Competitiveness

Slovenian Economic Mirror 5/2016

Short-term indicators of economic activity and confidence indicate that GDP growth in the euro area continued in the second quarter but is expected to be lower than in previous quarters. The United Kingdom’s referendum decision to leave the EU brings a great deal of uncertainties about the economic and political situation in Europe. In Slovenia, at the beginning of the second quarter, most short-term indicators of economic activity increased further.

Short-term indicators of economic activity and confidence indicate that GDP growth in the euro area continued in the second quarter, but is expected to be slightly lower than in previous quarters. In manufacturing, activity rose slightly in April; in retail trade and construction it has been stagnant for several months. After two months of slight growth, the value of the Economic Sentiment Indicator (ESI)typo3/#_ftn1 did not change significantly in June and remained close to the highest levels in the last few years. The manufacturing PMI indicates growth in most main trading partners.

Labour market conditions in the euro area continue to improve. In April the unemployment rate (10.2%) was around 2 percentage points lower than three years before when it had reached its high. With a further improvement on the euro area labour market, private consumption will remain the main driver of economic growth, according to the forecasts by the EC and ECB.

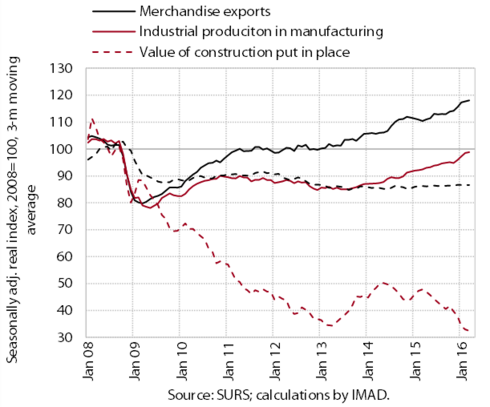

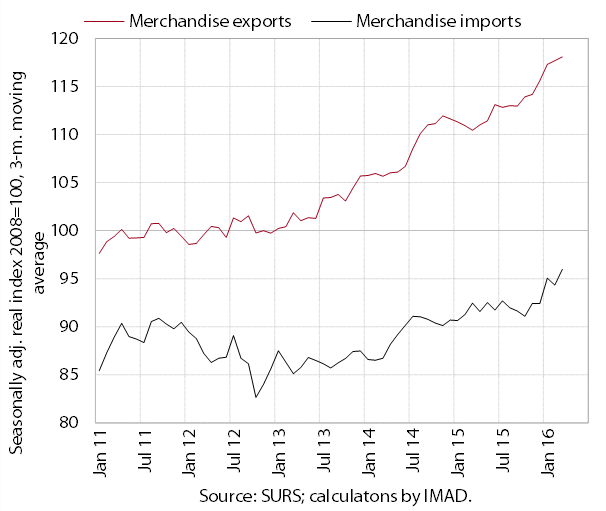

At the beginning of the second quarter, most short-term indicators of economic activity in Slovenia increased further. With favourable movements in cost competitiveness and foreign demand, merchandise exports and production volume in manufacturing continued to expand. After several months of decline, activity also rose in construction but remained low. The improvement in labour market conditions and the strengthening of private consumption contributed to further turnover growth in some segments of trade and in tourism-related services. In most other market services, turnover has not increased in the last months. The economic sentiment indicator also indicates a gradual strengthening of activity in most sectors in the next months.

Real merchandise exports and imports continued to rise in April. We estimate that this year's strong export growth stems from exports of most product groups, particularly vehicles and miscellaneous manufactured articles. Growth in merchandise imports was still mainly due to higher exports of consumer goods.

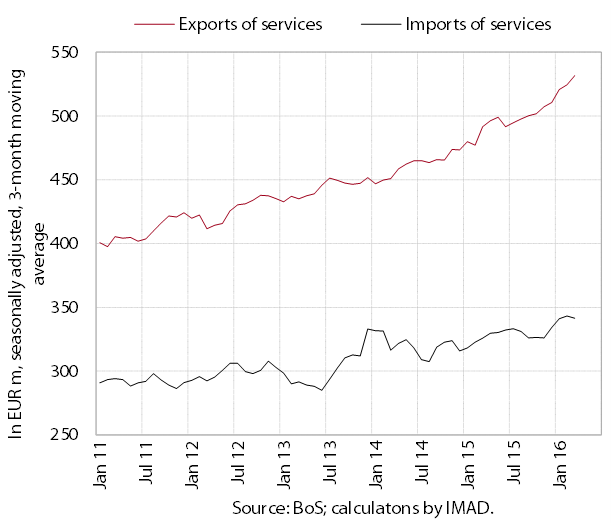

Growth in nominal exports of services continued in April, while growth in imports slowed. The year-on-year growth of exports in the first four months was mainly underpinned by stronger spending of foreign tourists in Slovenia and higher exports of transport and construction services. The year-on-year growth of imports arose primarily from higher imports of technical, trade-related business services.

Production volume in manufacturing increased further in April. It was up in more technology-intensive industries and, slightly, in low-technology industries. In medium-low-technology industries, where production increased the most at the beginning of the year, growth came to a halt, which we estimate was mainly due to the decline in the metal industry, the largest industry in this group. In the first four months, production in the metal industry was nevertheless 15.6% higher year-on-year (in April 12.6% higher) and, together with the more technology-intensive manufacture of ICT and electrical equipment (18.8% growth), made the largest contribution to the year-on-year production increase in manufacturing.

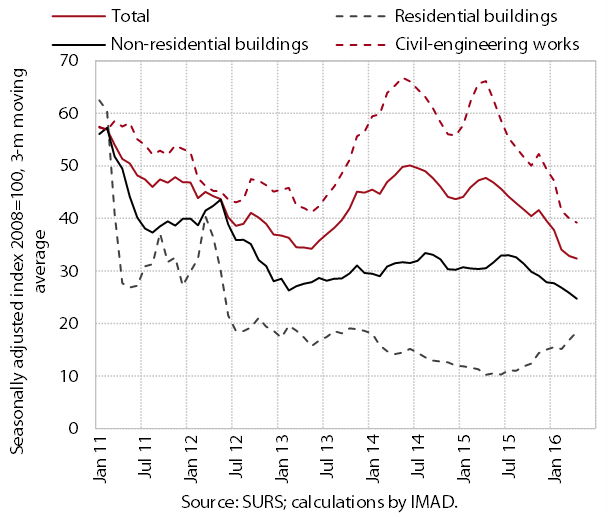

Construction activity has decreased significantly in the last year. In April the value of construction put in place rose at the monthly level but remained low. Owing to lower government investment, the value of construction put in place in civil-engineering declined considerably. Since mid-2015 only the construction of residential buildings had been rising, but remained close to last years’ lows.

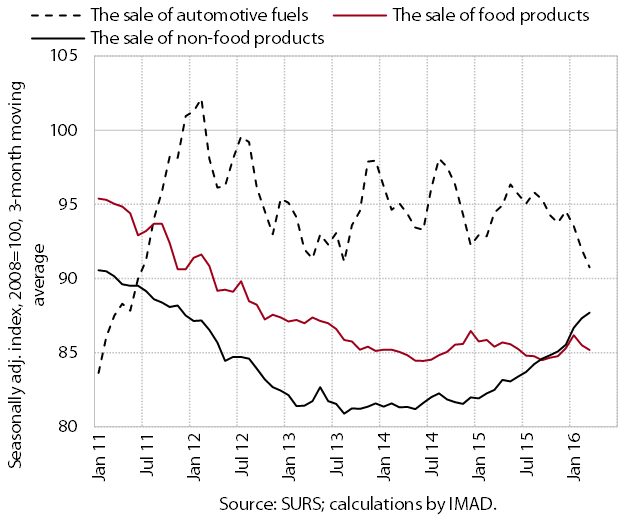

In April, distributive trades recorded further growth in the sale of vehicles and other durable and semi-durable non-food products. These segments also saw strong year-on-year turnover growth in the first four months of the year. The largest increase in turnover (of almost a quarter) was recorded for the sale of motor vehicles, owing to increased sales of new passenger and goods motor vehicles. The sales of telecommunication and computer equipment and household appliances were also higher, by around one-tenth. Nominal turnover in wholesale trade, having stagnated since summer 2015, was similar to that one year earlier. Turnover in the sale of automotive fuels and the sale of food remained lower year-on-year.

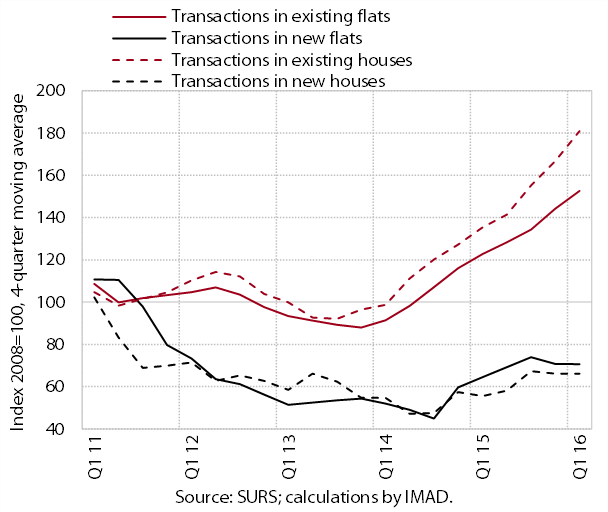

Residential property sales were up year-on-year again in the first quarter. The sales of existing residential propertiestypo3/#_ftn1 (houses and flats), which were otherwise seasonally lower than in the last quarter of 2015, were almost one-third higher. The number of transactions in newly built residential properties remained low (and slightly lower than in the same period of 2015).

Residential property prices rose in the first quarter and were up year-on-year. Prices of all dwelling types were higher than in the last quarter of 2015, except for new flats. These declined with the sale of flats from the bankruptcy estate, but remained up year-on-year. The largest year-on-year increase was observed for existing flats in Ljubljana (up 5.9%). Prices of houses remained lower year-on-year despite growth in the last two quarters.

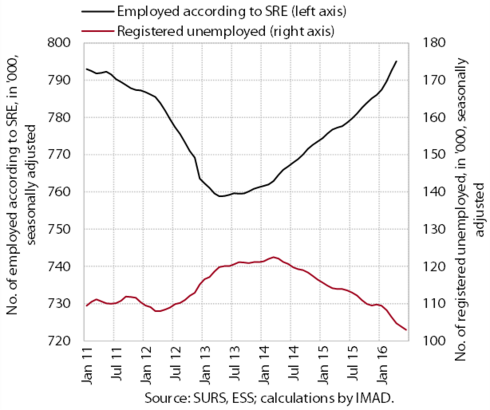

Amid higher confidence in the economy, the number of employed persons continued to increase in April. The confidence in economic recovery is also reflected in higher expectations regarding employment in the next months. Further growth in the number of employed persons was recorded in most private sector activities, again particularly in manufacturing, distributive trades, accommodation and food service activities and transportation. In public service activities, their number was higher year-on-year in the first four months, particularly in the sectors of health and education (in pre-primary and primary education).

In June the number of registered unemployed continued to decline. The main reason was the outflow from unemployment into employment, which strengthened slightly in the months to June. The outflow in the first half of the year was also larger year-on-year. The inflow into the unemployment register was smaller, largely owing to a smaller inflow of those who lost work and first-time jobseekers. At the end of June, the number of unemployed was 9.5% lower year-on-year, 99,795 persons being registered as unemployed.

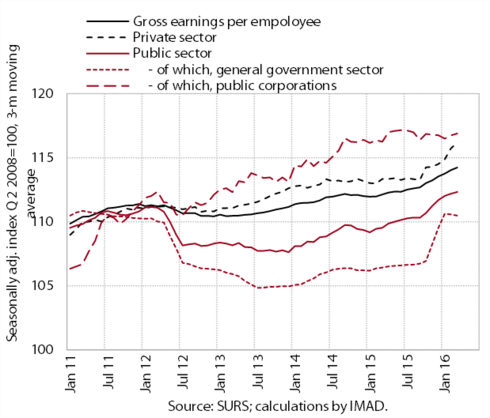

In the first four months, both sectors recorded the largest year-on-year growth of earnings in five years. After strengthening for a long period, the growth of average gross earnings per employee came to a halt in April. Private sector earnings dropped slightly, after rising notably in the last two quarters under the impact of good business performance in the previous year. Earnings in the public sector also fell somewhat, but remained similar to December when they rose owing to public servants’ promotions.

In June consumer prices rose year-on-year for the first time in one and a half years. The main contribution to growth (0.3%) came from higher prices of services; particularly the year-on-year growth of the prices of package holidays has been strengthening in the last few months. The negative contribution of energy prices was also smaller. This was reflected in core inflation, which has come close to the core inflation in the euro area in the last few months. Higher than in the same period of 2015 were also prices of semi-durable goods and, for the first time this year, food; prices of durable goods have been lower for quite some time. Similar price growth was also recorded for the euro area. It was underpinned by higher prices of services, food and semi-durable and durable goods, while the decline in energy prices has slowed in the last few months.

Industrial producer prices on the domestic and foreign markets and import prices remained down year-on-year in May. Industrial producer prices were lower particularly in the metal industry. In most other sectors prices are gradually approaching the levels of the same period in 2015; in some smaller sectors they were already higher. The decline in import prices has also slowed in the last months, owing to a smaller year-on-year fall in commodity prices on world markets.

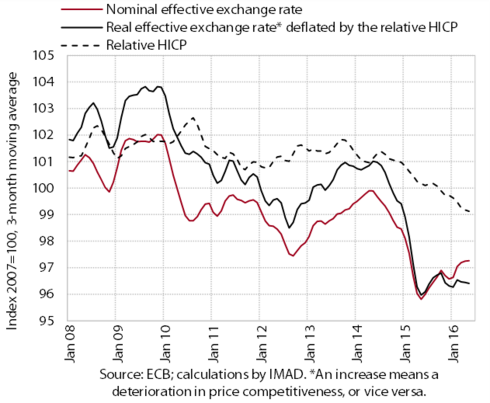

Despite the appreciation of the euro, the price competitiveness of Slovenia’s economy remains favourable. In May the appreciation of the euro against the currencies of most main trading partners continued, so that the nominal effective exchange rate increased further. However, a further decline in relative consumer prices significantly mitigated the growth of the real effective exchange rate, which therefore remained close to the lowest levels in 2015 and stimulative for Slovenian exporters.

The current account surplus widened further. In the twelve months to April, it amounted to 7.9% of estimated GDP and was the highest thus far. Its year-on-year widening in the first four months was mainly underpinned by favourable export trends, accompanied by the otherwise weak growth of imports owing to the relatively modest domestic consumption. The deficit in primary income was up year-on-year primary due to the lower receipts from the EU budget, while the deficit in secondary income was down particularly owing to the lower net payments of contributions and taxes to the rest of the world.

The financial account of the balance of payments recorded a net outflow again. In the first four months a part of the private financial sector increased financial investments in foreign securities, which is mainly linked to the excess liquidity on the domestic money market. The government repaid another portion of long-term liabilities to foreign portfolio investors. Among inflows, foreign direct investors increased investments in the Slovenian banking sector.

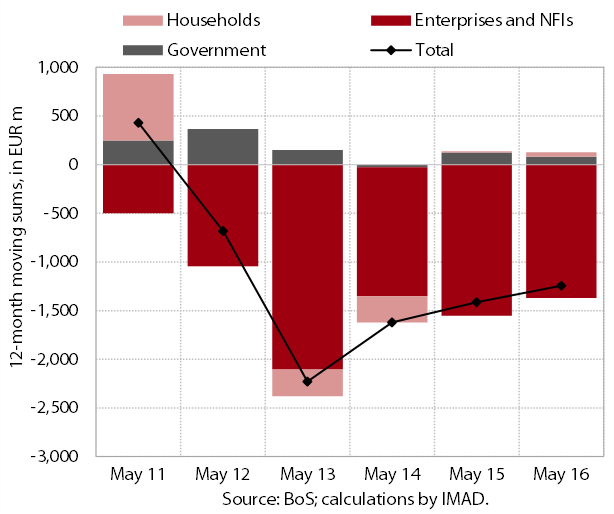

The decline in domestic non-banking sector loans is easing; the quality of banks’ assets is improving.typo3/#_ftn1 The year-on-year contraction in the volume of corporate and NFI loans continues (between EUR 1.4 billion and EUR 1.5 billion since the end of last year). Corporate and NFI deleveraging abroad is slowing, as the net inflows of short-term loans increase, while the net repayments of long-term loans decline. The volume of household loans in Slovenia’s banking system has risen slightly as a consequence of growth in new loans, while the decline in new loans to non-financial corporations has come to a halt in the last few months. The volume of non-performing claims continues to fall. At the end of April, it totalled EUR 2.7 billion and accounted for 8.0% of the banks’ total exposure, which is 3.6 percentage points less than in the same period of 2015.

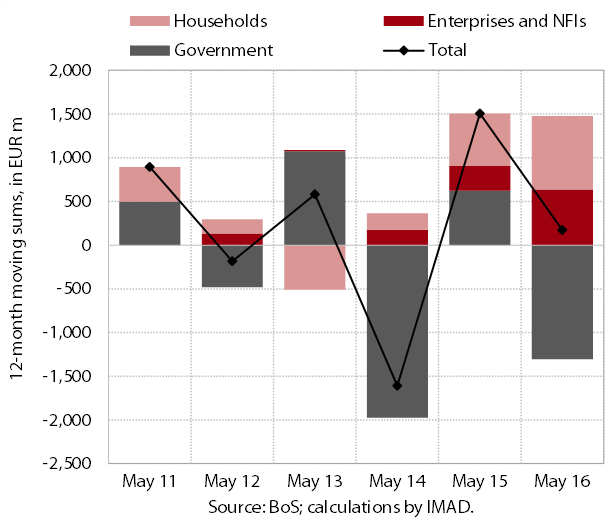

Among sources of finance, banks continue to repay their liabilities abroad while non-banking sectors increase deposits. The sum of bank debt repayments abroad in the twelve months to April dropped to EUR 1.1 billion, which is around one-fifth less than in the same period of 2015. Net repayments of loans slowed the most but still accounted for almost half of all net repayments. Similar to enterprises and NFIs, banks also recorded an inflow of short-term loans, but it was smaller. Non-banking sector deposits increased particularly owing to further growth in overnight deposits.

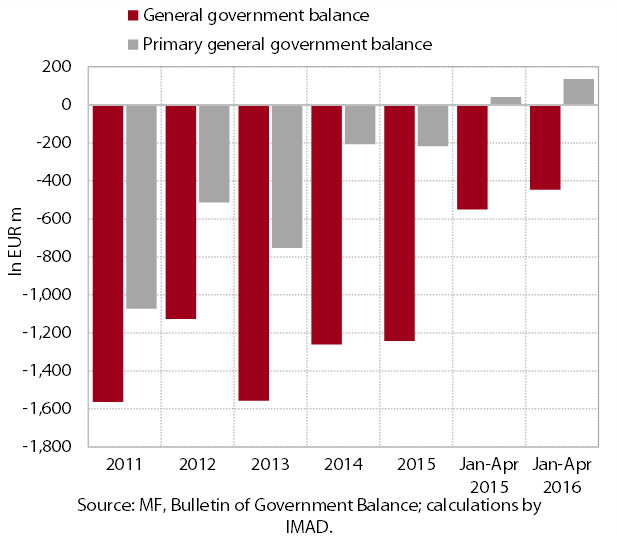

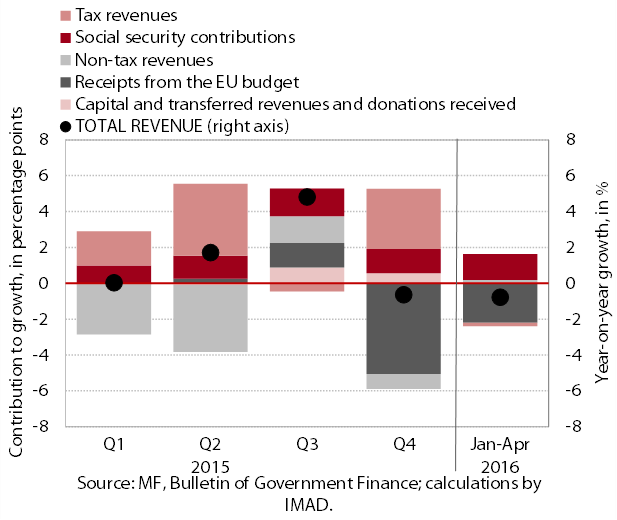

The general government deficit on a cash basis in the first four months was lower than in the same period of 2015. This was mainly related to the improvement in the economic situation and the end of the previous and the beginning of the new financial perspective of the EU.

General government revenue in the first four months was down slightly year-on-year. The bulk of its 0.8% decline stems from lower receipts from the EU budget; tax revenues also fell, but to a lesser extent. Their fall was mainly due to the postponement of the payments of corporate income tax and excise duties to May. The improvement in the economic situation shows in rising revenues from social contributions, personal income tax and VAT.

General government expenditure declined year-on-year in the first four months. The bulk of the 2.2% decline stemmed from lower investment owing to the delay in EU funds absorption at the beginning of the implementation of the new financial perspective of the EU, and lower payments into the EU budget. Slight declines were also recorded for interest expenditure (owing to the more favourable structure of public debt with regard to the interest rate) and transfers into reserves. Expenditure on goods and services was up year-on-year this year, after the containment, which was particularly pronounced at the beginning of 2015. Transfers to households were also higher, as a result of the partial removal of austerity measures.

Slovenia’s net budgetary position against the EU budget was positive in the first five months (at EUR 98 million). Slovenia received EUR 288 million from the EU budget in this period. More than half of receipts were funds paid out under the common agricultural and fisheries policies. From the cohesion fund, only the resources from the previous financial perspective were reimbursed this year (EUR 78 million); there were no reimbursements from the new perspective yet. The bulk of receipts from structural funds were paid out from the European Regional Development Fund.