Slovenian Economic Mirror

Slovenian Economic Mirror 1/2018

In Slovenia economic activity increased further towards the end of the year in most sectors; the rising value of the composite economic sentiment indicator is already close to its pre-crisis peak. The increase in employment and the decline in unemployment continued; wage growth was also higher in the recent period, following several years of only modest improvement.

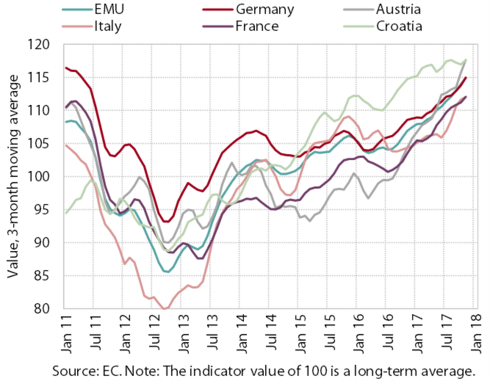

The euro area saw a continuation of relatively strong economic growth in the last quarter of 2017; short-term growth prospects are improving further. Activity rose in all sectors, the most in manufacturing. Confidence indicators (ESI and PMI) also improved, having already exceeded their highest pre-crisis values. According to the preliminary estimates of the German statistics office, the economy in Germany, Slovenia’s largest trading partner, grew by 2.2% in 2017, which is the most since 2011. Its growth was driven primarily by increased domestic demand, particularly private consumption and investments, with exports also higher than in the previous year. Favourable conditions are also reflected on the labour market, with the unemployment rate at a mere 3.6%. Strong economic growth also continues in Slovenia’s other main trading partners in the euro area.

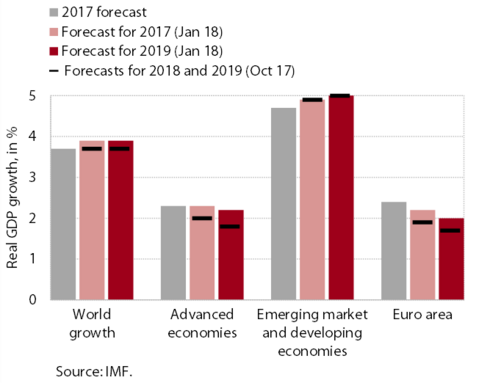

International institutions, most recently the IMF, have again revised upwards their economic forecasts in the last few months. According to the most recent IMF forecast, global economic growth will rise further to 3.9% this year (0.2 pps more than projected in October 2017) and continue at the same pace next year. Further growth will be recorded for Slovenia’s main trading partners (both inside and outside the euro area), which should have a favourable impact on the export expectations of Slovenian enterprises. The IMF estimates risks to the growth forecasts for this year and next as balanced, with a possibility of a further pickup in economic sentiment on the upside and of a financial market correction on the downside. Over the medium term, negative risks will predominate, notably the threat of accumulation of financial risks, protectionist policies, and geopolitical tensions. In this context, the IMF emphasises the urgency of implementing reforms to improve potential growth and ensure fiscal stability over the longer term.

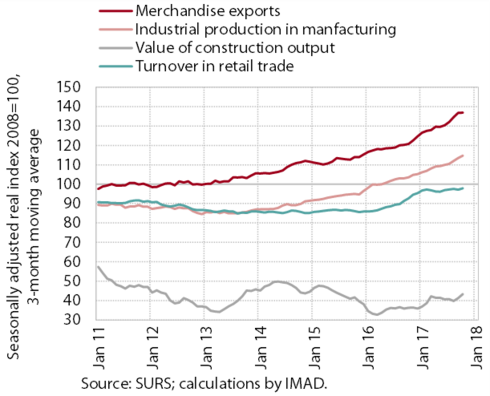

Towards the end of the year, economic activity increased further in most sectors, and the value of the composite economic sentiment indicator reached its ten-year high. The strong year-on-year growth of real exports continued, boosted by stronger foreign demand, and the growth of manufacturing output intensified. Moreover, the general improvement in domestic economic conditions, alongside favourable market developments, contributed to a further recovery of the residential property market. All of this, together with increased government investment, was reflected in a strengthening of construction activity. Growth in domestic and foreign demand, coupled with high consumer confidence, led to further turnover growth in market services. Business sentiment keeps improving and is now reaching ten-year highs.

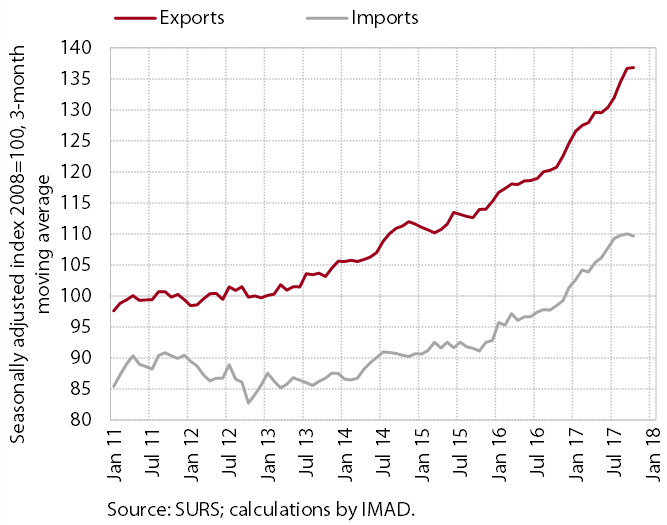

The strong year-on-year growth of merchandise exports and imports continued at the end of the year. In the first 11 months of 2017, exports were up 10.2% year on year. Their growth was driven primarily by exports of motor vehicles and machinery, but higher exports were also recorded for all other product groups. Germany, Italy and Austria remain Slovenia’s main trading partners; in terms of the share in total exports, exports to France increased the most in 2017 owing to higher exports of motor vehicles. The share of exports to Croatia and other countries from the former Yugoslavia dropped slightly, despite a nominal increase. Imports were up 10.6% year on year in the first 11 months of 2017 as a result of strengthening domestic demand and intense export activity.

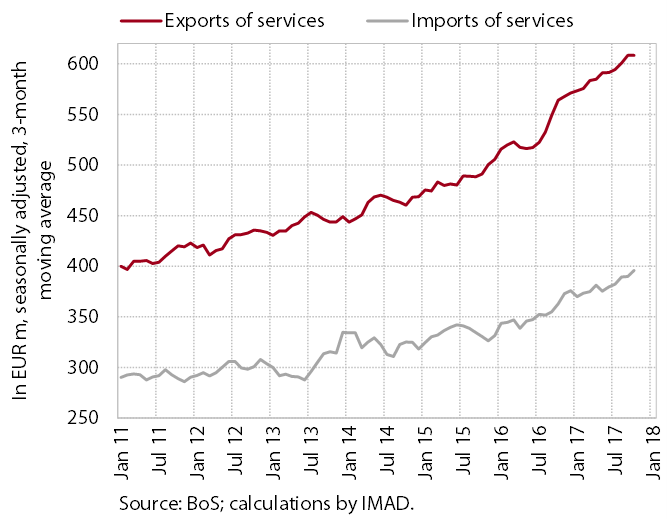

The strong year-on-year growth of exports of services continued, while the growth of imports of services strengthened further. The year-on-year export growth in the first 11 months of 2017 (11.2%) was largely underpinned by higher exports of transport services (road transport in particular), foreign tourist spending and exports of technical, trade-related business services. The growth of imports (9.0%) was also based mainly on imports of technical, trade-related business services and to a somewhat lesser extent on imports of transport services.

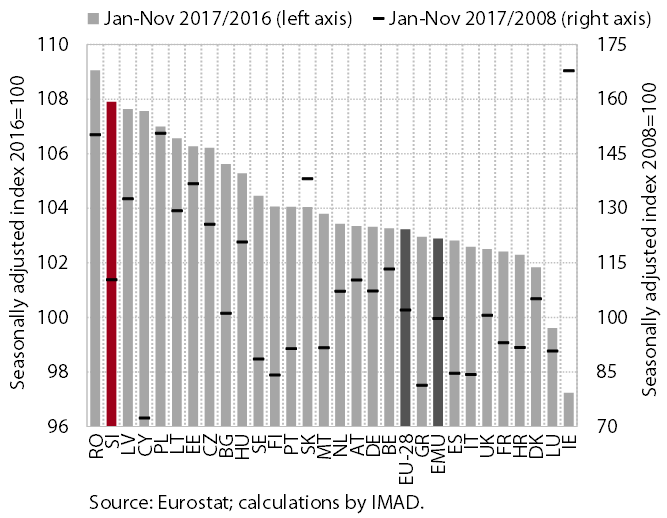

Production growth in manufacturing, which strengthened further in the second half of the year, was the second highest in the EU in 2017. The stronger growth was mainly due to higher growth in more technology-intensive industries, particularly the strengthening in the manufacture of motor vehicles (since the end of 2016) and ICT equipment (since mid-2017). The growth in medium-low-technology and the modest growth in low-technology industries also continued. In the first 11 months of 2017, production in all groups of industries according to technological intensity increased more year on year than in the EU as a whole.

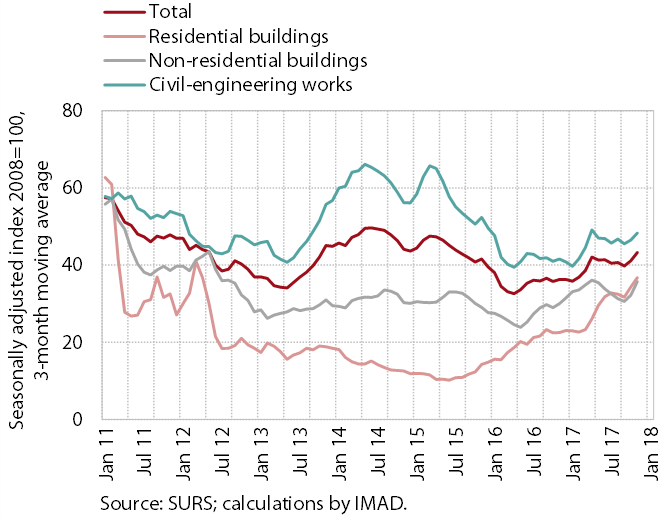

Activity in construction increased towards the end of last year, but remained low. It grew in all three construction segments. Its strengthening in the construction of residential buildings is related to the favourable labour market situation, reduced uncertainty, low interest rates and a considerable decline in the construction of flats in preceding years. The higher activity in the construction of non-residential buildings mainly reflects greater optimism in the private sector, while the higher value in civil-engineering works arises primarily from increased investment expenditure by the government.

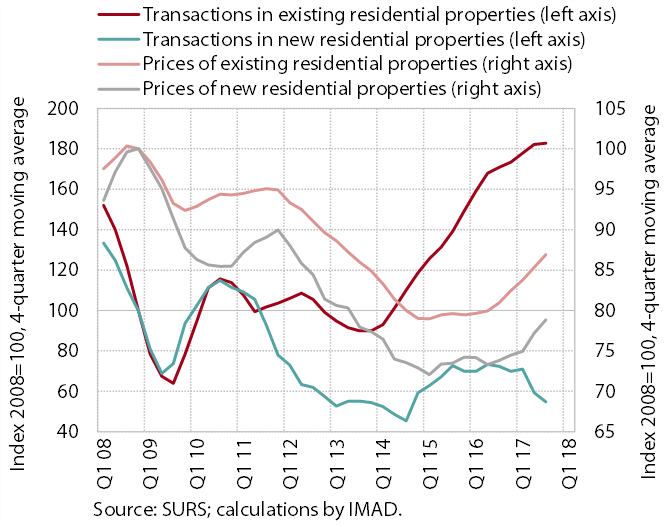

With a high number of transactions, average residential property prices rose further in the third quarter of 2017. The continuation of property market growth was, in our estimation, mainly due to the relatively favourable borrowing conditions and the improvement in the economic situation and consequent recovery of the labour market and high consumer confidence. With a high number of flats sold, the prices of existing flats – which account for around two thirds of all sales – were almost one tenth higher than in the same period of 2016. The highest price growth was again recorded in Ljubljana. The prices of new flats were also higher year on year, despite quarterly fluctuations; owing to the limited supply, however, the number of new flats sold remained low.

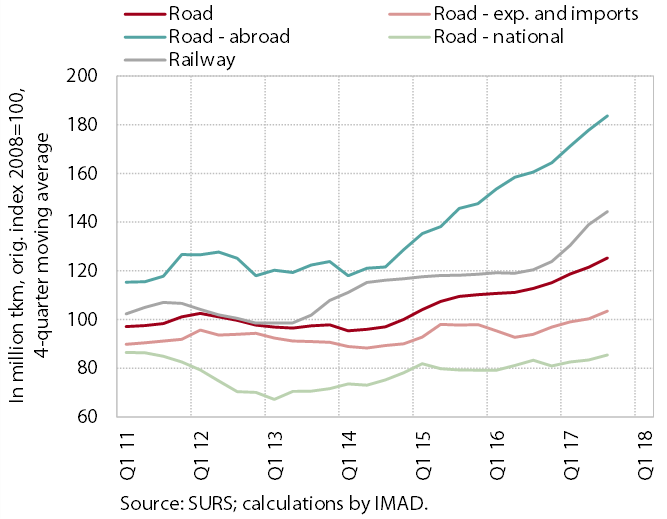

In the first three quarters of last year, land freight transport continued to strengthen in all transport categories. The rising foreign demand was reflected in a continuation of strong growth in transport services performed by domestic road hauliers abroad. Moreover, the more favourable domestic trends also contributed to stronger demand for their services in Slovenia. At the same time, there is an increase in foreign hauliers on Slovenian roads. Rail freight transport, meanwhile, grew particularly strongly in the first three quarters of 2017, mainly as a result of higher exports of these services.

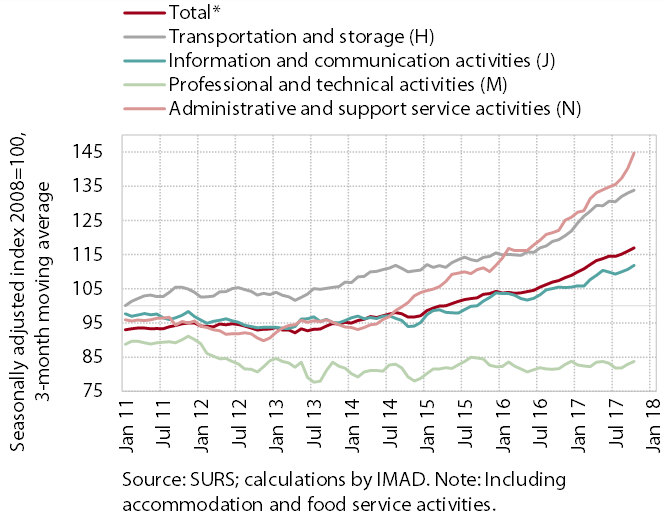

Nominal turnover in market services continued to increase at the end of 2017. Turnover growth in employment services, which is related to the rising demand for labour in more favourable economic conditions, strengthened further and was the greatest contributor to the strong turnover growth in administrative and support service activities. With rising foreign demand, turnover also increased further in more export-oriented services such as transport (road transport in particular) and computer services. The very low turnover in architectural and engineering services is mainly attributable to the prolonged stagnation of turnover in professional and technical services.

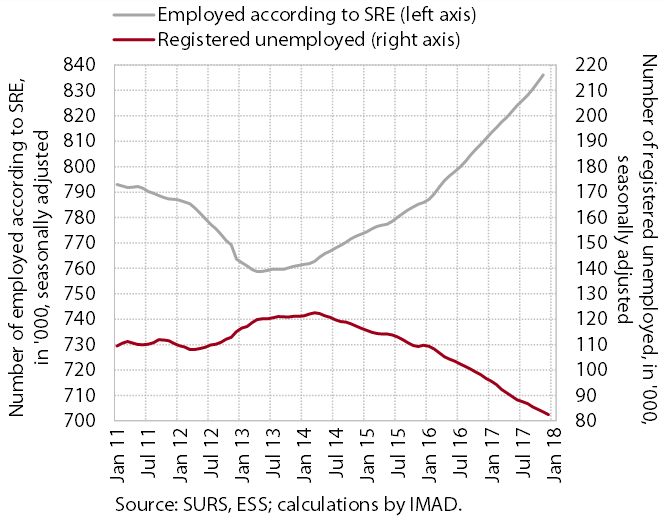

The number of employed persons is increasing and approaching a level last seen in 2007. Towards the end of last year, the number of persons employed rose further in most private sector activities, particularly manufacturing, trade and transportation. Especially in manufacturing, enterprises are increasingly facing a shortage of workers with the appropriate skills, which is reflected in a further increase in the employment of foreign workers in some sectors. The short-term expectations of enterprises about future employment remain high. In public service activities, the year-on-year growth in the number of persons employed is mainly a result of higher employment in the sectors of education (particularly primary education) and health.

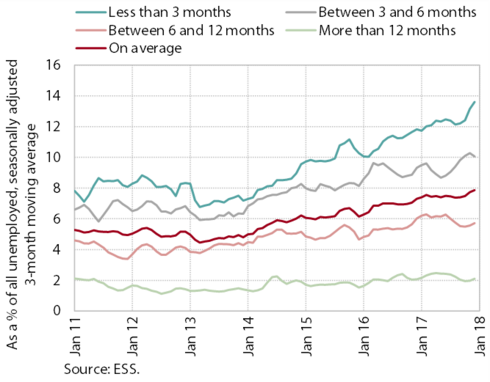

The number of registered unemployed persons declined in 2017 for the third consecutive year and even more markedly than before. The inflow into unemployment dropped again, largely because of a lower number of people who registered as unemployed due to the expiration of their temporary employment contracts. There were also fewer first-time jobseekers, which is related to the improvement in economic conditions and smaller generations of young people finishing school. As a result of the lower number of unemployed, the outflow into employment was also somewhat more modest than in the same period of 2016. The probability of transition from unemployment to employment remains relatively high. At the end of the year, 85,060 persons were registered as unemployed, 14.6% fewer than in December 2016.

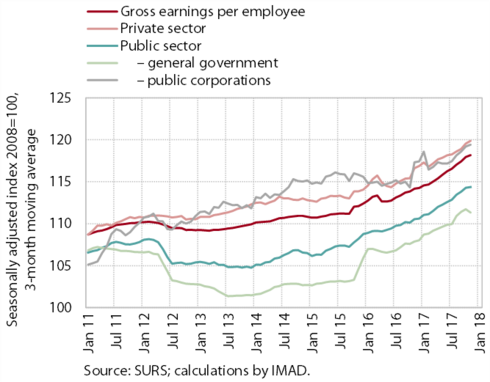

After several years of only modest improvement, private and public sector wages saw higher growth in the recent period. In the first 11 months of 2017, average gross earnings were up 2.7% year on year in both sectors. Wage growth remains lower than in the pre-crisis period, however, and does not exceed productivity growth. It is thus not causing any visible imbalances as yet. In the private sector, wage growth, in an environment of high activity, was strongest in manufacturing and certain market services, similar to the previous year. Wage growth in the public sector, on the other hand, stems from the elimination of certain wage anomalies and the regular promotions of the employed.

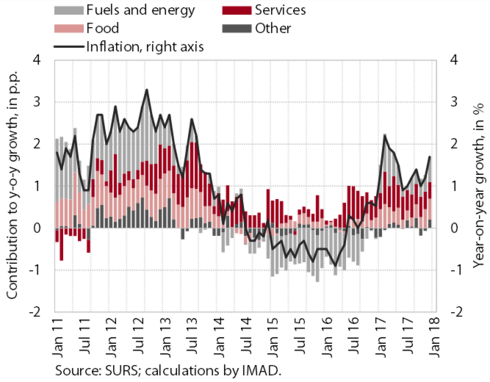

Year-on-year growth in consumer prices increased somewhat in December, to 1.7%. Inflation was mainly pushed up by higher prices of commodities, particularly energy and food (especially unprocessed food). Their contribution to headline inflation was 1.1 pps (two thirds). The contribution of prices of semi-durable goods (particularly clothing and footwear) rose further at the end of the year, while prices of durable goods were down year on year. The growth of prices of services, which was lower than on average in other months of 2017, contributed 0.4 pps. The absence of inflationary pressures is also reflected in core inflation, which remains low.

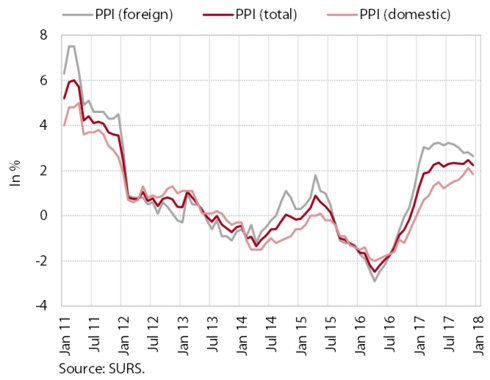

The year-on-year growth of industrial producer prices (2.2%) strengthened last year. With higher prices of commodities and favourable economic conditions, prices were up on both the domestic and foreign markets. They increased the most (by almost one tenth) in the manufacture of metal products, while in the majority of other sectors their growth was considerably lower.

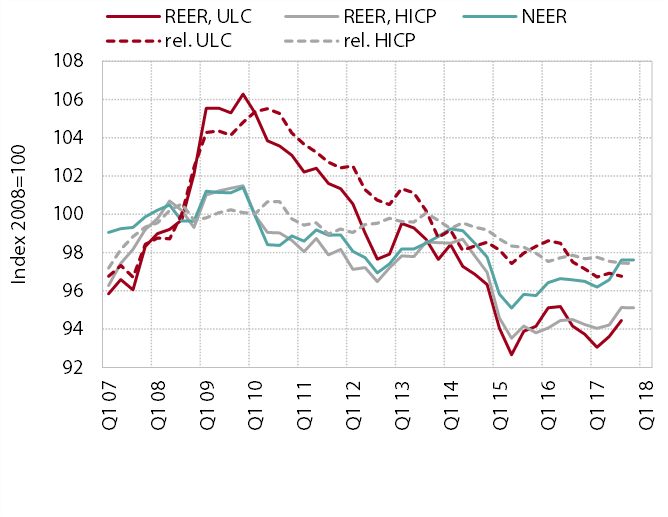

Price and cost competitiveness indicators deteriorated somewhat in the second half of the year but remain relatively favourable. The impact of the appreciation of the euro was relatively smaller than in most other Member States owing to the geographic structure of Slovenia’s trade. Exchange rate movements towards a deterioration in price and cost competitiveness were mitigated by a decline in relative prices compared to trading partners (lower inflation and a larger reduction in unit labour costs).

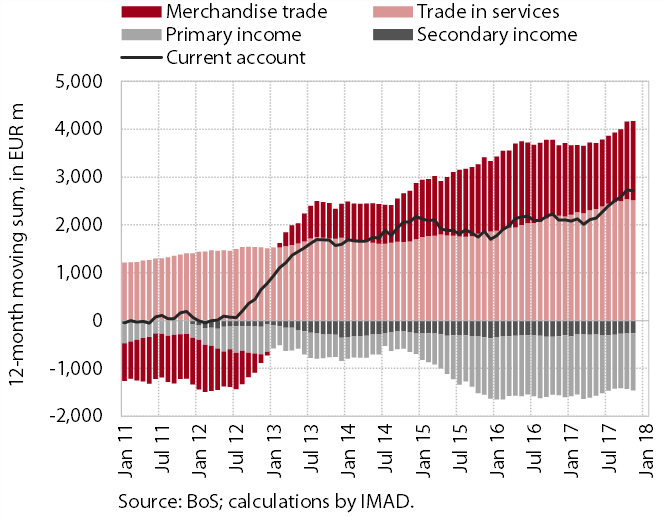

In the last few months the surplus of the current account of the balance of payments has been the highest thus far. The 12-month cumulative surplus for the period ending November 2017 amounted to EUR 2.7 billion or 6.3% of GDP. Its year-on-year widening was mainly due to the higher surpluses in trade in goods and services, reflecting both rising foreign demand and a favourable competitive position of Slovenian exporters. Imports are also picking up amid moderate growth in domestic consumption. The deficit in primary income was down year on year, for the most part because of lower net payments of interest on external debt, which is mainly related to lower yields on government bonds. The deficit in secondary income was also lower year on year, this owing to the net received transfers of the private sector (taxes, rewards, etc.).

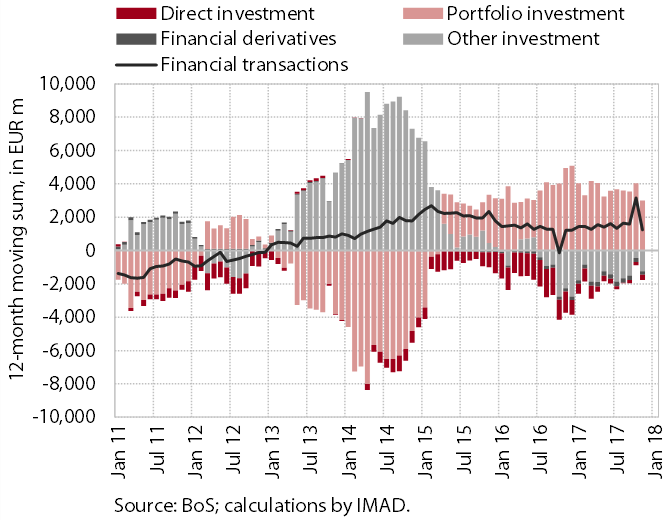

Net lending to the rest of the world continued. External financial transactions recorded a net outflow of EUR 1.2 billion in the 12 months to the end of November 2017. It was mainly underpinned by financial investments by the private sector and the BoS in foreign debt securities. These include both securities purchased on the basis of investment decisions of commercial banks and the BoS and those purchased under the asset purchase programme (APP) coordinated at the level of the Eurosystem. The net inflow in other investment is a consequence of government and BoS withdrawals of deposits from accounts abroad. The otherwise modest direct investment flows were mainly marked by inflows of equity capital from foreign investors.

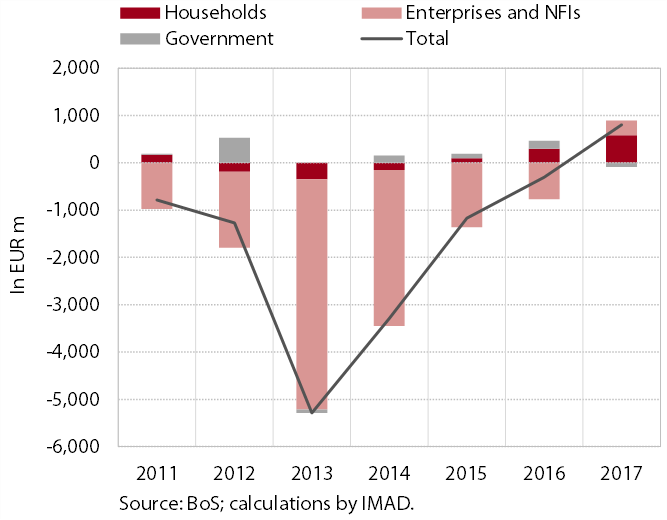

The volume of loans to domestic non-banking sectors rose last year for the first time since 2010. Favourable economic conditions contributed not only to growth in household loans (seen already since 2015), but also – after seven years of deleveraging – growth in corporate and NFI loans, though these slowed somewhat at the end of the year. In the last few years, enterprises have increased the demand for investment loans and working capital loans, while the demand for loans for refinancing has eased. Deposits of domestic non-banking sectors (particularly households and non-financial corporations) remain an increasingly important source of funding for the banking system and already account for almost 70% of the banking system’s total assets (compared with 42.2% at the end of 2008). Owing to low interest rates, particularly overnight deposits are on the rise, making up almost 65% of all non-banking deposits (33% at the end of 2008).

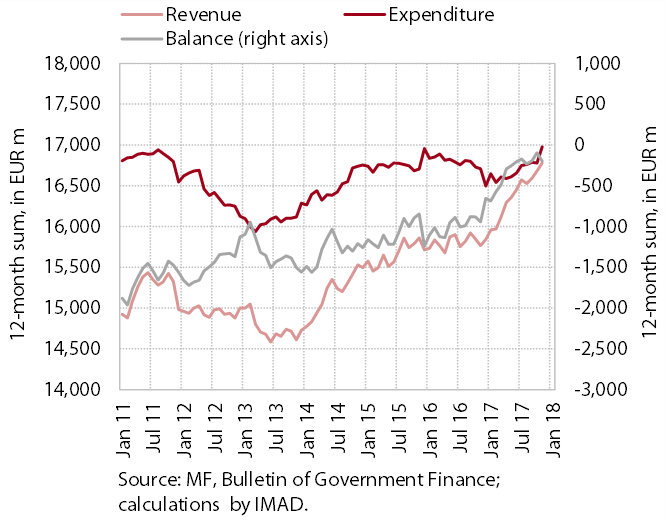

With the continuation of strong revenue growth, the general government deficit was significantly lower year on year in the first 11 months of 2017. It widened slightly towards the end of the year, however, owing to the payment in November of matured financial liabilities of hospitals. This boosted growth in expenditure on goods and services, while growth in other expenditures remained moderate (the highest growth rates being recorded for investment expenditure, compensation of employees, pensions and sickness benefits). Amid favourable economic trends, the strong growth of tax revenues and revenues from social contributions continued, maintaining a relatively low general government deficit on a cash basis. According to the preliminary release of data, the state budget recorded a deficit of 0.8% of GDP (EUR 332.4 million) last year, almost half less than planned at the adoption of the budget.

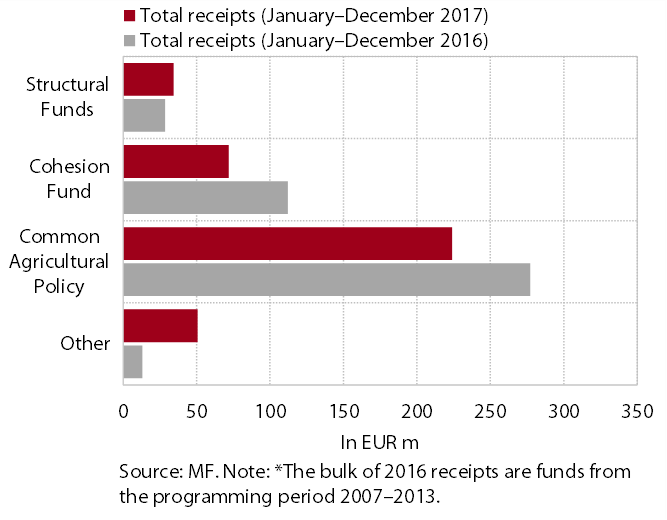

The net position of the state budget against the EU budget was positive in 2017 (at EUR 8.8 million); the absorption of funds under the new financial perspective has not yet fully started. Last year, Slovenia received EUR 387.3 million from the EU budget (41.9% of revenue envisaged for 2017) and paid EUR 378.5 million into it (90.1% of the amount planned). Revenue from the cohesion fund and structural funds deviated the most from the realisation planned. The slow absorption of funds under the new financial perspective is related primarily to the interdisciplinary nature of calls for proposals and projects linked to the implementation of the Smart Specialisation Strategy, but also to the change in market conditions, as a result of which some projects were abandoned and additional appropriations approved for other projects with lower implementation risk. The majority of funds obtained by the end of 2017 were allocated from the European Social Fund in support of the objectives of promoting employment, social inclusion and knowledge and enhancing institutional capacity and the rule of law.