Competitiveness

Slovenian Economic Mirror 2/2017

Boosted by foreign and domestic demand, the favourable trends in economic activity continued in Slovenia at the turn of the year; the outlook also remains encouraging. Under the influence of rising economic activity, the growth of employment and the moderate wage growth continue. Consumer price growth strengthened in the first months of the year, reflecting supply-side factors and a further pick-up in consumption. Loan volume was higher year on year in February for the first time in five and a half years; the maturity structure of sources of finance remains unfavourable. In January the general government budget was almost balanced.

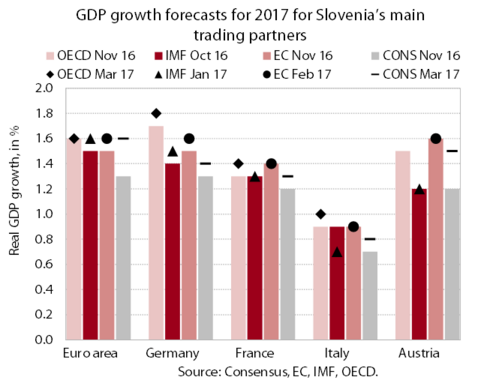

International institutions continue to raise their forecasts for GDP growth in 2017 and 2018 for Slovenia’s main trading partners. The latest forecasts for real GDP growth are for the most part slightly more positive than the autumn ones, a consequence of the expected stronger recovery in global economic growth and trade and the more favourable economic climate. The favourable prospects continue to be subject to risks, however, primarily associated with political uncertainty and global challenges.

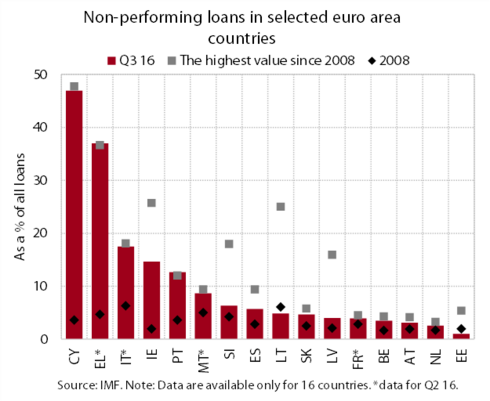

Lending conditions for enterprises and households in the euro area are improving amid the ECB’s expansionary monetary policy, which is reflected in the strengthening of positive credit flows. The resilience of the banking sector in the euro area is increasing, but the weak profitability of banks and the high levels of non-performing loans remain a concern. Non-performing loans are in fact declining, but in many Member States their level remains high.

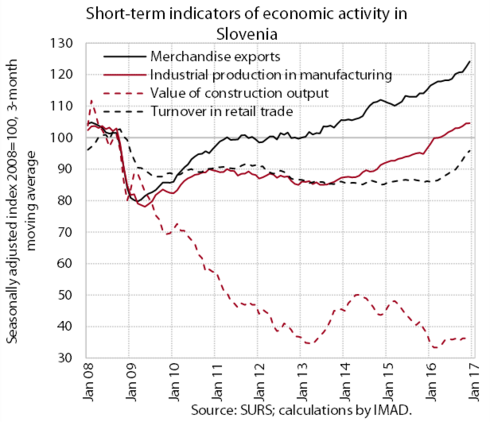

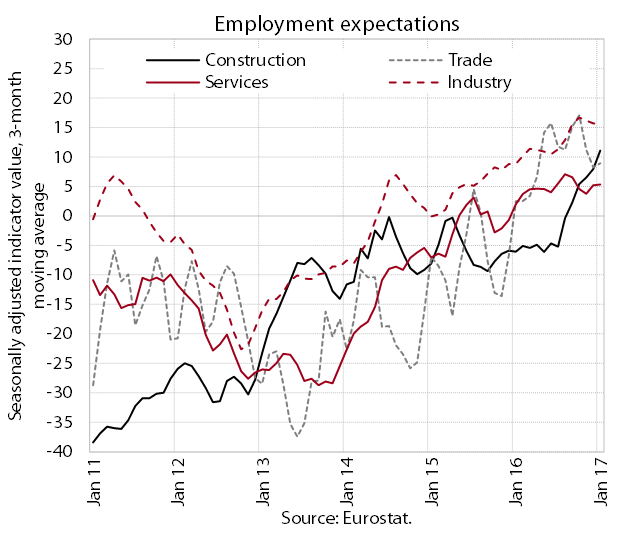

At the turn of the year, the favourable trends in economic activity continued. The growth in exports and manufacturing production continued amid the strengthening of foreign demand and the preservation of the favourable competitive position. Favourable labour market developments bolstered private consumption and significantly contributed to turnover growth in distributive trades and in services mainly related to leisure; this was also attributable to the higher number of foreign tourists. The strengthening of domestic demand and exports also contributed to further turnover growth in other market services. Only activity in construction remained modest, this as a result of low government investment. Economic sentiment continues to strengthen and points to a continuation of positive trends.

Real growth in merchandise exports and imports strengthened at the turn of the year. Export growth continues to reflect foreign demand and the ability of manufacturing enterprises to maintain their favourable competitive position. Expectations about future exports and orders in manufacturing have also remained positive. Exports of all main groups of manufactured goods, particularly machinery and chemical products, were rising at the end of 2016. The growth in imports is also increasing alongside favourable export movements and growth in domestic and investment consumption.

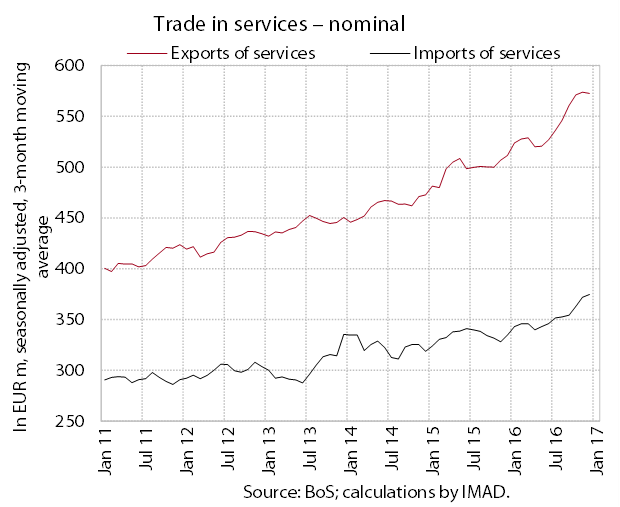

Nominal exports and imports of services remained high (seasonally adjusted). Exports and imports were up 13.8% and 8.0% year on year respectively. The year-on-year growth of both exports and imports was mainly due to transport and other business services.

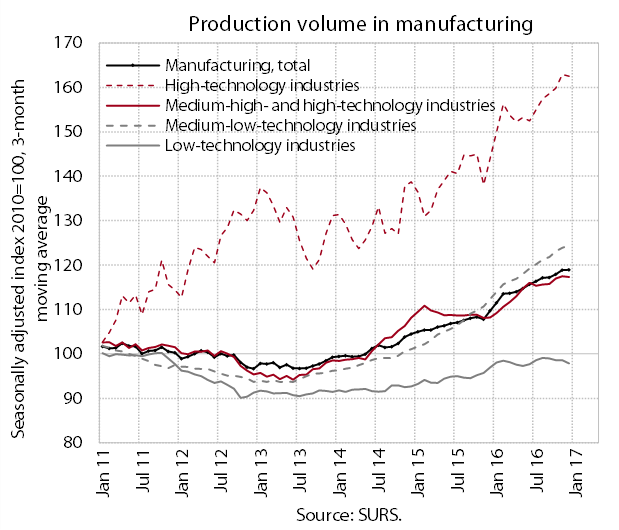

Production volume in manufacturing remained high at the beginning of the year. In all categories of technology intensity, production volumes were similar to those at the end of last year. In the last year, production has risen the most in the most export-oriented high-technology industries, particularly the manufacture of ICT equipment. The prospects for the first half of the year are favourable, with most manufacturing enterprises expecting a strengthening of demand, production and employment.

The value of construction output has remained more or less unchanged since the second quarter of 2016, though with considerable monthly fluctuations. Activity in 2016 and at the beginning of 2017 was significantly lower than in 2015, which is related particularly to low government investment and in January to unfavourable weather conditions. Amid the general improvement in economic conditions and a gradual rebound in the property market, the construction of flats and the construction of non-residential buildings started to pick up at the end of 2015 and mid-2016 respectively. Data on issued building permits show that favourable trends in the construction of buildings will continue.

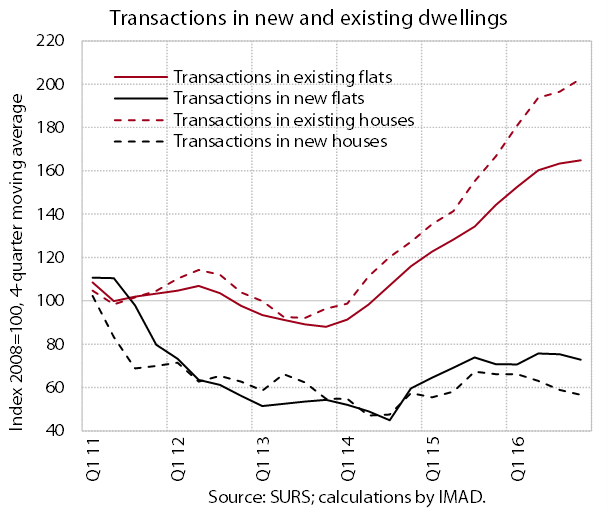

Sales of residential properties strengthened further last year. Sales of existing residential properties, which had already exceeded their 2007 peak in 2015, were up 16%. Sales of new residential properties remained at a similarly low level to that recorded in the previous year. We estimate that the rebound in the real estate market was due to the improvement in the economic situation and hence the recovery of labour market conditions, the relatively low effective interest rates on housing loans and the still relatively low prices.

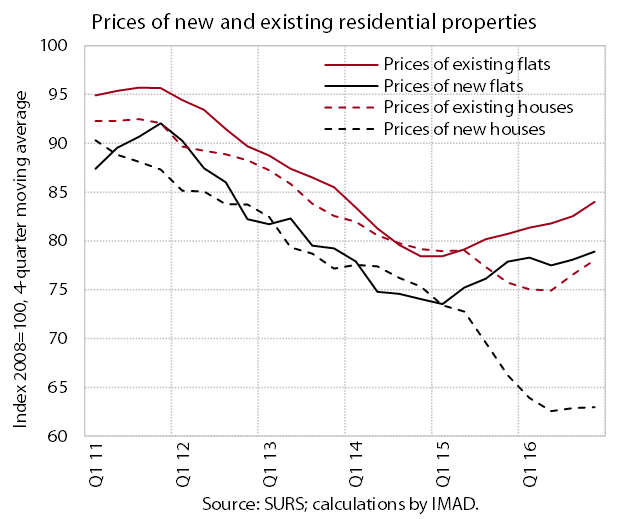

Prices in most residential property categories rose last year. On average, they were up 3.3% year on year. The prices of existing flats increased the most in Ljubljana (by 6.0%). The prices of new flats were also up year on year under the influence of transactions in more expensive flats (i.e. flats sold in areas of high demand and luxury flats). The prices of new flats from bankruptcy estates were mostly lower. The prices of existing houses were also higher last year, this following seven years of decline.

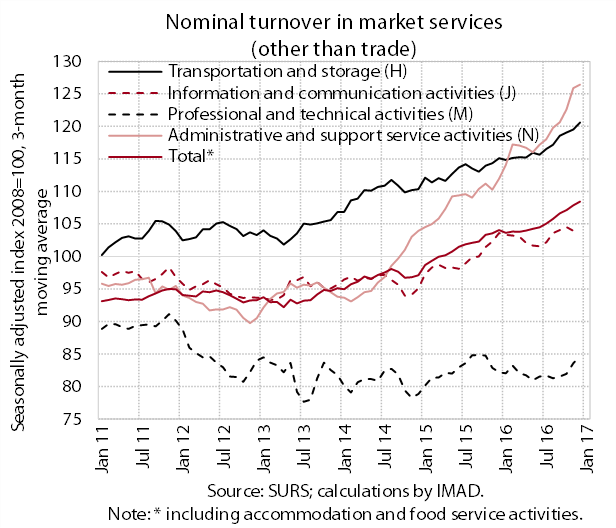

At the beginning of the year, nominal turnover in market services continued to grow. The growth in turnover in employment services (part of N activities) remained high, but owing to the improvement in labour market conditions, enterprises were also more frequently hiring workers directly rather than through agencies. Under the impact of higher exports of road transport services, positive trends also continued in transportation. Turnover growth in information and communication services slowed after a long period of growth that was boosted by computer services. In professional and technical activities, turnover in architectural and engineering services has ceased to decline, but activity remains low.

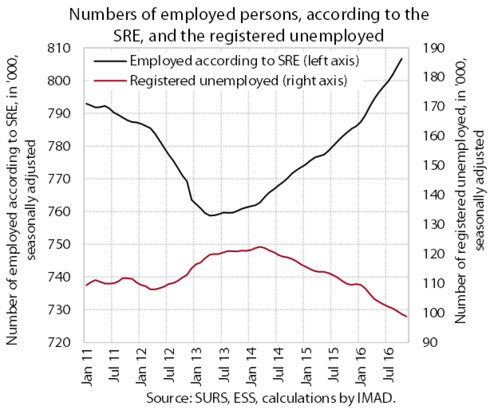

Following last year's growth, the strongest since the beginning of the crisis, the number of employed persons increased further in January. Higher year-on-year growth was recorded for most private sector activities. Short-term expectations of enterprises about future employment remain the strongest since the onset of the crisis. Owing to the relaxation of hiring restrictions in 2016, the growth of employment in public service activities was up year on year in the health sector, public administration and education (particularly at the primary level of education).

Following the significant fall in 2016, the number of registered unemployed continued to decline in the first quarter of this year. The decline continues to be mainly due to the outflow into employment, similar to that in the same period of 2016. Meanwhile, the overall inflow was smaller, primarily reflecting the lower inflow of those who became unemployed because of the termination of their fixed-term contracts. There were also fewer first-time jobseekers, which, in our view, was partly due to the smaller generations of young people finishing school and partly to the better economic conditions. At the end of March, 95,189 persons were registered as unemployed (13.6% fewer than in March 2016), which is close to the level recorded in the years of stable economic conditions before the crisis.

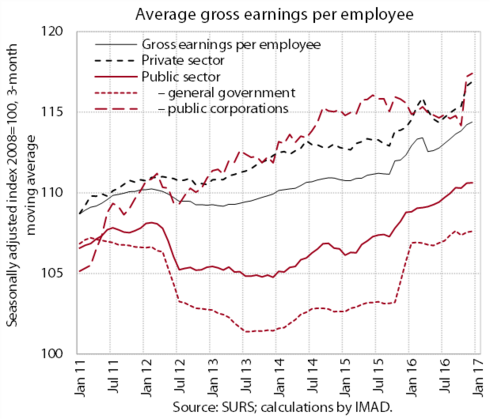

Average gross earnings per employee continue to increase at a modest rate. After recording strong growth at the end of 2016, which was underpinned by extraordinary year-end payments, earnings in the private sector and public corporations dropped in January, as expected. Earnings in the general government remained at the high level achieved at the end of year as a result of public servants’ promotions.

Consumer price growth has strengthened in the first part of this year. Year-on-year growth in energy prices continues to reflect higher prices of commodities while the rising overall inflation is also attributable to the relatively poor harvest in Spain and the resulting higher import prices of (unprocessed) food. Inflation in the euro area as a whole has increased for similar reasons. In Slovenia, stronger growth is also recorded in prices of services. With rising private consumption, the prices of leisure-related services in particular are rising, while the prices of telecommunication and public utility services are also higher. Durable goods prices have remained lower year on year, while the prices of semi-durables are similar to those one year earlier.

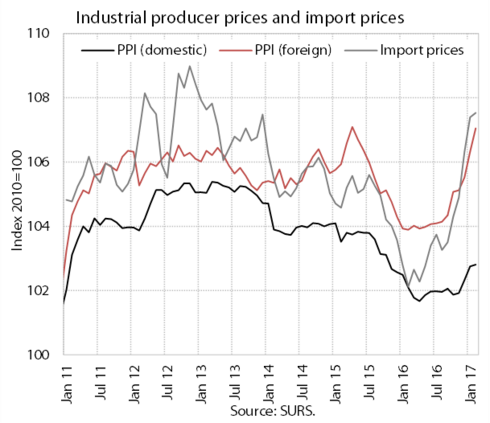

Industrial producer prices and import prices have been higher year on year since the end of last year. The main reason for this is further commodity price rises on world markets, which are, amid strengthening demand, gradually passed on to import prices and the prices of industrial products by domestic producers.

As a result of the weak euro and declining relative prices, the price competitiveness of exports improved at the beginning of the year. In the first two months of 2017, the euro lost value in nominal terms, particularly against major currencies outside the EU. Consumer price growth picked up year on year in this period, but less so than in Slovenia’s main trading partners. Price competitiveness improved in most euro area countries, Slovenia being among those with relatively more favourable price competitiveness movements.

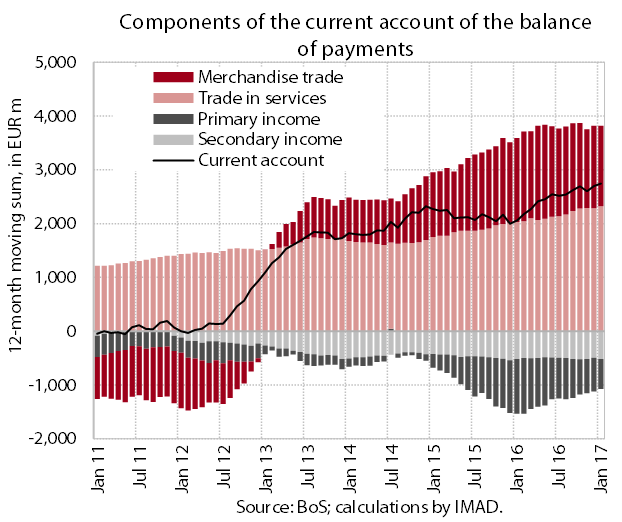

The surplus of the current account of the balance of payments rose further, totalling EUR 2.7 billion in the 12-month period as a whole (6.6% of estimated GDP). In comparison with the previous 12-month period, the larger surplus in current transactions was mainly due to the smaller deficit in primary income. The surplus in trade in services was also larger, primarily owing to higher revenue from construction works abroad and a larger surplus in trade in transport services. Imports of goods are also rising amid further growth in goods exports and domestic spending, which is reducing the trade surplus in goods.

The net financing of the rest of the world continues. Financial transactions with the rest of the world recorded a net outflow of EUR 1.3 billion, which was mainly underpinned by financial investment of the private sector and the Bank of Slovenia in foreign securities. Owing to the lower interest rates, the government was withdrawing deposits from accounts abroad and repaying foreign liabilities.

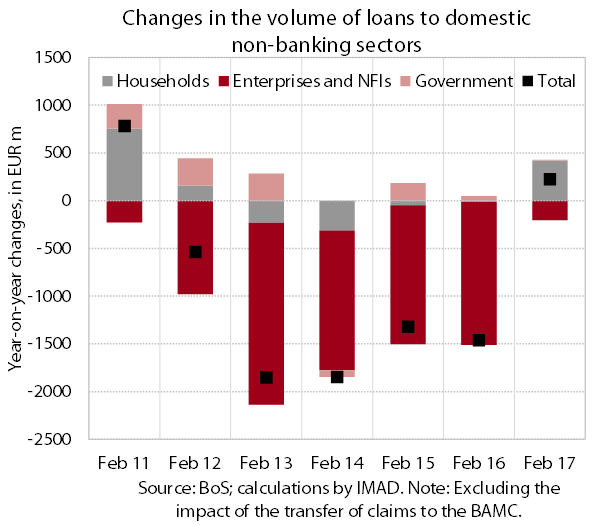

In February, the volume of loans to domestic non-banking sectors rose year on year for the first time since August 2011. In addition to the stronger growth in household loans, a significant factor in this increase was a slower decline in corporate loans. With new bank lending more or less unchanged, this decline is estimated to be largely due to lower corporate and NFI deleveraging. The borrowing terms are still unfavourable in Slovenia compared with the euro area average, which is also reflected in the outflow of the best clients from the Slovenian banking system to banks abroad. Enterprises thus borrowed around EUR 150 million net abroad in the last 12 months, this solely in the form of long-term loans. The quality of banks’ assets continues to improve. In the last few years the improvement has mainly been due to a reduction in the volume of the non-performing loans (NPLs) of large enterprises. In the future, the decline in NPLs could to a greater extent than thus far also be due to more effective management of non-performing loans in the micro, small and medium-sized enterprise (MSME) sector.

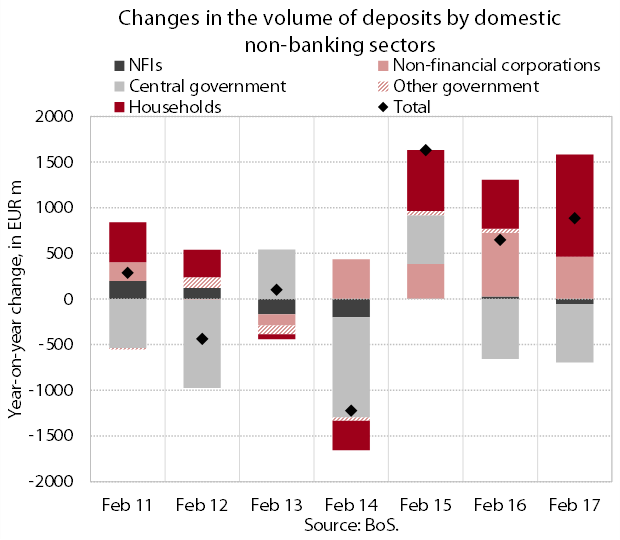

The structure of bank liabilities continues to change in favour of non-banking sector deposits. At the end of February, these accounted for more than two-thirds of the banking system's total assets, which is around 50% more than before the financial crisis. However, their maturity structure is fairly unfavourable (around 60% of all non-banking sector deposits being overnight deposits), which increases liquidity risk and hinders lending. The volume of liabilities to foreign banks, standing at EUR 2.7 billion at the end of February, continues to decline.

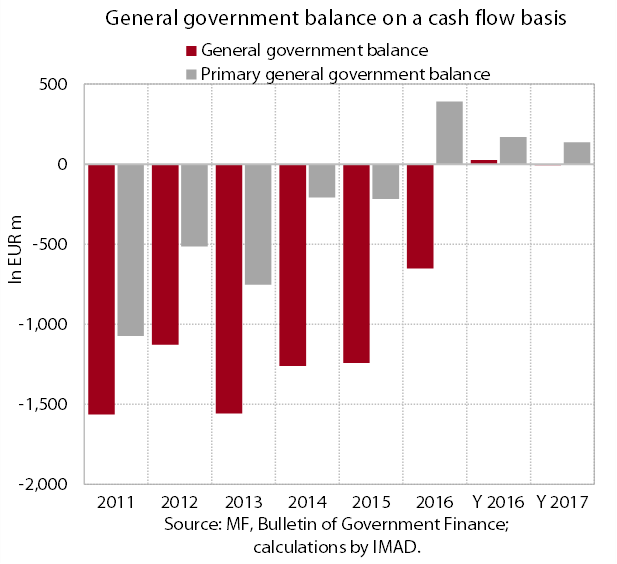

In January 2017 the general government position on a cash basis was almost balanced. Amid the strengthening of economic activity, tax revenues and revenues from social contributions continued to rise, while receipts from the EU budget remained low. Non-tax revenue growth was under the impact of one-off factors. Expenditure growth arose from most categories, the main factors being the payments of subsidies in agriculture (the dynamics of which may differ from year to year) and an increase in compensation of employees owing to the growth of employment and earnings in the public sector.

The general government deficit has been declining in the last few years; in 2016 it amounted to 1.5% of GDP. This decline has been taking place under the impact of the improvement in macroeconomic conditions, which since 2014 has been reflected in the strengthening of tax revenues and revenues from social contributions; the growth of these revenues is also influenced by the adopted permanent measures. In 2014 and 2015 fiscal consolidation on the expenditure side was strongly supported by temporary measures, which affected wage policy, employment of public servants, social benefits and transfers, but with the relaxation of these measures in 2016, the deficit decline was to a larger extent than in previous years achieved by reducing flexible categories of expenditure. As a result of the lower receipts from EU funds, investment in particular, i.e. co-financing with EU funds, dropped upon the transition to the 2014–2020 financial perspective. The growth of intermediate consumption was also slower, stemming mainly from higher expenditure in public institutes in the health sector. Capital transfers related to the BAMC were also significantly lower in 2016. A comparison of expenditure levels in 2016 against 2008 shows the largest increases for expenditure on social benefits (pensions), interest payments and compensation of employees and the largest declines for investment and general government subsidies. The impact of one-off factors, similarly to 2015, was negligible in 2016.

The general government debt declined in 2016 and its maturity continues to be extended owing to active debt-management policy. The decline interrupted the upward trend seen since mid-2008. The debt-to-GDP ratio decreased by 3.5 percentage points in 2016 (to 79.7% of GDP at the end of 2016), which ranks Slovenia in the middle of EU Member States. On the other hand, Slovenia is still among the Member States whose debt has increased the most relative to pre-crisis levels. In 2016 the Government increased the existing issues of long-term bonds and issued new ones in a total value of around EUR 4.8 billion. The bulk of newly issued debt in 2016 was used to repay principals due (around EUR 3.6 billion) and, owing to favourable borrowing conditions on international financial markets, to swap bonds issued in 2012–2014 with the required yield of over 5% for long-term bonds with more favourable financing terms. The implicit interest rate on the total debt declined to 3.7% in 2016, which is the lowest figure ever.