Competitiveness

Slovenian Economic Mirror 4/2016

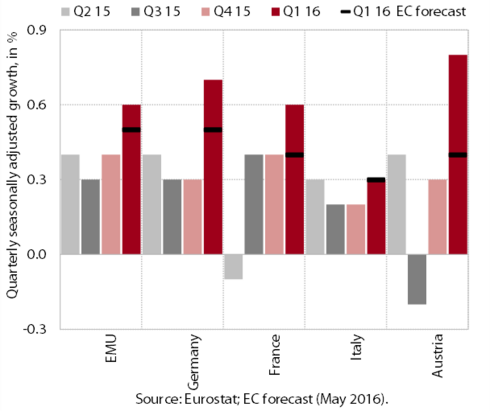

In the first quarter, economic growth in the euro area strengthened to 0.6% (seasonally adjusted) and GDP was up 1.7% year-on-year. GDP growth in Slovenia also continued in the first quarter owing to a notable strengthening of exports. The labour market situation continues to improve. In the first quarter the number of employed persons rose slightly again.

In the first quarter economic growth in the euro area accelerated and exceeded expectations. According to Eurostat’s estimate, GDP rose by 0.6% (seasonally adjusted) and was 1.7% higher year-on-year. GDP growth in the euro area and in most of Slovenia's main partners was somewhat higher than the spring expectations of the European Commission. The main driver of growth was domestic demand, particularly private consumption and investment.

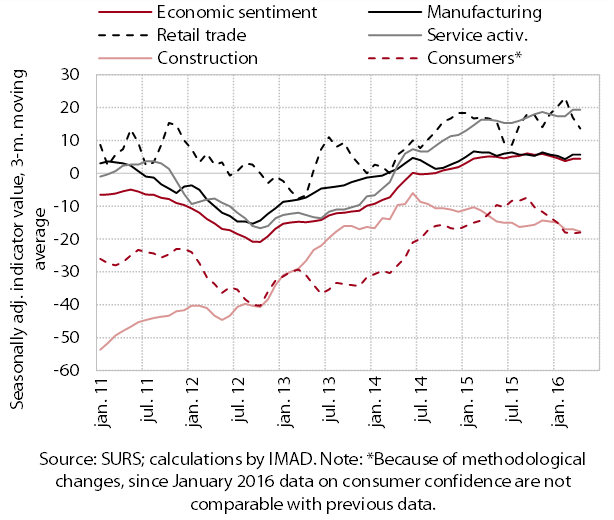

Confidence indicators indicate a moderation of economic growth in the euro area in the second quarter. The values of the Economic Sentiment Indicator (ESI) and the Purchasing Managers Index (PMI) remain similar to previous months. The Ifo Economic Climate Index for the second quarter fell to its lowest level in a year but remained above the long-term average.

After the interruption at the end of 2015, real merchandise exports rose noticeably in the first quarter; imports also increased. We estimate that exports were up in most product groups, notably transport equipment and machinery and miscellaneous manufactured articles. The growth of merchandise imports was mainly underpinned by higher imports of consumer goods.

Nominal exports of services rose further in the first quarter; imports were also up after the fall at the end of 2015. Year-on-year export growth in the first quarter was largely due to higher exports of transport services and stronger non-resident spending in Slovenia. The year-on-year growth of imports mainly stemmed from higher imports of technical services, trade-related business services, financial services and transport services.

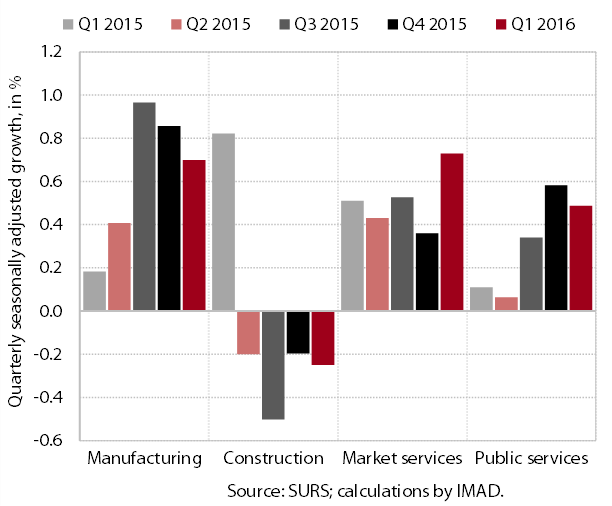

After easing at the end of last year, the growth of production volume in manufacturing strengthened in the first quarter. Production volume in medium-low-technology industries, which on average significantly exceed the levels from the same period of 2015, increased the most again. In some industries (particularly the metal and rubber industry) production volumes were also favourably impacted by low commodity prices. Year-on-year, production volume was also up in most low-technology and some more technology intensive industries. Among the latter, it was smaller in the manufacture of transport equipment (after last year’s increase) and in the chemical industry (after last year’s fall). Growth prospects for manufacturing remain favourable, as according to data on business trends, most enterprises surveyed expect further growth in demand, production and employment.

The decline in construction output deepened in the first quarter. Construction activity has plummeted in the twelve months to March. As a result of lower government investment, the value of construction put in place for civil-engineering works fell notably. Only the construction of residential buildings had strengthened since mid-2015, but remained close to the lowest levels recorded in the last few years.

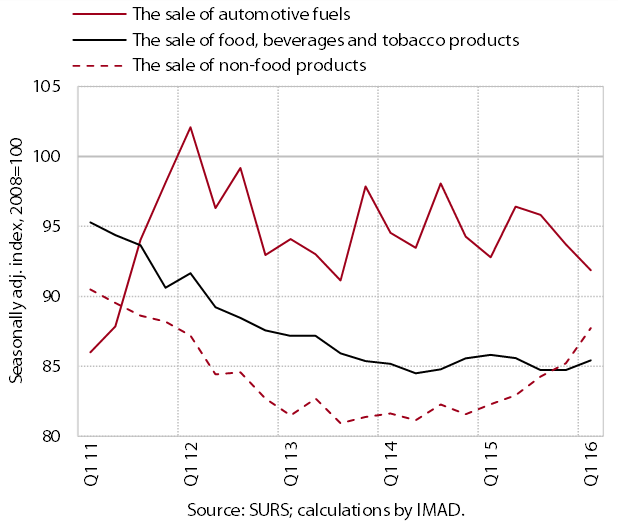

Distributive trades recorded further growth in the sale of vehicles and other durable and semi-durable non-food products. After the decline in the second half of last year, turnover also rose in wholesale trade and the sale of food products. Turnover in the sale of automotive fuels declined further. Turnover was up year-on-year in most trade segments, the most, by nearly a quarter, in the sale of motor vehicles, owing to a surge in the sale of new passenger and freight vehicles.typo3/#_ftn1

With rising sales in discount stores, the concentration ratio in stores selling food fell again in 2015. Between 2007 and 2015, discount retailers increased their combined share in total sales revenues on the Slovenian market from 6.5% to 21.2% (in the last year by 1.6 percentage points). The increase was a consequence of the expanding network of their stores, but also changes in buying behaviour of Slovenian consumers, which were also due to the economic crisis. This led to a decline in the shares of the three largest suppliers in total sales revenues and in the concentration ratio, measured by the Hirschman-Herfindahl Index, which came close to the threshold between moderate and high levels of market concentration (1,800) in 2015.

Last year’s strong growth in nominal turnover in market services decelerated in the first quarter. Amid further growth in turnover generated on foreign markets, the slowdown was mainly attributable to transport and information-communication services; activity in architectural and engineering servicestypo3/#_ftn1 also remained low. With higher sales on the domestic market attributable to growth in production activity, turnover increased further in legal-accounting and management consultancy services. Strong turnover growth in employment services, which mainly provide workers to the manufacturing sector, continues. The favourable developments in the accommodation and food service activities were boosted mainly by increased spending of foreign tourists.

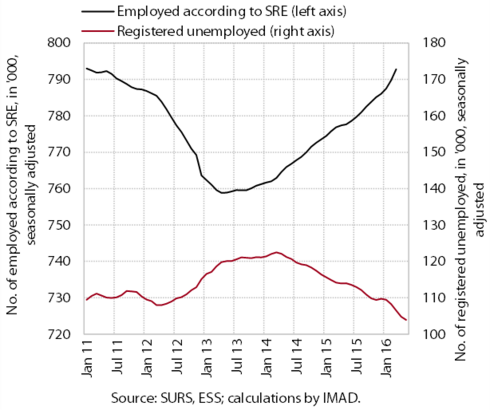

Growth in the number of employed personstypo3/#_ftn1 strengthened slightly in the first quarter. According to our estimate, this was attributable not only to growth in activity but also higher confidence in the continuation of economic recovery, which is reflected in higher expectations with regard to hiring over the next months. Further growth was recorded for most private sector activities, particularly distributive trades, transportation, accommodation and food service activities, and manufacturing.typo3/#_ftn2 In public services, the number of employed persons was higher year-on-year in the health sector and education, where it rose the most in pre-school education owing to larger generations of children. The number of employed personstypo3/#_ftn3 was also up year-on-year (by 0.9%) according to the Labour Force Survey data.

Registered unemployment continued to decline in May. The decline was mainly due to the stronger outflow from unemployment into employment, which was also up year-on-year in the first five months. The inflow into the unemployment register was smaller, largely owing to a smaller inflow of people who lost work and first-time jobseekers.typo3/#_ftn1 At the end of May, the number of unemployed was down 9.0% year-on-year; the number of registered unemployed totalled 102,289. The number of unemployed also dropped further according to the Labour Force Survey data, by 0.8%.

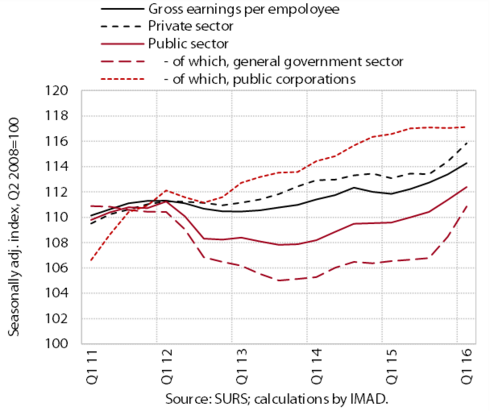

In the first quarter, growth in average gross earnings per employee strengthened further. After stagnating since mid-2014, earnings in the private sector rose notably for the second consecutive quarter owing to higher basic earnings and good business performance in the previous year. Earnings also increased in the public sector, as a result of December's promotions of public servants; in public corporations, earnings have remained unchanged in the last year. Both sectors recorded the highest year-on-year growth of earnings in five years. In the private sector, growth was up year-on-year in almost all activities. This year, earnings again rose the most in industry and, after four years, in most market services.

In May prices remained lower year-on-year. The decline was due to the falling energy prices; in the absence of cost pressures, prices of durable goods remained lower too. Prices of food and semi-durable goods remained similar year-on-year, while growth in services prices increased slightly in May. Under the impact of lower energy prices, prices also continued to fall year-on-year in the euro area. On the other hand, prices of services, food and semi-durable and durable goods remained higher year-on-year.

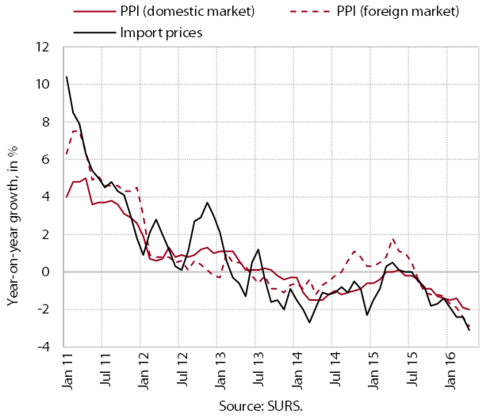

Amid a further year-on-year decline in commodity prices on global markets, import prices and industrial producer prices continued to fall in April.

Price competitiveness remains favourable, despite the deterioration at the beginning of the year. With the euro appreciating against the currencies of most main trading partners,typo3/#_ftn1 the nominal effective exchange rate is rising. Amid domestic deflation, relative consumer pricestypo3/#_ftn2 continue to decline, which has mitigated the growth of the real effective exchange rate. This was still slightly lower year-on-year in the first four months as a whole, while in most euro area countries it already increased year-on-year in the same period. The main reason for the more favourable movements in Slovenia is, alongside a larger decline in relative prices, lower growth in the nominal effective exchange rate due to the geographical structure of Slovenia’s external trade.typo3/#_ftn3

typo3/#_ftn3

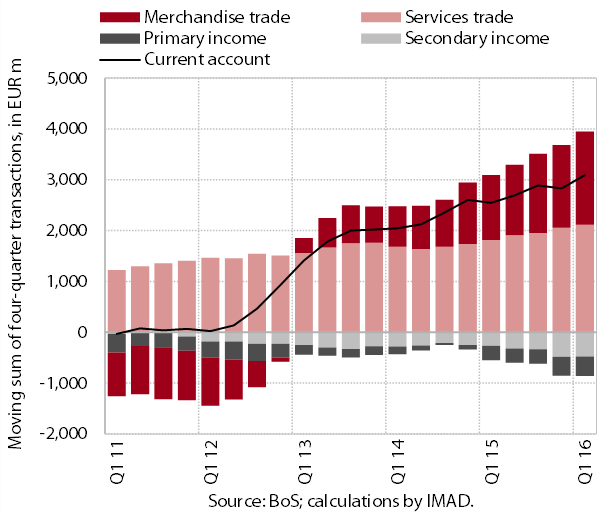

The current account surplus widened further in the first quarter and totalled 7.8% of estimated GDP in the twelve months to March. The year-on-year widening was almost entirely due to the rising surplus in external trade in goods and services, particularly as a result of favourable export trends and relatively weaker domestic consumption. The contribution of the terms of trade was positive again. Owing to the falling prices of energy and other goods, import prices declined even faster than export prices.

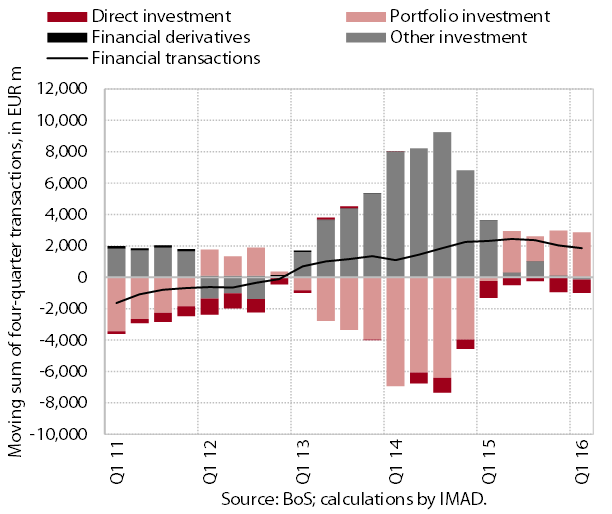

The financial account of the balance of payments recorded a net outflow again in the first quarter. The private sector was net financing the rest of the world, mainly by short-term trade credits and financial investments in foreign securities. The government increased deposits in foreign accounts and repaid a portion of foreign loans. Among inflows, the borrowing of the Bank of Slovenia from the Eurosystem increased.

Domestic non-banking sector loans are falling at a slower pace; the quality of banks’ assets is improving.typo3/#_ftn1 The contraction in the volume of corporate and NFI loans is gradually easing, while the volume of household loans is rising. This is also a consequence of growth in new loans extended to households; the decline in new loans to non-financial corporations has come to a half in the last few months. After increasing in previous months, corporate and NFI net repayments abroad eased significantly in March. In the twelve months to March they totalled just above EUR 420 million, which is almost 60% less than one year before. This significant decline was mainly due to stronger short-term borrowing, while net repayments of long-term loans remained relatively high despite the moderation. The share of non-performing claims, which continues to decline, amounted to 8.2% at the end of March.

As regards sources of finance, banks continued to repay foreign liabilities, while non-banking sectors were increasing deposits. The sum of bank debt repayments abroad in the last twelve months totalled between EUR 1.5 billion and EUR 1.5 billion, almost three-quarters more than in the same period last year. With a smaller amount of foreign liabilities scheduled to mature in the next periods and solid inflows of deposits by non-financial corporations and households, this will not represent major pressures on bank liquidity. Of non-banking sectors’ deposits, only government deposits saw a significant decline. Owing to the low deposit interest rates, overnight deposits are rising in particular (and, to a lesser extent, deposits redeemable at notice) and already account for as much as 57.5% of all domestic non-banking sectors’ deposits.

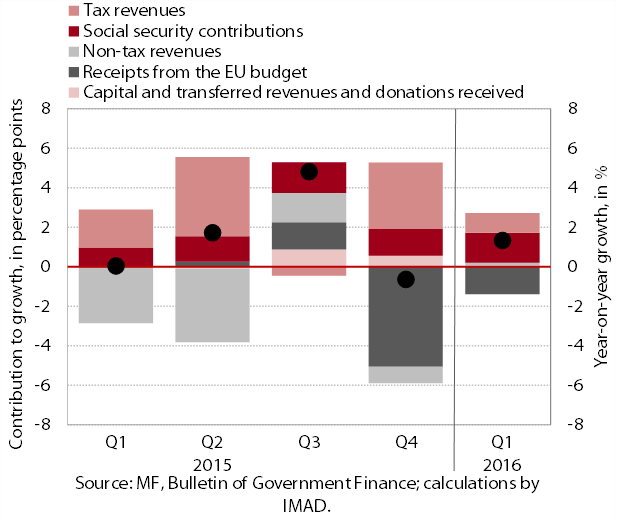

The general government deficit on a cash basis in the first quarter was lower than in the same period of 2015. The main factors in the year-on-year deficit decline (from EUR 655 million to EUR 539 million) were the strengthening of economic activity, a higher total amount of wages and the end of the previous and the beginning of the implementation of the new financial perspective of the EU (and thus lower public investment and payments into the EU budget).

General government revenue in the first quarter was slightly higher year-on-year. Its 1.3% growth arose from higher inflows of social contributions and taxes, particularly: VAT (owing to the introduction of fiscal cash registers and the strengthening of private consumption), personal income tax (owing to wage and employment growth) and corporate income tax. The payments of excise duties were down year-on-year owing to their partial postponement from March to the first days of April. The growth of tax revenues was therefore more modest. The strong receipts of EU funds in the first two months, which were related to the previous financial perspective, were followed by modest receipts in March, so that the inflows from the EU budget were lower than in the first quarter of 2015.

In the first quarter general government expenditure was slightly lower year-on-year. The bulk of the 1.6% decline stemmed from lower expenditure on investment (owing to the beginning of the implementation of the new financial perspective of the EU) and lower payments into the EU budget. Slight declines were also recorded for interest expenditure (owing to the more favourable structure of public debt with regard to the interest rate) and transfers into reserves. Transfers to households and expenditure on goods and services were higher after the year-on-year decline in the first quarter of 2015 and a partial removal of austerity measures from 2012.

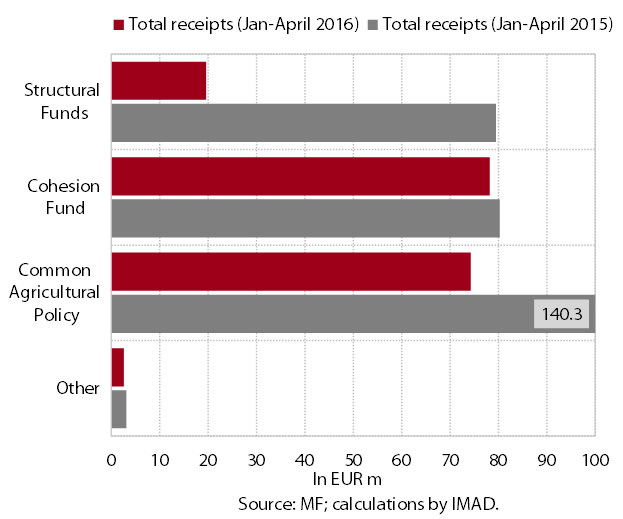

Slovenia’s net budgetary position against the EU budget was positive in the first four months (EUR 39.0 million). Slovenija received EUR 199 million from the EU budget in this period. The bulk of receipts were cohesion policy funds from the previous financial perspective (2007–2013), which were already reimbursed to the state budget in the first two months. However, Slovenia is late in preparations for the absorption from the new financial perspective (2014–2020). In May 2016 the fourth revision of the Operational Programme for the implementation of the EU Cohesion Policy was adopted; the introduction of ex-ante conditionalities,typo3/#_ftn1 i.e. pre-conditions to taken into account during the implementation of operational programmes, also poses a problem. All this is reflected in lengthy preparations and protracted procedures, particularly in infrastructure and environmental projects.