Slovenian Economic Mirror

Slovenian Economic Mirror 2/2020

At the end of last year, moderate economic activity in Slovenia continued, while confidence started to improve. Confidence improved in almost all sectors, particularly manufacturing. Enterprises in this sector have higher expectations about production volume and orders, which is related to the improvement in the global economy. On the labour market, unemployment continues to decline at a moderate pace, while higher household disposable income as a consequence of growth in wages, social transfers and employment has a favourable impact on private consumption.

(copy 1)

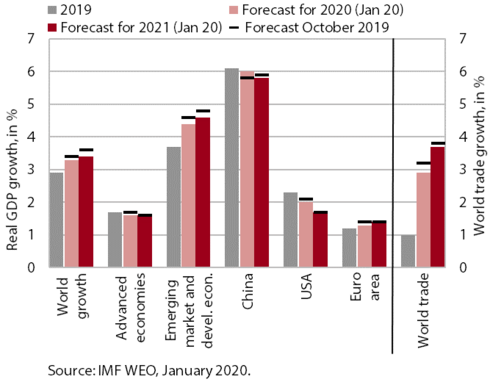

IMF forecast of economic growth and world trade for 2020 and 2021

The IMF downgraded its forecast for global economic growth and trade again at the beginning of the year; the forecast of the euro area is also somewhat lower. The IMF expects growth in the global economy and trade to strengthen to 3.3% and 2.9% respectively this year, which is lower than previously announced. The forecast for advanced and emerging market economies was downgraded the most, while the IMF is more optimistic regarding this year’s growth in China, particularly due to the moderation of trade tensions with the US. The forecasts for Slovenia’s main trading partners were not changed significantly. Euro area growth will strengthen to 1.3% this year due to higher foreign demand, but will be lower than predicted in October particularly due to the lower forecast for Germany, where manufacturing activity remained weak at the end of last year. After last year’s modest growth (0.5%), Germany is otherwise expected to reach 1.1% growth this year. According to the IMF, risks to the forecast remain mainly on the downside, despite the recent trade agreement between the US and China, the regulated withdrawal of the UK from the EU and the improvement in industry and global trade.

Goods trade (real)

The moderation of economic activity in Slovenia’s main trading partners also influenced the slowdown in external trade movements in the last quarter of 2019. Exports to Germany, Italy and Austria, the main destinations of Slovenian goods exports, declined year on year. Particularly exports of some main products for intermediate consumption, related particularly to the car industry, declined further. After several quarters, exports of vehicles increased again, particularly to France. In goods imports, a moderation is recorded particularly for growth in imports of intermediate products in connection with slower growth in manufacturing.

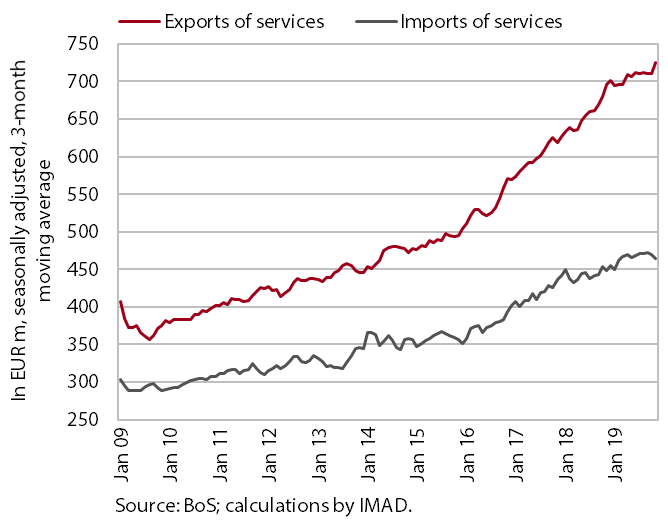

Trade in services – nominal

Nominal exports of services have strengthened again in the last few months, while imports have declined. A significant contribution to growth in exports of services came particularly from exports of information and communication services, technical, trade-related services and processing services related to distribution activity in the area of medicinal and pharmaceutical products. After several months of moderation, exports of construction services rose noticeably again. Growth in exports of transport services is visibly moderating, mainly due to the slowdown in international trade. The decline in imports of services is significantly influenced by technical, trade-related services, which were driving growth in previous years. Growth in imports of most other services continues at very low rates.

Slovenia’s export market share on the world and EU markets of goods

In the first three quarters of 2019, export market share on the world market increased particularly due to exports of medicinal and pharmaceutical products to Switzerland. After 4.4% growth in 2018, Slovenia’s export market share on the world goods market increased by 3.8% on average in the first three quarters of last year. The key contribution to growth came from stronger exports of medicines to Switzerland, but these being mainly re-exports of previously imported medicines, they had no major impact on domestic economic activity. This specific factor excluded, since mid-2018 Slovenian goods exports have mostly been rising more slowly than global import demand, i.e. Slovenia’s world export market share has been slightly declining. The general slowdown in export growth and, consequently, global market share, is partly due to the pronounced orientation of Slovenian exports to EU markets, where import demand (nominally, in USD) has been rising more slowly during this period than global imports on average.

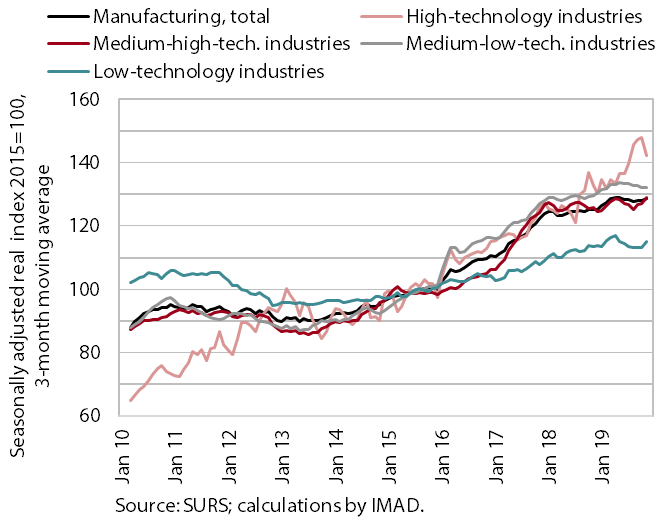

Production volume in manufacturing

At the end of the year, production volume in manufacturing remained at the level achieved in the first quarter. Particularly production in medium-high-technology industries strengthened again in the last few months of the year, but also production in low-technology industries, although both increased the least in the eleven months as a whole. High-technology production rose the most during this period, with significant fluctuations. Production in medium-low-technology industries, which mainly produce intermediate goods, remained almost unchanged.

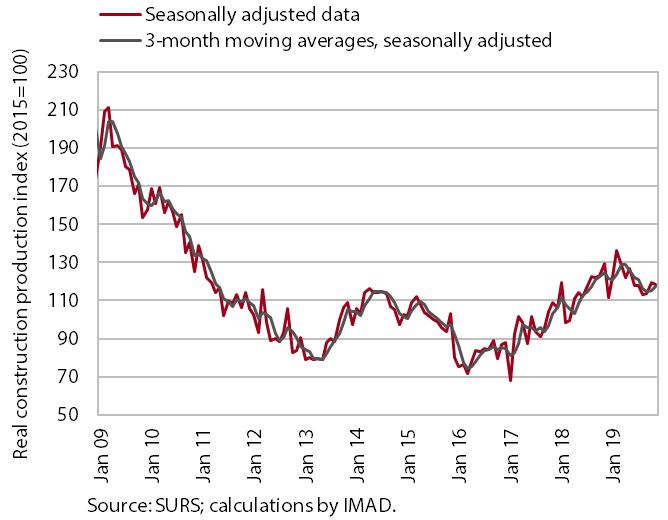

Activity in construction

The value of construction output increased towards the end of last year after several months of decline, but was lower than one year before. Following strong growth at the beginning of 2019, also owing to favourable weather conditions, the value of construction output fell in the middle of the year. The decline was the most pronounced in the construction of non-residential buildings, which was related to deteriorated expectations of the business sector and its investment activity. Towards the end of the year, activity strengthened across all construction sectors, the most in the construction of non-residential buildings. After increasing in the middle of the year, the stock of contracts was significantly higher year on year at the end of the year, while the number of new contracts was lower, with strong monthly fluctuations.

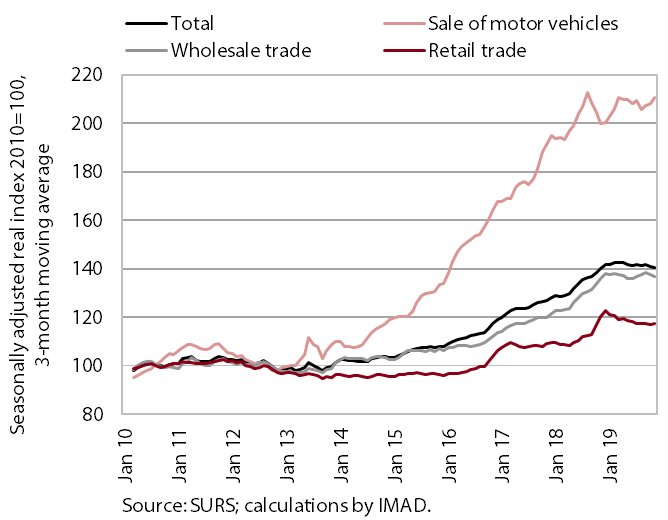

Turnover in trade

In November, turnover in trade maintained the level seen at the beginning of the year. Turnover in retail trade ceased declining in the last months to November. Amid a fall in the sale of automotive fuels and stagnation in the sale of food and beverages, November saw further modest growth in the sale of non-durable non-food products and a significant increase in the sale of household appliances. Turnover in wholesale trade remained similar to that at the beginning of 2019, which is attributable to the moderation of activity growth in related activities (especially manufacturing). Turnover in the sale of motor vehicles improved somewhat at the end of last year after stagnating in the first half. The improvement was a consequence of higher passenger car sales to natural persons and December’s high growth of sales to legal persons.

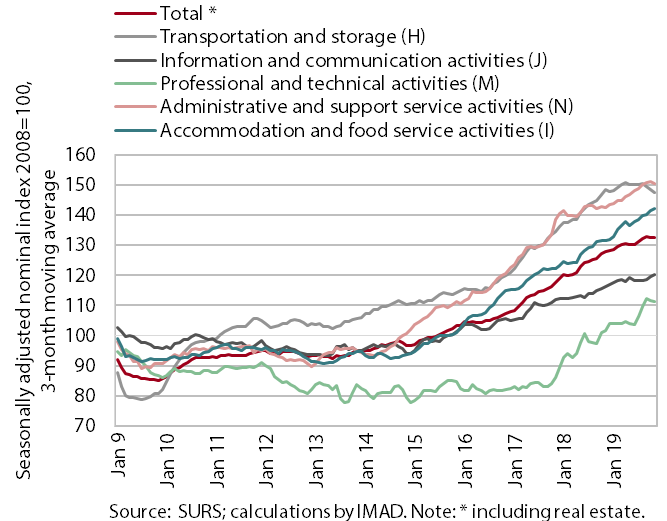

Nominal turnover in market services (other than trade)

Turnover in market services remained at the achieved level towards the end of last year. November saw a continuation of strong turnover growth in information and communication activities, which has, for a quite a long time, been due to growth in exports of computer services; turnover in telecommunications also increased significantly for the second consecutive month after several months of decline. Further growth was also recorded in accommodation and food service activities, mainly owing to good business results of enterprises serving food and beverages. Turnover growth in administrative and support service activities decreased, despite renewed growth in employment services. In professional and technical activities, turnover dropped again amid a further fall in architectural and engineering services. Since the middle of the year, turnover has also continued to shrink in most transportation activities.

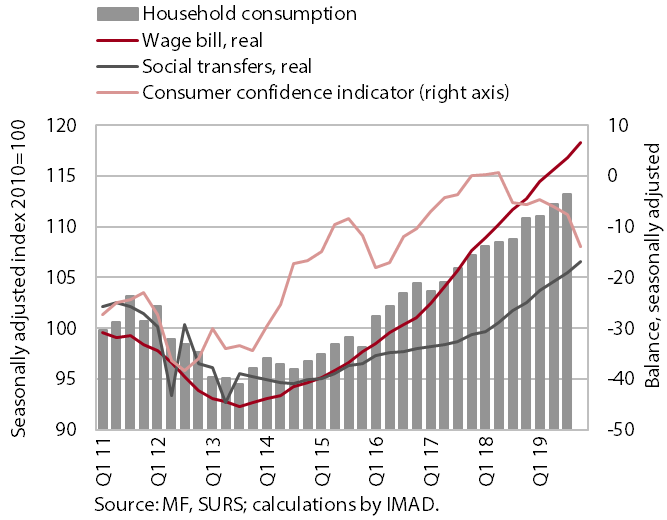

Selected indicators of household consumption

With rising disposable income, household consumption continued to grow in the last quarter of 2019. The increase in household resources was a result of stronger growth in the net wage bill and social transfers (including pensions). Newly granted consumer loans were lower year on year in November, following October’s significant increase (before the introduction of tighter borrowing conditions). Increased uncertainty regarding future economic conditions was also reflected in a decline in the consumer confidence indicator and further growth in household saving at the end of last year. Household deposits rose by EUR 628 million in the last quarter (relative to the third), or by EUR 1.7 billion (relative to December 2018) to EUR 20.8 billion.

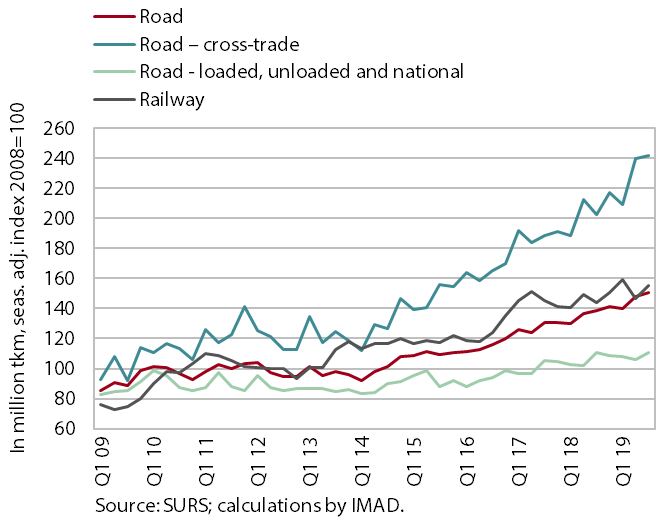

Road freight transport

The volume of road and rail freight transport increased in the third quarter of 2019. Road transport abroad (cross-trade and cabotage) increased further and was one fifth higher year on year. The volume of road transport that is at least partially connected to the territory of Slovenia (exports, imports and national transport together) increased as well, but maintained the level recorded in the same period of 2018. Growth in rail freight transport has slowed in the last two years compared with road transport, despite an increase in the third quarter.

Economic sentiment indicator

Economic sentiment improved somewhat again in January, but remains considerably lower year on year. The improvement was attributable to all sectors, except retail trade, where expectations about future sales dropped in particular. Higher confidence in manufacturing arose mainly from higher orders and business expectations regarding the volume of production. Confidence in construction and among consumers improved for the second consecutive month after a period of pronounced decline. Confidence in service activities, fairly stable in the last period, also remained relatively high.

The number of employed persons and the number of registered unemployed persons

Labour market conditions improved further towards the end of last year, but the improvement was less intense than in the previous year. In the first eleven months, the number of persons employed increased 2.5% year on year (the most in construction, transportation and storage, and accommodation and food service activities), which is less than in the same period of 2018. Employment growth is still largely based on the hiring of foreigners (their contribution to total employment growth exceeding 70%), which is a consequence of demographic change and the shortage of domestic labour. The number of unemployed persons continues to decline, albeit more slowly than at the beginning of 2019 amid increasingly limited labour supply. At the end of December, 75.292 persons were registered as unemployed, 4.1% fewer than in the same period of 2018.

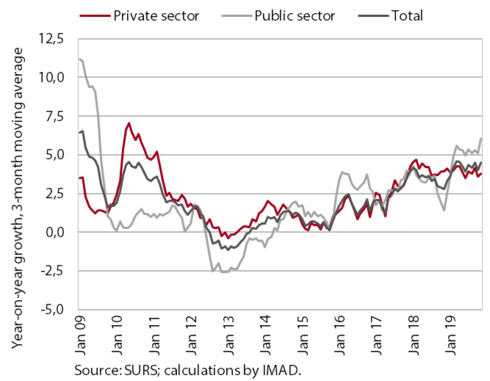

Average gross wage per employee

Last year, wage growth was higher than in 2018 mainly due to wage rises in the government sector. Year-on-year wage growth in the first eleven months as a whole was higher (4.3%) than in the same period of the previous year (3.4%). The higher growth was mainly a consequence of higher growth in the general government sector owing to the agreed wage rises and promotions. To some extent, it was also due to the increase in the minimum wage. With relatively low unemployment and good business performance, wage growth in the private sector remained similar to that one year earlier. Wages rose the most in administrative and support service activities and accommodation and food services activities.

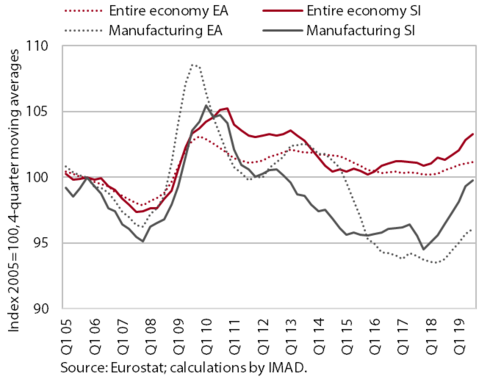

Real unit labour costs (RULC), total in the economy and manufacturing

Unit labour costs are rising in most sectors, notably manufacturing. With low productivity growth and stronger wage growth, real unit labour costs (RULC) increased by 2.1% year on year in the first three quarters of 2019 (in EMU by 1%). As in other euro area countries, RULC growth was more pronounced in more export-oriented sectors, particularly manufacturing. A more pronounced slowdown in productivity growth and, consequently, an increase in RULC in manufacturing activities is partly related to their greater integration in global value chains and already started with the cooling of activity in trading partners in 2018. In the first three quarters of 2019, the faster growth of wages than productivity (i.e. an increase in RULC) also gradually spread to the majority of service activities and construction.

Year-on-year price growth in Slovenia and in the euro area

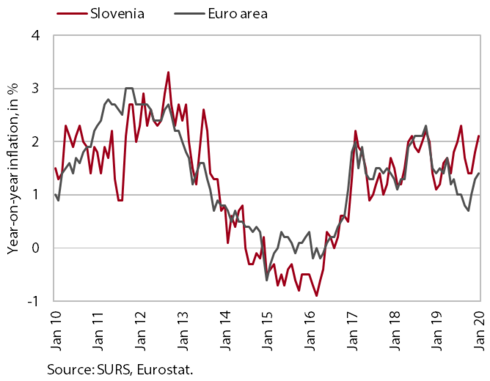

Consumer prices declined in January due to seasonal factors, while in year-on-year terms their growth strengthened to 2.1%. The greatest contribution to total year-on-year growth came from higher prices of goods, which was largely a consequence of higher food and energy prices. Food prices are rising due to growth in meat prices as a result of the outbreak of the African swine fever. The growth of fruit prices is also strengthening, reflecting last year’s worse harvest. Prices of semi-durable goods continue to rise moderately, while prices of durable goods remain down year on year. Growth in prices of services is gradually easing amid lower prices of holiday packages.

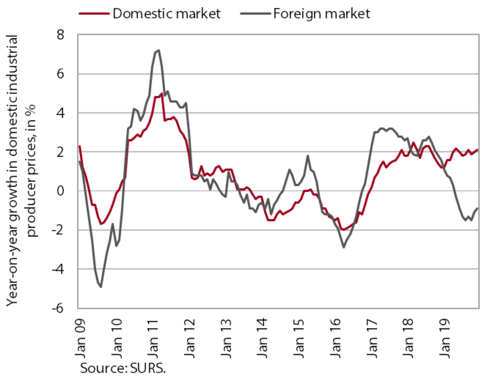

Year-on-year growth in Slovenian industrial producer prices on the domestic and foreign markets

Year-on-year growth in Slovenian industrial producer prices declined to 0.6% last year due to lower prices on foreign markets. With the moderation of foreign demand, prices on foreign markets were lower year on year in all industrial groups mainly due to lower prices of intermediate goods (by 0.9%), which account for almost half of the index value. Price growth on the domestic market strengthened somewhat, particularly due to strong growth in prices of energy (higher prices in electricity, gas and steam supply, where year-on-year growth is moving around 15%). Amid increased spending and higher meat prices, somewhat higher price growth was also recorded for non-durable consumer goods (2.3%).

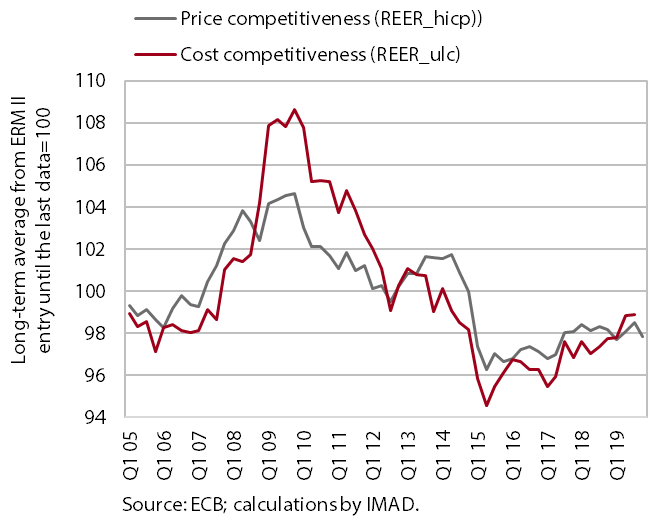

Price and cost competitiveness

Cost competitiveness is gradually deteriorating, while the indicator of price competitiveness has been stable in recent years, with occasional fluctuations. With faster growth in unit labour costs compared with trading partners, the indicator of cost competitiveness (REER_ulc) of the Slovenian economy deteriorated somewhat again in the third quarter of last year. The indicator of price competitiveness (REER_hicp) also deteriorated in the third quarter, but it improved again with a relative decline (relative to trading partners) in inflation towards the end of the year. The exchange rate of the euro against the basket of currencies of 37 more important trading partners (NEER) had no major impact on competitiveness in the last quarter. NEER and REER_hicp have been moving at similar levels since mid-2017, with fluctuations.

Components of the current account balance

In November, the current account surplus increased further and was higher year on year in the last twelve-month period (at 6.4% of estimated GDP). Amid faster real growth in exports than imports, this was mainly due to higher surpluses in goods and services. The net outflow of primary income declined further, mainly due to higher receipts from the EU budget for the implementation of the common agricultural and fisheries policy and lower net payments of interest on external debt. The deficit in secondary income was higher year on year, particularly due to higher payments into the EU budget (VAT-based and GNI-based contributions).

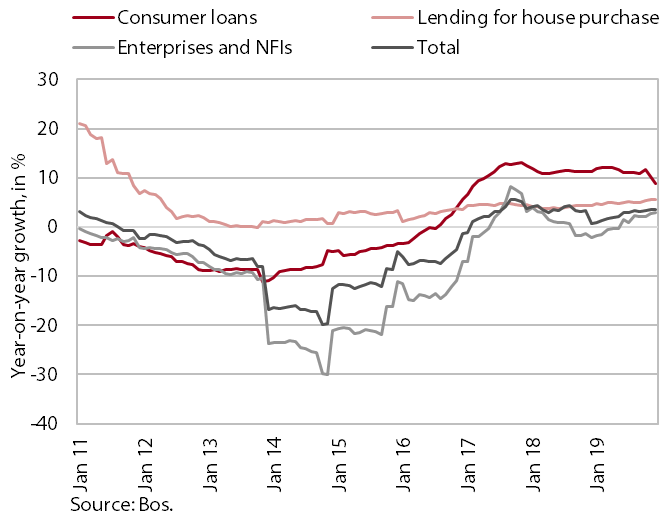

Year-on-year growth rates of loans in the Slovenian banking sector

In 2019, lending activity in the Slovenian banking system remained underpinned mainly by growth in deposits of domestic non-banking sectors. Year-on-year growth in loans to domestic non-banking sectors increased last year as a result of somewhat stronger growth in corporate and NFI loans, but remained modest. Total growth continued to be mainly driven by household loans, whose year-on-year growth was stable (around 6%). The structure of growth, however, changed somewhat with the introduction of a binding macroprudential instrument, as the contribution of consumer loans declined (growth fell by around 2 pps to 8.9% at the end of the year), while the contribution of housing loans increased by a similar extent. Growth in non-banking sector deposits continued mainly due to household deposits. Their growth strengthened further under favourable labour market conditions, while deposits of non-financial corporation declined, for the first time since 2012. Banks’ dependence on foreign sources of finance thus remained low.

Revenue, expenditure and balance of the consolidated general government budgetary accounts

Last year the consolidated balance of public finances was in surplus for the second consecutive year, but it was lower than in 2018, as expected. The lower surplus was mainly due to the absence of one-off revenues, which had significantly strengthened revenue growth one year earlier (high dividend payments and one-off receipts from the EU budget). The decline in revenue growth in 2019 was also a consequence of lower growth in tax revenues. Growth in revenue from personal income tax was lower owing to changes in the taxation of holiday allowance. Growth in revenue from VAT also moderated. Expenditure growth was only slightly higher last year than in 2018, except for investment expenditure, where growth was significantly more moderate, and interest payments, which dropped further. The bulk of expenditure growth derived from the adopted agreements on wage rises and employment growth in the public sector and measures in the area of transfers to individuals and households.

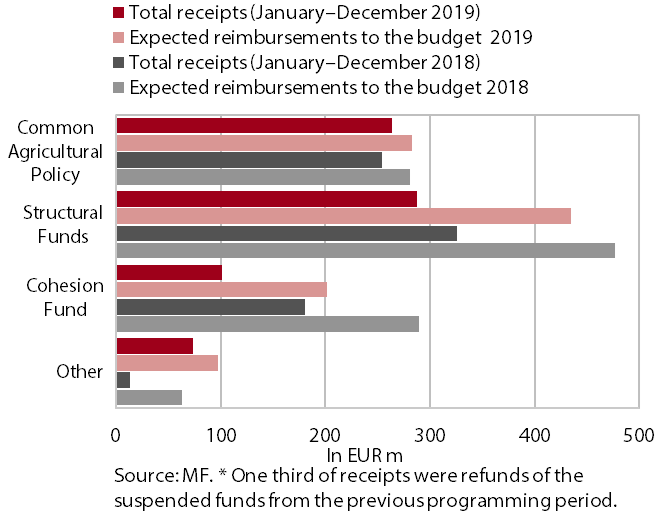

Receipts from the EU budget

Slovenia’s net budgetary position against the EU budget was positive in 2019 (at EUR 216.6 million). Last year, Slovenia paid EUR 509.7 million to the EU budget (102.8% of the amount planned for 2019) and received EUR 726.3 million from it (71.4% of planned revenue). The bulk were receipts from structural funds (40% of all or 66.2% of planned receipts). The deviation from the planned realisation was lowest in revenue under the Common Agricultural and Fisheries Policy (93.3%) and highest in revenue from the Cohesion Fund (50.1%). By the end of 2019, 36% of the amount allocated under the EU Cohesion Policy was paid from the state budget, according to SVRK data.