Competitiveness

Slovenian Economic Mirror 1/2017

The relatively favourable developments in the euro area have continued. In Slovenia, favourable trends in economic activity also continued; the labour market situation improved further. Despite the economic growth achieved, bank loan financing has remained modest; the maturity structure of the banks’ liabilities has deteriorated further.

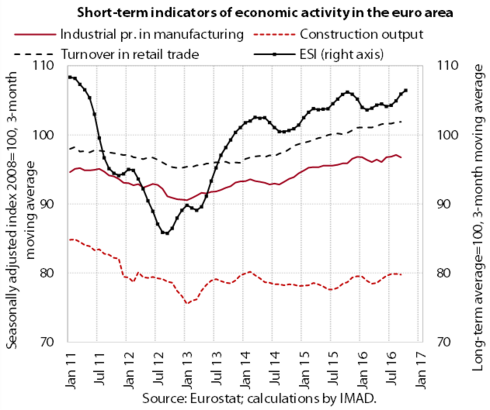

The relatively favourable economic developments in the euro area continued at the beginning of the last quarter of 2016. With the strengthening of private consumption, which had been the main driver of economic growth in the euro area in the first three quarters of 2016, turnover increased the most in retail trade. With the indicators of confidence in the economy and among consumers improving further, prospects also remained favourable for the beginning of 2017.

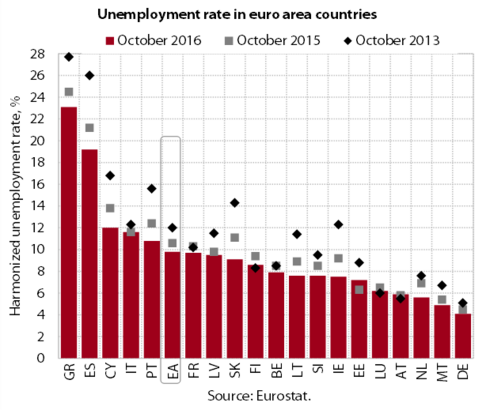

The strengthening of private consumption was attributable to the improvement in labour market conditions in the euro area. In October 2016 the unemployment rate, which has declined since 2013, was at its lowest point since 2009. In the third quarter, employment increased further and was at its highest level since 2008.

Most sectors have recorded further activity growth in the last few months. With higher foreign demand and favourable export competitiveness, the growth of exports and manufacturing production has continued to strengthen year on year. Further growth in private consumption contributed to the stronger turnover growth in the distributive trades witnessed in the last few months; this was particularly the case not only in the segments of durable and semi-durable goods, but also in leisure-related services, which is partly attributable to the high number of foreign tourist arrivals. Construction activity remained modest, mainly owing to lower government investment.

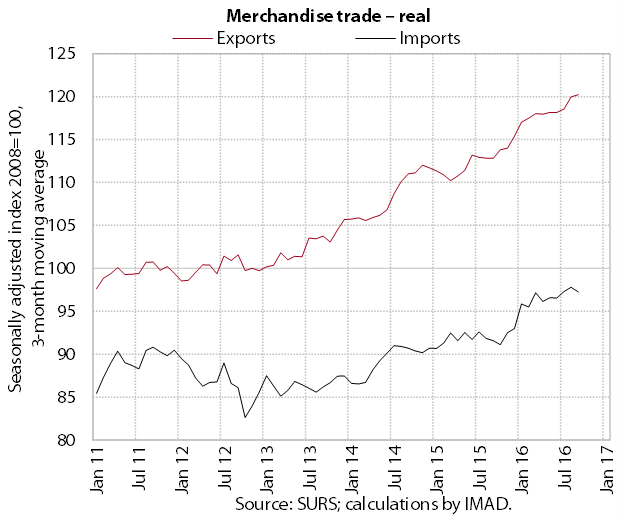

Real merchandise exports and imports maintained their high levels at the beginning of the last quarter of the year. In the first 10 months of 2016 exports were 5.4% higher year on year. Exports increased in most sectors, with the main contribution to growth coming from motor vehicles. Real imports were up 4.3% year on year in the first 10 months of 2016, boosted by rising household consumption, private corporate investment and manufacturing production.

Exports of services increased further; imports remained similar to the third quarter. The year-on-year export growth in the first 10 months of 2016 (7.6%) was largely attributable to stronger exports of transport services, higher revenues from construction works abroad and increased spending by foreign tourists. Import growth (3.7%) was based on imports of technical, trade-related business services, transport services and higher resident spending abroad.

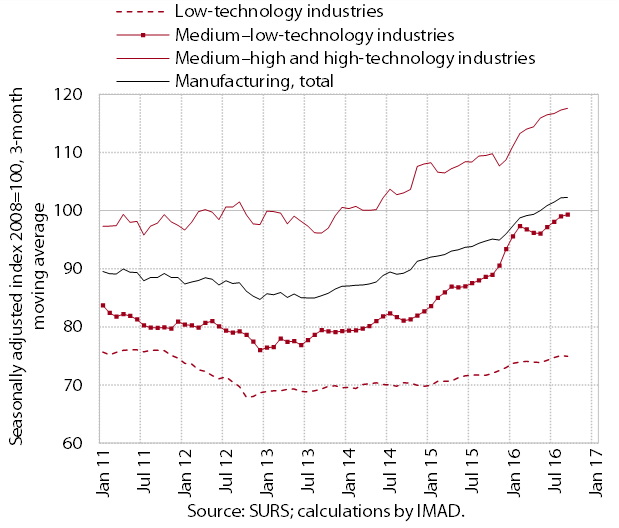

Production volume in manufacturing remained high at the beginning of the last quarter of 2016. In the first 10 months of the year production expanded in all industry groups in terms of technological intensity and was, on average, 7.6% higher than in the same period of 2015. The largest year-on-year increases were recorded for the medium-low-technology metal and rubber industries and the technologically more intensive manufacturing of ICT and electrical equipment, which recorded significantly higher sales, particularly on foreign markets. Production was also up year on year in most low-technology industries (notably the textile and furniture industries), where sales growth remained modest both domestically and abroad.

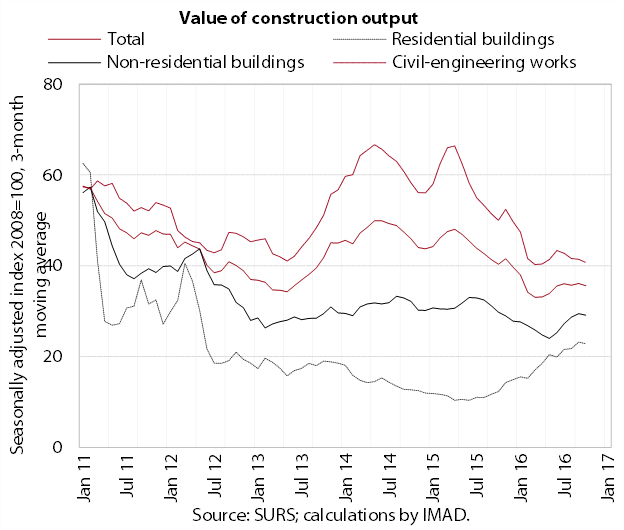

After increasing in the second quarter, the value of construction output remained more or less unchanged in the months that followed. Activity in the first 10 months of 2016 was much lower than one year before, which is mainly attributable to lower government investment. The general improvement in economic conditions and a gradual rebound on the real estate market have boosted not only the construction of flats, but also, in recent months, non-residential buildings.

With the continuation of relatively high sales, residential property prices increased further in the third quarter and were 5% higher year on year. The prices of existing flats, which account for around two-thirds of total sales, rose the most in Ljubljana. With a larger share of newly built flats sold in high-end residential buildings, the prices of new flats also increased year on year; however, the number of flat sales remained low. The prices of houses were also up year on year – existing houses in particular – the sales of which have been rising for the third consecutive year.

At the turn of the fourth quarter of 2016, nominal turnover continued to grow in most market services. In the 10 months of 2016, turnover growth in transportation and computer services mainly stemmed from foreign demand. In segments that are more dependent on domestic investment demand (especially architectural and technical services), turnover remained low. In the 10 months to October 2016, turnover was up year on year in most market services.

With labour market conditions improving further, consumer confidence continued to improve at the end of the year, which was reflected in the further growth in household consumption. Purchases of durable goods (passenger cars and home furnishings), which have been rebounding for quite some time, continued to grow, as did spending on semi-durable goods and services, which started to strengthen more notably in 2016. Among the latter, spending on leisure-related services at home and abroad rose the most notably.

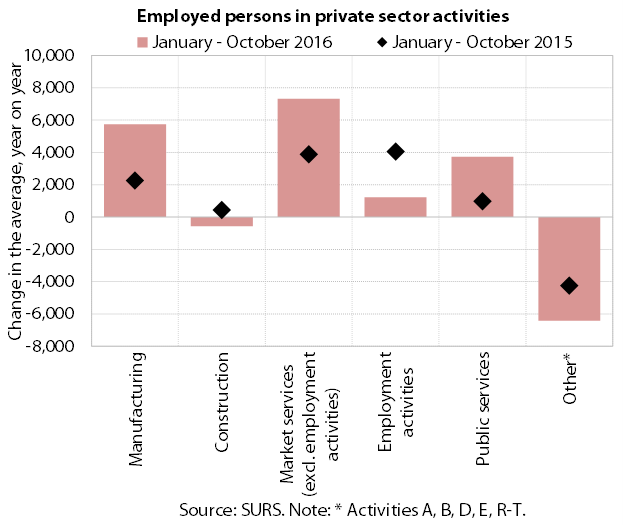

With GDP growth becoming broader-based, the number of employed persons increased more in the first 10 months of 2016 than in the same period of 2015. Employment growth was higher year on year in most private sector activities. In employment activities, the number of employed persons rose less than it had one year before, which indicates more frequent direct hiring by companies in other sectors. Companies’ expectations about future employment improved further and were at their highest level since the onset of the crisis at the end of the year. With the relaxation of hiring restrictions, employment growth in public service activities was up year on year in the health sector, public administration and primary education.

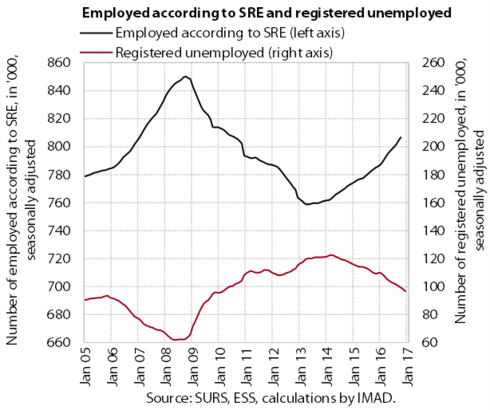

With increased hiring, registered unemployment declined further in 2016 (by 8.5%). The number of registered unemployed was close to the level seen during the years of stable economic growth. The outflow into employment was the largest since the beginning of the crisis. The inflow into unemployment declined further, particularly the inflow that was due to the termination of fixed-term employment contracts. There were also fewer first-time jobseekers, which in our view was also partly due to slightly fewer young people finishing school and the improved job prospects when leaving school to enter the labour market. At the end of 2016 a total of 99,615 persons were registered as unemployed, 11.9% fewer than at the end of 2015.

The growth of average gross earnings in the first 10 months of 2016 was the highest in five years, but still significantly weaker than before the crisis. In the private sector, growth is related to the strengthening of economic activity; in the public sector, this is mainly attributable to the promotions of public servants and the return of the pay scale. Earnings in public corporations remained close to the high levels seen in previous years.

Consumer prices were higher year on year at the end of 2016 (0.5%), largely as a result of increases in the prices of commodities and services. The fall in energy prices, the main reason for the price decline in 2015, began to decelerate in the second half of the year. At year end, energy prices were similar to those recorded one year earlier. Higher commodity prices contributed to rises in food prices (especially unprocessed food). Price growth in services strengthened and was broader-based, in contrast to previous years when it was mainly affected by one-off factors. With a further rebound in private consumption and more foreign tourist arrivals, higher prices were recorded, particularly for leisure-related services. The prices of durable and semi-durable goods remained down year on year.

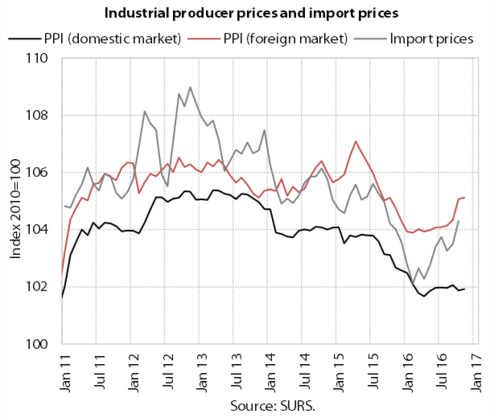

The year-on-year decline in industrial producer prices is slowing; in November the prices of imported goods were higher year on year. With rising demand, the higher commodity prices on global markets gradually pass through into import prices and domestic industrial producer prices. Domestic producer prices are hovering at roughly the same levels on the domestic market, whereas they have been rising since the middle of the year on markets abroad.

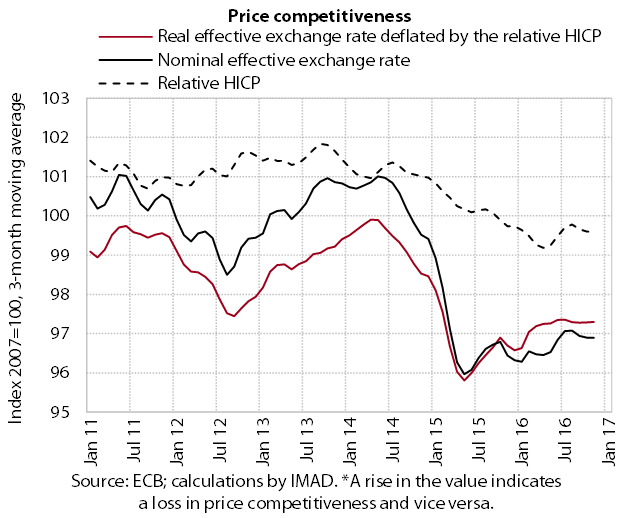

In 2016 the price competitiveness of Slovenia’s economy remained close to the favourable levels of the preceding year. The smaller year-on-year loss of competitiveness in the first eleven months of 2016 than for most other euro area countries was due to the appreciation of the euro, which had a relatively minor impact on Slovenia owing to the geographic structure of its trade. Moreover, the decline in relative consumer prices was still one of the largest in the euro area.

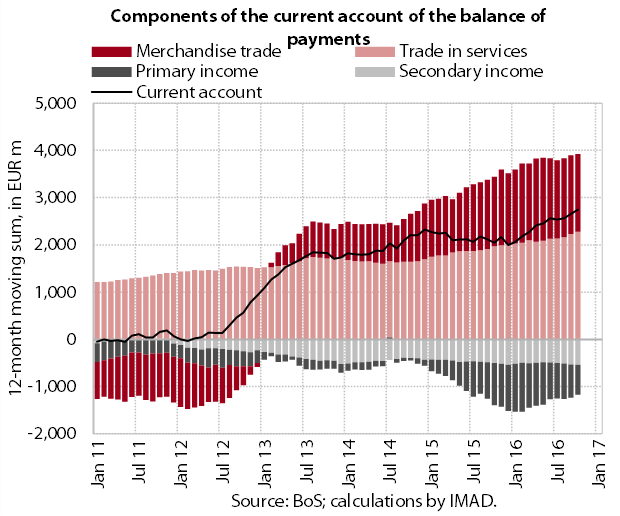

The current account surplus continues to widen. In the first ten months of 2016 it was up year on year, primarily owing to a larger surplus in merchandise and services trade, which reflects favourable export trends amid improving export competitiveness and a relatively slower rebound in domestic consumption. The deficit in primary income was smaller year on year, largely as a result of the lower estimates for the reinvested profits of foreign investors and lower interest payments on external debt. In the 12 months to October, the current account surplus totalled 6.9% of GDP.

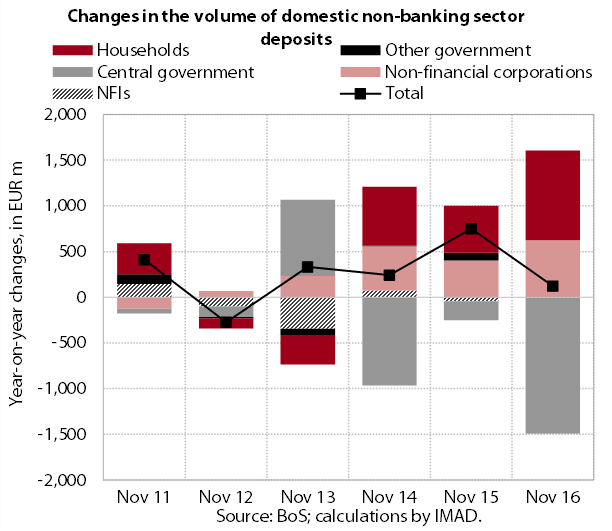

The structure of bank liabilities is changing in favour of non-banking sector deposits. With increases recorded mostly for overnight deposits (by enterprises and households), the maturity structure of bank liabilities is deteriorating. The banks continue to reduce their liabilities abroad (predominantly those to foreign banks), which account for only just above 10% of their total assets, compared to almost 40% before the crisis.

The year-on-year contraction in the volume of loans granted to domestic non-banking sectors continued to decelerate in November. With new bank lending more or less unchanged, this slowdown is estimated to be largely due to reduced corporate and NFI deleveraging. The banks’ lending conditions in Slovenia are still relatively less favourable than in the euro area as a whole, which is also reflected in enterprises seeking alternative sources of finance. Corporate borrowing abroad is increasing, mostly in the form of short-term loans. The year-on-year repayment of long-term loans eased notably owing to a large monthly inflow in October.

The structure of bank liabilities is changing in favour of non-banking sector deposits. These otherwise declined year on year in October, which is a consequence of the base effect and the outflows of government deposits and, to a lesser extent, NFI deposits, while household and corporate deposits continue to rise. It is mainly overnight deposits that are rising, which is deteriorating the maturity structure of sources of finance.

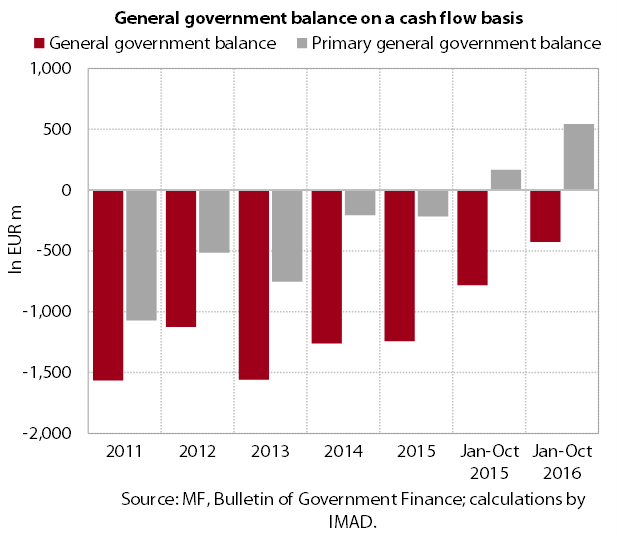

The general government deficit on a cash basis halved year on year in the first 10 months of 2016. This decline mainly reflects the improved economic conditions, the change in the flow of EU funds and the retention of some measures to contain expenditure. The surplus, excluding interest expenditure, tripled year on year.

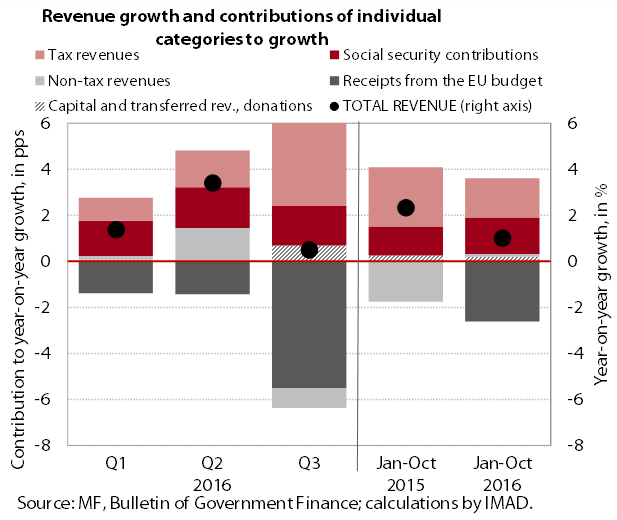

General government revenue rose year on year in the first 10 months. The fastest growth was recorded for revenues related to favourable labour market developments. Despite a more positive trend, the year-on-year growth of consumption-based revenues remains relatively low. This is related not only to the slow recovery in total nominal domestic spending, but also to transitional factors such as the effect of the change in the payment of VAT on imports.

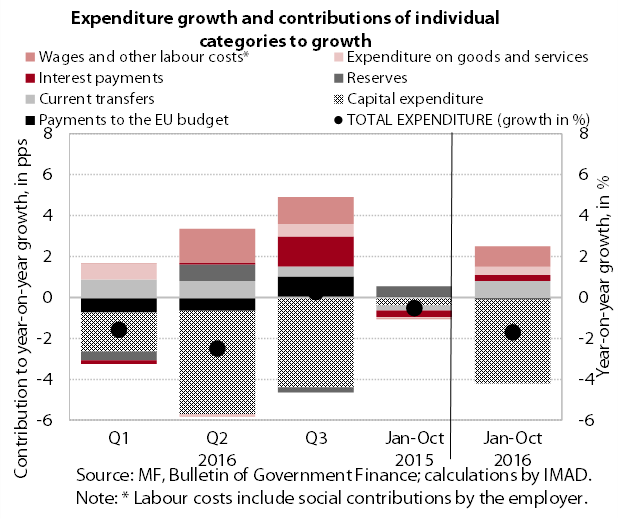

General government expenditure continues to decline year on year. The main reason for the decline is lower investment upon the transition to the implementation of the new EU financial perspective. The uninterrupted increase in the long-term trend growth rate in other expenditures witnessed since early 2016 continued at the beginning of the third quarter, primarily owing to expenditure related to the partial relaxation of austerity measures (the wage bill in the public sector, transfers to individuals and households) and expenditure on goods and services.

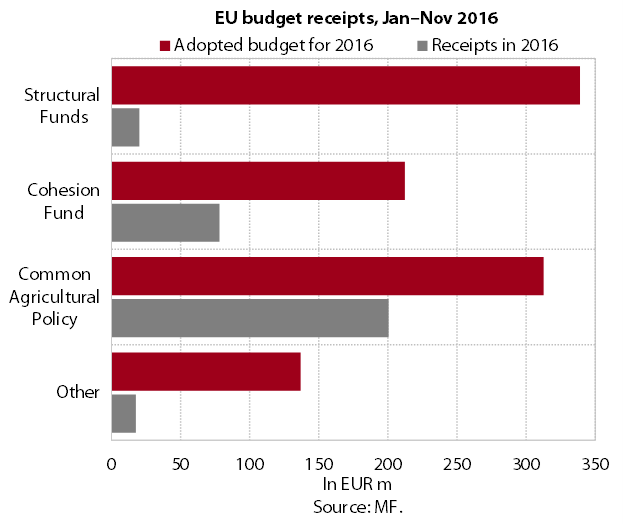

The net position of Slovenia’s state budget against the EU budget was negative in the first 11 months of 2016. During this period Slovenia’s EU budget receipts amounted to EUR 341.5 million, while its EU budget payments totalled EUR 33 million more. The bulk of the funds received were from the Common Agricultural and Fisheries Policy. The majority of the resources from the Cohesion Fund and Structural Funds were paid into the state budget in the first half of the year from the previous financial perspective. Under the new financial perspective, EUR 85 million had been disbursed from the state budget to beneficiaries by the end of November.