Slovenian Economic Mirror

Slovenian Economic Mirror 7/2017

Economic growth in the euro area continued in the third quarter; in the autumn international institutions significantly improved their forecasts for the euro area economy for this year and next. In the third quarter high economic growth in Slovenia continued and remained broad-based. The labour market situation continues to improve with favourable economic conditions and high labour demand, while the growth of wages remains moderate.

In the third quarter economic growth continued in all Slovenia’s main euro area trading partners. Seasonally adjusted, euro area GDP rose 0.6% quarter on quarter and 2.5% year on year. This growth mainly reflects growth in exports, private consumption and investment. Business confidence indicates a continuation of growth in the last quarter of the year, as economic sentiment indicators (ESI, PMI, Ifo) improved further in the autumn months, reaching ten-year highs.

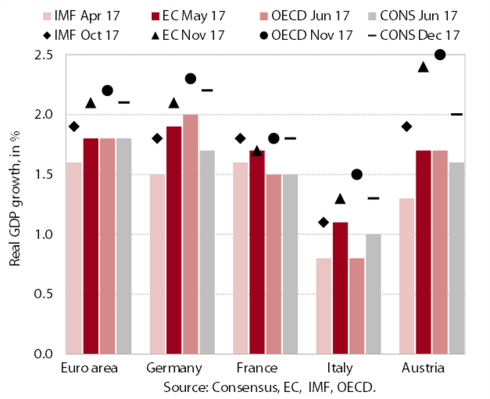

In the autumn international institutions significantly improved their growth forecasts for the euro area. The autumn forecasts for the euro area by the IMF, EC, OECD and Consensus are higher than earlier forecasts, mainly as a consequence of stronger-than-expected growth and favourable economic prospects. Economic growth in 2018 is expected to be mainly driven by private consumption and investment. Risks to the forecast are mostly balanced. Downside risks are mainly related to external factors (geopolitical risks, protectionist policies, a global tightening of financial conditions), while the upside risks arise from the euro area (a further improvement in business confidence).

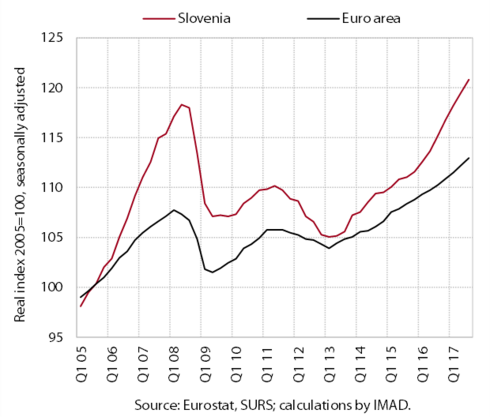

In the third quarter high economic growth continued. GDP was up 4.5% year on year in real terms. Quarterly GDP growth rates in Slovenia have exceeded the euro area average in the last two years. Slovenia has thereby closed the gap relative to the pre-crisis level, which was wider than on average in the euro area owing to a steeper fall in GDP in the first years of the crisis.

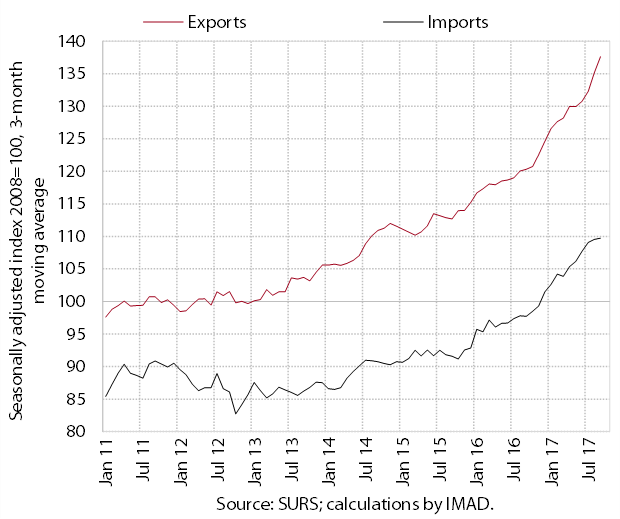

Growth in real merchandise exports and imports continues. We assess that export growth in the first nine months of 2017 was mainly driven by exports of motor vehicles and electrical equipment, which together account for around one quarter of total manufacturing exports. Export growth continues to stem from rising foreign demand and the favourable competitive position of manufacturing. Further, albeit somewhat slower, growth in imports was underpinned by high production activity and the strengthening of private consumption.

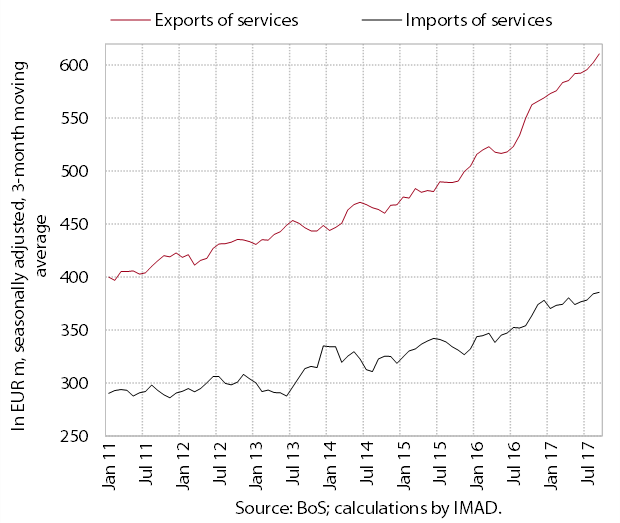

Nominal exports of services have increased further in recent months, and imports have remained high. The growth of exports is, in addition to higher spending by foreign tourists in Slovenia and exports of transport (road) services, largely due to exports of technical, trade related business services. Imports of such services also make a significant contribution to the growth of services imports.

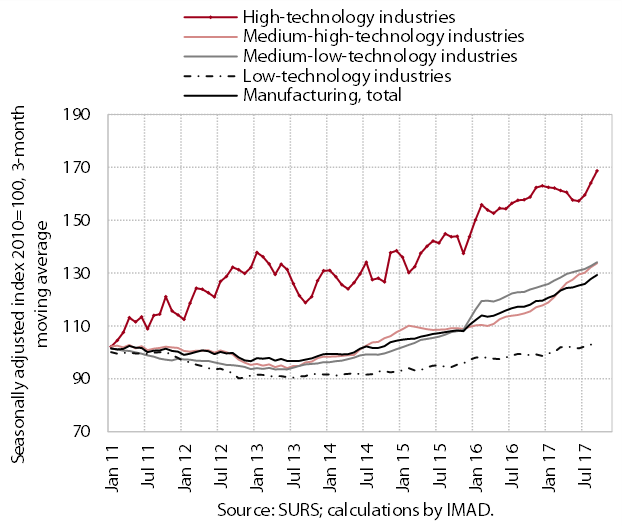

Production volume in manufacturing continues to increase in most activities. The first ten months recorded the strongest growth in the manufacture of transport equipment (by around one fifth) and machinery and equipment (by 15.0%). The prospects remain favourable, as most enterprises surveyed expect further growth in production at the beginning of 2018. The main limiting factor to production remains the shortage of skilled labour (cited by one third of enterprises surveyed); insufficient demand is highlighted by one fifth (compared with almost one third last year).

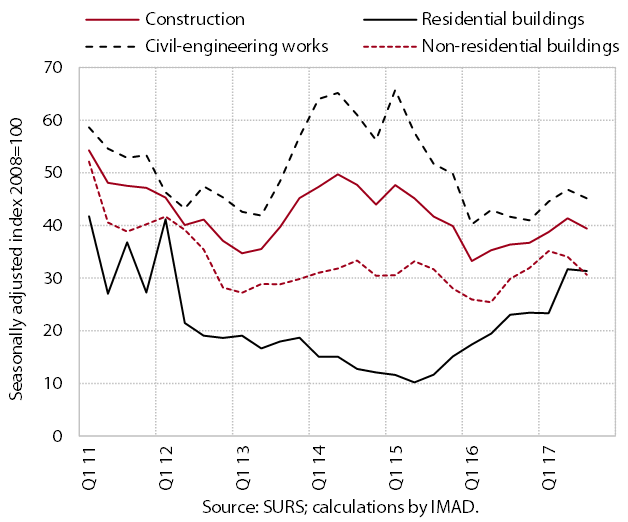

After growth in previous quarters, activity in construction recorded a decline in the third. It nevertheless remained higher year on year, and in the first nine months was up 14.2%. The higher level of construction of buildings year on year reflects stronger investment activity and the recovery of the housing market and, particularly in the construction of civil-engineering works, the rebound of government investment.

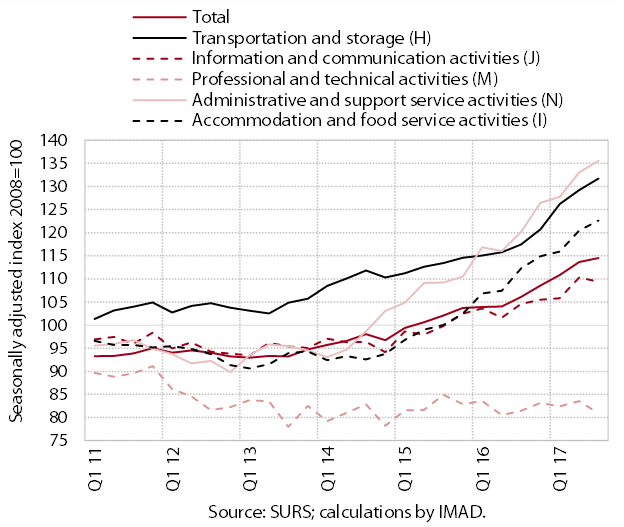

In the third quarter nominal turnover rose further in most market services. Growth in administrative and support services is mainly due to the further strengthening of turnover in employment services related to the rising demand for labour in the favourable economic conditions. Growth in road transport has resulted primarily from higher exports of these services. Further growth in accommodation and food service activities is boosted by increased spending of domestic and foreign tourists. Turnover in information and communication services remained similar to the previous quarter, but stagnated in computer and telecommunication services. The low activity in professional and technical services stems particularly from architectural and engineering services.

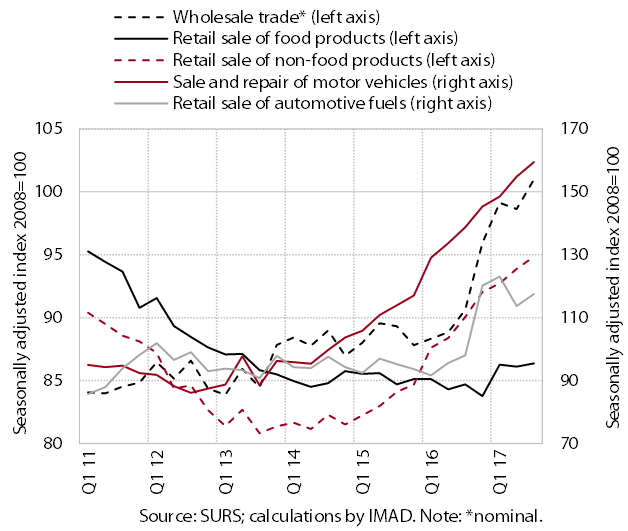

Most trade segments recorded further sales growth in the third quarter. In the main three segments sales were around one tenth higher year on year in the first nine months. The strong growth of sales in durable and semi-durable goods in retail trade was boosted by further growth in household consumption. Alongside the higher sales of cars to legal persons and for export, this contributed to further turnover growth in the sale of motor vehicles. With high activity in trade-related sectors (particularly manufacturing and transport), turnover also rose in wholesale trade.

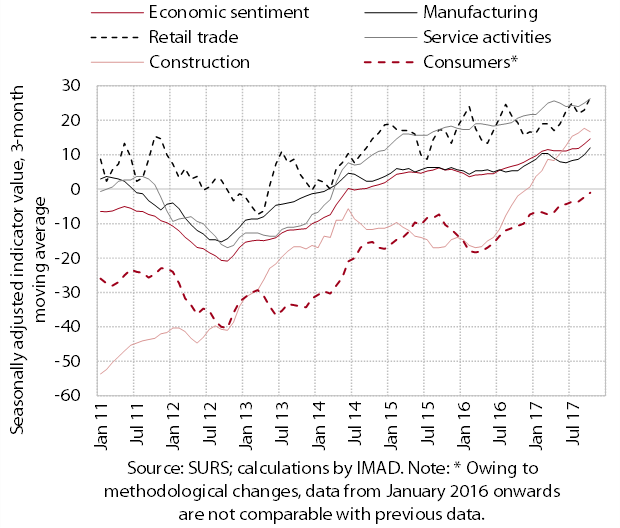

Economic sentiment continues to improve in the second half of the year, recording levels similar to those before the crisis. Since mid-year, confidence has been rising across all sectors, the fastest in manufacturing and construction. Consumer confidence is reaching the highest levels since these data have been available.

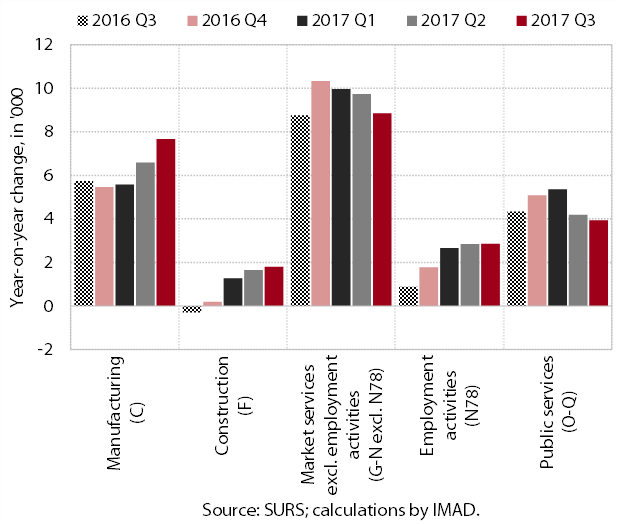

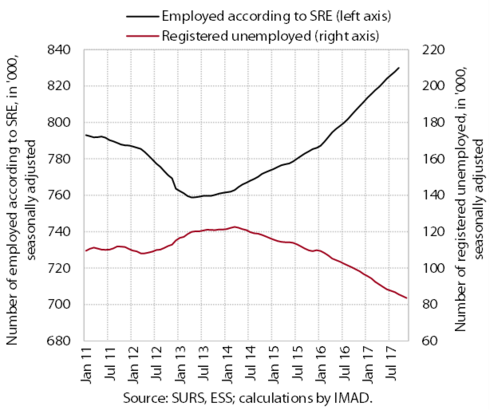

With favourable economic conditions, the number of employed persons rose further in the third quarter, to a level comparable to that in the pre-crisis year 2007. High labour demand is also indicated by an increase of approximately one third in the number of vacancies than in the same period last year, and by high expectations of enterprises about future employment. Particularly in manufacturing, enterprises are facing a shortage of skilled labour and some sectors continue to increase the employment of foreigners. The year-on-year rise in the number of employed persons in public services has resulted mainly from employment growth in the sectors of education (primary education in particular) and health.

Registered unemployment continues to decline. The inflow into unemployment in the first eleven months was smaller year on year, mainly on account of the lower number of expired fixed-term employment contracts. There were fewer first-time jobseekers, which is related to better economic conditions and smaller generations of young people finishing school. The outflow into employment in the first eleven months was somewhat smaller than in the same period last year. At the end of November 82,415 persons were registered as unemployed, 14.9% fewer than in November 2016.

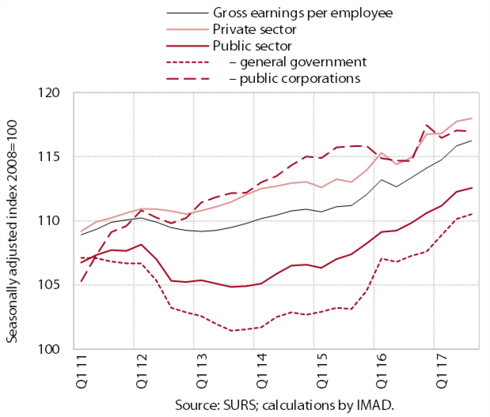

Wage growth remained moderate in the third quarter. It was similar to that in the previous quarter in both the private and public sectors. In the first nine months it was around 2.5% higher in nominal terms in both sectors. Among private sector activities, manufacturing and some market services stood out in terms of growth, similar to last year. The moderate growth is, in our assessment, attributable particularly to the relatively low growth of prices and productivity and hiring in activities with below-average wages.

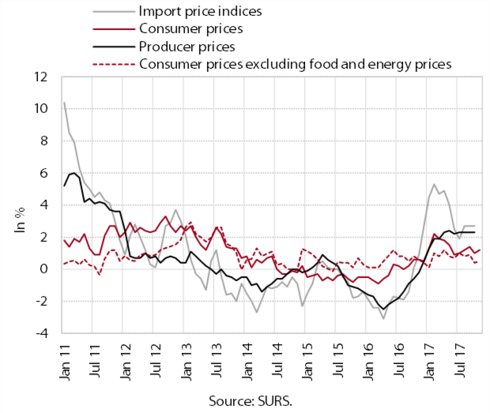

Year-on-year consumer price growth remains relatively low. The contribution of food prices, the main driver of inflation in addition to prices of energy and services, strengthened in November. The contributions of other price groups remained relatively low. The decline in prices of durable and semi-durable goods slowed slightly in November. The movement of core inflation indicates no major pressures on price growth. The year-on-year growth of industrial producer and import prices continues, exceeding slightly the growth of consumer prices. The main drivers of growth are price rises in commodities, energy and non-durable consumer goods. Growth in domestic producer prices for industrial products sold on the domestic market has strengthened somewhat in recent months, while it has slowed slightly for industrial products sold abroad.

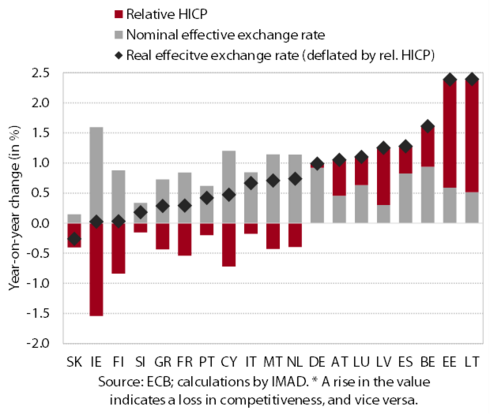

The price competitiveness of Slovenia’s economy remains relatively favourable despite this year’s deterioration. The appreciation of the euro against the currencies of main trading partners, particularly those outside the EU, has eased in recent months. The increase in the nominal effective exchange rate in Slovenia was in any case among the smallest in the euro area this year, given that Slovenia performs an above-average share of its external trade in the euro area and is thus less sensitive to exchange rate fluctuations. Price competitiveness also continues to be favourably affected by lower growth in relative prices (inflation) in Slovenia.

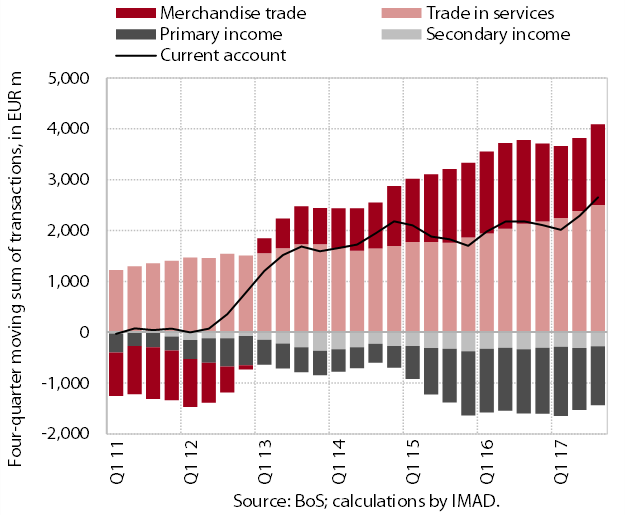

The surplus of the current account of the balance of payments continues to rise; in the last twelve months it totalled EUR 2.7 billion (6.3% of GDP). The higher surplus in current transactions in comparison with the previous 12-month period was mainly due to the greater trade surplus in services resulting from higher net revenue from travel and the surplus of trade in other, trade-related services. The surplus in merchandise trade was lower year on year, mostly due to the deteriorated terms of trade. The deficit in primary income was down largely because of lower net payments of interest on external debt as a result of lower yields on government bonds. The deficit of secondary income was also lower, owing to higher transfers to the private sector.

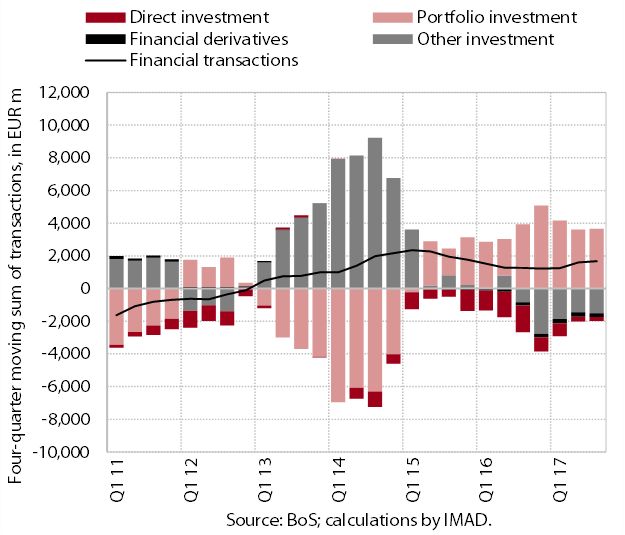

The net outflow of external financial transactions continues. External financial transactions recorded a net outflow of EUR 1.7 billion in the last twelve months, with the net outflow of the private sector exceeding the net inflow of the government sector and the BoS. The government was withdrawing deposits from its accounts abroad, as did the BoS, which also increased its liabilities within the Eurosystem. At the same time, it increased investment in foreign securities, but the outflows from these transactions were lower than the inflows. Within the private sector, commercial banks were strengthening financial investments in foreign debt securities and repaying foreign loans. Short-term trade credits of enterprises to the rest of the world rose, reflecting favourable export trends.

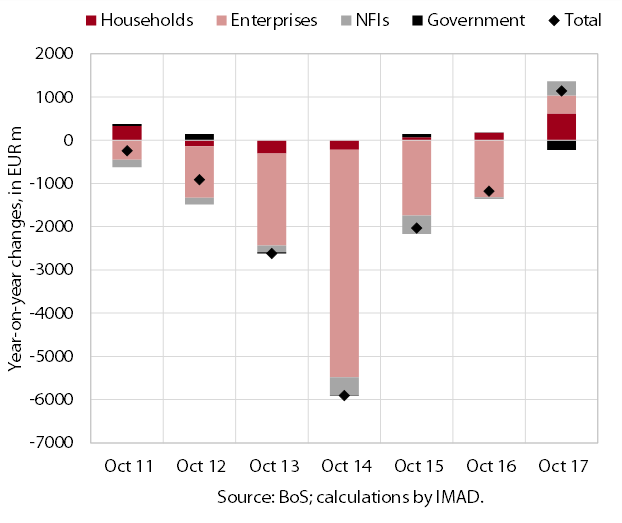

The year-on-year growth in loans to domestic non-banking sectors continued in October. The volume of household loans (consumer loans in particular) continues to rise steadily. Banks’ willingness to extend loans for consumption is related to the relatively high level of interest rates for consumer loans compared with housing loans, and their shorter maturities. This is easing the pressures on maturity matching in the banking system’s balance sheets, given that overnight deposits in particular are rising among the sources of funding for banks. Since mid-year the volume of corporate loans has also been picking up, in our assessment owing mainly to the further moderation of deleveraging, given that the volume of new loans has dwindled slightly in recent months.

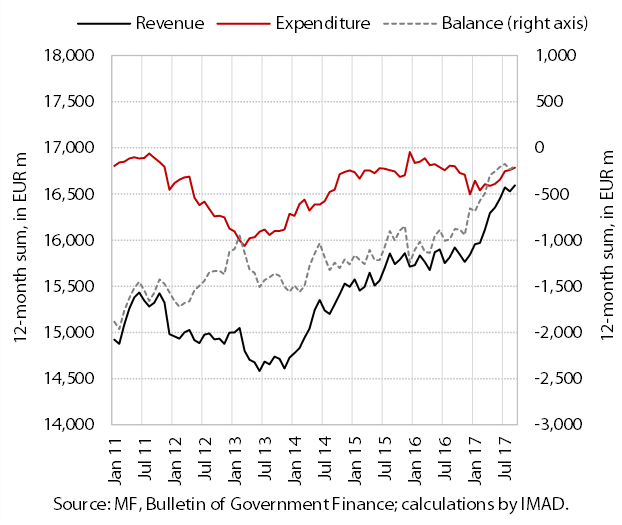

Favourable public finance movements continue. In the first nine months the general government balance on a cash basis recorded a surplus of 0.1% of GDP, which has arisen from strong revenue growth and the retention of moderate expenditure growth. Strong revenue growth is underpinned primarily by favourable economic conditions, while in the third quarter revenue from EU funds was also up year on year after a relatively long period. Expenditure growth has resulted mainly from growth in employee compensation, some transfers (pensions and sickness benefits) and expenditure on goods and services. Towards the end of the year, expenditure growth is expected to strengthen owing to the settlement of matured financial liabilities of hospitals and the payments of cohesion policy funds, which tend to accumulate at this time of the year.