Competitiveness

Slovenian Economic Mirror 7/2016

Economic growth in the euro area continued in the third quarter of 2016; moderate economic growth is also expected for the last quarter of the year. During the summer months positive developments also continued in Slovenia; the prospects for the last quarter are also favourable.

(copy 1)

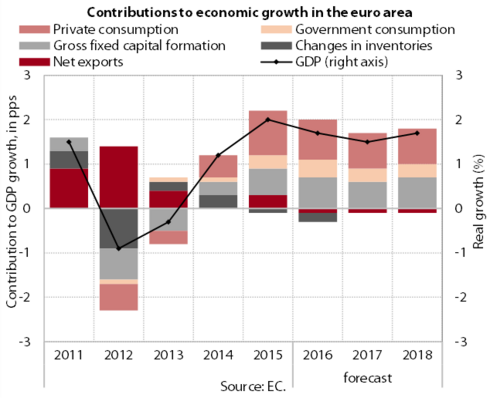

Economic activity in the euro area is increasing; moderate economic growth is also expected for the remainder of the year. According to Eurostat’s preliminary flash estimate for the third quarter, GDP in the euro area grew by 0.3% (seasonally adjusted) and was 1.6% higher than in the same quarter of 2015. In its autumn forecast, the European Commission expects a continuation of moderate economic growth in the remainder of the year; this is also indicated by the Economic Sentiment Indicator (ESI), which reached the highest value this year in October, and the composite Purchasing Managers Index (PMI). The European Commission otherwise predicts 1.7% GDP growth in the euro area for this year (1.6% in the spring), while in 2017, GDP will be lower than projected primarily owing to the expected consequences of Brexit (1.5%; compared with 1.8% in the spring). Its growth will continue to be driven by private consumption and investment.

Credit standards for loans to enterprises in the euro area did not ease further in the third quarter and banks expect their tightening in the future. After two years of easing, credit standards for enterprises remained unchanged, according to the ECB survey. Credit standards for households continue to ease, the main factor being greater competition between the banks. With low interest rates, loan demand increases further across all loan categories.

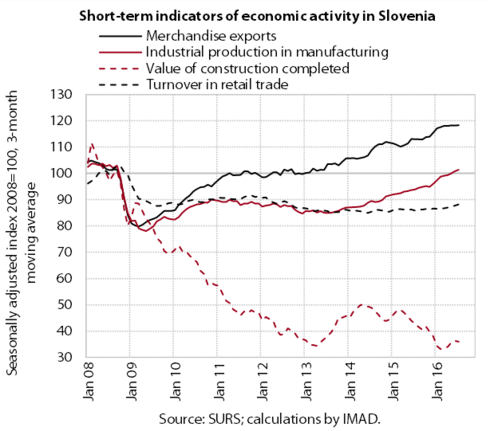

Favourable developments continue across most sectors. Real merchandise exports and manufacturing output remained high during the summer months. After the increase in the second quarter, activity in construction has stayed almost unchanged, but lags significantly behind the level from the same period of last year. Turnover in market services is gradually rising. With the improvement in labour market conditions, turnover is rising in some segments of trade and in accommodation and food service activities, where it is also underpinned by higher spending by foreign tourists. Confidence in the economy and among consumers indicates a continuation of favourable developments in the last quarter.

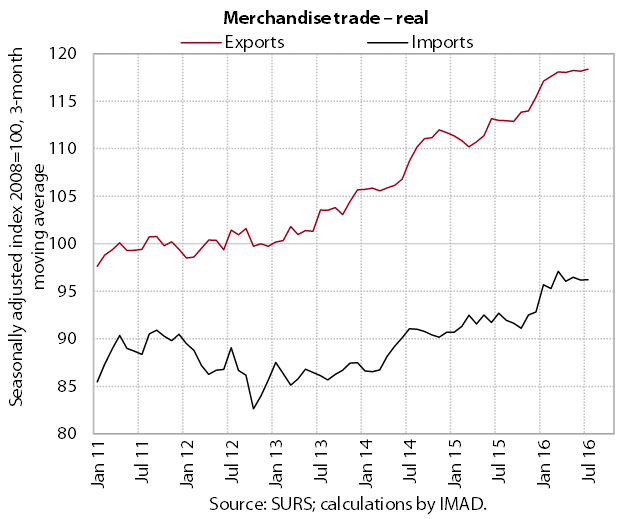

After vigorous increases early in the year, real merchandise exports and imports remain high. In the first eight months, real merchandise exports were up 6.2% year on year. Higher exports were recorded in most manufacturing industries, the greatest contribution to growth coming from exports of transport equipment. The year-on-year growth of imports stood at 4.2% in the same period. It was, to a similar extent, due to the higher imports of investment goods and consumer goods related to the stronger investment activity of the private sector and household consumption.

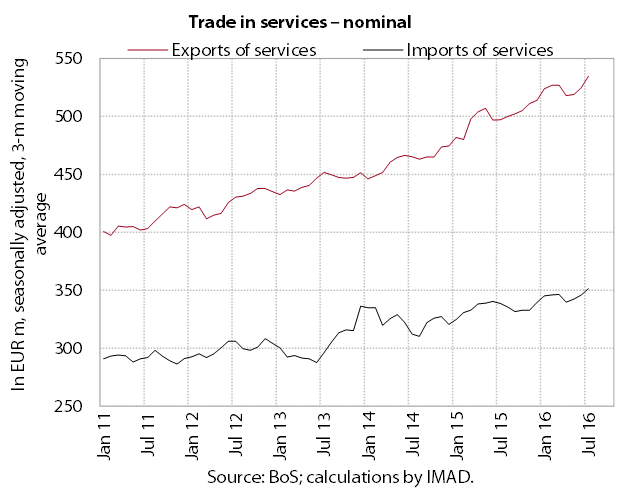

Growth in nominal exports and imports of services continues. The year-on-year growth of exports in the first eight months (6.1%) was largely underpinned by higher exports of transport and construction services, while the year-on-year growth of imports (3.6%) arose primarily from increased imports of technical, trade-related business services and higher resident spending abroad (imports of travel).

Production volume in manufacturing remains high. In the first eight months, production volume was up year on year in most industries. According to business tendency data, most enterprises surveyed expect further growth in demand and production in the last quarter of the year. Insufficient demand (domestic, in particular) otherwise remains the main limiting factor to production, with more and more enterprises also facing a shortage of skilled workers. In the first eight months, the number of employed persons in manufacturing rose by around 5,800 (3.2%) year on year. The largest contribution to employment growth was made by some more export-oriented industries, where production increased the most relative to the same period last year (the rubber and metal industries, ICT and electrical equipment manufacturing).

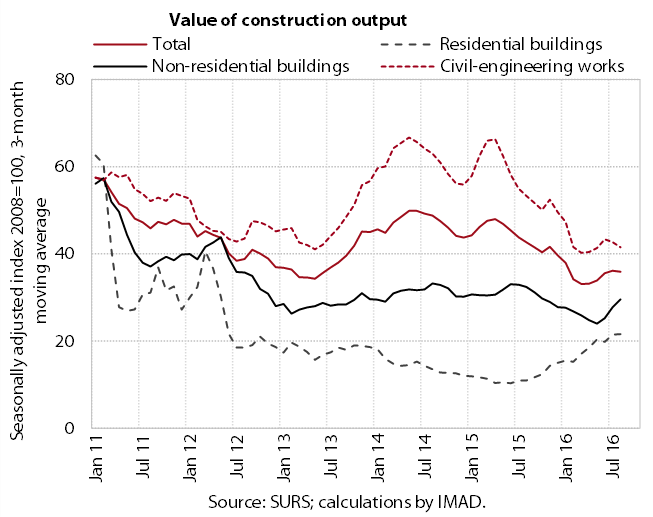

After having increased in the second quarter, the value of construction output remained roughly unchanged in the summer. However, owing to a sharp decline around the turn of the year, construction activity is noticeably lower than in 2015. Only the construction of residential buildings, having recovered strongly since mid-2015, is higher than last year.

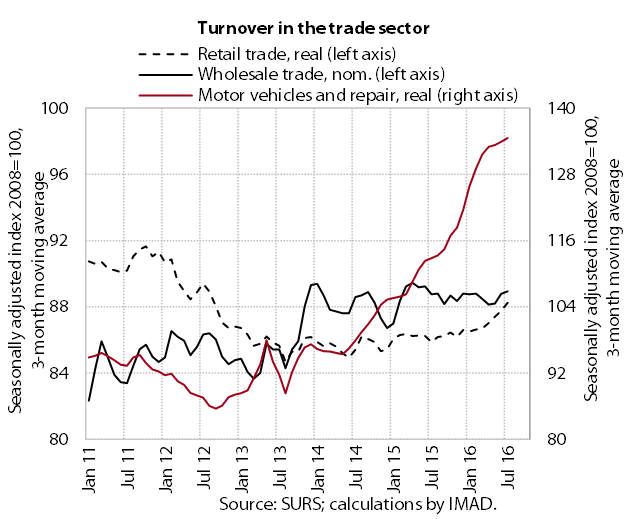

In distributive trades, the sales of vehicles and non-food products continue to grow. Retail trade has been increasing steadily since the beginning of the year, in recent months not only owing to the sales of non-food products, but also the rising sales of automotive fuels. Food product sales have remained low amid changes in consumer behaviour; this is the only sector where turnover has not risen year on year. Reflecting further growth in the sales of new passenger and goods motor vehicles, motor vehicle sales recorded the highest year-on-year growth (of more than one-fifth) in the first eight months.

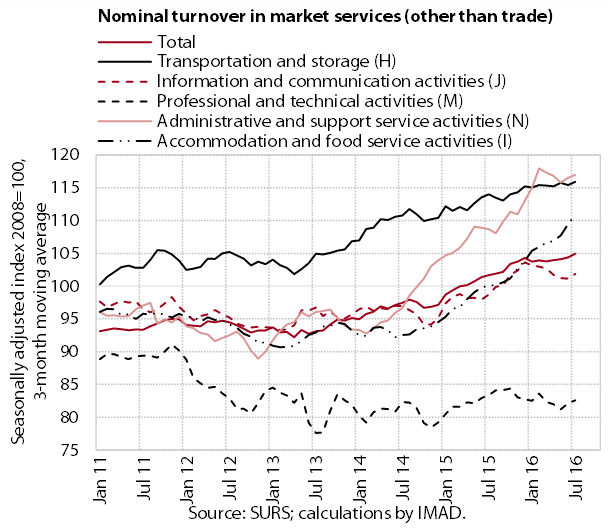

Nominal turnover in market services is gradually rising. With increased spending by both domestic and foreign tourists, turnover expands the most in accommodation and food service activities. Turnover growth in the largest sector, transportation, is weak owing to the decline in export revenue from land transport. In the first eight months, turnover was up year-on-year in all market services.

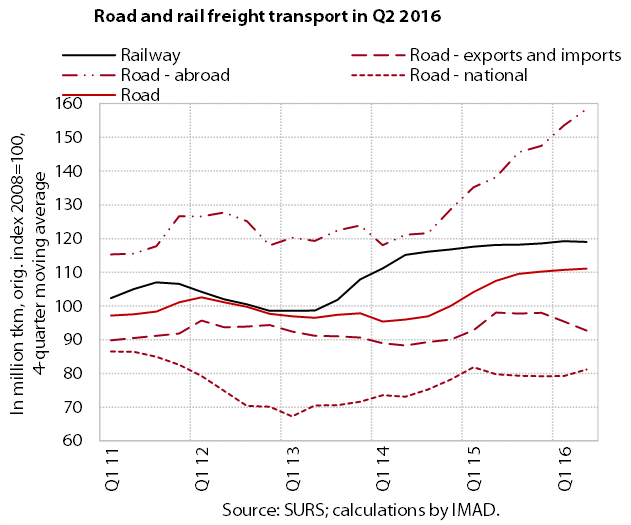

The volume of road freight transport has stagnated in the last quarters. Only the journeys carried out by Slovenian road hauliers entirely abroad have been rising more notably, which is related to the favourable foreign demand and the liberalisation of the transport market, as hauliers are also increasingly competing for business in other countries. Foreign hauliers have made a greater contribution to the increasing freight transport on Slovenian roads than domestic hauliers. Rail freight transport has retained its level despite the decline in export orders in the first half of the year.

Household consumption is rebounding with the recovery of labour market conditions and rising disposable income. August recorded a further increase in the consumption of durable goods, where purchases of passenger vehicles increased the most. Purchases of some semi-durables also rose slightly. We estimate that households also spent more on services related to accommodation, food, recreation and culture. Consumer confidence has also improved considerably since the middle of the year.

Economic sentiment has been improving since mid-year. Confidence has increased the most in construction; in other sectors it has remained high, similar to the first half of the year.

Solvency is improving. The number of non-payers and the amount of outstanding liabilities of legal persons and sole proprietors were lower again year on year in the third quarter. Payment delays shortened, but long-term outstanding liabilities remained high. They accounted for 73% of total outstanding liabilities in legal persons and 83% in sole proprietors. Including September’s round of compulsory and voluntary set-offs, the mutual indebtedness of business entities declined by EUR 2.9 billion in the period since April 2011.

The number of bankruptcy proceedings initiated against legal entities and sole proprietors and the number of personal bankruptcy filings declined in the last two quarters. The most bankruptcy proceedings against legal entities and sole proprietors were again filed in distributive trades and construction, in sole proprietors also in accommodation and food service activities. Although the number of personal bankruptcy filings was lower year on year (by 12%), it still totalled 2,703 in the first nine months. The amounts of reported claims were a third lower.

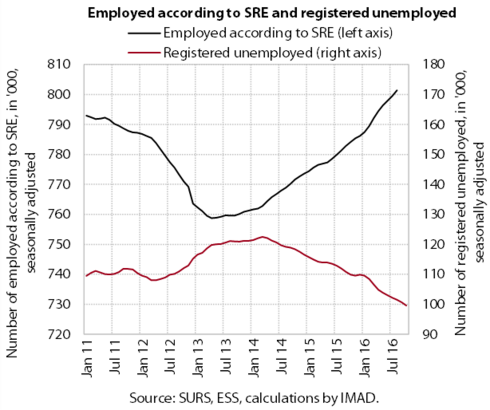

The number of employed persons continues to increase, reflecting higher confidence and economic activity. Its year-on-year growth in the first eight months was higher than in the same period of 2015 in most private sector activities, particularly manufacturing, distributive trades, accommodation and food service activities, and professional, scientific and technical activities. With the relaxation of hiring restrictions, growth in public service activities was higher year-on-year in the health sector, public administration and primary education. Employment prospects remain favourable.

With increased hiring, registered unemployment continues to decline. This is attributable not only to the outflow into employment, which was higher year on year in the first ten months, but also a gradual decrease in the inflow into unemployment. This was lower mainly owing fewer first-time jobseekers and fewer persons out of work for business reasons or due to the termination of their fixed-term employment contracts. At the end of the October, 97,263 persons were registered as unemployed, which is 9.5% less than last year.

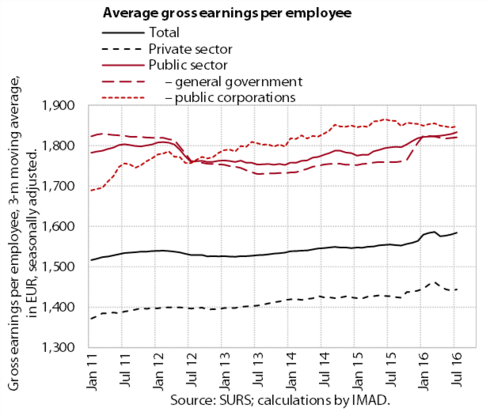

Average gross earnings are rising at a moderate pace. In the private sector, their growth is related to the strengthening of economic activities; in the public sector, it is mainly due to public servants’ promotions in December 2015. In the first eight months, the private sector and the government sector recorded considerably higher year-on-year growth than for the same period of 2015. Unlike in previous years, earnings were lower only in public corporations.

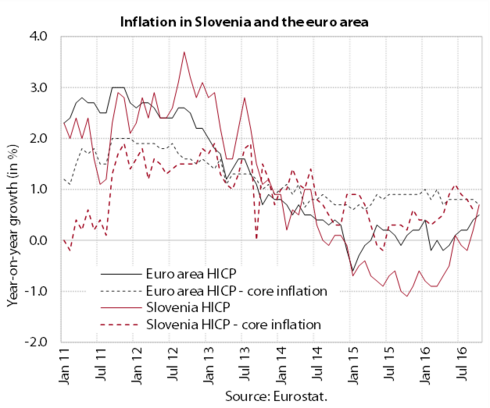

After almost two years of deflation, Slovenia has recorded consumer price growth in the last two months. Year-on-year inflation stood at 0.6% in October. The higher year-on-year growth mainly reflects the ever smaller energy price declines and the strengthening of food price growth. Prices of services are higher year on year; prices of semi-durable goods are also up again, after the decline in the summer months. Prices of durables remain lower. The strengthening of prices in the euro area is more modest because of lower food price growth.

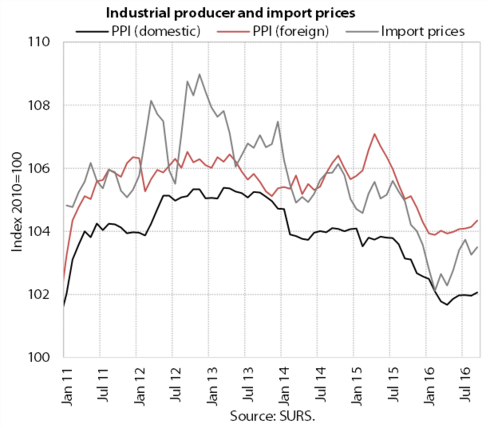

The year-on-year declines in industrial producer prices and import prices are easing amid higher commodity prices on world markets. Similar trends are also recorded for industrial producer prices in the euro area.

The price and cost competitiveness of the Slovenian economy remain close to the favourable levels seen last year. The smaller deterioration was a consequence of the appreciation of the euro, which had a smaller impact on Slovenia than on most other euro area countries due to the geographic structure of Slovenia's trade. In the last few months, the euro has almost stopped appreciating against our basket of currencies. In the first nine months, price competitiveness losses were also mitigated by declining relative consumer prices, the effect of which has been decreasing in recent months. Relative unit costs in the first half of the year were at the same level as in the first half of 2015.

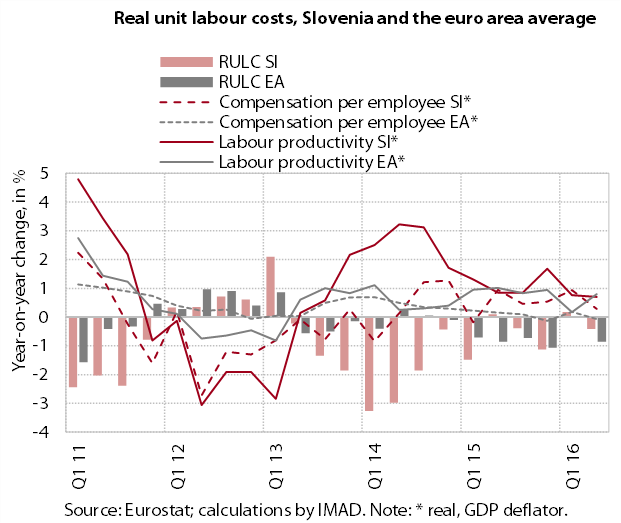

Unit labour costs declined again in the second quarter. The year-on-year growth of compensation per employee remained moderate (0.3%), lagging slightly behind productivity growth (0.7%); real unit labour costs thus declined slightly (-0.4%). Similar, or even slightly more favourable, dynamics were also recorded at the level of the euro area as a whole.

In the second quarter, real unit labour costs in manufacturing, the sector that is the most exposed to international competition, declined more than at the level of the whole economy. The year-on-year decline of 1.5% was attributable to the rebound in productivity growth (4.7%). In the middle of the year, real unit labour costs in manufacturing in Slovenia and in the euro area as a whole were similar to those before the crisis.

Slovenia’s merchandise market shares of world and EU exports continued to increase in the first six months. The stronger growth in the EU was largely the result of increased market shares in Germany, Croatia and Italy, coupled with renewed stronger growth on most relatively less important EU markets. Among the most important products in the manufacturing sector, Slovenia increased its EU market shares of medical and pharmaceutical products, rubber products, paper and paperboard, non-ferrous metals, machinery specialised for particular industries and miscellaneous manufactured articles. Of the most important export markets outside the EU, the market shares in Bosnia and Herzegovina and Serbia increased the most. The strong market share growth on the world market was not only due to the base effect, but also to more modest growth in import demand from non-EU markets (North and South American and Asian markets). Similar to 2013–2014, it was one of the highest in the EU Member States.

The current account surplus is the highest thus far; in the twelve months to August, it totalled 6.7% of GDP. In the first eight months of the year, its year-on-year increase was mainly underpinned by the surplus in international trade in goods and services, which reflects export competitiveness, the growth of export markets and weak domestic consumption. The deficit in primary income was down year on year largely owing to the lower estimates of reinvested earnings of foreign direct investors. Net payments of interest on external debt were also lower, which is a consequence of further bank and government deleveraging abroad. The deficit of secondary income is narrowing primarily as a result of the lower payments into the EU budget.

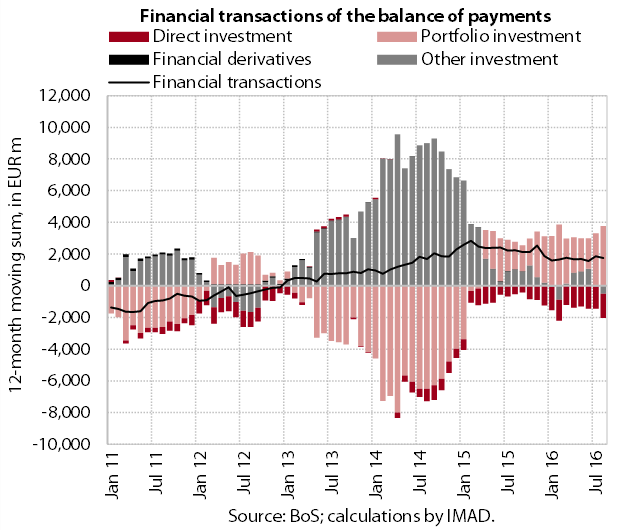

The net financing of the rest of the world continues. In the first eight months, this was a consequence of a net outflow of portfolio investment, while other investment and direct investment recorded net inflows. The Bank of Slovenia increased investment in foreign debt securities, in line with the public sector purchase programme (PSPP). Because of lower returns, the government and commercial banks reduced their assets in foreign accounts and continued to repay external debts. The year-on-year increase in the net inflow of direct investment was mainly due to inter-company loans of foreign direct investors.

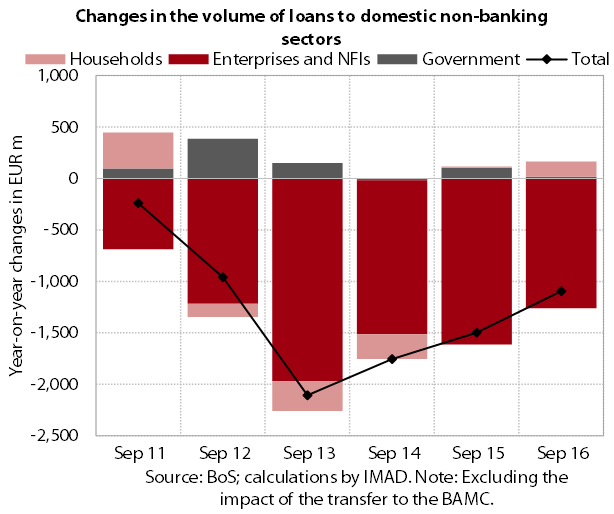

The volume of loans to domestic non-banking sectors continues to contract. Its decline is a consequence of further corporate and NFI deleveraging, while households are borrowing in the form of housing and consumer loans.

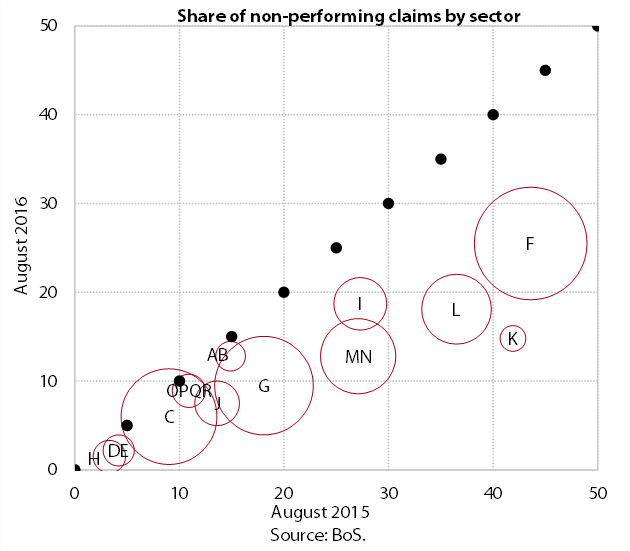

The quality of banks’ assets started to improve at a faster pace in the first two months of the third quarter. The acceleration was attributable to the sale of a portion of non-performing claims and higher write-offs. At the year-on-year level, the largest declines were recorded for non-performing claims against enterprises in the sectors with high shares and volumes of non-performing claims, i.e. construction, distributive trades, professional, scientific and technical activities and administrative and support service and real estate activities. Compared with EU countries that requested financial assistance, Slovenia has reduced the share of non-performing claims the most since the beginning of the banking system stabilisation.

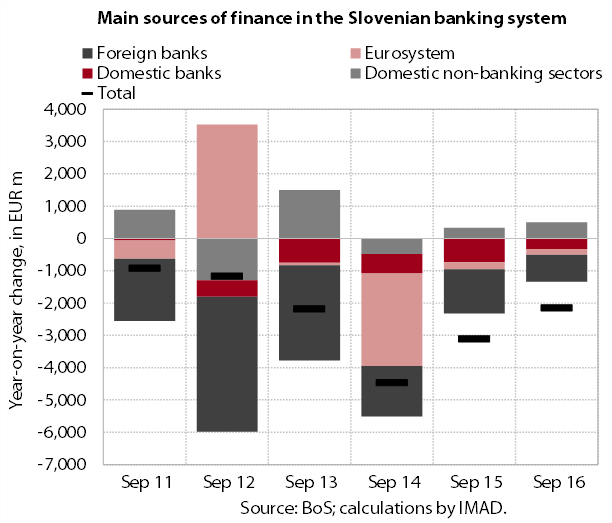

The structure of sources of finance for banks is changing in favour of non-banking sector deposits. These account for as much as two-thirds of the banking system’s total assets, which is around half more than in 2008. Overnight deposits predominate, being almost one-fifth higher year on year. Banks’ dependency on foreign bank financing continues to decline gradually.

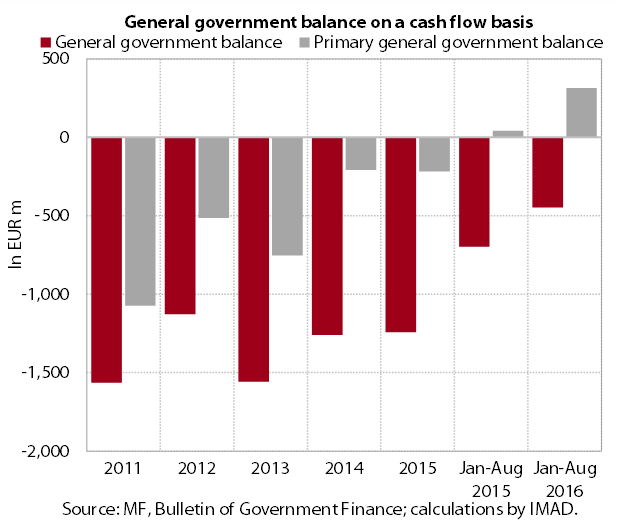

The general government deficit on a cash basis in the first eight months was lower than in the same period of 2015. This reflects the improving economic conditions, a significant change in the flows of EU funds and the retention of some measures to contain expenditure growth. The general government balance excluding interest expenditure, which is important for the moderation of public debt growth, recorded a surplus, which was significantly higher than in the same period last year.

General government revenue rose year on year in the first eight months. The fastest growth is recorded for revenues related to labour market conditions, i.e. the strengthening of earnings and employment. The relatively low year-on-year growth in revenues related to consumption is attributable to transitional factors – in VAT revenue, to the effect of the change in the payment of VAT on importation.

General government expenditure dropped year on year in the first eight months. The bulk of the decline results from lower investment (at the beginning of the implementation of the new financial perspective of the EU). Most of the other expenditures are rising, particularly those related to the easing of some austerity measures (earnings, hiring in the public sector, transfers to individuals and households).

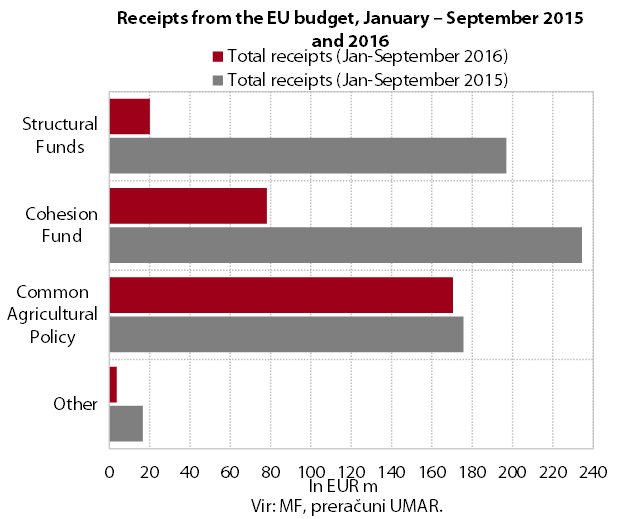

Slovenia's net budgetary position against the EU budget is negative (minus EUR 8.4 million). In the first nine months of 2016, Slovenia received EUR 297.3 million from the EU budget. The bulk of receipts were funds for the implementation of the Common Agricultural and Fisheries Policy. The majority of receipts from the Cohesion Fund and Structural Funds (EUR 98.4 million) were paid into the state budget in the first five months (from the previous financial perspective). Only EUR 20 million was disbursed from the state budget for projects (until the end of August). Payments into the EU budget totalled EUR 305.7 million in the first three quarters.