Slovenian Economic Mirror

Slovenian Economic Mirror 4/2020

The consequences of dealing with the COVID-19 epidemic are being felt in the entire euro area – a decline in economic activity, historically low indicators of confidence and expectations, forecasts of a deep recession in 2020. In this uncertain situation, the pace of recovery will to a great extent depend on epidemiological conditions and economic policy measures at various levels. Since March, the epidemic and the urgent measures to contain its spread have also had a severe impact on economic activity in Slovenia, which has contracted particularly in individual more exposed sectors (trade, transportation, tourism, accommodation and food service activities). In the second quarter, the decline in activity is expected to deepen. Following a steep fall in April, economic sentiment improved somewhat in May, but confidence in all sectors and among consumers remains at record lows. With the adoption of containment measures, labour market conditions started to deteriorate noticeably in March. After a rapid rise, growth in the number of unemployed slowed down and only came to a halt only in recent weeks. By the end of May, the number of unemployed had risen to 90,415, which is 25.6% more than a year earlier.

Short-term indicators of economic activity in the euro area

Owing to the adoption of containment measures related to the COVID-19 epidemic, economic activity in the euro area contracted significantly in March. The March decline in short-term economic activity and confidence indicators was significantly more pronounced than at the peak of the economic and financial crisis in 2009. The sharp fall in turnover in retail trade (-11.2% relative to February) indicates a significant decline in household consumption. Owing to the shutdown of some production plants and supply chain disruptions, euro area manufacturing production dropped more than 11% at the monthly level. The decline was largest in durable goods production. Construction activity also decreased noticeably in March (by more than 14% relative to February). In the first quarter, euro area economic activity contracted by 3.8% in quarterly terms (3.2% year on year). An even greater decline is expected in the second quarter, when GDP is set to fall by around 12.0% relative to the previous quarter according to the EC’s forecasts.

The economic sentiment indicator (ESI) for the euro area

Economic sentiment in the euro area improved somewhat in May, but it remained significantly lower than at the beginning of the year. With the relaxation of measures, the value of the composite PMI rose slightly from April’s record lows. The indicator shows that euro area economic activity also contracted significantly in May, but less than in April. The value of the economic sentiment indicator (ESI) also stabilised after April’s record decline. Confidence declined further in service activities and construction, albeit less than in the previous two months, while it is expected to rise in industry and retail trade and among consumers. Judging by the Ifo Business Climate Index, expectations about the future economic situation are also optimistic in our most important export partner, Germany.

GDP, 1st quarter of 2020

In the first quarter of 2020, real GDP declined by 2.3% year on year. With increased uncertainty and the closure of all non-essential service activities due to the measures taken to contain the COVID-19 epidemic in mid-March, the decline was mainly attributable to a fall in the group of trade, transportation, and accommodation and food service activities. Household consumption dropped noticeably. Investment in fixed assets also declined, mainly as a consequence of lower investment in machinery and equipment. Exports and imports declined as well, due to a fall in world trade and international trade barriers. Final government consumption was the only consumption aggregate that strengthened year on year.

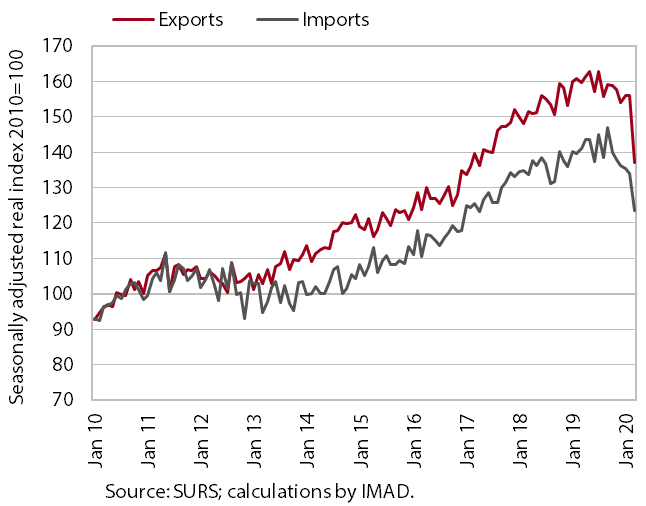

Trade in goods with the EU – real

Trade in goods, especially with EU countries, declined markedly in March with the spread of the coronavirus epidemic, particularly in neighbouring countries. Goods exports to the EU had already been slowing gradually for several months, but the marked decline in March was mainly due to measures to contain the epidemic in Slovenia’s main trading partners. The sharpest decline was recorded for exports to Italy, where, in addition to the closure of most shops, all non-essential production came to a standstill in the second half of the month. Owing to disruptions in international transport, significantly worse expectations regarding orders and the adoption of measures to contain the epidemic in Slovenia, imports also fell markedly in March.

Trade in services – nominal

External trade in services fell sharply in March. The introduction of measures to contain the epidemic, in particular the closure of the country’s borders and hotels and restaurants, had a major impact on tourism, as spending by foreign tourists, same-day visitors and transit passengers declined by almost 60%. The number of all overnight stays by foreign tourists has fallen sharply, in March by more than two-thirds year on year. Exports of transport and construction services were also noticeably lower (by around 12% and 13.6% respectively), while exports of ICT services continued to rise. Imports of services also fell, albeit to a lesser extent than exports. Spending by Slovenian tourists abroad dropped in particular.

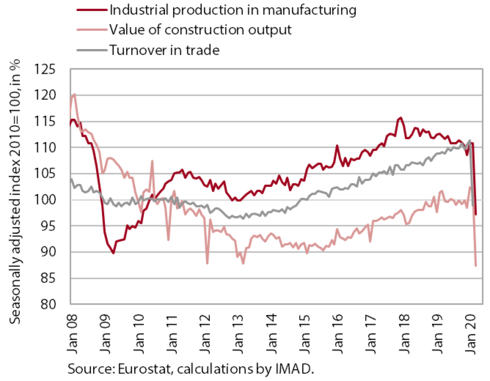

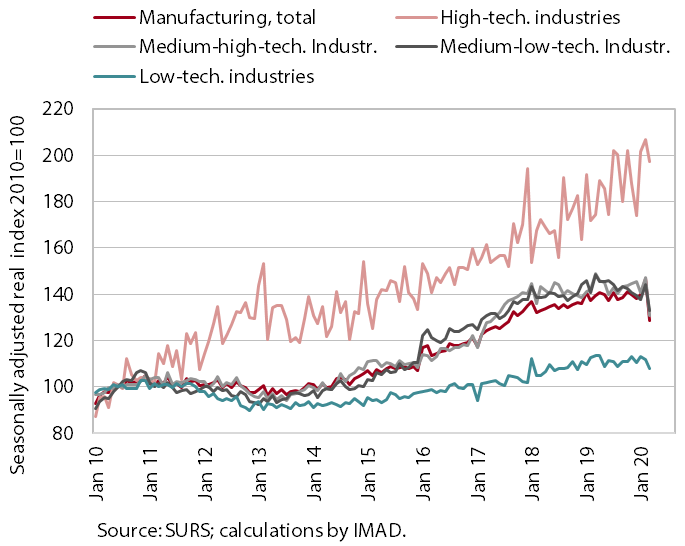

Production volume in manufacturing

With the spread of the coronavirus, manufacturing output declined sharply in the EU and Slovenia in March. The decline was similar to that at the beginning of the economic crisis at the end of 2008. It was attributable to lower foreign demand, supply chain disruptions and the shutdown of production in some companies after the declaration of the epidemic in Slovenia. Production fell the most in medium-low- and medium-high-technology industries. The decline in high- and low-technology industries was more modest, but in our assessment this was largely thanks to a few individual, less affected industries (the pharmaceutical industry and the food industry).

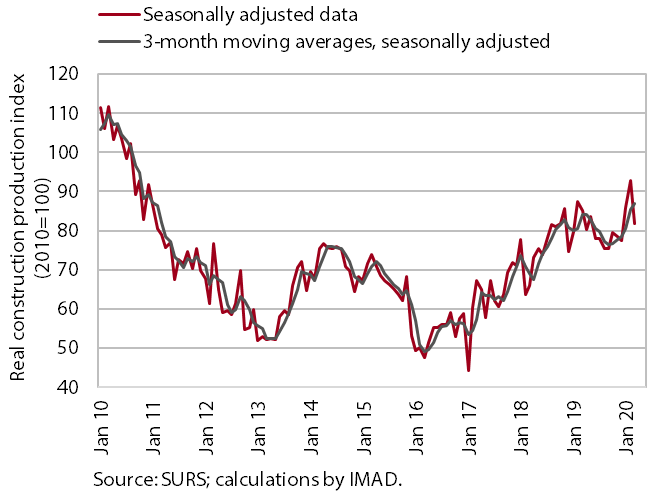

Activity in construction

After strengthening at the beginning of the year, activity in construction declined in March with the declaration of the epidemic and the adoption of measures to contain its spread. In March, the value of construction output fell in all construction segments. The decline was most intense in the construction of civil- engineering works (-17.6%) and smaller in the construction of residential (-5.5%) and non-residential (-4.4%) buildings. On account of the high activity in the first two months, the value of construction output in the first quarter as a whole was otherwise as much as 10.8% higher than in the last quarter of last year. In all three construction segments, the indicators of contracts also fell sharply in March, the least in civil-engineering works.

Turnover in trade

With the declaring of the epidemic and the closure of shops selling non-essential goods, turnover in trade fell sharply in March. In March and, according to preliminary data, also in April, the fall was largest in the sale of motor vehicles. With the adoption of measures to contain the spread of the virus and a decline in motor vehicle traffic, a significant fall was also recorded in retail sales of automotive fuels. Turnover was also down year on year in retail trade in non-food products, where, amid a fall in most sectors, it increased in the sale of pharmaceutical and medicinal products and in trade by mail order or the internet. Turnover in the sale of food products, which under the impact of uncertainty had already risen significantly in February, was also higher in March, while in April it was slightly lower year on year according to preliminary data.

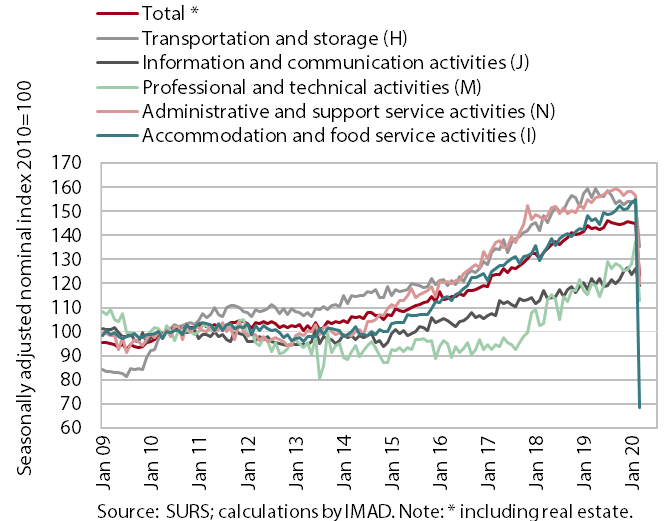

Nominal turnover in market services

Turnover in market services plunged in March in most areas. With the introduction of measures to contain the epidemic and hence the closure of all hotels and restaurants and the country’s borders, turnover declined the most in accommodation and food service activities. All of this also affected the activities of travel agencies, which together with employment agencies also contributed to a strong decline in administrative and support service activities. Owing to a sharp fall in turnover in architectural and engineering services, a considerable decline was also seen in professional and technical activities. Turnover also fell in transportation, mainly due to a complete shutdown of public passenger transport. The smallest decline was in information and communication activities, which we estimate is mainly related to sales on the domestic market.

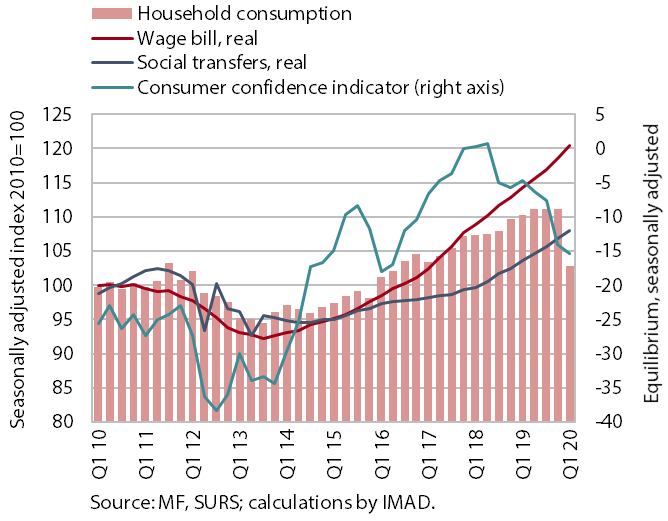

Selected indicators of private consumption

Household consumption declined in the first quarter due to the introduction of measures to contain the epidemic. It was 6.4% lower than a year earlier, mainly due to the closure of all service companies and shops selling non-essential goods in mid-March and to greater consumer caution. The uncertainty was also reflected in a deterioration in the consumer confidence indicator, which recorded a further sharp fall in April. Disposable income otherwise increased in the first quarter under the impact of further growth in the net wage bill (also as a result of the increase in the minimum wage in January and a change in personal income tax rates) and social transfers. With a decline in spending, household savings rose more strongly, which is already reflected in increased deposits.

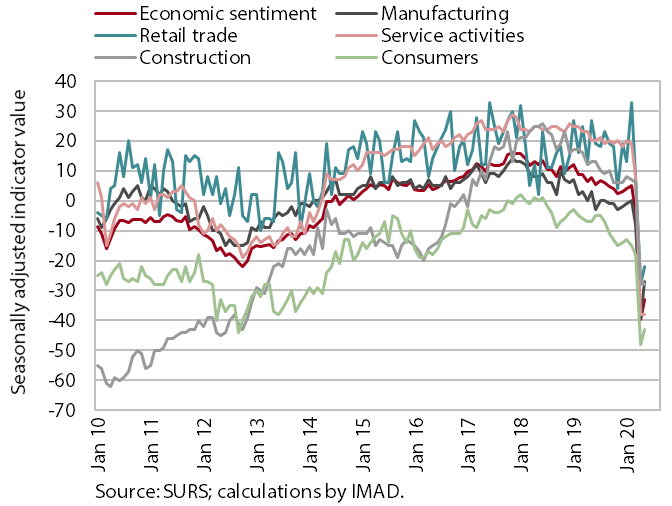

Economic sentiment

After a significant deterioration in economic sentiment in April, the indicators of expectations improved slightly in May but remained significantly lower than at the beginning of the year. Due to the spread of the epidemic, in addition to the situation indicators, the indicators of expectations also deteriorated significantly in all activities. Confidence declined most sharply in service activities and retail trade. Consumer confidence also fell, this to the lowest level since measurements began in 2005. In May, the indicators of expectations improved slightly, but they remained significantly lower than at the beginning of the year. In all sectors except construction, confidence in May was lower than during the economic and financial crisis ten years earlier.

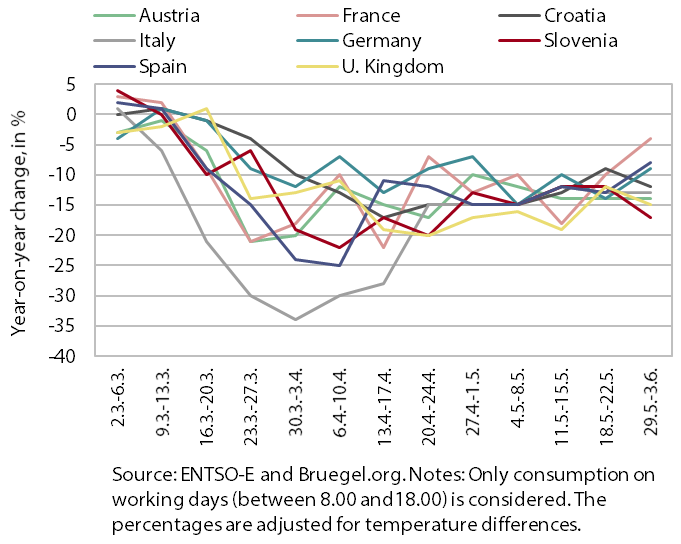

Electricity consumption in selected EU countries and the UK

After a pronounced decline in March and April, the year-on-year fall in weekly electricity consumption gradually started to slow in May. Electricity consumption, one of the indicators of economic activity, was on average 14% lower year on year at the weekly level in Slovenia in May (in April, with the spread of the epidemic, it declined by 20%). With more and more measures being relaxed, in May consumption also fell less than in previous weeks in most other countries. The only exception was Germany, with a 12% average decline in weekly consumption, which was more than the average weekly decline from the beginning of the crisis up to the end of April (9.5%).

Traffic of electronically tolled vehicles on Slovenian motorways

Freight traffic on Slovenian motorways, which declined markedly after the adoption of measures to contain the epidemic, was around one-fifth lower year on year in the last week of May. After a more than 40% decline in the weeks from mid-March to the second half of April, freight traffic was gradually rising until the end of May, but it remained lower than in the same period last year. The distance travelled by domestic and foreign trucks declined by around one-tenth and around one-quarter respectively. The fall in foreign truck traffic, which was initially much more pronounced than in domestic truck traffic, has since decreased under the impact of EU measures for the free flow of goods across borders and due to the easing of measures in some neighbouring countries.

Number of registered unemployed persons

The rapid deterioration in labour market conditions has eased somewhat in recent weeks. After a relatively favourable first two months, when employment increased particularly due to the hiring of foreigners, the year-on-year growth in the number of employed persons dropped sharply in March (0.6%; in March 2019, 3.1%). Registered unemployment started to rise after the outbreak of the epidemic in the second half of March. In the first half of April, the rapid increase continued. By the end of May, the number of unemployed persons had risen to 90,415, which is 25.6% more than one year earlier. On 4 June, the figure was 89,765, according to EES unofficial (daily) data, which is 0.7% less than at the end of May. The easing of labour market conditions in the last few weeks is attributable to the lifting of containment measures and a resumption of most activities, but also to the adoption of the first legislative package of intervention measures to mitigate the consequences of the epidemic for citizens and the economy and then the third package at the beginning of June.

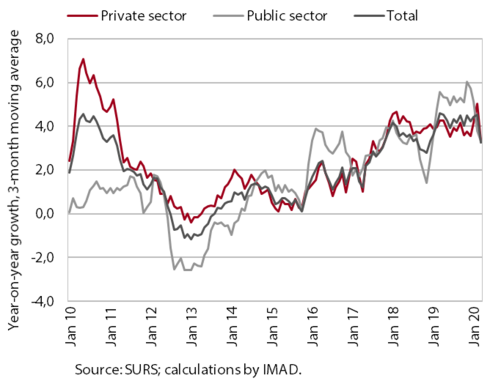

Average gross wage per employee

Year-on-year wage growth dropped sharply in March due to a fall in private sector wages. In the first two months, year-on-year wage growth in the private sector was still strong (4.7%), largely due to the increase in the minimum wage and a general shortage of workers. With a large part of employed persons posted to temporarily wait for work at home, the average wage was 1.4% lower year on year in March. The decline was particularly pronounced in accommodation and food service activities (18.8%). After moderate growth in the first two months, wage growth in the public sector picked up slightly in March (3.5%), partly due to a temporary introduction of additional pay for people working in crisis conditions.

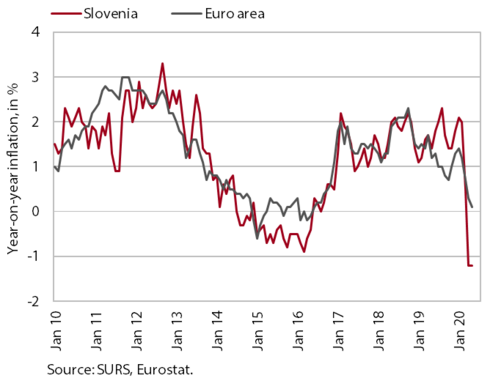

Consumer prices

The year-on-year price decline remained at 1.2% in May. Overall, the greatest contribution to deflation came from lower prices of energy (oil products and electricity), which lowered inflation by 2.4 pps according to our estimate. Without the counter-cyclical adjustment of excise duties on motor fuels, the negative contribution would have been even greater. Prices of semi-durable and durable goods remain lower year on year (by 2.9% and 2.3% respectively), while prices of food continue to rise. Owing to above-average seasonal growth, year-on-year growth in prices of fresh fruit rose significantly in May, to 23.4%, which we assess is a consequence of greater demand and a worse harvest (due to frost). Growth in meat prices also remains high. Growth in prices of services strengthened somewhat in May after easing in previous months.

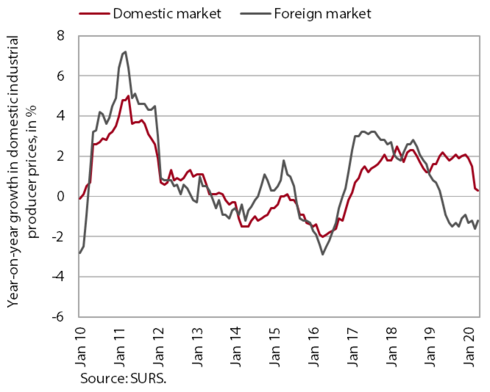

Slovenian industrial producer prices

Slovenian industrial producer prices declined year on year in April (by 0.4%). Prices were down particularly on foreign markets, this in all industrial groups. They fell by slightly more than 1% on average year on year. Prices on the domestic market were somewhat higher, mainly on account of higher prices of consumer goods. Consumption of non-durable goods has increased in recent months due to the spread of the epidemic, which has contributed to stronger growth in prices of this type of goods (over 3%), according to our assessment. Growth in durable consumer goods prices remains at around 1%. The significantly lower economic activity and the government measure which reduced electricity prices for households and small business consumers have contributed to a year-on-year decline in prices of raw materials and energy.

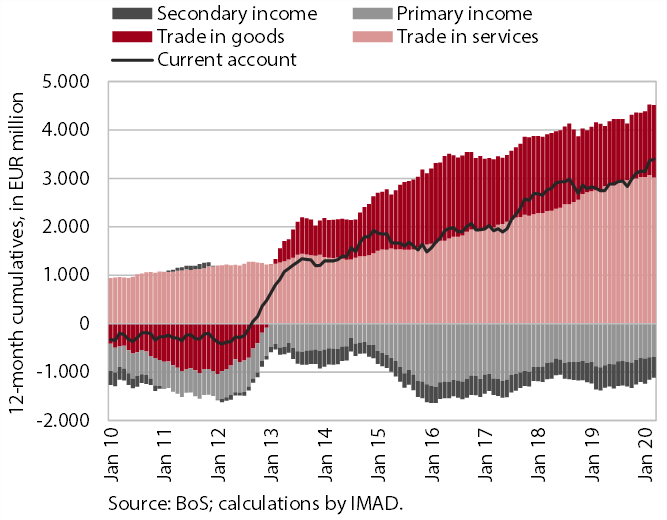

Current account

The measures to stem the spread of the epidemic had a significant impact on external trade in goods and services in the first quarter, while in other current account segments their impact was not yet perceived. In the first quarter, the current account surplus was again higher year on year. Its growth was mainly driven by the surplus in trade in goods. This was to a great extent attributable to developments in March, when goods trade fell significantly due to the adopted measures, with the decline in imports being larger than that in exports. After several years of growth, the surplus in services was lower year on year in the first quarter, particularly in trade in travel and air and railway transport services. Net outflows of primary income dropped further, mostly owing to lower net payments of income on equity and interest on external debt. The lower net outflows of secondary income were marked especially by lower payments into the EU budget.

Year-on-year growth rates of loans in the Slovenian banking sector

The volume of loans to domestic non-banking sectors dropped markedly at the monthly level in April, but, owing to solid lending activity in previous months, the moderate year-on-year growth continued. The monthly decline exceeded EUR 180 million, which is the largest fall since August 2016. A decline was recorded for both corporate and household loans. The volume of consumer loans, which decreased for the sixth consecutive month, thus recorded only 1.5% year-on-year growth. Since the outbreak of the epidemic, the sharpest fall has been in other household loans, including overdrafts. This can be attributed to a marked decline in spending, given that many shops, bars, restaurants and services activities were closed following the introduction of containment measures. Meanwhile, the growth in household deposits continued to strengthen in April, reaching almost 10% year on year. With low deposit interest rates, the overall growth was driven by overnight deposits.

Yields to maturity of ten-year government bonds

The yield to maturity of the Slovenian government bond remained unchanged in May. The yields to maturity of bonds issued by euro area countries were significantly influenced by the ECB’s decision to set up a fund for recovery after the pandemic. This led to a decline in bond yields of most euro area countries, particularly the more peripheral ones. The yield to maturity of the Slovenian bond did not change much, while the spread between the Slovenian and German bond yields increased slightly, to 126 basis points.

Consolidated general government budgetary accounts

In the first four months of this year, the deficit of the consolidated balance of public finance totalled EUR 793 million. The decline in revenue, which had still been limited to VAT and excise duties in the first quarter, extended to all major tax categories and social contributions in April. The fall in tax revenues is a result of paralysed economic activity, deferrals or instalment payments of tax liabilities made possible by the intervention legislative measures taken during the epidemic, and the tax reform adopted last year. The deficit also widened as a consequence of expenditure growth, which was higher than in the same period of last year and in the first quarter of this year, when, for the most part, it did not yet reflect the impacts of the epidemic and the support measures adopted. In April, these strengthened particularly transfers to individuals and households, subsidies, and other current transfers (for the purchase of protective equipment). To a lesser extent, the measures (the payment of bonuses for workers with additional workload during the epidemic and for work in difficult working conditions) also influenced wage bill growth. In the first four months, this strengthened year on year, mainly due to higher payments based on the adopted agreements and more funds paid by the ZZZS to public health institutes. As a result of increased ZZZS transfers to public institutes, the growth of expenditure on goods and services also strengthened considerably in the first quarter.