Slovenian Economic Mirror

Slovenian Economic Mirror 6/2024

At the turn of the third quarter, the available economic indicators for Slovenia were mostly higher year-on-year, while month-on-month data primarily pointed to continued growth in trade. In other sectors, indicators remained largely stable compared to previous months. Goods exports and imports fell in August, although they remain higher than a year ago, mainly due to growth in trade in vehicles and pharmaceutical products. Trade in services was lower year-on-year in the first seven months, mainly due to decline in trade in transportation and other business services. In August, production volume in manufacturing remained largely unchanged from July but was higher year-on-year. Real turnover in market services increased in July, as did real turnover in trade, especially in the sales of motor vehicles and sales of food and non-food products. According to data on the value of construction work put in place, construction increased slightly in July, although it remained significantly lower than in the same month last year. After an improvement in August, economic sentiment slightly deteriorated in September, though it remains stronger than in the same period last year. The value of the confidence indicator was lower in retail trade and construction, where the year-on-year decline was the sharpest. In contrast, indicator value in other activities and among consumers were higher than a year ago. Growth in the number of persons in employment continued in July; when seasonally adjusted, the decline in the number of registered unemployed came to a halt in September; year-on-year wage growth was higher in July than in previous months. The year-on-year growth of consumer prices (0.6%) continued to moderate in September. Prices remained unchanged month-on-month on average, with the year-on-year inflation declining due to a higher base in September last year, largely influenced by the expiry of the partial exemption from the RES and CHP contribution.

Contributions to GDP growth in the euro area, Q2 2024

In the second quarter of 2024, euro area GDP grew by 0.2%, with economic sentiment indicators suggesting that similar growth continued in the third quarter. Net trade was the main driver of growth in the second quarter, supported by positive contributions from government consumption and changes in inventories, while investments and, to a lesser extent, private consumption declined. Services contributed to the increase in value added, while activity in industry and construction declined. Survey indicators point to continued moderate economic growth in the euro area during the third quarter. The composite Purchasing Managers’ Indicator (PMI) slipped into contractionary territory in September (49.6), with the average value for the third quarter still pointing to weak growth in activity. Growth was driven by services, with the services PMI remaining above 50 throughout the quarter. The manufacturing PMI pointed to a further contraction in September, amid a persistent decline in new orders. The Economic Sentiment Indicator (ESI) in the euro area has remained virtually unchanged since the beginning of the year but was slightly higher year-on-year in September. Sentiment improved among consumers and in services but weakened in other activities. According to the ECB and OECD projections from September, euro area GDP growth is expected to reach 0.8% or 0.7% this year respectively, with both institutions forecasting 1.3% growth for 2025.

GDP growth forecasts for Germany, September 2024

According to September forecasts from international institutions, Germany’s GDP growth is expected to recover slightly next year after two years of stagnation or recession. After a slight improvement at the beginning of the year, activity fell again in the second quarter, with the available indicators suggesting that GDP also declined in the third quarter. Manufacturing production and construction activity were down on average in July and August compared to the second quarter, and the composite PMI, which has been falling since June, was at its lowest level in a year in September (47.2). The international institutions expect real GDP to pick up in the coming quarters as real incomes and thus private consumption continue to rise, foreign demand increases, and the dampening effects of tight monetary policy fade. In their joint September forecast, the German institutes projected a 0.1% decline in Germany’s GDP this year, followed by growth of 0.8% in 2025 and 1.3% in 2026. The German economy is facing major structural challenges (decarbonisation, digitalisation, demographic pressures and stronger competition with companies from China) and the adjustment processes are dampening economic growth.

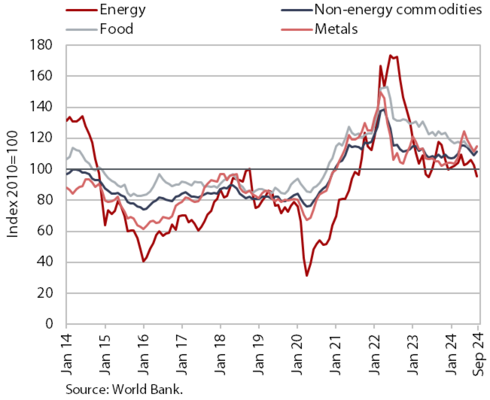

Commodity prices, September 2024

In September, the price of Brent crude oil declined and was also lower year-on-year; prices of non-energy commodities rose in September both month-on-month and year-on-year. The average dollar price of Brent crude oil dropped for the second consecutive month, reaching USD 74 (a 7.9% decrease compared to August), while the average euro price fell to EUR 66.7 (a 8.7% decrease compared to August). Year-on-year, the dollar price of Brent oil decreased by 21% and the euro price by 24%. This decline is largely attributed to relatively weak demand from China amid a slowdown in economic activity growth. The price of Brent oil rose to over USD 80 per barrel in early October as the conflict in the Middle East escalated. The euro prices of natural gas on the European market (Dutch TTF) fell to EUR 36.1 per MWh in September, down 5.9% from August (they were 2.2% lower year-on-year). According to the World Bank, the average dollar price of non-energy commodities increased slightly in September (by 2.3% compared to August). Among the main commodity groups, food prices rose markedly, driven primarily by higher grain prices. Prices of non-energy commodities were 2% higher in September, with prices of beverages rising in particular (by 63.3%), especially of cocoa and coffee.

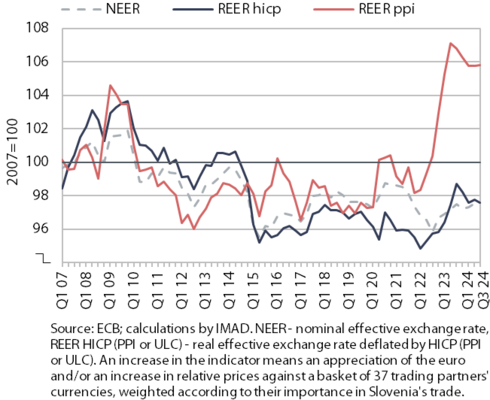

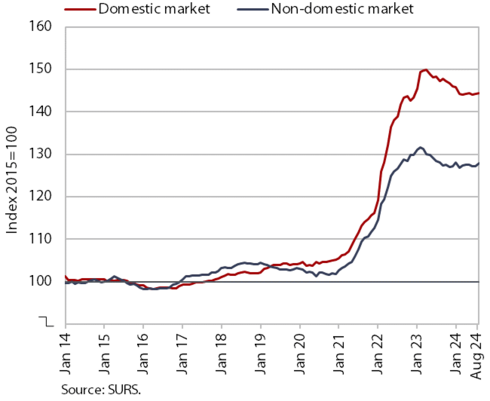

Effective exchange rate, Q3 2024

Price competitiveness indicators have improved slightly since mid-2023, but the price competitiveness of industrial producer prices in manufacturing remains relatively unfavourable. After a sharp deterioration in 2022 and the first half of 2023, the price competitiveness indicators, REER hicp and REER ppi, improved slightly in the second half of 2023 and the beginning of 2024 before stabilising in the last two quarters. During this period, their dynamics were primarily driven by relative price movements (i.e. the growth of Slovenian prices compared to growth in its trading partners), which have risen sharply since early 2022 due to cost pressures but have declined in the last four quarters. Both indicators remain above pre-energy crisis levels, with the REER ppi – reflecting the price competitiveness of industrial producer prices in manufacturing – being particularly high.

Short-term indicators of economic activity in Slovenia, July–August 2024

The available economic indicators for Slovenia were mostly higher year-on-year at the turn of the third quarter. On a month-on-month basis, they point primarily to continued growth in trade. In other sectors, they remained largely stable compared to previous months, with goods exports and imports showing a month-on-month decline in August. Economic sentiment slightly deteriorated in September, though it remained stronger than in the same period last year. Both exports and imports of goods decreased month-on-month in August, though remaining higher than a year ago. In the first eight months, exports and imports of goods were on average higher year-on-year (by 3.1% and 2.8% respectively, based on original data). Trade in vehicles and pharmaceuticals were the main contributors to year-on-year growth. Trade in services was lower year-on-year in the first seven months. This was mainly due to trade in transport and other business services. In August, the production volume in manufacturing remained largely unchanged from July (seasonally adjusted), following declines in previous months; in the first eight months of the year, production was 0.6% higher than in the same period last year (working day-adjusted). After decreasing in the second quarter, real turnover in market services increased in July. It was also higher year-on-year in all segments except transportation and storage, where it is still below last year’s levels. Real turnover in trade also rose in July, particularly in the sales of motor vehicles, but also in the sales of food and non-food products; it was also higher year-on-year. Construction activity, which has been gradually declining since the beginning of last year, was 12% lower year-on-year in July. Following an improvement in August, economic sentiment deteriorated slightly in September, though it remained higher year-on-year.

Electricity consumption by consumption group, August 2024

In August, electricity consumption in the distribution network was higher year-on-year. The main reason for this was higher industrial consumption (4.2% year-on-year), largely due to the effects of last year’s low base as a consequence of the floods and their impact on production processes in certain companies. Small business consumption was 1.8% lower year-on-year in August, while household consumption was similar to last year’s level. The low base effect was not noticeable in household consumption, as household electricity consumption increased in the days following the floods last year, mainly due to the drying of properties.

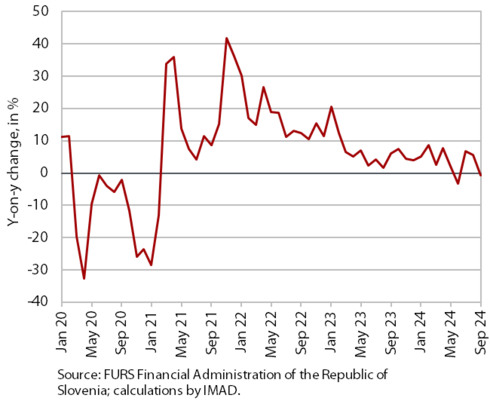

Value of fiscally verified invoices – in nominal terms, September 2024

After two months of relatively strong year-on-year growth, the nominal value of fiscally verified invoices was 1% lower year-on-year in September. This weaker growth can be attributed to last year’s higher base, driven by increased purchases after the floods, which affected trade performance, and unfavourable weather conditions this year, which have dampened the growth of certain tourism-related activities. Turnover in trade was 2% lower year-on-year. Notably, turnover in retail trade, which accounted for nearly half of the total value of fiscally verified invoices, decreased year-on-year for the first time this year (by 1%). Turnover in the sales of motor vehicles was similar to September last year, while turnover in wholesale trade remained lower year-on-year. Year-on-year turnover growth in accommodation and food service activities, certain creative, arts, entertainment and sports services, and betting and gambling weakened significantly (overall growth in accommodation and food service activities and in other service activities was 3%, compared to 14% in August and an average of 9% in the previous eight months).

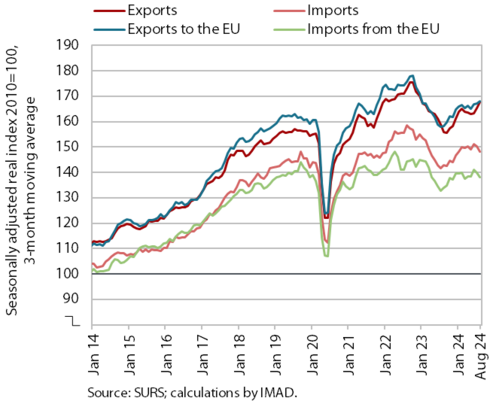

Trade in goods – real, August 2024

Both exports and imports of goods decreased month-on-month in August, though remaining higher than a year ago. After two consecutive months of growth, real exports fell by 1.9% in August compared to July. This was due to lower exports to EU countries (-2.8%), particularly to Italy, Austria, Croatia and France, while exports to Germany rose slightly. On a month-on-month basis, exports declined in most main product groups, although exports of pharmaceutical and other chemical products increased. Imports fell for the second month in a row (by 4.1%), with declines seen in imports from both EU and non-EU countries. Imports of consumer goods fell sharply (all seasonally adjusted).

In the first eight months, exports and imports of goods were on average higher year-on-year (by 3.1% and 2.8% respectively, based on original data). Trade in vehicles and pharmaceuticals were the main contributors to year-on-year growth. Sentiment in export-oriented activities and expectations for export orders remained at a very low level in September.

Slovenia’s export market share in the EU market, Q2 2024

Slovenia’s export market share of goods in the EU market continued to increase in the first half of 2024 (by 5.9% year-on-year), returning to the pre-pandemic and pre-energy crisis levels. In the first two quarters of this year, it was around 0.50%. In the second quarter, year-on-year growth of EU imports continued to lag behind that of Slovenian exports. The market share of road vehicles has increased significantly year-on-year, but it remains below the levels seen at the end of 2021. The market share of pharmaceutical products, electrical machinery and equipment, and most energy-intensive product groups (chemical products, non-metallic mineral products and metals, and the paper industry) has also continued to increase. Among Slovenia’s most important trading partners, the strongest year-on-year increases in the country’s market share were recorded in France and Croatia and the share was also higher in Germany. Slovenia holds the largest market share in Croatia (11%), while its market share in Germany, the country’s most important trading partner in terms of its share in total Slovenian goods exports, stands at 0.57%.

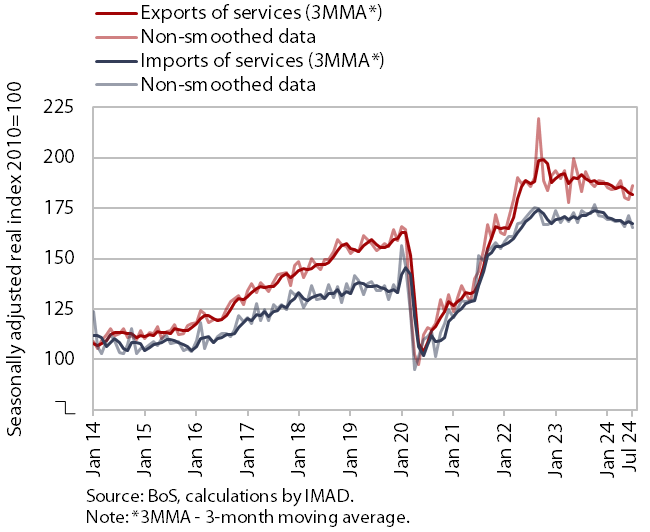

Trade in services – in real terms, July 2024

In July, trade in services was almost on a par with the previous months, with exports increasing and imports falling; in the first seven months, trade in services was down year-on-year. The month-on-month increase in exports in July was mainly due to exports of administrative and support service activities and ICT services, while exports of tourism-related services also increased slightly. Exports of transport services declined but were higher than at the beginning of the year. Imports of most main groups of services were lower than in previous months, with only a slight increase in imports of ICT services (seasonally adjusted). Both exports and imports of services were higher in the first seven months than in the same period last year, mainly due to the decline in trade in transport and administrative and support service activities. Exports of tourism-related services was also lower than in the same period of 2023, while imports remain higher year-on-year.

Production volume in manufacturing, August 2024

In August, production volume in manufacturing remained largely unchanged from July (seasonally adjusted), following declines in the previous few months. A further decline was observed only in low-technology industries, while other groups according to technological intensity either experienced growth or remained stable. In the first eight months, manufacturing output was slightly higher than in the same period last year (by 0.6%, working day-adjusted). Production rose in most medium-technology industries, with the metal industry showing the most significant growth compared to last year (starting from last year’s low base). Conversely, the decline remained largest in the production of other non-metallic mineral products. Production in most low- and high-technology industries was lower year-on-year in the first eight months. The sharpest declines were recorded in the wood-processing and furniture industry and in the leather industry.

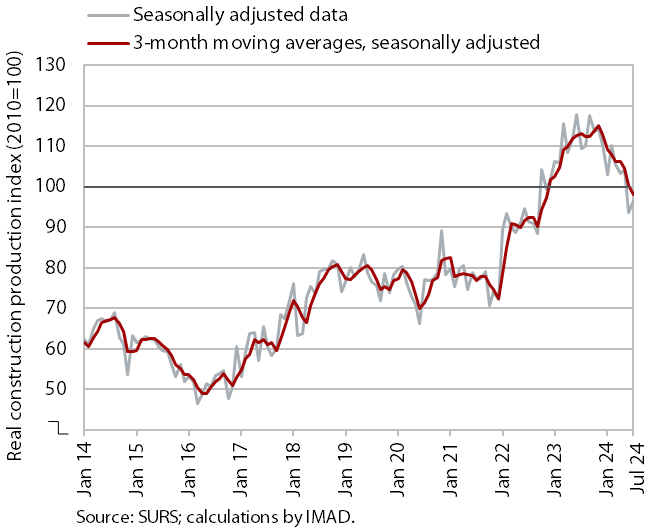

Activity in construction, July 2024

According to data on the value of construction work put in place, construction increased slightly in July, although it remained significantly lower than in the same month last year. After experiencing robust growth at the beginning of last year, the value of construction work put in place gradually declined both last year and in the first half of this year, with monthly fluctuations. In July, it was 12% lower compared to the same month last year. The largest year-on-year decline was recorded in civil engineering (by 21%). Activity also decreased in the construction of buildings and specialised construction activities. This lower activity was (among other things) related to government investment activity. While government investment expenditure (according to the consolidated general government budgetary accounts) remained nearly unchanged in the first seven months of the year compared to the same period last year (-3%), expenditure on new construction, reconstruction and renovation, which has a bigger impact on construction activity, dropped by as much as 26%.

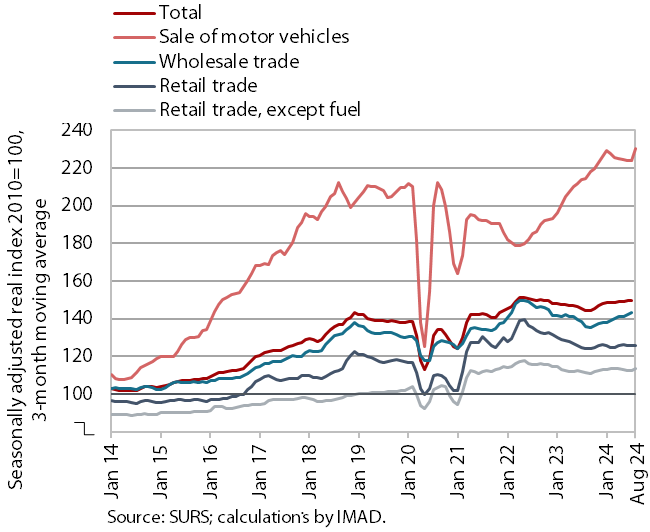

Turnover in trade, July–August 2024

Real turnover in the trade sector rose in July and, according to preliminary data, again in August; it was also higher year-on-year. Following declines in the first two quarters, turnover in the sales of motor vehicles rebounded strongly in July (and in August, according to provisional SURS data), rising by 8% year-on-year in the first seven months. Turnover in wholesale trade continued to grow, increasing by 2% year-on-year in the first seven months. After stagnating in the first half of the year, retail sales of food, beverages and tobacco increased in July (and in August, according to preliminary SURS data) and was already 2% higher year-on-year in the first seven months. Retail sales of non-food products also rose, though they remained largely unchanged year-on-year. Among non-food items, after robust growth in 2021 and 2022, sales of pharmaceuticals, medical devices, and computer and telecommunications equipment declined for the second year in a row, while sales of household appliances and audio and video equipment increased by 11%.

Turnover in market services, July 2024

After a decline in the second quarter, real turnover in market services increased in July and was also higher year-on-year (by 4.6%). Total turnover grew by 1.8% month-on-month in July, following a 1.4% decline in the second quarter. The most notable turnover growth occurred in professional and technical activities, where a three-month downward trend in architectural and engineering services came to a halt. After stagnating in the first half of the year, accommodation and food service activities experienced a strong increase in turnover. Similarly, turnover in transportation and storage increased, driven by growth in land and air transport. Meanwhile, turnover continued to fall in information and communication and in administrative and support service activities, though at a slower pace than in the previous month. The decline in the former was primarily due to a further drop in turnover in telecommunication services, while the latter saw continued drops in turnover in employment and travel agencies. The level of turnover in real estate activities remained stable compared to the previous month. In the first seven months of 2024, transportation and storage was the only activity to record a year-on-year decrease in real turnover.

Selected indicators of household consumption, July–August 2024

The available data indicate a year-on-year increase in household consumption at the start of the third quarter. The number of new passenger cars sold to natural persons was 20% higher year-on-year in July and turnover from the sales of motor vehicles rose by an average of 10% in real terms in July and August. During the same period, spending on food, beverages and tobacco also rose year-on-year (by 2% in real terms), and after a year-on-year decline in the first half of the year, spending on non-food products also rose (by 5% in real terms). In July and August, the number of overnight stays by domestic tourists in Slovenia was similar to last year, while spending on tourist services abroad was 1% higher in nominal terms in July. The year-on-year growth in household consumption during the third quarter is also evident from the year-on-year growth in the nominal value of fiscally verified invoices, which stood at 4% in the third quarter.

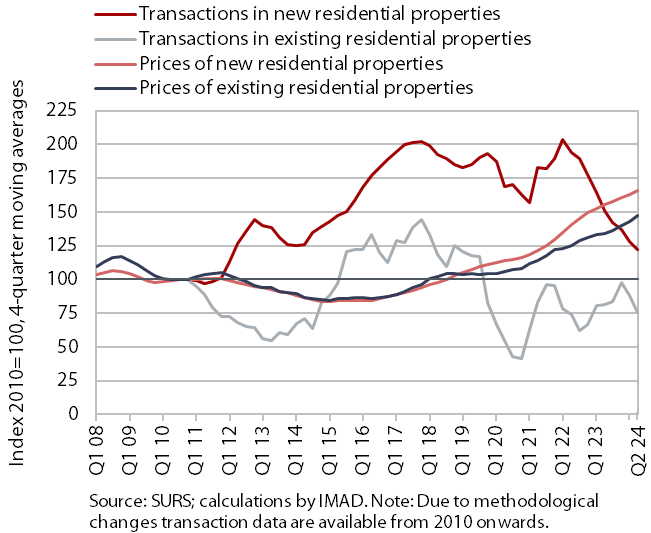

Real estate, Q2 2024

Amid a further decline in the volume of sales, year-on-year growth in dwelling prices remained relatively strong in the second quarter. After price growth halved last year (to 7.2% on average), prices in Q2 2024 were 6.7% higher compared to the same quarter in 2023 and 2.2% higher compared to the first quarter of this year. Prices of existing dwellings, where the number of transactions declined significantly in the last two years, were 6.1% higher year-on-year. Year-on-year growth in newly built dwellings was even stronger (15.4%). The number of transactions in this segment, which represents only a small part of total sales (4%), fell sharply year-on-year (by more than a half), after being relatively high in 2023 (almost 50% higher than in 2022 and at the highest level since 2018).

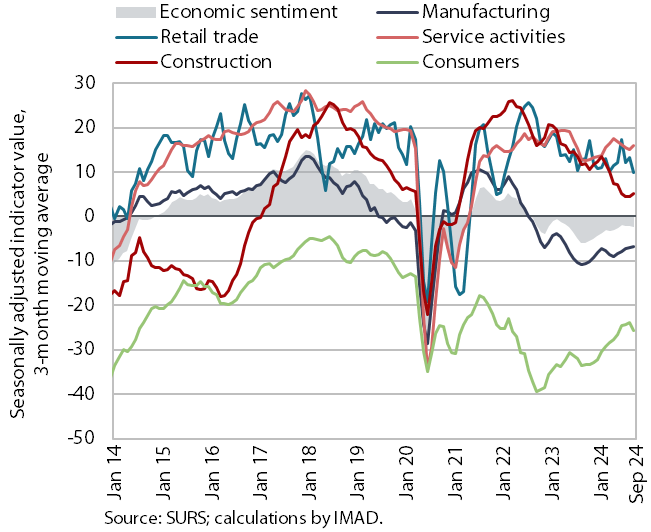

Economic sentiment, September 2024

Following an improvement in August, economic sentiment deteriorated slightly in September, though it remained higher year-on-year. The monthly decline in the economic sentiment indicator was driven by lower confidence among consumers and in all activities with the exception of services. The economic climate indicator improved compared to September last year. Confidence in retail trade and construction declined, with construction showing the largest year-on-year drop (in this activity, indicators for overall order levels and employment expectations fell both month-on-month and year-on-year). In contrast, confidence indicators in other activities and among consumers were higher than a year ago.

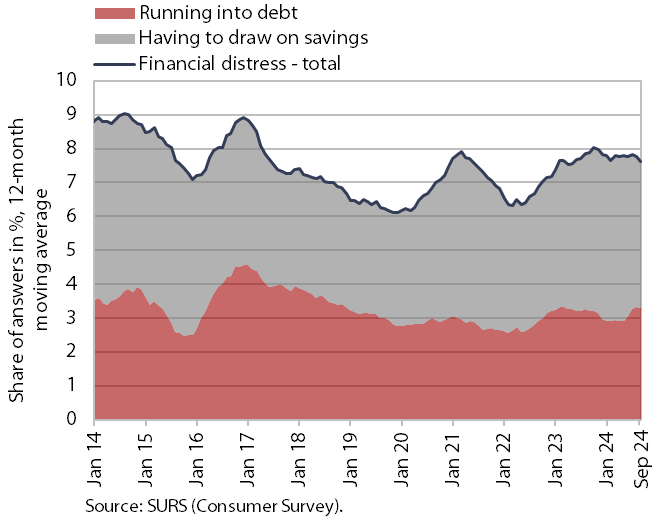

Households facing financial distress, September 2024

The situation of households facing financial distress deteriorated slightly on average in the third quarter, while it improved slightly compared to the same quarter last year. Compared to the previous quarter, the share of households facing financial distress increased the most among those in the lowest-income quartile (from 11.9% to 13.5%), while their financial situation improved year-on-year (the share fell by 5.4 p.p.). The share of households facing financial distress having to draw on savings to meet their needs declined year-on-year. According to our estimate, this was partly due to positive developments in the labour market (higher employment and wages). The share of households running into debt increased year-on-year, partly due to the relaxation of the Bank of Slovenia’s requirements for obtaining consumer loans.

Number of persons in employment, July 2024

The number of persons in employment increased slightly month-on-month in July (seasonally adjusted), with year-on-year growth (1.1%) slightly below the average for the first six months but still higher than at the end of last year. This year’s acceleration of year-on-year growth is largely due to a change in the definition of persons in employment at the beginning of the year, which now includes workers posted abroad. In July, growth in the number of persons in employment was once again strongest in construction, which is facing a severe labour shortage, further impacted by the aforementioned change in definition. The year-on-year increase in the overall number of persons in employment was driven, as has been the case for the past year, by a higher number of employed foreign nationals, while the number of employed Slovenian citizens fell. The share of foreign citizens among all persons in employment was 15.8% in July, 1.1 p.p. higher than a year earlier. The activities with the highest shares of foreign workers were construction (50%), transportation and storage (34%), and administrative and support service activities (28%).

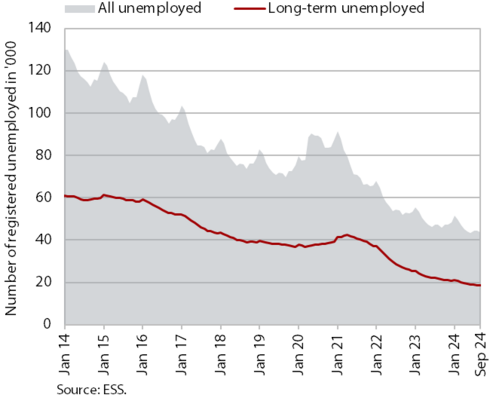

Number of registered unemployed persons, September 2024

The month-on-month decline in the number of registered unemployed (seasonally adjusted) came to a halt in September, with the number of unemployed increasing slightly (by 0.3%). According to original data, 43,847 people were unemployed at the end of September, 1.4% less than at the end of August. Year-on-year, the number of unemployed was 4.7% lower in September, marking a smaller decrease than in previous months. Amid labour shortages and retirement of older employees, the numbers of long-term unemployed (more than one year) and of unemployed over 55 fell year-on-year at the end of September, by 13.6% and 10% respectively. In the first nine months, just over 1% of the unemployed moved to inactivity or retirement each month, similar to previous years, which also contributed to the decline in unemployment.

Average real gross wage per employee, July 2024

The year-on-year growth in the average gross wage in July (5.8%) was higher in real terms than in previous months. In the public sector, it was similar (3%) as in June and higher than in the previous months, which was related to the increase in the value of the pay scale grades in June, in line with the agreement on the partial adjustment of wages to inflation. Wage growth in the private sector (7.4%) was higher in real terms than on average in the first six months, which is related mainly to lower year-on-year inflation and a severe labour shortage. In the first seven months, the overall average gross wage increased by 6.6% in nominal terms – by 7.8% in the public sector and by 4.4% in the private sector.

Number of FSA beneficiaries and UB recipients, July 2024

In July, the numbers of financial social assistance (FSA) beneficiaries and of unemployment benefit (UB) recipients were lower year-on-year. The number of UB recipients stood at 12,832 (original data) in July, which is significantly below the long-term average. Year-on-year, this represents a 6.8% decline in the number of recipients. The unemployed recipients of financial social assistance (18,730 persons) mainly include the long-term unemployed and persons with a lower level of education. Despite the high demand on the labour market, some people are unable to find a suitable job because they belong to the group of people with low employment prospects. Amid high employment and a fall in the number of long-term unemployed, the number of FSA beneficiaries continued to fall year-on-year in July. In July, 71,513 persons were entitled to FSA (original data), which is 5.1% less than a year ago.

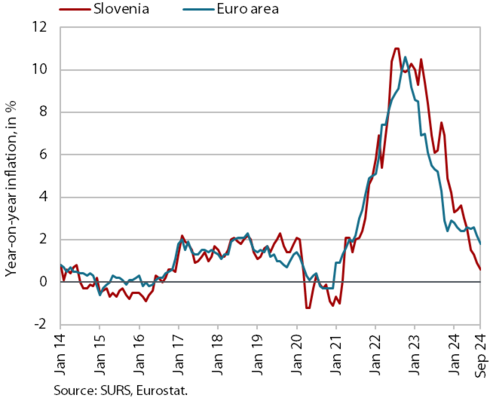

Consumer prices, September 2024

The year-on-year price growth (0.6%) continued to moderate in September. Prices remained unchanged month-on-month, with the year-on-year slowdown in inflation mainly due to a higher base, largely influenced by the expiry of the partial exemption from the RES and CHP contribution in September last year. The year-on-year price decline in the housing, water, electricity, gas and other fuels group thus nearly doubled in September compared to August (-6.1%), while the monthly price drop was modest. After two months of strong seasonal price declines, the seasonal price increase in the clothing and footwear group was more pronounced in September than in previous years (14.3% month-on-month), though prices remained lower year-on-year (0.6%). Year-on-year growth in services prices decelerated somewhat, though remaining relatively high (3.9%). We estimate that the slower growth this time was primarily due to the moderation of price growth in the restaurants and hotels group, where prices were 4.2% higher year-on-year (compared to a 6.7% increase in August). The prices of food and non-alcoholic beverages rose slightly month-on-month in September, while their year-on-year growth increased by 0.1 p.p. to 1.5% compared to August.

Slovenian industrial producer prices, August 2024

The year-on-year decline in Slovenian industrial producer prices slowed slightly in August (to 1%, compared to 1.9% in July). In addition to the lower base, a somewhat stronger monthly price increase of 0.4%, the highest since February 2023, also contributed to the smaller year-on-year decline this time. Prices were higher both on the domestic (by 0.2%) and foreign markets (by 0.5%). On a monthly basis, prices increased in most industrial groups, with the most pronounced increase in non-durable consumer goods (by 2%), while only the prices of durable consumer goods fell (by 2.2%). Lower prices in the raw materials group (by 1.8%) continued to contribute the most to the year-on-year price decline, while energy prices also fell by around a tenth. The strongest price increase was recorded for non-durable consumer goods (2%). Slovenian industrial producer prices continued to be lower year-on-year, both on the domestic market (by 1.9%) and on the foreign market (by 0.2%).

Loans to domestic non-banking sectors, August 2024

Year-on-year growth of loans to the domestic non-banking sectors strengthened slightly in August, though it remained relatively subdued (1.8%). This growth was mainly due to increased growth in housing loans (2.9%) in recent months. Amid solid household spending on durable goods (cars, furniture, household appliances), consumer credit continued to expand at the fastest pace (15.7%), though growth has gradually slowed. However, new lending in the form of consumer credit remains robust, accounting for nearly half of total new lending to households in August. Corporate and NFI borrowing remains subdued, reflecting weak economic activity and relatively high interest rates, though the year-on-year decline has slightly eased in recent months (-2.5%). The year-on-year growth in non-banking sector deposits remains slightly above 2%. Despite the higher growth in time deposits (30%), their share remains at just over a fifth of total deposits in the non-banking sector. The quality of banks’ assets remains solid and the share of non-performing loans has remained unchanged at 1% since April last year.

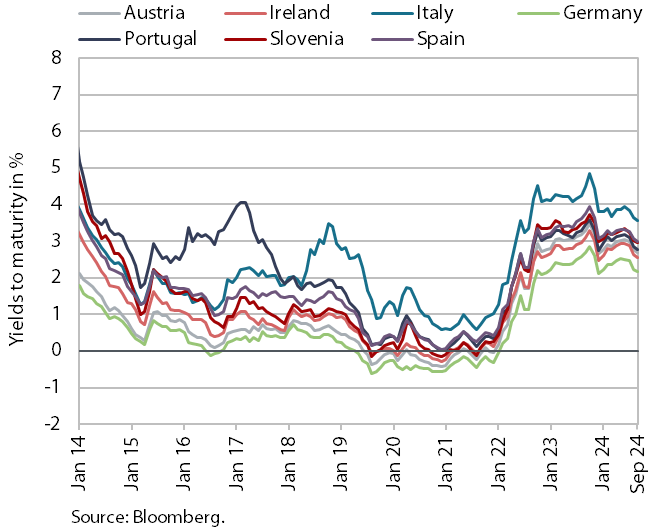

Government bonds, Q3 2024

Yields to maturity of euro area government bonds declined gradually throughout the third quarter. This was significantly influenced by the ECB’s monetary policy, which has already cut key interest rates twice this year as inflationary pressures eased. As a result, the yield on Slovenian bonds fell by 21 b.p. compared to the previous quarter, reaching 3.07%. However, the spread to the German bond remained largely unchanged (77 b.p.).

Current account of the balance of payments, July 2024

The surplus of the current account of the balance of payments increased in July, mainly due to the trends in trade in goods. The 12-month current account surplus was also higher than a year earlier, amounting to EUR 3 billion (4.6% of estimated GDP for 2024). The year-on-year increase was mainly due to a higher surplus in trade in goods. Primary and secondary income also contributed to the improvement in the current account balance. The primary income deficit decreased due to lower net outflows of income from equity capital (dividends and profits) and higher net interest receipts by the Bank of Slovenia from deposits in foreign accounts. The secondary income deficit decreased due to higher net positive transfers to the government sector from abroad (funds for current international cooperation from the EU budget) and higher private sector transfers (payments of non-life insurance premiums). The surplus in trade in services was lower than a year ago, mainly due to lower surplus in trade in travel services.

Revenue (top figure) and expenditure (bottom figure) of the consolidated general government budgetary accounts, August 2024

In the first eight months of this year, the deficit of the consolidated balance of public finances was lower year-on-year. It totalled EUR 379 million, compared with EUR 798 million in the same period last year. Revenues increased by 11.9% year-on-year. This growth was driven not only by increased revenue from social contributions, following the transformation of the complementary health contribution into a mandatory contribution, but also by higher corporate income tax revenues, resulting from a higher tax rate and balancing payments this year. Personal income tax receipts also contributed to this government revenue growth, reflecting labour market conditions and the lack of adjustment of the income tax scale and tax relief to inflation this year. Growth in revenues from VAT also strengthened. Revenues from excise duties decreased year-on-year, due to lower revenues from excise duties on energy products and electricity, while revenues from excise duties on tobacco products and on alcohol and alcoholic beverages increased. Total receipts from the EU budget were also lower year-on-year. In the first eight months of the year, expenditure increased by 8.8% year-on-year. The key drivers of this increase were (i) transfers to individuals and households, primarily due to the high regular annual indexation of pensions, (ii) expenditure on goods and services and other healthcare expenditure in connection with the transformation of the complementary health insurance into a mandatory contribution, along with flood recovery expenditure, and (iii) expenditure on salaries, wages and other personnel expenditure, which was influenced by the adjustment of pay grades this year (by 3.36%). Investment expenditure was lower year-on-year. From August 2023 to the end of August 2024, EUR 820.6 million had been disbursed from the state budget to rectify the consequences of floods and landslides, of which EUR 262.5 million was disbursed in the first eight months of this year, most of it for ongoing maintenance and insurance under the emergency Flood Recovery Act. In August, the European Commission proposed for Slovenia to be paid EUR 428.4 million in financial support from the EU Solidarity Fund (Slovenia had already received an advance of EUR 100 million in December last year) to help it deal with the consequences of the floods.

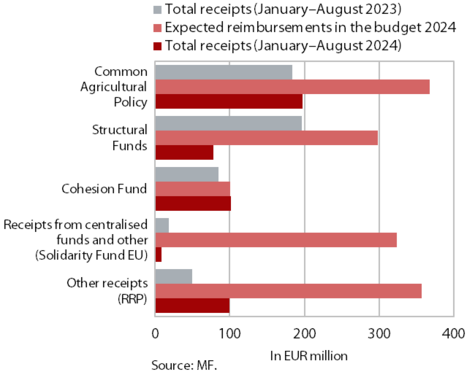

EU budget receipts, August 2024 (top figure) and absorption of 2014–2020 ECP funds (EU part) for the period 1 January 2014–31 August 2024 (bottom figure)

Slovenia’s net budgetary position against the EU budget was positive in the first eight months of 2024 (at EUR 84.5 million). In this period, Slovenia received EUR 488.6 million from the EU budget (33.8% of receipts envisaged in the adopted state budget for 2024) and paid EUR 404.1 million into it (56.2% of planned payments). The bulk of receipts (40.5% of all reimbursements to the state budget, 53.7% of the planned reimbursements in 2024) were resources for the implementation of the common agricultural and fisheries policy and resources from the Cohesion Fund (20.7% of all reimbursements, 100.4% of the planned reimbursements). Reimbursements from the structural funds amounted to 16.1% of all reimbursements (26.4% of the planned reimbursements). The highest payments into the EU budget came from GNI-based payments (49.9% of all payments).

According to the MKRR data, under the Operational Programme for the Implementation of EU Cohesion Policy 2014–2020 (from January 2014 to the end of August 2024), payments from the state budget totalled EUR 3.55 billion (EU share), representing 106% of the available funds. Under the Operational Programme for the Implementation of EU Cohesion Policy 2021–2027 (from January 2021 to the end of August 2024), payments from the state budget totalled EUR 44.4 million (EU share), which corresponds to 1% of the available funds.