Slovenian Economic Mirror

Slovenian Economic Mirror 7/2024

In the third quarter, higher export activity played a key role in strengthening economic growth in Slovenia. Household spending continued to grow solidly, and government consumption maintained a high growth rate. In contrast, the decline in gross fixed capital formation deepened significantly, especially in construction. Year-on-year growth in the average gross wage remained relatively high in August. In the public sector, this was driven by an increase in the value of the pay scale grades following a partial wage adjustment for inflation in June, while in the private sector, persistent labour shortages continued to be a key driver of wage growth. The downward trend in the number of registered unemployed has stalled over the past two months, though their numbers remain lower than during the same period last year. Inflation continued to ease in October, with prices declining by 0.5% month-on-month while remaining unchanged year-on-year. The primary driver of the monthly decline this time was a new method of calculating network charges for electricity. This led to approximately a one-tenth month-on-month decrease in electricity prices, while year-on-year prices fell by over one-fifth.

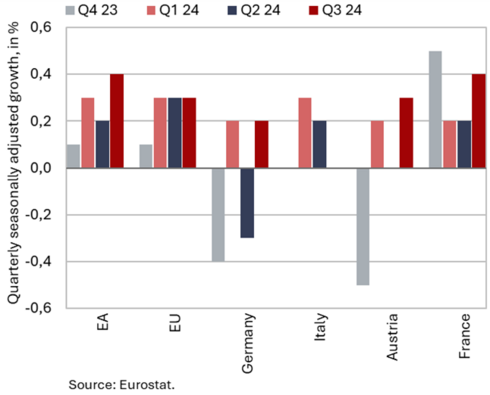

Quarterly GDP growth in Slovenia’s main trading partners, Q3 2024

In the third quarter, euro area GDP increased by 0.4% quarter-on-quarter and by 0.9% year-on-year. Among Slovenia’s main trading partners for which data is available, France recorded the strongest quarter-on-quarter GDP growth (0.4%; 1.3% year-on-year), driven significantly by consumption related to the Olympics. Austria’s GDP grew by 0.3% (-0.1% year-on-year) and Germany’s by 0.2% (-0.2% year-on-year), while Italy’s stagnated (+0.4% year-on-year). According to the survey indicators, economic activity stagnated quarter-on-quarter at the beginning of the fourth quarter. The Economic Sentiment Indicator (ESI) and composite economic confidence indicator (PMI) for the euro area were similar in October to the third quarter average. The PMI value stood at 50, indicating stagnating activity. The services PMI was above 50, reflecting continued growth, while the manufacturing PMI was below 50, pointing to further contraction amid a persistent decline in new orders. The euro area ESI was higher year-on-year in October, with significant improvements in sentiment among consumers and in services, while sentiment in industry deteriorated notably.

IMF GDP growth forecasts, October 2024

In October, the IMF left its forecast for global economic growth unchanged. The global economy has remained resilient this year (growth was forecast at 3.2%), though with large differences in activity growth between countries and sectors. Inflation has weakened and boosted growth in real household income and private consumption. Unemployment remained low in most countries, while international trade has started to recover. Next year, global GDP growth is expected to remain at the same level as this year, with low inflation and a less restrictive monetary policy. In 2025, growth is expected to weaken in the US (from 2.8% to 2.2%), amid a gradual tightening of fiscal policy and lower growth in private consumption, and to increase slightly in the euro area (from 0.8% to 1.2%), mainly thanks to strengthening of private consumption. Strong domestic demand in India and Indonesia and stimulus measures in China will support relatively strong growth in Asia. Heightened geopolitical tensions, especially the ongoing conflict in the Middle East, which could drive up oil prices if it escalates further, and the imposition of custom duties that could negatively impact international trade, remain significant risks.

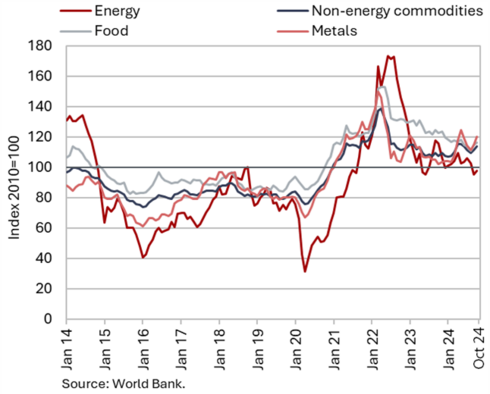

Commodity prices, October 2024

In October, prices of Brent crude oil and non-energy commodities rose slightly month-on-month on average. The average dollar price of Brent crude oil increased by 2.2% to USD 75.6 in October and the euro price by 4.1% to EUR 69.4. Year-on-year, the dollar price of Brent crude oil decreased by 16.5% and the euro price by 19.2%. The euro prices of natural gas on the European market (Dutch TTF) reached EUR 40.4 per MWh in October, up 12% from September (they were 14.1% lower year-on-year). According to the World Bank, the average dollar price of non-energy commodities continued to rise in October (by 2.1% compared to September).

Among the main commodity groups, the most significant price increases were observed in metals and minerals and fertilizers. Year-on-year, prices of non-energy commodities were 5.7% higher in October, with significant price hikes in beverages (up by 63%), especially of cocoa and coffee, and metals (up by 17.4%).

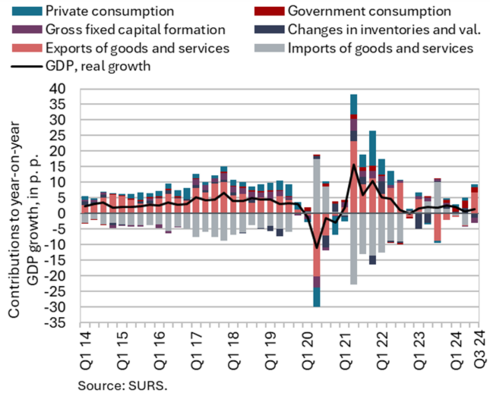

Gross domestic product, Q3 2024

In the third quarter of 2024, GDP rose by 0.3% quarter-on-quarter (seasonally adjusted) and by 1.4% year-on-year. Year-on-year growth has increased compared to the second quarter of this year, mainly due to higher export activity. After falling year-on-year in the first half of the year, exports of goods and services rose by 8.4% year-on-year, mainly due to the low base from last year and a higher number of working days in the third quarter of this year. Export growth was higher than import growth (6.5%), resulting in a positive contribution of the external trade balance to GDP growth (1.9 p.p.). The solid growth of household spending continued (1.9%) and growth of government consumption remained high (9.1%). In contrast, the decline in gross fixed capital formation deepened dramatically (-8.2%).

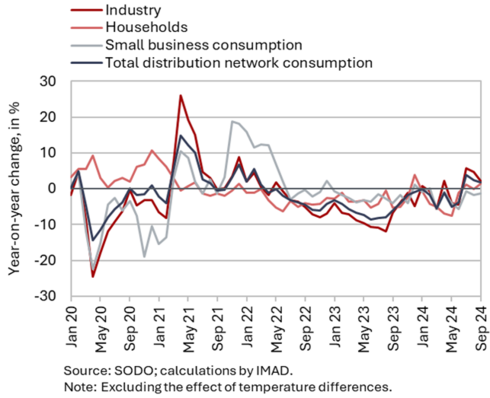

Electricity consumption by consumption group, September 2024

In September, electricity consumption in the distribution network was higher year-on-year. With the same number of working days, industrial consumption in September was 2.3% higher year-on-year, partly due to the low base effect from last year as a result of the floods and their impact on the production processes of some companies. In September, small business consumption decreased by 1.4% year-on-year, which was the same percentage as that by which household consumption increased.

Value of fiscally verified invoices – nominal, October 2024

After a decline in September, the nominal value of fiscally verified invoices rose by 2% year-on-year in October. Year-on-year growth in total turnover was primarily driven by a 2% increase in trade, which accounted for more than three-quarters of the total value of fiscally verified invoices issued. Turnover in retail trade, which had declined in September, was 4% higher year-on-year in October (6% higher on average in the first eight months). Turnover growth continued in the sales of motor vehicles (7%), while turnover in wholesale trade remained lower year-on-year (-6%). Following a moderation of growth in September, partly due to unfavourable weather conditions, turnover growth in accommodation and food service activities doubled in October (to 4%), although this growth was still significantly below the average for the first eight months (9%). Turnover growth in certain creative, arts, entertainment and sports services and betting and gambling remained at a similar level to the previous month (4%) but still well below the average for the first eight months (11%).

Trade in goods – in real terms, September 2024

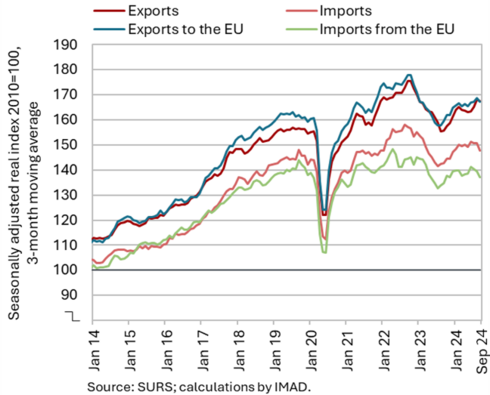

Real exports of goods increased in the third quarter compared to the second, while imports declined (seasonally adjusted); however, both exports and imports increased significantly year-on-year. Amid major monthly fluctuations, the quarterly increase in exports (by 2.6%) was primarily driven by stronger trade with Germany and non-EU countries. Notably, exports of intermediate goods (e.g. chemicals, metals and metal products) saw significant growth, along with certain products in the machinery and equipment group. Exports of pharmaceutical products (excluding goods processing) have been on a strong upward trend for several quarters, rising by approximately 30% in the third quarter compared to the same period last year. In contrast, exports to France declined sharply, mainly due to a drop in exports of road vehicles. In terms of imports (-2.3%), those of intermediate goods and capital goods fell month-on-month, while those of consumer goods remained at the level of the previous quarter (all seasonally adjusted). Year-on-year, both exports and imports saw significant growth in the third quarter (by 10.1% and 5.8% respectively), which is primarily due to the low base from the previous year and a higher number of working days in the third quarter of this year.

At the beginning of the last quarter of this year, sentiment in export-oriented manufacturing activities remained very low in Slovenia. As in the previous quarters, companies reported that the uncertain economic situation, weak domestic and foreign demand, and a shortage of skilled labour are the main obstacles to their business activity.

Trade in services – in real terms, September 2024

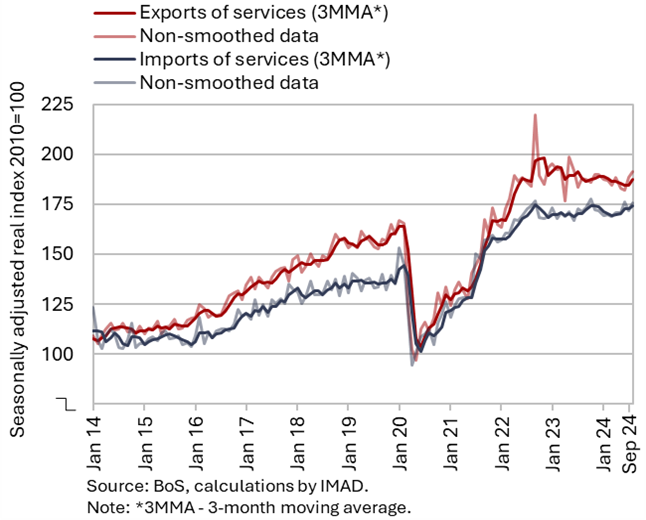

In the third quarter, imports and exports of services increased quarter-on-quarter, while they were lower year-on-year in the first nine months. Exports of services increased compared to the previous quarter, mainly due to higher exports of tourism-related services (particularly favourable in August), other business-related services and ICT services (seasonally adjusted). Exports in all of these service groups were also higher year-on-year in the third quarter. Exports of transport services remained unchanged quarter-on-quarter. Exports of construction services continued to decline and were around 15% lower than a year earlier. In terms of imports, quarterly growth was primarily driven by transport services, with imports of construction services also increasing, both reaching their highest levels of the past year (seasonally adjusted).

In the first nine months, exports of services declined year-on-year, while imports were slightly higher. The decline in exports was largely driven by a fall in trade in transport services, other business services and construction services. Exports of tourism-related services were also slightly lower year-on-year in this period, due to a significant decline in the second and early third quarters, while imports of these services were higher year-on-year.

Production volume in manufacturing, September 2024

Manufacturing output continued to shrink in the third quarter (despite a recovery in September) (seasonally adjusted) but was 3.0% higher than in the third quarter of last year (working day-adjusted). On average, production in low-technology industries fell in the third quarter, while in the other groups it was higher than or similar to the previous quarter (seasonally adjusted). In a year-on-year comparison, it was higher in medium-technology industries, while it remained largely unchanged in low- and high-technology industries. In the first nine months, manufacturing output was 0.7% higher year-on-year. After last year’s decline, production increased in most energy-intensive industries, with the exception of non-metallic mineral products (with modest activity in construction). All energy-intensive industries are still lagging behind pre-crisis levels, most notably the paper industry, where production is more than a fifth lower than at the start of 2021. The manufacture of motor vehicles, trailers and semi-trailers remained lower than a year ago.

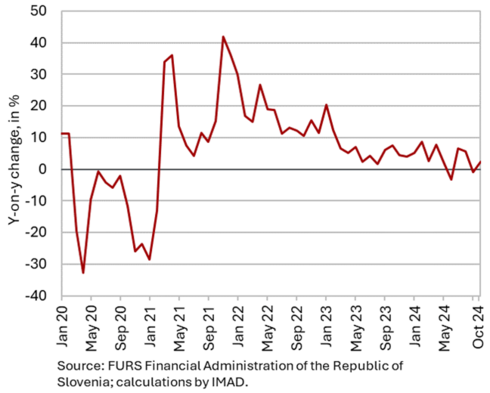

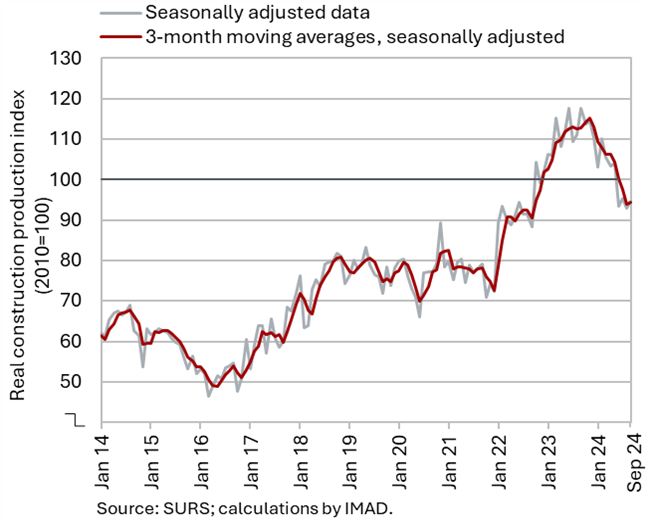

Activity in construction, September 2024

According to data on the value of construction work put in place, construction activity continued to decline in the third quarter, remaining significantly lower than in the same period last year. After last year’s robust growth of construction activity, the value of construction put in place this year has fallen sharply. In September, the value of construction put in place was 18% lower year-on-year, and for the first nine months combined, it was down by 10%. The most significant year-on-year drops were seen in civil engineering (down 14%) and construction of buildings (down 13%), while the smallest decline occurred in specialised construction activities (down 6%).

This lower activity was (among other things) related to government investment activity. Capital expenditure (according to the consolidated general government budgetary accounts) was 6% lower in the first nine months of this year than in the same period last year. However, spending on new buildings, reconstructions and adaptations – areas most closely tied to construction activity – plummeted by 27%.

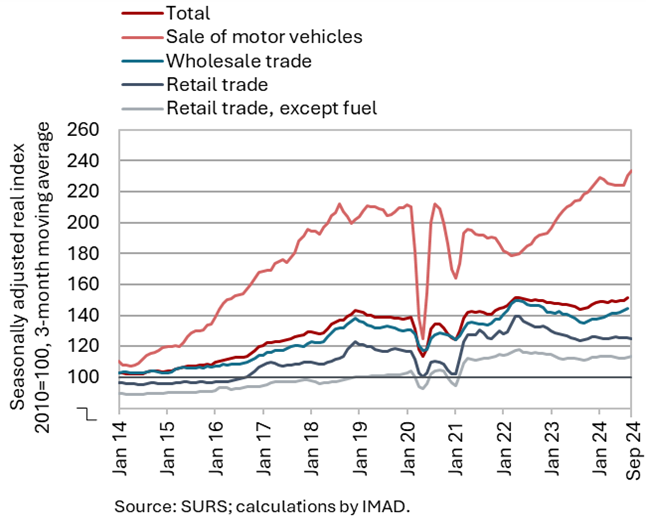

Turnover in trade, August–September 2024

In August, real turnover increased in most trade sectors and was also higher at the annual level. In August, turnover in the sales of motor vehicles increased for the third month in a row; in the first eight months, it was 8% higher year-on-year. After stagnating in the first half of the year, turnover in retail sales of food, beverages and tobacco increased for the second consecutive month (it was 2% higher year-on-year in the first eight months). Turnover also increased in retail sales of non-food products (remaining on average similar to last year’s levels over the same period). Among non-food products, after robust growth in 2021 and 2022, sales of pharmaceuticals and medical products declined year-on-year for the second year in a row, while sales of household appliances and audio and video equipment increased by around 10% year-on-year in the first eight months. After two months of growth, turnover in wholesale trade declined slightly (but was up 2% year-on-year on average in the first eight months). According to preliminary SURS data, turnover in September declined in the sales of motor vehicles and in the retail sales of food and non-food products.

Turnover in market services, August 2024

Real turnover in market services continued to increase slightly in August and remained higher year-on-year (by 1.3%). Total turnover rose month-on-month for the second month in a row, this time by 0.9% (seasonally adjusted). The strongest growth was observed in administrative and support service activities, where declines in employment and travel agencies came to a halt. Turnover growth also resumed in information and communication, driven by higher sales in the two main services (telecommunications and computers services). After stagnating in the first half of the year, turnover in accommodation and food service activities increased for the second month in a row. However, after robust growth in the previous month, turnover declined in professional and technical activities, as it did in transportation and storage. After three months of growth, turnover also declined in real estate activities. In the first eight months, transportation and storage was the only activity with a year-on-year decrease in real turnover.

Selected indicators of household consumption, August–September 2024

Household consumption in the third quarter was 1.9% higher year-on-year in real terms. Households spent more on new passenger cars and non-food products (up by 3.5%). Expenditure on tourist services abroad was also higher year-on-year (up by 4.7% in nominal terms), with the number of overnight stays by Slovenians in Croatia rising by 0.5% year-on-year. Turnover in retail sales of food, beverages and tobacco was similar to the third quarter of last year (+0.3%). However, the number of overnight stays by domestic tourists in Slovenia in this period was down year-on-year (by 3.2%).

In the third quarter, the value of fiscally verified invoices (a turnover indicator) grew by 3% year-on-year in nominal terms. In the context of lower price growth, this represents the highest quarterly real growth of the year.

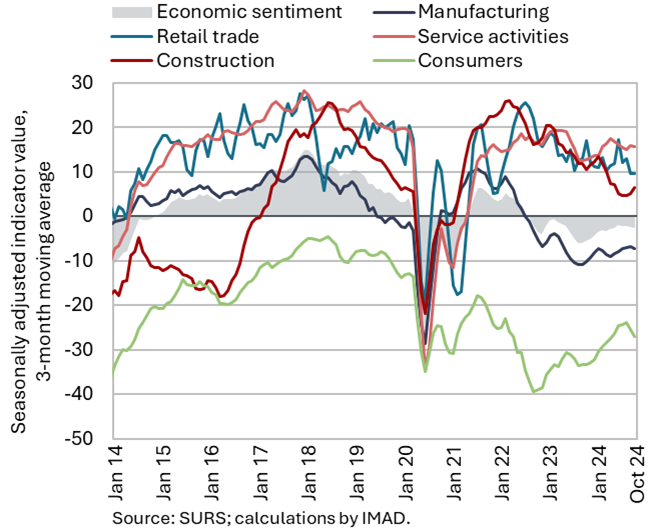

Economic sentiment, October 2024

In October, the value of the sentiment indicator fell compared to September, although it remained higher than in the same month last year. All confidence indicators contributed to this monthly decline except for construction, which had no impact. Year-on-year, sentiment indicators improved among consumers, in manufacturing and in services, while they deteriorated in construction and retail trade. Consequently, the economic sentiment indicator has been below its long-term average for around two years. Of all the confidence indicators, only indicators in services and construction were above their long-term averages.

Road and rail freight transport, Q2 2024

In the second quarter of 2024, the volume of road freight transport remained unchanged, while the volume of rail transport continued to increase. With the total volume of road transport performed by Slovenian vehicles remaining unchanged, cross-trade increased again, up by almost 4%, while road traffic performed at least partially on Slovenian territory (exports, imports and national transport) recorded a decline. The volume of road goods transport fell by 5% year-on-year and by almost 14% compared to the second quarter of 2019. In this longer-term comparison, cross-trade has declined by as much as a third. Despite some improvement in the first two quarters of this year, its share of total transport remains below 45%, almost 6 p.p. lower than before the COVID-19 epidemic. Rail freight transport, which had increased sharply at the end of last year, initially fell this year but rose again in the second quarter of 2024. It also increased year-on-year, by 5%, though it remained 4% lower than in the same quarter of 2019.

Number of persons in employment, August 2024

The number of persons in employment rose slightly in August (seasonally adjusted), with year-on-year growth (1.1%) slightly below the average for the first seven months. Employment remained higher in August than at the end of last year, as this year’s acceleration of year-on-year growth is largely due to a change in the definition of persons in employment at the beginning of the year, which now includes workers posted abroad. In August, growth in the number of persons in employment was again strongest in construction, which is facing a severe labour shortage, further impacted by the aforementioned change in definition. As has been the case for the past year, the year-on-year increase in the overall number of persons in employment was driven by a rise in the number of employed foreign nationals, while the number of employed Slovenian citizens fell. The share of foreign citizens among all persons in employment was 15.8% in August, 1.2 p.p. higher than a year earlier. The activities with the highest shares of foreign workers were construction (50%), transportation and storage (34%), and administrative and support service activities (28%).

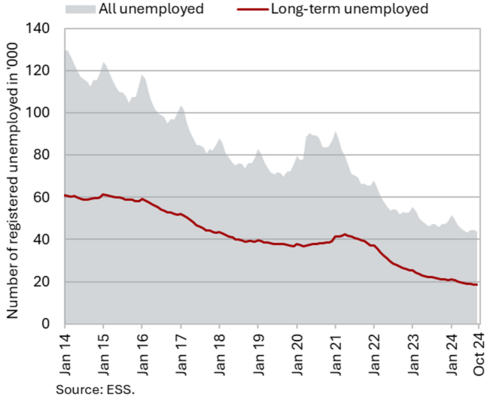

Number of registered unemployed persons, October 2024

In October, the number of unemployed persons (seasonally adjusted) remained similar to the previous month. According to original data, 45,463 people were unemployed at the end of October, 3.7% more than at the end of September. This increase largely reflects seasonal trends, driven by a higher inflow of first-time job seekers into unemployment. Year-on-year, the number of unemployed was 3.7% lower in October, although this decrease was smaller than in previous months. Amid labour shortages and retirement of older employees, the numbers of long-term unemployed (those unemployed for more than one year) and of unemployed over 55 fell year-on-year at the end of October, by 12.7% and 9.9% respectively.

Average nominal gross wage per employee, August 2024

In August, the year-on-year real growth of the average wage remained relatively high (4.9%). Growth in the public sector (2.7%) was similar to the previous two months and higher than on average in the first five months, which is attributed to adjustments in the pay scale grades implemented in June, in accordance with the agreement on the partial adjustment of wages to inflation. Year-on-year wage growth in the private sector (5.9%) was higher in real terms than on average in the first seven months. This was primarily due to lower year-on-year inflation amid continued strong upward pressure on (nominal) wage growth stemming from a shortage of labour. In the first eight months, overall average gross wage increased by 6.5% year-on-year in nominal terms – by 7.7% in the public sector and by 4.3% in the private sector. This increase was lower than that observed in the same period last year.

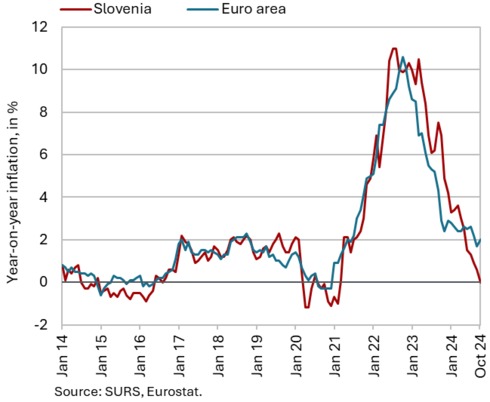

Consumer prices, October 2024

Inflation continued to ease in October, with prices declining by 0.5% month-on-month while remaining unchanged year-on-year. This time, inflation eased mainly due to a new method of calculating network charges for electricity, which led to a roughly 10% month-on-month decrease in electricity prices, while year-on-year, electricity prices were down by 22.7%. Prices in the housing, water, electricity, and gas and other fuels group were 8.6% lower year-on-year in October. A year-on-year decline in goods and services prices was also observed in the transport and communications groups (by 3.1% and 0.3% respectively). In the food and non-alcoholic beverages group, the year-on-year price increase was roughly on a par with the previous month (1.4%), as was the decline in durable goods prices (by 1.2%). Following a marked seasonal price drop in July and August, prices in the clothing and footwear group saw a significant seasonal increase for the second month in a row, further strengthening the growth of semi-durable goods prices in October (reaching 2.1%). Monthly price declines in package holidays and services within the restaurants and hotels group contributed to a further gradual slowdown in services price growth, which at 3.2% year-on-year in October reached its lowest point since March 2022.

Slovenian industrial producer prices, September 2024

With Slovenian industrial producer prices remaining stable on a month-on-month basis, the year-on-year decline eased slightly in September, reaching -0.9%. This decrease was largely driven by an 8.4% drop in energy prices and a 1.4% decline in intermediate goods prices, although the latter’s price drop is gradually easing (prices were still 4.7% lower year-on-year at the beginning of the year). For the first time since June 2020, prices in the capital goods group were also lower year-on-year (-0.1%). Meanwhile, growth in consumer goods prices remained stable (1.2%). Domestic prices continued to decline year-on-year (-2.1%), with decreases observed in all groups except consumer goods. In September, prices on foreign markets were higher year-on-year (by 0.2%) for the first time since August 2023. This growth was mainly driven by a 2% increase in prices on non-euro-area markets, while prices in euro-area markets declined by 0.4% year-on-year.

Loans to domestic non-banking sectors, September 2024

Year-on-year growth in the volume of loans to domestic non-banking sectors nearly tripled in September compared to August, reaching 5.0%, the highest rate since the beginning of 2023. This substantial increase was primarily driven by strong growth in NFI loans. Their volume rose by almost 60% month-on-month (EUR 725 million) and by 75% year-on-year. Lending to other sectors remained largely consistent with the activity observed in the first eight months of the year. The decline in lending to non-financial corporations continued to slow gradually, with a 3.6% year-on-year decrease recorded in September. Meanwhile, the year-on-year increase in household loans has stabilised at just under 6% in recent months. Year-on-year growth in consumer loans remains high (15% in September), although it is gradually slowing. Meanwhile, the growth of household loans strengthened slightly, reaching 3%. With NFI deposits falling by more than 40%, the year-on-year growth in non-banking sector deposits remains above 2%. Household deposits are also rising at a similar rate. They rose by EUR 483 million in the first nine months, the lowest level since 2015. We estimate that this is also due to the relatively low interest rates on deposits, which are also lagging behind the euro area average. The quality of banks’ assets remains solid, with the share of non-performing loans holding steady at 1% since April of last year.

Current account of the balance of payments, September 2024

The surplus on the current account of the balance of payments was EUR 691 million higher year-on-year in the third quarter of this year. This increase was mainly due to the goods trade balance (EUR 497 million). Real exports of goods increased more sharply year-on-year than imports, and the terms of trade improved again. We estimate that the quantity fluctuations contributed EUR 271 million to the year-on-year change in the balance of goods trade in the third quarter and the terms of trade contributed EUR 226 million. The surplus in trade in services was also higher year-on-year, due to a larger surplus in trade in technical, trade-related services; the surplus in trade in travel and transport was also higher. The primary income deficit was smaller year-on-year in the third quarter. This was mainly due to lower net outflows of dividends and profits and higher net interest income from investments by domestic commercial banks in foreign debt securities. The secondary income deficit remained largely unchanged. The 12-month balance of the current account of the balance of payments showed a surplus of EUR 3.2 billion in September (4.8% of estimated GDP).

Revenue of the consolidated general government budgetary accounts (top figure) and expenditure of the consolidated general government budgetary accounts (bottom figure), Q3 2024

In the third quarter of this year, the deficit of the consolidated balance of public finances was lower year-on-year, continuing the trend seen in the first half of the year. The deficit amounted to EUR 160.2 million in the third quarter, compared to EUR 384.5 million in the same period last year, and was halved to EUR 432.7 million year-on-year in the nine-month period. Revenue increased by 10.3% year-on-year in the third quarter, marking a slowdown compared to the second quarter (14.2%), mainly due to slower growth in VAT revenue, a year-on-year decline in revenue from the EU and lower growth in revenue from corporate income tax, which remained significantly higher year-on-year in all three quarters due to a higher tax rate and higher balancing payments of tax this year. Growth in non-tax revenues (profit sharing and property income) and revenues from excise duties accelerated, particularly due to increased excise duties on certain energy products and tobacco products. As in previous quarters, the third quarter also saw strong growth in revenue from social contributions, attributed largely to the transformation of the complementary health contribution into a mandatory contribution, and in revenue from personal income tax, which is due to the labour market conditions and the lack of adjustment of the income tax scale and tax relief to inflation this year. Expenditure rose by 6.2% year-on-year in the third quarter, a slower growth compared to the second (10.1%), the decline being primarily due to a large year-on-year reduction in expenditure on subsidies, investments, interest, and goods and services. However, the high growth in transfers to individuals and households was maintained, mainly due to the high regular annual adjustment of pensions at the beginning of the year. In the last two quarters, expenditure on sickness benefits, which had declined last year, began to rise again year-on-year. The quarterly growth dynamics of expenditure on salaries and wages and other personnel expenditure is affected this year by a change in the timing of the payment of holiday allowances (in the first quarter this year, but otherwise in the second quarter), and the growth of this expenditure was much lower in the nine-month period than in the same period last year.

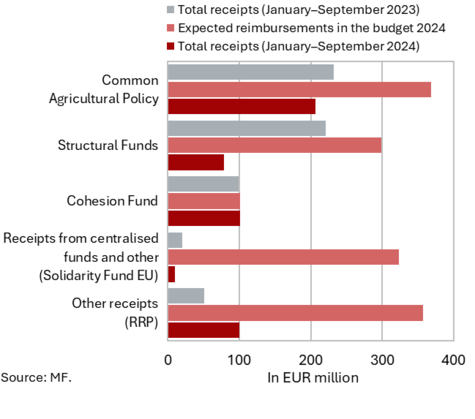

EU budget receipts, September 2024 (top figure) and absorption of 2014–2020 ECP funds (EU part) for the period 1 January 2014–30 September 2024 (bottom figure)

Slovenia’s net budgetary position against the EU budget was positive in the first nine months of 2024 (at EUR 42.2 million). In this period, Slovenia received EUR 498.1 million from the EU budget (34.4% of receipts envisaged in the adopted state budget for 2024) and paid EUR 455.9 million into it (63.4% of planned payments). The bulk of receipts (41.5% of all reimbursements to the state budget, 56.2% of the planned reimbursements in 2024) were resources for the implementation of the common agricultural and fisheries policies and resources from the Cohesion Fund (20.3% of all reimbursements to the state budget, 100.4% of the planned reimbursements in 2024). Reimbursements from the structural funds amounted to 15.8% of all reimbursements (26.4% of the planned reimbursements in 2024). The highest payments into the EU budget came from GNI-based payments (50.2% of all payments).

According to the MKRR data, under the Operational Programme for the Implementation of EU Cohesion Policy 2014–2020 (from January 2014 to the end of September 2024), payments from the state budget totalled EUR 3.55 billion (EU share), representing 106% of the available funds. Under the Operational Programme for the Implementation of EU Cohesion Policy 2021–2027 (from January 2021 to the end of September 2024), payments from the state budget totalled EUR 48.3 million (EU share), which corresponds to 2% of the available funds.