Competitiveness

Slovenian Economic Mirror 3/2016

GDP growth in the euro area continued at the beginning of the year. Activity increased further in most sectors in Slovenia at the beginning of the year. The labour market situation continues to improve. Owing to good business performance, average gross earnings per employee in the private sector rose significantly in the last four months. Export competitiveness improved further.

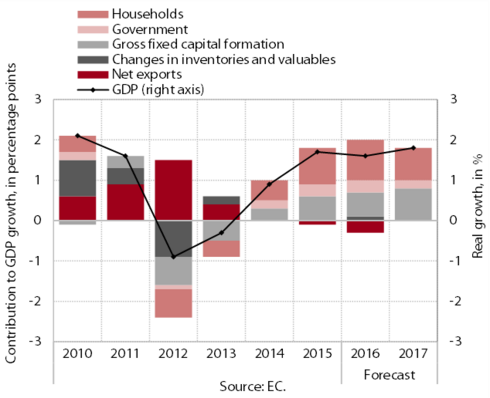

In the first quarter GDP in the euro area rose further; the EC projects that GDP growth in 2016 will be similar to last year. According to Eurostat’s preliminary flash estimate, GDP in the euro area was up by 0.6% (seasonally adjusted) in the first quarter of 2016 and by 1.6% compared with the first quarter of the previous year. In its latest forecast, the EC did not change significantly its expectations about GDP growth in the euro area in 2016 (1.6%; in February 1.7%) and 2017 (1.8%; in February 1.9%). Growth will continue to be driven by the recovery in domestic demand. The risks to the forecast remain high. They are related to the possibility of weaker growth of the global economy and trade (with a further moderation of growth in emerging economies, particularly China).

In the first quarter, lending conditions for enterprises and consumer loans in the euro area improved further. The main factor behind the improvement remained competition between banks. The indicators of the ECB survey show an improvement in credit standards for all loan maturities and enterprise sizes and for consumer loans. The credit standards on housing loans have tightened mainly owing to the implementation of the EU mortgage credit directive, which requires an in-debt assessment of the borrower’s creditworthiness. The demand for all types of loans is also expected to increase in the second quarter, which could additionally boost credit recovery. The net flow of loans to enterprises and households was positive in the first quarter.

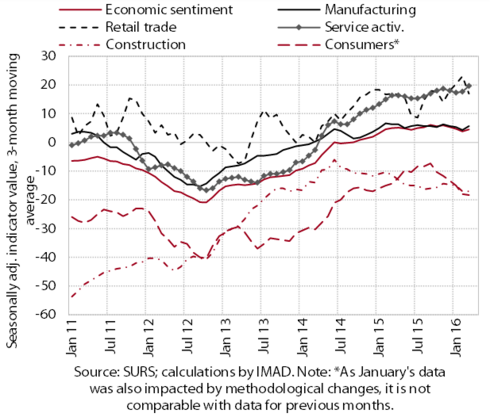

Most short-term indicators of economic activity in Slovenia improved further at the beginning of the year. Merchandise exports and production volume in manufacturing increased the most amid positive developments abroad and increased competitiveness. With the improvement in labour market conditions and the strengthening of private consumption, further growth was recorded in the trade sector and tourism-related services. Imports of consumer goods were also higher. Turnover also expanded in most other market services. In the construction sector, activity fell further, to a similarly low level as recorded in early 2013. The sentiment indicator indicates a continuation of the gradual strengthening of activity in most sectors.

Growth in merchandise exports strengthened in the first two months; importstypo3/#_ftn1 also rose after hovering at the achieved level for a long period. Exports of most products increased at the beginning of the year, particularly motor vehicles and metal and chemical industry products. Import growth in the last few months was largely a consequence of higher imports of consumer goods.

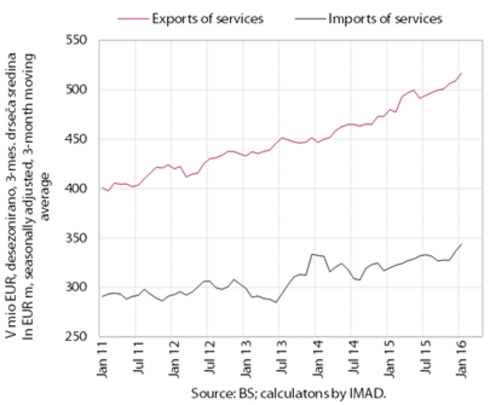

In February services exports continued to increase; imports were also strengthening over the last few months. The year-on-year growth of exports in the first two months was underpinned by higher exports of transport services, higher spending of foreign tourists and exports of telecommunication and computer services. The year-on-year growth of imports mainly stemmed from higher imports of technical services, services related to trade, administrative and support services, financial services and transport services.

Production volume in manufacturing rose significantly at the beginning of the year. In February it increased further in all categories of technological intensity, particularly in medium-low-technology industries. The majority of these industries exceeded last year's levels; production was also up year-on-year in most other sectors. After last year’s strong growth, only the production of transport equipment recorded a significant decline, but, similar to the production of most other technologically more intensive industries, it exceeded the levels of 2008.

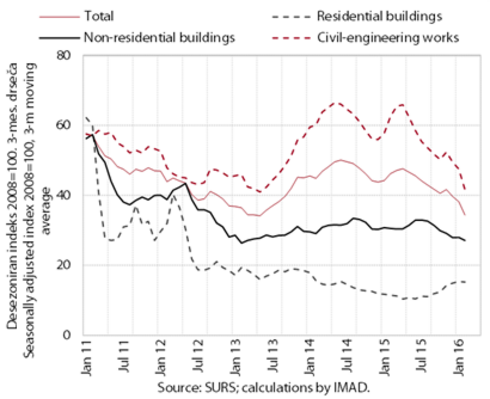

The value of construction put in place dropped strongly at the beginning of the year. In the last twelve months, construction activity was dwindling. As a result of lower government investment, the value of construction put in place for civil-engineering works fell notably. Since mid-2014 only the construction of residential buildings had been rising, but remained close to the lowest levels recorded in the last years.

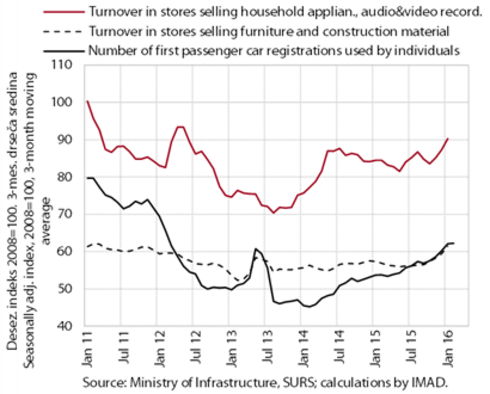

At the beginning of the year, turnover rose across most trade segments, the most in the sale of motor vehicles and non-food products, where the sales of household appliances, computer and telecommunication equipment, furniture, textile, clothing and footwear increased in particular. After stagnating at the end of last year, turnover also rose in the sale of food products and wholesale trade, while it continued to drop in the sale of automotive fuels. In the first two months, the largest year-on-year increase, of nearly a quarter, was recorded for turnover in the sale of motor vehicles, owing to a surge in the sale of new passenger and freight vehicles.

In February most market services recorded further nominal turnover growth. Turnover growth in transportation and communication services slowed in the last months. We estimate that the moderation was mainly attributable to the sales on the domestic market, as the sales on foreign markets are rising. Higher sales on the domestic market contributed to further turnover growth in legal-accounting, management-consultancy and employment services and in accommodation and food service activities.

Growth in the volume of road freight transport slowed last year. International road transport recorded a significant increase, particularly transport abroad, the segment that is the most dependent on foreign demand. The volume of national transport, which is more related to domestic factors, increased only slightly amid modest activity in some sectors (particularly construction). In the year as a whole, road freight transport rose by a tenth. Railway freight transport maintained the achieved level after the moderation of the strong growth of export orders for transport services.

Household spending rose further at the beginning of the year. With stronger growth in the net wage bill, purchases of durable and semi-durable goods increased further. Purchases of non-durable goods had also risen since the end of last year. Expenditure on tourism-related services continued to grow. Imports of consumer goods were also up.

After the deterioration in the first quarter, confidence indicators improved in most activities and among consumers.

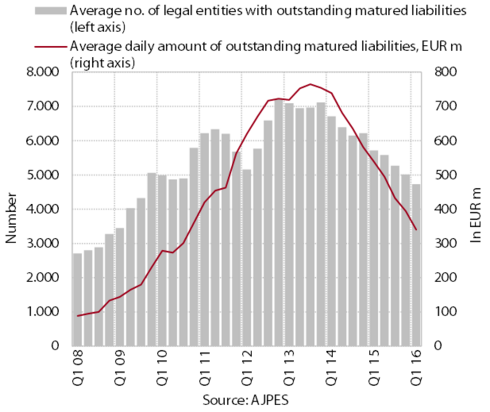

In the first quarter, solvency improved further. The number of non-payers and the amount of outstanding liabilities of legal entities and sole proprietors declined year-on-year and payment delays shortened. The average number of sole proprietors with outstanding liabilities for more than 5 days in a month was the lowest since 2010. Long-term outstanding liabilities remained high, accounting for 75% of all outstanding liabilities of legal entities and 79% of all outstanding liabilities of sole proprietors. The mutual indebtedness of business entities decreased as a result of set-offs. Together with the round of compulsory and voluntary set-offs that took place in March, the mutual indebtedness of business entities declined by EUR 2.7 billion in the period since April 2011.

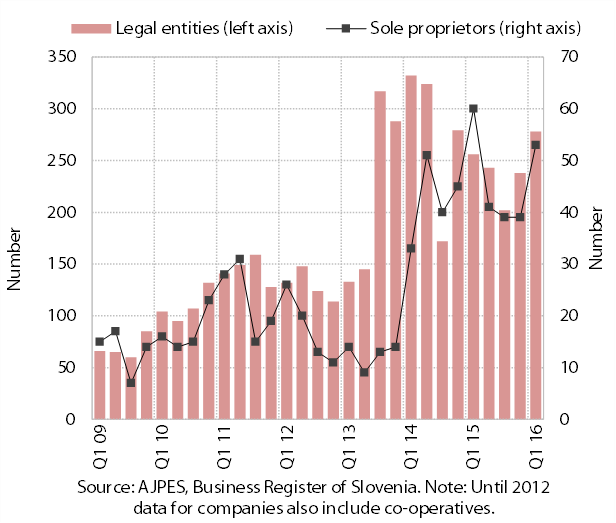

The number of bankruptcy proceedings filed against legal entities and sole proprietors has been rising since the middle of 2015; the number of personal bankruptcy filings remains high. The most bankruptcy proceedings against legal entities and sole proprietors were again filed in distributive trades and construction and, in sole proprietors, in accommodation and food service activities. After the adoption of the legislative amendment that exempted all bankruptcy petitioners from depositing an advance, personal bankruptcy filings surged. In the first quarter of 2016, 1,073 personal bankruptcies were filed, but the amount of reported claims was more than half lower than in the same period last year.

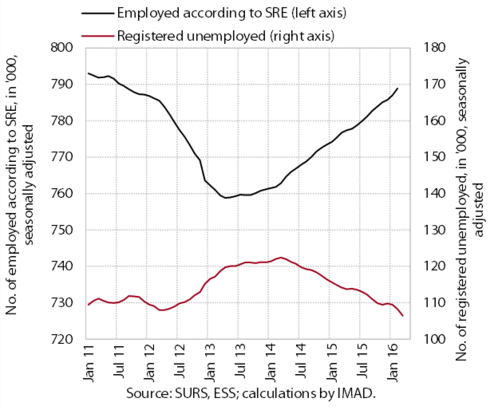

At the beginning of the year, the number of employed persons continued to grow. Reflecting activity growth, in February their number rose further in most private sector activities, notably manufacturing, the sector to which most of the employment services workers were assigned according to our estimate. It also increased further in most market services, where the total number of employed exceeded the number recorded before the crisis. Year-on-year, the number of employed was up particularly in medium-low technology manufacturing and transportation, accommodation and food service activities, and distributive trades. In public services it was up year-on-year particularly in the health sector; in education, it rose the most in pre-school and basic education, also owing to larger generations of children.

In April registered unemployment continued to decline. The more notable decline in the last months was mainly attributable to the stronger outflow into employment, which was also up year-on-year in the first four months of 2016. The inflow into unemployment due to job loss and the inflow of first-time jobseekers were also smaller. At the end of April, the number of unemployed was down 8.2% year-on-year; the number of registered unemployed totalled 105,453.

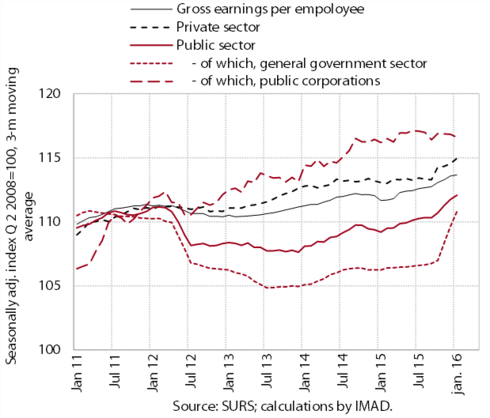

After stagnating for one and a half years, average gross earnings in the private sector rose significantly in the last four months under the impact of past business performance. After two years of modest growth, earnings in the public sector continued to rise mainly owing to growth in public corporations; in the general government, they maintained the high level reached at the end of the year as a result of promotions and overtime and extraordinary payments related to the increased inflows of refugees and migrants. In the first two months, private and public sector earnings recorded the highest year-on-year growth in five years.

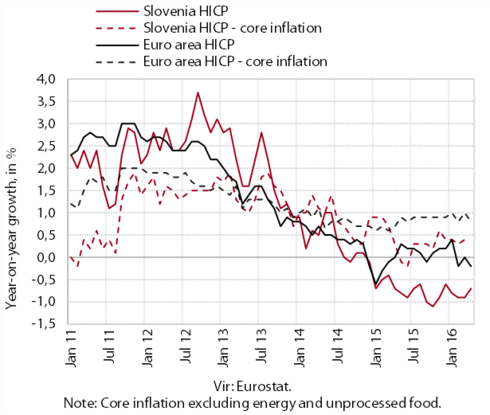

In April prices remained down year-on-year primarily owing to lower oil prices on global markets. In the absence of cost pressures, prices of durable goods stayed lower year-on-year, while food prices were similar to those in the same period last year. The growth of services and semi-durable goods prices strengthened slightly in April, but remained modest. Prices in the euro area were also down year-on-year in April. With lower energy prices in year-on-year terms, this was also attributable to the lower growth of services prices compared to previous months. Prices of food and semi-durable and durable goods remained up year-on-year.

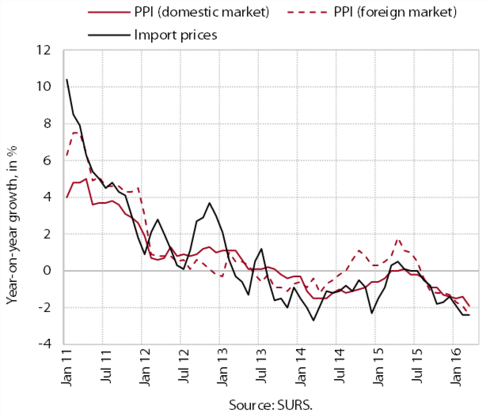

Amid lower commodity prices on world markets, the year-on-year declines in import prices and industrial producer prices deepened at the beginning of the year.

Price competitiveness remained favourable for exporters in the first quarter. The real effective exchange rate deflated by the relative HICP rose slightly owing to the appreciation of the euro against the currencies of most main trading partners, but its real value remained close to last year’s lowest levels since Slovenia’s entry into the ERMII in 2004 or the adoption of the euro in 2007. At the year-on-year level, price competitiveness improved further, reflecting the decline in relative prices, one of the largest in the euro area.

Last year cost competitiveness improved further. The improvement was attributable mainly to the decline in the exchange rate of the euro and partly to relative unit labour costs. In terms of cost competitiveness gains as measured by the real effective exchange rate, Slovenia ranked in the middle of countries in the euro area. The decline in the nominal effective exchange rate was smaller than in most other euro area countries because of the geographical structure of Slovenia’s trade. In contrast, the decline in relative costs was one of the largest in the euro area.

Last year Slovenia offset the loss in cost competitiveness relative to the euro area experienced in the first years of the crisis. This was a consequence of the relatively faster growth of labour productivity in the last few years. The total increase in real unit costs since the beginning of the crisis was still slightly higher than the EU average, but the gap narrowed.

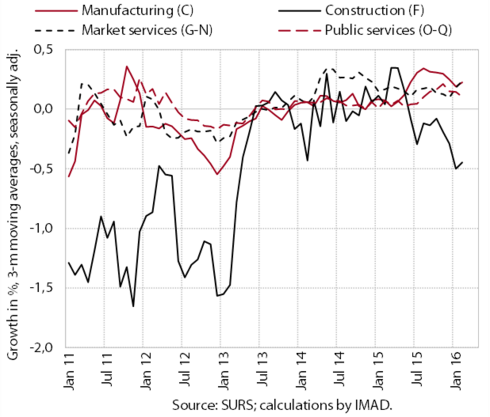

Last year, too, the improvement in cost competitiveness mainly stemmed from the tradable sector, particularly manufacturing, but also distributive trades, accommodation and food service activities and transportation. The improvement was a consequence of growth in value added amid a more moderate increase in employment and modest wage growth. In manufacturing the level of real unit labour costs had already been lower than in 2007 since the first quarter of 2015. Their position relative to the pre-crisis period was also better in comparison with the euro area and the EU.

The current account surplus widened further. In the twelve months to February, it totalled 7.9% of estimated GDP. The year-on-year widening in the first two months was mainly underpinned by growth in the surplus in international trade in goods and services, which was, amid weak import growth, mainly due to the continuation of favourable export trends. The deficit in primary income was lower mainly on account of smaller net payment of interest on external debt, while the deficit in secondary income narrowed owing to lower payments into the EU budget.

The financial account of the balance of payments recorded a net outflow again in February. The government repaid another portion of its long-term liabilities to foreign portfolio investors. The private sector was net financing the rest of the world, mainly by short-term trade credits, which is related to growth in exports of goods and services. Among inflows, the borrowing of the Bank of Slovenia from the Eurosystem increased.

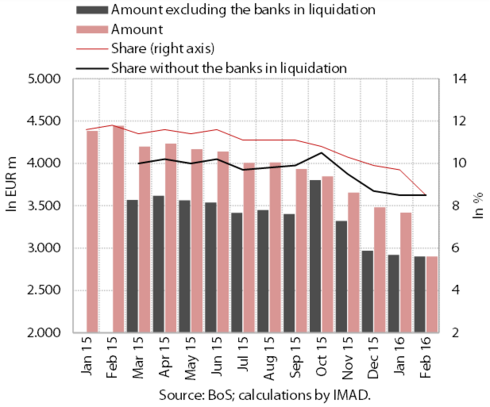

The decline in the volume of domestic non-banking sector loans remained relatively strong in March. Loan volume was down EUR 1.7 billion in the last 12 months. Not taking into account the liquidation of two smaller banks, the deleveraging would be similar to that recorded one year before (EUR 1.3 billion), according to our estimate. Government loans expanded, while household loans declined slightly despite the growth of housing loans. Corporate and NFI deleveraging abroad rose somewhat in the last months owing to higher net repayments of long-term loans. In February it exceeded EUR 810 million year-on-year, and was around 3% higher than in the comparable period of 2015. The share of non-performing claims declined significantly again in February, to 8.5%, which was a consequence of the liquidation of two smaller banks.

Looking at sources of finance, banks continued to repay foreign liabilities, while deposits were rising more slowly than in the same period of the previous year. Banks repaid EUR 1.5 billion in foreign liabilities in the twelve months to February, which is around 65% more than in the comparable period one year before. Around two thirds of net repayments were recorded in the first six months of this period. Around 45% of net repayments were accounted for by foreign credits, the rest by deposits and bonds. The increase in deposits by domestic non-banking sectors was smaller year-on-year in March, mainly owing to the net outflow of government deposits and partly due to a smaller net inflow of household deposits. The net inflow of corporate deposits in banks rose. The maturity structure of deposits continued to deteriorate gradually, given that overnight deposits increased the most; deposits redeemable at notice rose slightly.

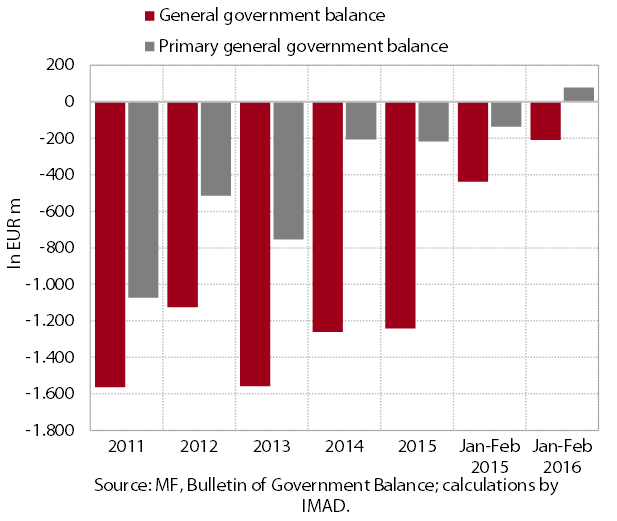

The general government deficit on a cash basis in the first two months was significantly lower than in the same period of 2015. The half lower deficit (EUR 209 million) is related to the expiry of the previous perspective and the beginning of the implementation of the new financial perspective of the EU, growth in earnings and employment and favourable borrowing conditions.

General government revenue was 5% higher year-on-year in the first two months. Half of the increase stemmed from higher tax revenues – particularly from unallocated revenues, which were, for technical reasons, recorded as negative in the first two months of 2015. Revenues from excise duties and VAT were lower owing to the lower rates of excise duty on energy, a decline in the sale of tobacco products and higher deductions of input VAT. The increase in total revenue was also due to higher payments of social contributions and higher receipts from the EU budget related to the previous financial perspective.

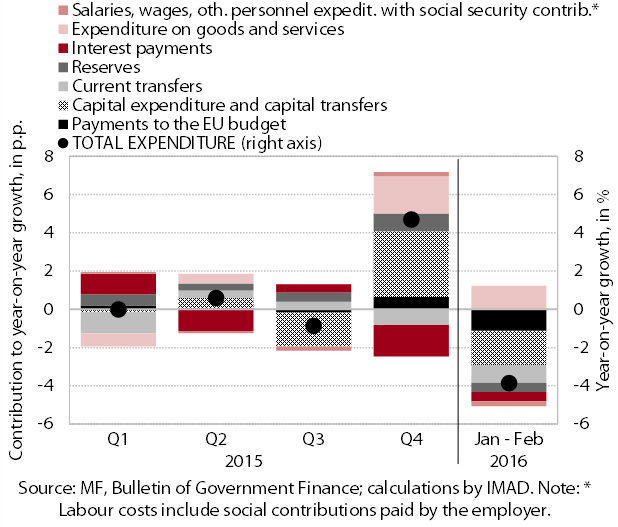

General government expenditure in the first two months was 3.8% lower year-on-year. All main categories of expenditure were down, except expenditure on goods and services, and transfers to households, where austerity measures from 2012 were partly removed. The year-on-year decline in expenditure mainly stemmed from: (i) lower investment expenditure at the beginning of the implementation of the new financial perspective of the EU; (ii) lower payments into the EU budget, where last year additional funds for the implementation of the common agricultural policy had been called; (iii) lower payments of subsidies; and (iv) a delay in the proper recording of transfers into social security funds.

Slovenia’s net budgetary position against the EU budget was positive in the first quarter (EUR 15.7 million). Receipts from the EU budget (EUR 155.6 million) involved funds from the previous financial period (2007–2013), which officially came to an end in 2015. Slovenia’s payments into the EU budget stood at EUR 139.9 million in the same period.