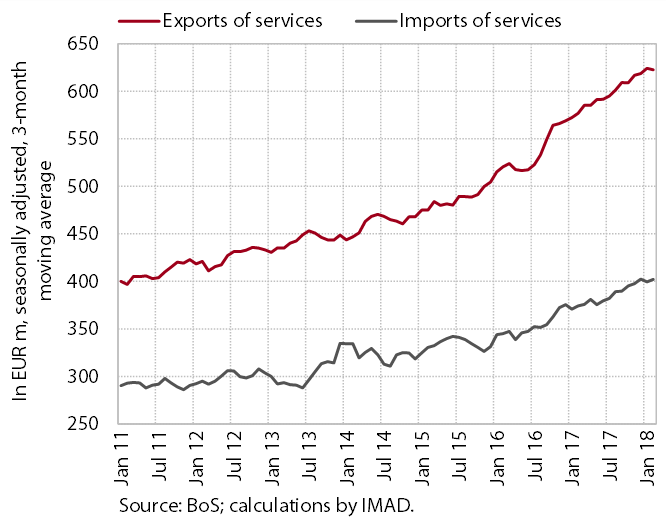

In the first quarter exports and imports of services maintained their high levels from the end of the year. The year-on-year growth of exports was due primarily to higher exports of transport and technical, trade-related services. Almost two thirds of the total exports of services in the first quarter were exports of travel (33%) and transport services (30%), which have been gaining importance in recent years. In imports to Slovenia, transport services account for the largest share (22%), followed by travel services (19%) and technical, trade-related services (16%). The latter also made the greatest contribution to import growth in the first quarter of this year.

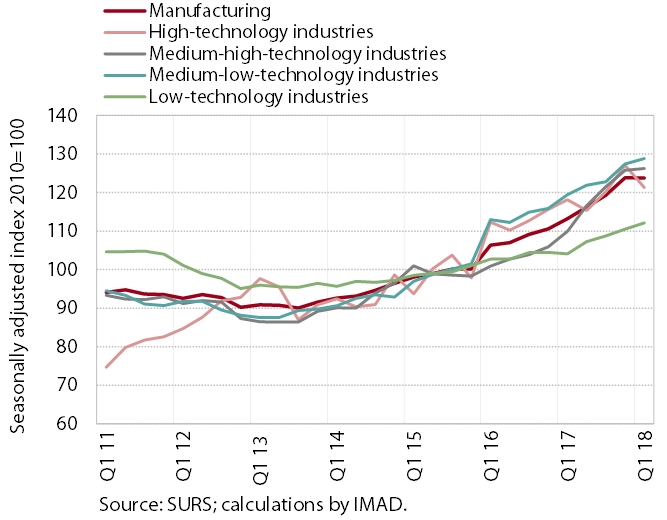

Production volume in manufacturing in the first quarter remained almost unchanged relative to the end of the year. After last year’s surge, production in export-oriented industries came to a halt or slowed under the impact of weaker growth in foreign demand. In low-technology industries, which are primarily oriented to the domestic market, it rose further. Year-on-year growth in manufacturing production remained strong (9.2%). It was still highest in the manufacture of transport vehicles (under the impact of a one-off factor), machinery and equipment (owing to higher investment activity both domestically and abroad) and ICT equipment.

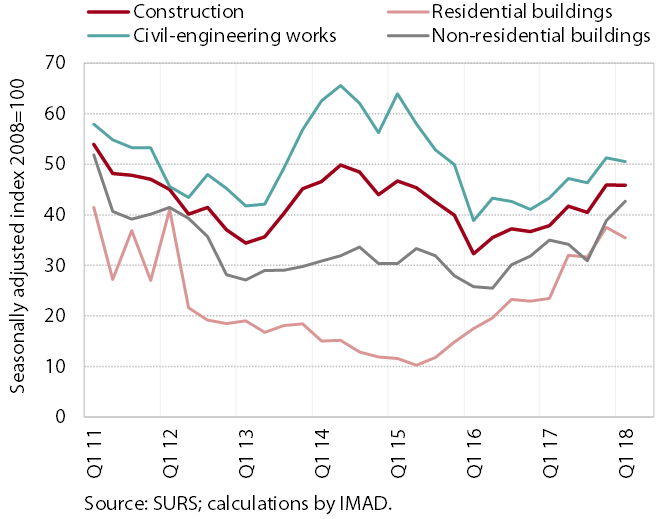

Amid adverse weather conditions, activity in construction remained unchanged in the first quarter. In the last two years construction activity has been strengthening steadily, but at the beginning of this year it remained at the level of the last quarter of 2017 due to unfavourable weather conditions. The strengthening in the construction of buildings in recent months mainly reflects greater optimism in the private sector, while the higher value of civil-engineering works arises primarily from increased government investment.

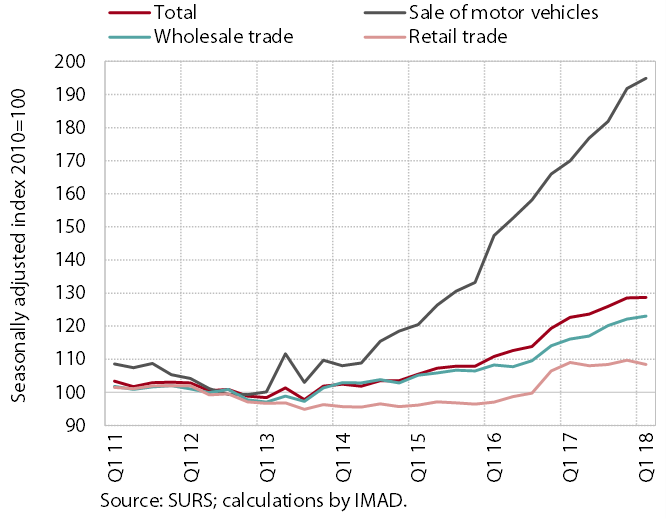

Turnover in trade in the first quarter remained at the level of the previous quarter and was 3.9% higher year on year. The highest year-on-year growth rates were again recorded in the sale of motor vehicles (12.4%) driven by rising sales to domestic natural and legal persons and foreign customers. With high activity of trade-related sectors (particularly manufacturing and transport), turnover also rose in wholesale trade (4.0%). In retail trade, turnover was lower year on year in the sale of food products and automotive fuels, after last year's growth, while turnover in the sale of non-food products was up again year on year.

Turnover growth in market services slowed in the first quarter. This was attributable primarily to the lower turnover in administrative and support service activities, particularly employment services. With a decline in telecommunications, turnover in information and communication activities remained at the level of the preceding quarter. Further turnover growth was recorded in transportation and warehousing, particularly on account of exports of road transport services. With higher spending by domestic and foreign tourists, turnover also rose further in accommodation and food service activities; after last year’s acceleration, further turnover growth was also recorded in professional and technical activities.

The deterioration in business sentiment has slowed in the last few months. Confidence deteriorated further only in retail trade, owing to lower current and expected sales. In manufacturing and service activities, confidence indicator values have stabilised above their long-term average after worsening early in the year. Confidence in construction continues to rise and consumer confidence remains high.

In the first quarter employment continued to rise. The number of persons employed reached the level of 2008. It was up year on year in all private sector activities, especially manufacturing, construction, accommodation and food service activities, and transport. Employment growth is, in addition to a decline in the number of the unemployed, mainly due to the hiring of foreign workers. These accounted for around 40% of the increase in the total number of the employed. In the public sector, employment growth mainly stems from increased employment in the education and health sectors.

Amid strong hiring, the number of registered unemployed persons continues to decline. The outflow into employment is somewhat lower than last year, yet still high. The fall in unemployment also reflects a somewhat lower inflow into unemployment year on year, which is mainly due to fewer expiries of fixed-term employment contracts. There are also fewer first-time jobseekers, which can be attributed to better economic conditions and smaller generations of young people finishing school. At the end of May, 76,705 persons were thus registered as unemployed, 12.5% fewer than in May 2017.

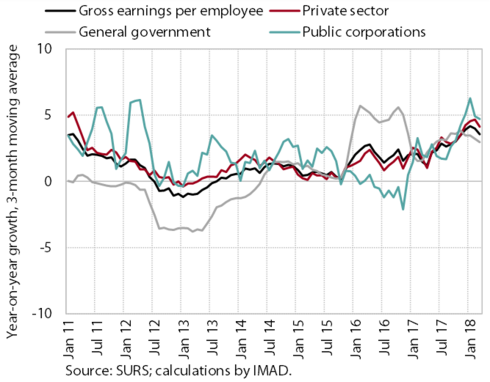

In the first quarter both the private and the public sector recorded higher year-on-year wage growth than last year. Wage growth in the private sector was attributable primarily to strong economic activity and hence good business results. Wages rose year on year particularly in construction, manufacturing and certain market services. Wage growth in the public sector, on the other hand, reflected the implementation of agreements with trade unions and the regular promotions of employees.

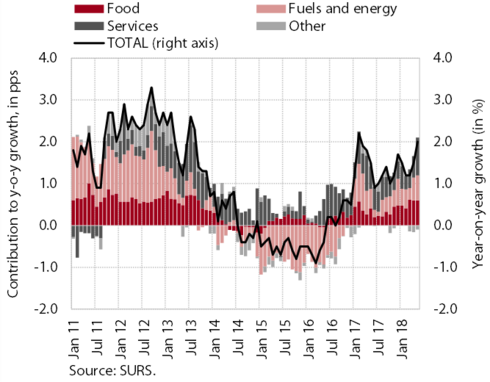

Inflation increased in April and May. Besides from the higher energy prices as a consequence of strong oil price growth on world markets and the depreciation of the euro, a significant contribution to growth also came from prices of services, which recorded the largest year-on-year increase in three years. Strong price growth was recorded in the “recreation and culture” group, where prices of package holidays rose strongly in April and May. The contribution of prices in “communications” also rose in May. The contribution of food prices remains relatively significant. Prices of semi-durable and durable goods remain down year on year. Core inflation otherwise rose slightly in May, but continues to hover around 1%.

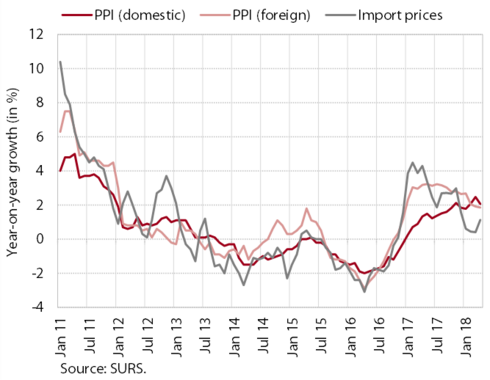

Year-on-year growth in import prices is rising, while growth in domestic industrial producer prices remains almost unchanged. The stronger growth of import prices is attributable to the significantly higher prices of energy (8.9% year on year) and price rises in non-energy commodities. Slovenian industrial producer prices on the domestic and on the euro area market are rising at similar rates (around 2%). Price rises on non-euro area markets eased notably, which is mainly a consequence of the high base.

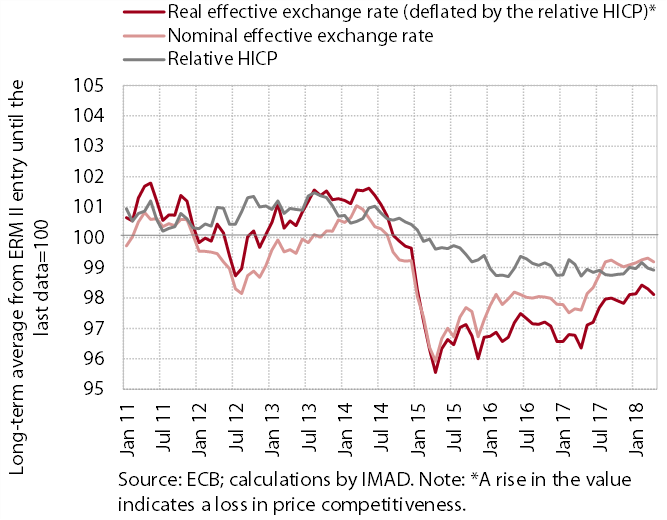

The price competitiveness of the Slovenian economy improved in April, after deteriorating further in the first quarter. The prolonged period of the gradual appreciation of the euro against the currencies of most main trading partners (and hence growth in the nominal exchange rate) came to a halt in April. With inflation similar to that in trading partners, the real effective exchange rate declined.

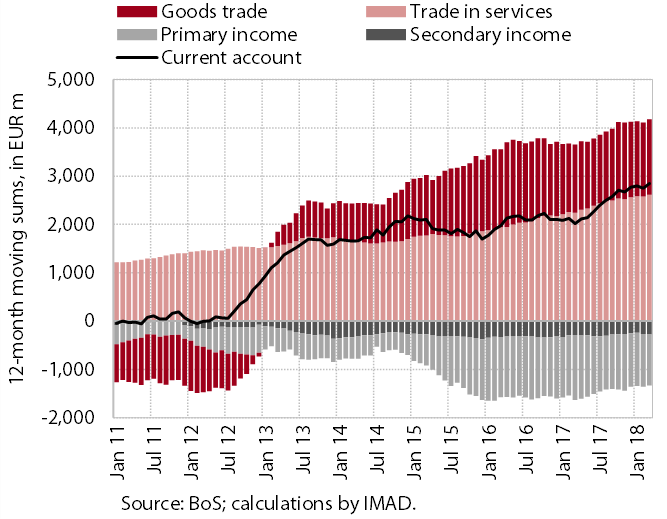

The surplus of the current account of the balance of payments remains high. The 12-month cumulative surplus for the period ending March 2018 amounted to EUR 2.8 billion or 6.1 % of GDP. The year-on-year increase in the first three months was mainly due to the higher surplus in international trade in goods and services. The terms of trade improved year on year, the growth for import prices (0.1%) being lower than for export prices (1.0%). This was attributable to the modest year-on-year growth of import prices of energy and industrial products and a decline in euro prices of other primary commodities. The deficit in primary income was down, for the most part because of lower external debt servicing costs and lower net outflows of dividends abroad. Net interest payments of the general government sector declined as a result of lower implicit interest rates. Owing to the significant deleveraging of commercial banks and increased investment in foreign securities, the private sector recorded net interest receipts. The BoS recorded stable net interest receipts, as its financial assets significantly exceeded its liabilities to the Eurosystem. The deficit in secondary income was lower because of the higher net positive current transfers of the government sector (receipts from the EU budget).

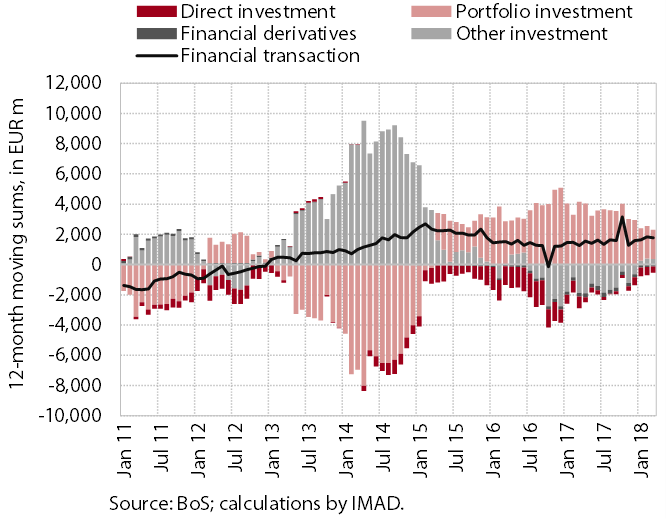

The net outflow in external financial transactions continues. External financial transactions recorded a net outflow of EUR 1.8 billion in the last 12 months, which continued to arise from net outflows in portfolio investment, particularly financial investment of commercial banks, the BoS and insurance companies. Other investment recorded a net inflow, as the government and the BoS were withdrawing deposits from their accounts abroad. A net inflow was also recorded for direct investment: among inflows, the inflow of equity predominated and among outflows, debt financing of affiliated companies abroad.

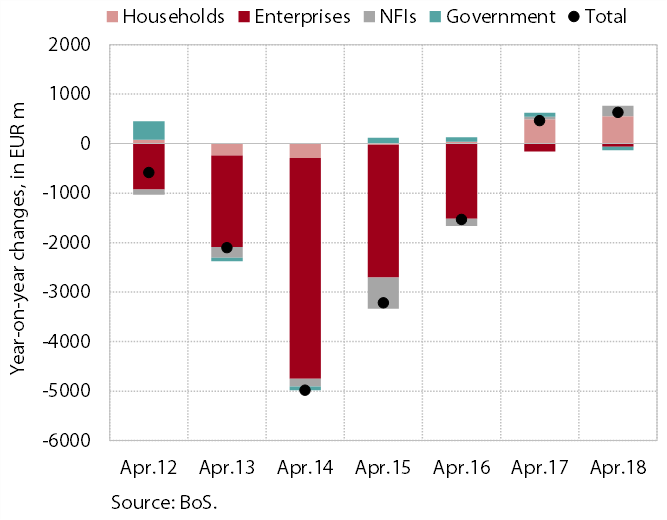

Year-on-year growth in loans to domestic non-banking sectors remains low. Corporate deleveraging has risen slightly again. Besides on bank loans, enterprises are to a greater extent than in previous years relying on other sources of finance. The relatively strong growth of household loans has slowed. Borrowing in the form of housing and consumer loans eased. Deposits by domestic non-banking sectors continue to expand, but with low deposit interest rates their maturity structure is deteriorating further. Overnight deposits thus already account for almost 70% of all non-banking sector deposits. Bank deleveraging abroad came to a halt this year, the share of liabilities to foreign banks stabilising just below 5%. Non-performing loans continue to fall gradually. Arrears of more than 90 days (EUR 1.1 billion) represent only 3.2% of the banking system’s total exposure.

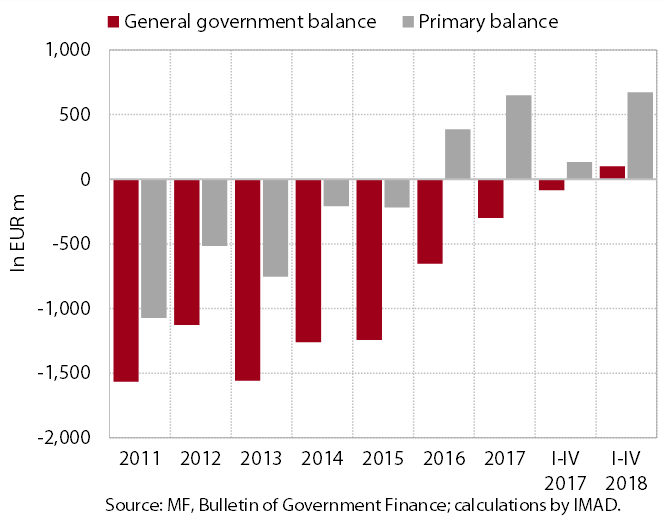

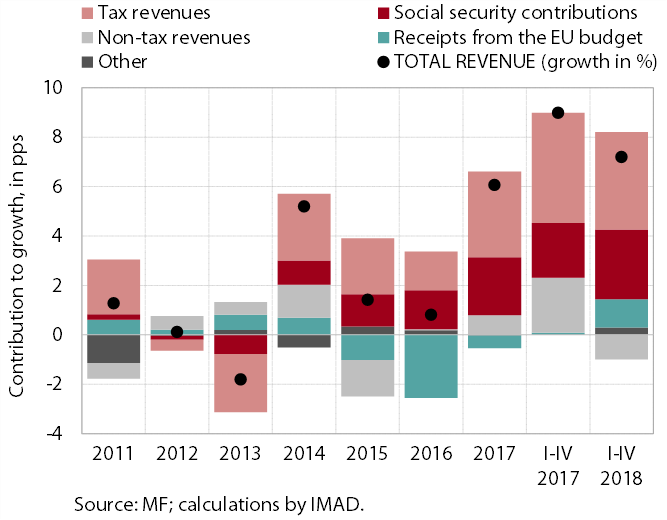

The general government balance was positive in the first four months (EUR 100 million). The further improvement in the general government balance, which turned into a surplus in April, continued to be influenced by favourable economic trends. Their impact was particularly pronounced on the revenue side, in the form of strong growth in revenue from taxes and social contributions.

The year-on-year growth of general government revenue totalled 7.2% in the first four months. The growth of revenues from social contributions and taxes (particularly personal income tax, CIT and, after strong April, VAT) was similarly high as in the same period of 2017. It continued to reflect favourable labour market trends, consumer optimism and (last year’s) improvement in business results. After relatively modest growth in preceding years, the inflows from excised duties were somewhat lower than in the same period of last year. Receipts from the EU budget were also higher year on year, owing to the increased inflows from structural funds in April. Non-tax revenues were lower year on year primarily due to lower dividend payments into the budget and a one-off inflow of interest in January 2017.

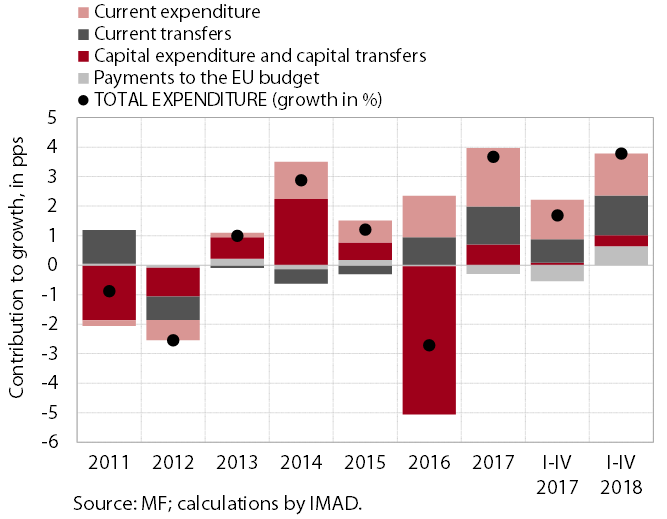

General government expenditure in the first four months was 3.8% higher year on year. After stagnation of total expenditure in the first quarter, in April its year-on-year growth was boosted particularly by higher expenditure on goods and services and somewhat stronger growth in expenditure on pensions and the wage bill. Payments into the EU budget were also higher, this as a result of the expected stronger dynamics of EU funds absorption at the level of the EU. Investment expenditure is also rising from its low levels.