Competitiveness

Slovenian Economic Mirror 6/2016

The prospects for economic growth in the euro area remain favourable; the risks are on the downside and arise mainly from outside the euro area. Most short-term indicators of economic activity in Slovenia increased further at the beginning of the third quarter.

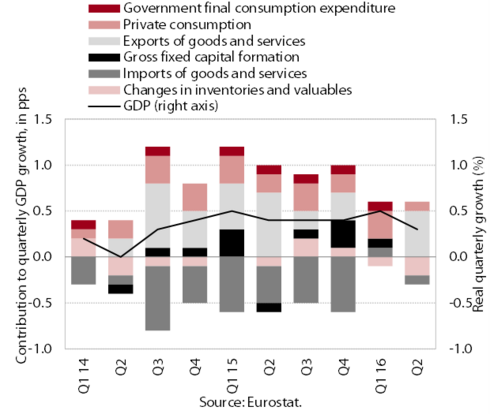

Economic growth in the euro area continued in the second quarter. GDP rose by 0.3% (seasonally adjusted; by 0.5% in the first quarter) and was 1.6% higher year on year. The largest contribution to GDP growth came from net exports, while growth in private consumption, which has been the main driver of the recovery in recent quarters, was low.

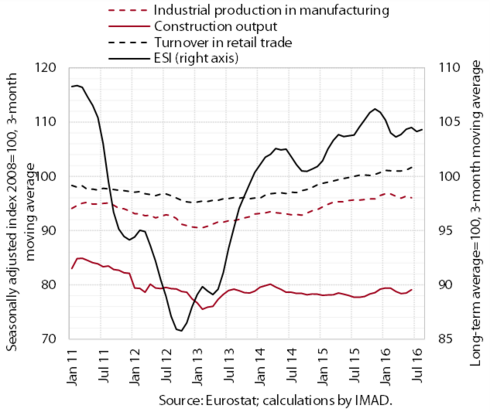

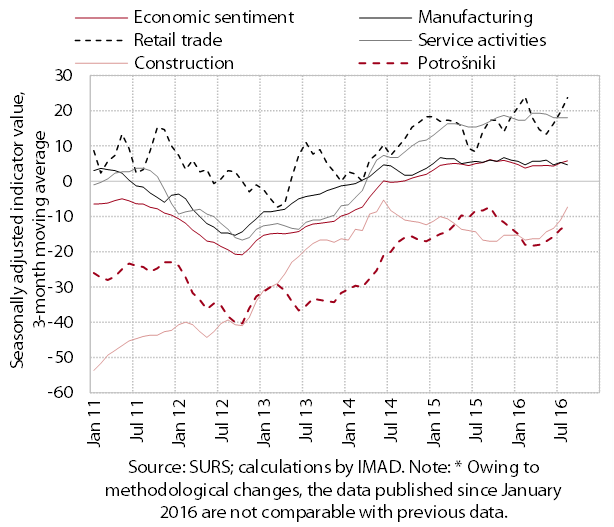

Growth prospects for the third quarter remain favourable, indicating that economic growth in the euro area will remain at around the same rate as in the second quarter. In July activity in the retail and construction industries climbed to its highest level this year, while activity in manufacturing remained similar to previous months. The Economic Sentiment Indicator (ESI) and the composite Purchasing Managers Index (PMI) for the third quarter, which remain at roughly the same levels as in the second quarter, also indicate that moderate economic growth will continue. The uncertainty caused by the United Kingdom’s decision to exit from the EU has not adversely affected confidence indicators and economic activity thus far.

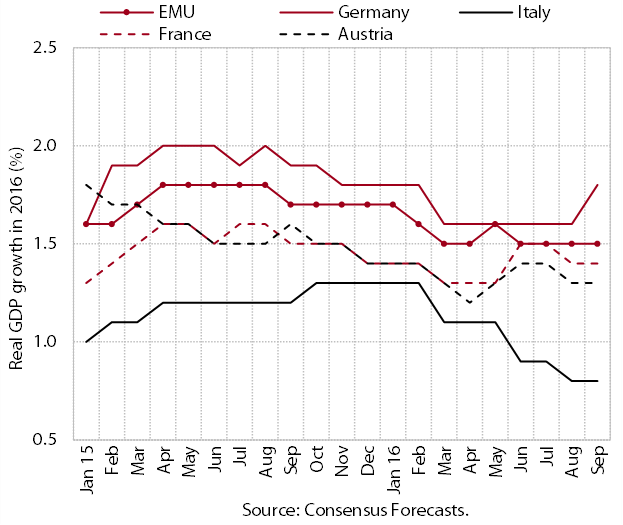

In the autumn, none of the international institutions significantly revised their forecasts for economic growth in the euro area for this year. The ECB and the IMF raised slightly their forecasts for this year’s GDP growth in the euro area (to 1.7%). The Consensus forecast has been left unchanged at 1.5% since June; the same growth is also predicted for the euro area by the OECD, which otherwise reduced its forecast slightly. For next year international institutions project slightly lower growth than this year (1.3–1.6%). The key risks to GDP growth remain tilted to the downside and arise mainly from outside the euro area (weak domestic demand, potential negative implications of the EU membership referendum in the UK.)

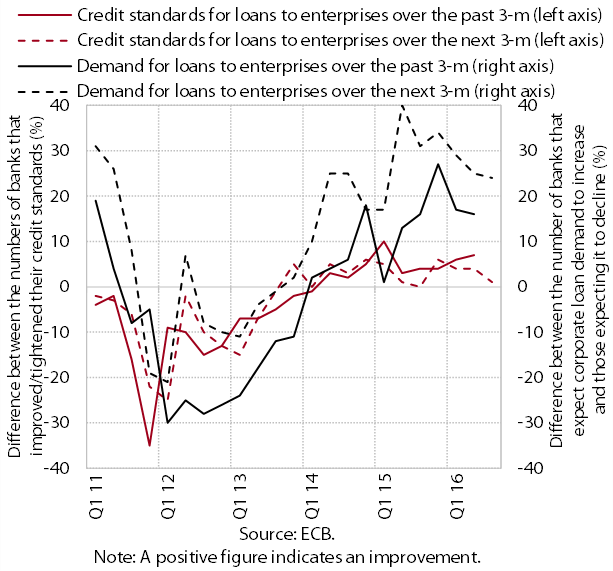

In the second quarter, credit standards for enterprises and households in the euro area improved further and the demand for all types of loans increased. The indicators of the ECB survey show an improvement in credit standards for all loan maturities and enterprise sizes and for household housing and consumer loans. The main factor behind the improvement remained competition between the banks. Net credit flows strengthened with the improvement in credit standards and higher demand; the latter is also expected to increase in the third quarter. In the first half of the year, net credit flows were higher year on year.

Most short-term indicators of economic activity in Slovenia increased further at the turn of the third quarter. Growth in merchandise exports continued, as did growth in manufacturing output, which exceeded the figures from 2008 for the first time. Turnover in market services remained high. Improving labour market conditions and growth in private consumption were reflected in further growth in some segments of trade. Turnover also expanded further in tourism-related services, which was also attributable to higher spending by foreign tourists in Slovenia. In recent months activity has also been picking up in construction, and growth prospects for this sector have continued to improve. Confidence in the economy and among consumers remains high, suggesting that these favourable trends will continue.

Real merchandise exports and imports continued to grow in July. In the seven months to July, real merchandise exports were up 5.8% year on year owing to higher exports in most manufacturing activities. Imports rose 3.7% year on year in the same period, largely as a consequence of higher imports of consumer goods related to stronger household consumption.

Growth in nominal services imports and exports slowed during the summer months. The main reason for the year-on-year growth of exports in the first seven months of the year (4.9%) was higher exports of transport and construction services, while the year-on-year growth of imports arose primarily from increased imports of technical and trade-related business services.

Production volume in manufacturing increased further in July and exceeded 2008 levels for the first time. Since the beginning of the year, production has increased the most in industries of higher technology intensity, most of which have already exceeded pre-crisis levels. Only the manufacture of other machinery and equipment still lags behind, but this has also not yet returned to pre-crisis levels in the EU. Following the decline in the second quarter, production volumes also resumed growth in medium–low-technology industries, which (with the exception of the metal industry) still lag behind their 2008 levels. The recovery remains slowest in low-technology industries, which are further away from their pre-crisis figures than their counterparts in the EU. The wider gap of these industries than in the EU is mainly due to the textile and furniture industries, where production volume has fallen by about half since 2008.

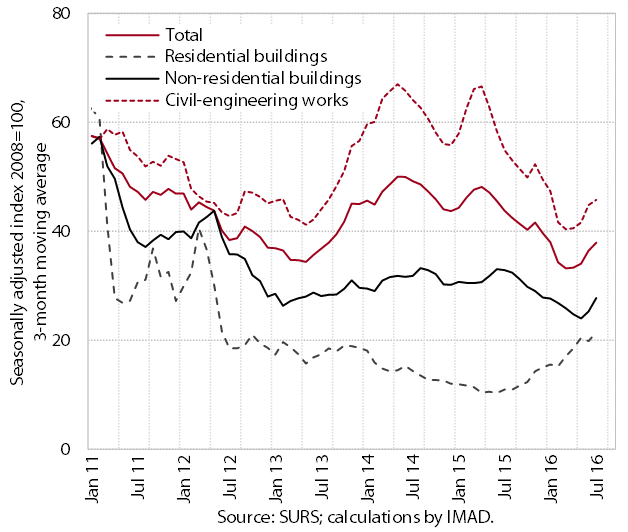

In July the value of construction completed increased for the fourth consecutive month. After the decline in construction activity in 2015 and early this year, the value of construction completed strengthened over the remainder of the year. Residential construction began to rebound in mid-2015, and activity has also recently strengthened in the construction of non-residential buildings and civil-engineering works.

The number of residential property transactions continued to strengthen in the second quarter and was almost a quarter higher year on year. The sales of existing dwellings, having already surpassed the pre-crisis level in 2015, continued to rise. The sales of newly built dwellings were also up year on year, mainly owing to further sales of dwellings from the bankruptcy estate and flats sold by the Housing Fund of the Republic of Slovenia, but were still well below the figures from 2007.

In the second quarter, residential property prices rose for the second time in a row and were up over the same quarter of 2015. Higher year-on-year prices were recorded for existing flats, which account for around two-thirds of all transactions. They were up the most in Ljubljana (by 4.2%), where the number of flats sold was the highest in nine years. The prices of new flats and all types of houses remained lower than the previous year.

Distributive trades continued to record strong sales of vehicles and other non-food products in July. Turnover in these sectors was also significantly higher than in the same period last year. The largest year-on-year increase in the first seven months was recorded for turnover in motor vehicles, which was up almost one-fifth owing to higher sales of new passenger and goods motor vehicles.typo3/#_ftn1 Sales of telecommunications, computer equipment and household appliances were also almost one-tenth higher. Turnover in the sale of automotive fuel and wholesale trade was similar to that in the same period of 2015. Food product sales remained lower year on year.

Although nominal turnover in market services continues to stagnate, it remains high. With increased spending by both domestic and foreign tourists, turnover continues to rise in accommodation and food service activities. It remains high in computer and employment servicestypo3/#_ftn1 and the transportation sector. In the latter, export revenue from land transport services is declining whereas turnover in warehousing is increasing. Turnover in telecommunicationstypo3/#_ftn2 and in architectural and engineering activitiestypo3/#_ftn3 has been falling since the beginning of the year, as well as in legal and accounting and management consultancy activitiestypo3/#_ftn4 in recent months. In the first seven months of the year, turnover was still higher year on year across most market service activities.

Road freight transport continues to stagnate. Road transport carried out entirely abroad increased further in the first quarter of 2016 under the impact of strong foreign demand. The volume of international transport (where the place of loading/unloading is in Slovenia) declined, which is partly linked to domestic factors. National transport stagnated, reflecting the weak activity in some sectors, particularly construction. After the strong growth in export orders came to an end, rail freight transport has remained at the achieved level for a long period of time.

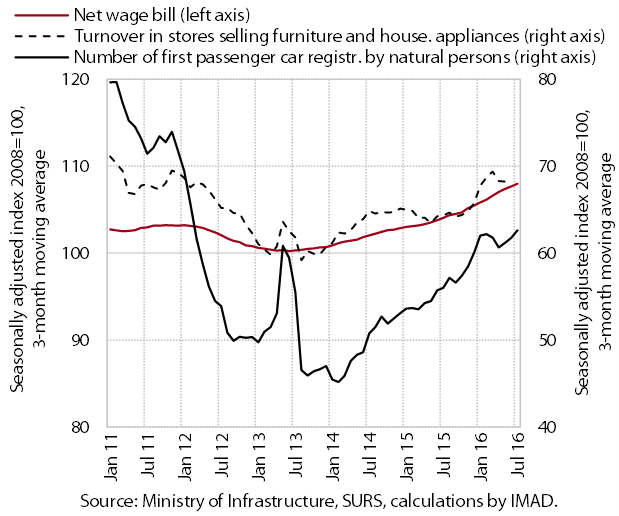

According to the indicators available, household final consumption continued to grow in July. With the growth in employee compensation and social transfers, we estimate that disposable income has continued to increase. Purchases of durable goods (vehicles and household appliances in particular) and some semi-durable goods (clothing, footwear and goods for personal care) are still rising. According to our estimates, spending on services related to tourism, leisure and recreation was also up in July.

Against the backdrop of higher confidence in the economy, the number of employed personstypo3/#_ftn1 continues to rise. The year-on-year growth in the number of employed persons in first seven months of the year was higher than in the same period of 2015, particularly in manufacturing,typo3/#_ftn2 professional, scientific and technical activities, accommodation and food service activities, and in distributive trades. With the removal of hiring restrictions, public service activities recorded stronger growth, particularly in the health sector, public administration and primary education. Expectations about employment also remain positive.

With increased hiring, registered unemployment continued to decline in the third quarter. The decline was attributable not only to the outflow into employment, which was also higher year on year in the first nine months, but also to the decreasing inflow into unemployment. This was mainly due to a lower number of first-time jobseekers and persons out of work due to business reasons or the termination of their fixed-term employment contracts. At the end of September, the number of persons registered as unemployed was 95,125, which is 9.2% less than last year.

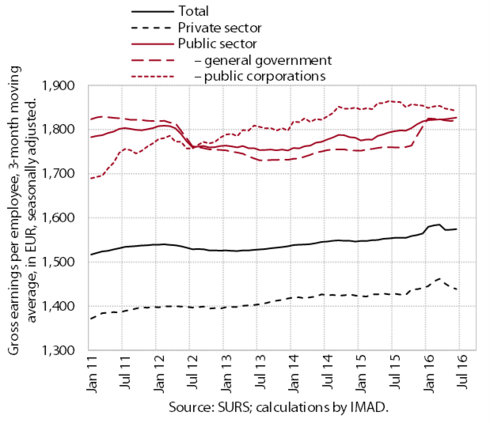

Average gross earnings did not change significantly during the period from the end of 2015 to July 2016. Extraordinary payments caused a slight upward swing in earnings in the private sector during this period, while public sector earnings remained close to their level in December, when they had risen owing to the promotions of civil servants. In the first seven months, earnings in both sectors recorded considerably higher year-on-growth than for the same period in 2015. Unlike in previous years, average earnings fell only in public corporations, where they were around one percent lower year on year.

Consumer prices have remained similar year on year. However, the prices of food and services have remained higher than in the same period of 2015. Price movements have also been affected by year-on-year declines in energy prices, but their negative contribution has decreased in recent months. Prices of durable and semi-durable goods have also remained lower. Inflation is also low in the euro area, reflecting higher prices of services and food and higher prices of durable and semi-durable goods.

Industrial producer prices and import prices remain down year on year. However, these price declines are easing on both foreign and domestic markets. On the domestic market, they are also affected by import prices, which are falling at a slower pace owing to a smaller decline in commodity and industrial producer prices in the euro area.

The current account surplus is at its highest level thus far and totalled 6.6% of estimated GDP in the twelve months to July. The main reason for its year-on-year increase in the first seven months of the year was the higher surplus in international trade in goods and services, which reflects better terms of trade and faster real growth in exports than imports. The deficit in primary income and secondary income was down year on year largely owing to the lower cost of servicing the external debt and the lower payments into the EU budget (VAT-based and GNI-based payments) respectively.

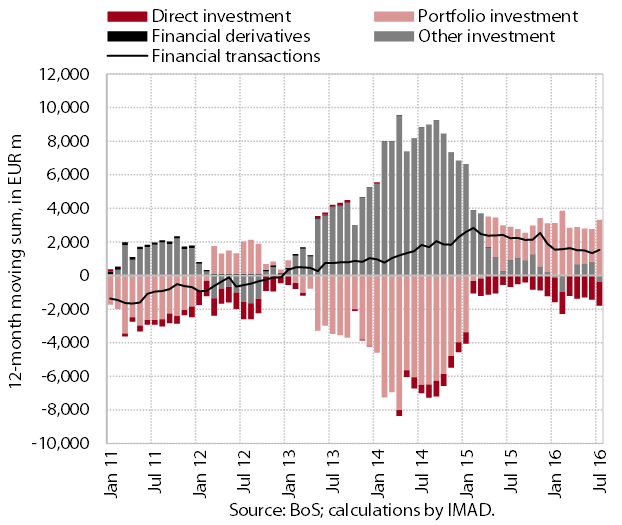

The financial account of the balance of payments recorded a net outflow in the seven months to July. The Bank of Slovenia significantly increased its financial investment in foreign securities during this period, while the government and commercial banks deleveraged abroad.typo3/#_ftn1 Direct investment inflows have remained modest since April, which is when foreign investment in the Slovenian banking sector increased. Although Slovenia still recorded a net inflow, this was mainly due to a decline in Slovenia’s direct investment abroad, both in the form of equity and debt financing.

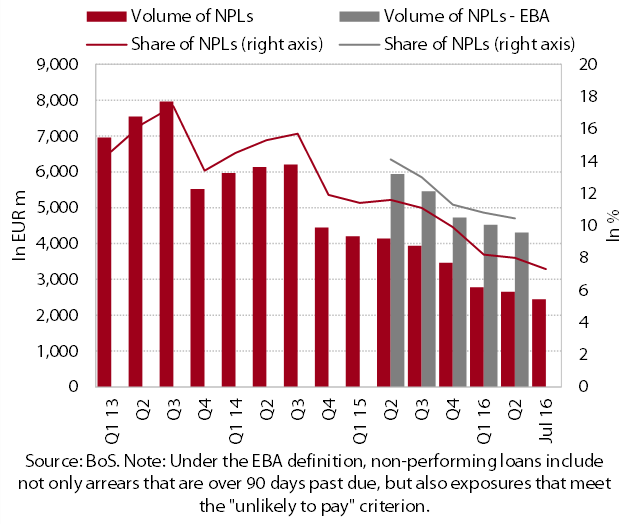

Lending activity in the Slovenian banking system remains modest amid further deleveraging of the corporate sector, while the quality of banks’ assets is improving. The volume of corporate and NFI loans continues to decline year-on-year. Owing to more favourable lending conditions, enterprises are taking out short-term loans abroad. Household loans at Slovenian banks continue to expand. According to our estimates, this is due to banks focusing more on the less risky segment of borrowers such as households, given their lower levels of indebtedness and the favourable developments on the labour market. In addition to housing loans, consumer loans therefore also rose year on year in August, for the first time since May 2010. The quality of the banks’ assets also continued to improve. This time, a significant contribution came from the sale of a portion of one of the banks’ non-performing claims.

Among the bank sources of finance available, the deposits held by domestic non-banking sectors play an increasingly important role, while the volume of inter-bank financing and liabilities to the euro-system contracts. As a result of low deposit interest rates, only overnight deposits are still rising and already account for over 60% of total non-banking sector deposits. However, we do not consider these deposits to be a sufficiently robust foundation to revive bank lending over the longer term. Lending to households has therefore been strengthening in recent months, taking the form of consumer loans, which generally have shorter maturities. Banks continue to reduce not only their liabilities to domestic and foreign banks, but also to the ECB, as there is no need for this type of funding amid the high liquidity of the banking system and weak lending activity.

The year-on-year decline in the general government deficit on a cash basis continued in the middle of the year. In the seven months to July, the deficit was EUR 235 million lower year on year, reflecting the favourable economic situation and changes in inflows from the EU budget. If interest payments are not taken into account, the general government balance recorded a surplus in the middle of the year.

General government revenue did not change significantly year on year in the first seven months. Growth in tax revenues, reflecting the favourable economic situation and labour market trends, stabilised in the middle of the year at around 3%; this was despite some one-off impacts which prevented even faster growth. The fastest growth was recorded for revenues from the corporate income tax (which contributed around two thirds to this year’s tax revenue growth) and for social contributions. Tax revenue growth was almost entirely neutralised by the fall in EU funds owing to the transition to the new financial perspective.

The year-on-year contraction in general government expenditure is largely a consequence of lower inflows from the EU budget; however, some categories of expenditure are rapidly rising. Expenditures on wages and reservestypo3/#_ftn1 are rising at the fastest pace this year. Some transfers to individualstypo3/#_ftn2 and households have also increased since the partial removal of the austerity measures. The rapid growth of expenditure on goods and services slowed in the middle of the year while expenditure on investment, subsidies and interest payments continued to fall.

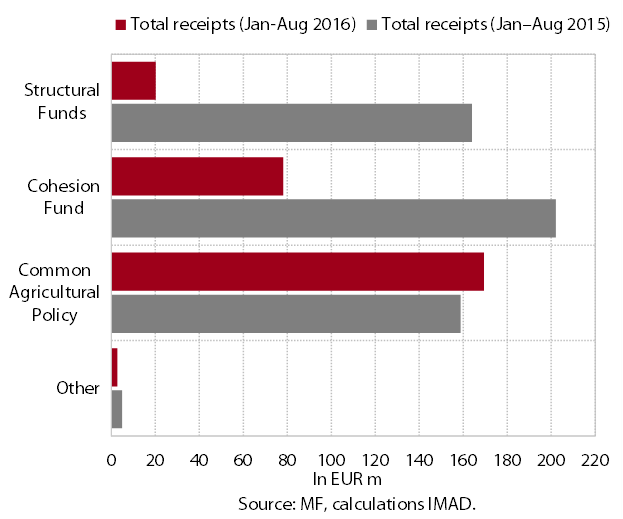

Slovenia’s net budgetary position against the EU budget was positive in the first eight months of the year and stood at EUR 24 million. Slovenia received EUR 295 million from the EU budget during this period. Over half of this total comprised receipts under the Common Agricultural and Fisheries Policy; from the Cohesion Fund and Structural funds, only the funds from the previous financial perspective were reimbursed this year (EUR 98 million in total). This year only EUR 20 million was paid from the state budget for projects under the new financial perspective. With EUR 574 million allocated for beneficiaries in the first half of the year and the value of signed contracts standing at EUR 370 million, payments are expected to increase gradually in the months to come.