Slovenian Economic Mirror

Slovenian Economic Mirror 1/2025

Sentiment indicators for the euro area and Germany deteriorated in the fourth quarter of 2024. In Slovenia, activity in most sectors was higher year-on-year in the first ten to eleven months of 2024, and activity in construction continued to lag behind. Real exports of goods have stagnated since the slump in September, while manufacturing output rose slightly from mid-2024 onwards. In the first three quarters of 2024, the export market share for goods increased for the second year in a row. Real income in market services has fallen significantly since mid-2024, while its growth in trade accelerated in the second half of the year. Economic sentiment remained low at the end of the year, but was slightly above the previous year’s level. Developments on the labour market were subdued in the final months of 2024, with employment reaching a record high and unemployment remaining low. In the first 11 months, employment was 1.2% higher than in the same period of 2023, boosted by the employment of foreigners. With the exception of an increase due to a methodological change at the beginning of 2024, it has largely stagnated since the second half of 2023, but rose slightly in November 2024. At the end of 2024, 47,038 people were unemployed, representing a 2.7% decrease compared to December 2023. On average, unemployment in 2024 was 5.6% lower year-on-year. In October, year-on-year real growth in the average gross wage was higher than in previous months (6.8%), amid higher nominal growth (6.5%) and low (zero) inflation. The year-on-year inflation rate at the end of 2024 was 1.9%, less than half that of a year earlier (4.2%), with food and non-alcoholic beverage prices contributing around a quarter to inflation. The deficit of the consolidated balance of public finances was around EUR 0.5 billion lower in the first 11 months of 2024 than in the same period of 2023.

Composite Purchasing Managers’ Index (PMI) for the euro area, December 2024

Sentiment indicators for the euro area deteriorated in the fourth quarter of 2024. With both indicators that form the composite PMI declining, the average PMI value fell to 49.3 in the fourth quarter (down from 50.3 in the third). The services PMI signals a slowdown in growth in this segment, while the manufacturing PMI, which has been below 50 since July 2022 amid a sustained decline in new orders, indicates ongoing contraction. The Economic Sentiment Index (ESI) in the euro area fell sharply in December, with confidence in industry deteriorating markedly, and was also significantly lower year-on-year. In the fourth quarter, it was lower on average than in the third and similar to the level a year ago. The Ifo indicator, which measures the business climate in Germany, also declined quarter-on-quarter in the fourth quarter, with indicators for most activities declining, and was also lower year-on-year. According to the ECB’s December forecast, the euro area economy grew by 0.7% in 2024 and is projected to grow by 1.1% this year and 1.4% next year. The higher growth is expected to be supported primarily by private consumption as real income rises, although the forecasts are subject to significant geopolitical and economic uncertainties.

GDP growth forecasts for Germany, December 2024

In their latest forecasts, German institutions do not anticipate any significant recovery in German economic growth in 2025. After two years of contraction (-0.3% in 2023; around -0.2% in 2024 according to institutions’ estimates), GDP growth in Germany is expected to be modest in 2025 (with forecasts ranging between 0% and 0.5%) and around 1% in 2026. These forecasts have been revised significantly downwards from the previous projections, mainly due to the weak industrial sector, which is grappling not only with cyclically low demand but also with structural problems. As a result, the forecasts for exports and corporate investment in 2025 have been significantly downgraded. Growth prospects for private consumption have also been revised significantly downwards, reflecting weaker labour market conditions amid high uncertainty. As inflation is expected to continue to ease, households’ real incomes should keep rising, which, together with a lower savings rate, will enable further, albeit modest, growth in private consumption. The projected easing of monetary policy and the resulting lower financing costs are expected to stimulate a recovery in investment in the coming year, and exports are also likely to improve, driven by stronger foreign demand. The main risks to the outlook are growing protectionism, geopolitical conflicts, and uncertainties about the impact of structural change and future financial and economic policy directions following the German elections.

Commodity prices, December 2024

The average dollar prices of Brent crude oil fell slightly in December, while prices of non-energy commodities increased. In December, the average dollar price of Brent crude oil fell by 0.7% month-on-month to USD 73.86, while a weaker euro meant that the euro price increased slightly (by 0.8% to EUR 70.49). Year-on-year, the dollar price of Brent crude oil decreased by 5% and the euro price by 1.1%. In 2024, the oil price in dollars or euros was on average around 2.5% lower than in 2023. Given the lower gas storage filling levels, euro prices of natural gas on the European market (Dutch TTF) continued to rise in December (by 1.2%). The euro price was 25.5% higher year-on-year in December, while the average prices in 2024 were 16.4% lower. According to the World Bank, the average dollar price of non-energy commodities rose by 1.9% month-on-month in December and by 7.9% year-on-year. In particular, prices of agricultural raw materials for beverages have risen (by 18.4% month-on-month and by 66.6% year-on-year) in the face of strong price increases for cocoa and coffee. In 2024, dollar prices of non-energy commodities were 1.9% higher than in 2023.

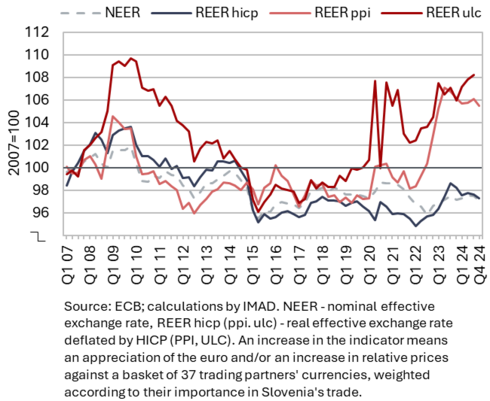

Effective exchange rates, Q4 2024

The improvement in price competitiveness indicators of the Slovenian economy continued in the fourth quarter of 2024, with cost pressures remaining high throughout the year; signs of easing emerged in mid-2024, primarily in manufacturing. Both price competitiveness indicators (REER hicp and ppi) have gradually improved since the energy shock, i.e. mid-2023, with relative prices (in Slovenia compared to its trading partners) decreasing. However, the cost competitiveness indicator (REER ulc) deteriorated again in the first three quarters of 2024 after a short period of improvement under the influence of the increase in relative (nominal) unit labour costs (ULC). During this period, ULC growth in construction accelerated sharply, driven by a decline in construction activity and thus productivity, while labour costs continued to rise. In manufacturing, the most export-oriented part of the economy, ULC growth slowed significantly in mid-2024 (amid a cyclical recovery in productivity).

Since the end of 2023, real unit labour costs (RULC) – which are the mirror image of unit profits – have risen alongside the growth in nominal labour costs. This shows that companies – unlike during the energy crisis, when the high cost increases were largely passed on to prices – are absorbing the cost increases through reduced profits instead of passing them on to prices in order to maintain their price competitiveness. RULC growth is also strongest in construction, while it slowed significantly in manufacturing in mid-2024.

Short-term indicators of economic activity in Slovenia, October−November 2024

In Slovenia, activity in most sectors was higher year-on-year in the first ten to eleven months of 2024. Real exports of goods, which have stagnated since the slump in September, and manufacturing production, which has increased slightly since mid-2024, exceeded their previous year’s levels by 3.5% and 1.2% respectively in the first 11 months. Real turnover in trade, where growth increased month-on-month in the second half of the year, was up 2.7% year-on-year in the first ten months. The largest year-on-year increase was recorded in the sales of motor vehicles, where turnover recovered steadily in October following a decline in the first half of the year. Year-on-year growth in the other trade sectors was much more modest. Following a sharp contraction in mid-2024, the decline in turnover in market services deepened again in the last two months. In the first ten months of 2024, turnover was 1.6% higher year-on-year. Only transportation and storage and professional and technical activities recorded lower real income than a year ago, with both declining month-on-month in October. Construction activity increased significantly in November 2024 after gradually declining in previous months but was still lower year-on-year.

Value of fiscally verified invoices – nominal, December 2024

In December 2024, the nominal value of fiscally verified invoices increased by 2% year-on-year for the third month in a row. In the fourth quarter of last year, the nominal growth halved compared to the third quarter. Total growth in trade in December was similar to November, when it had halved (1%). In retail trade, which accounted for half of the total value of fiscally verified invoices, the value in December 2024 was similar to December 2023, after having increased year-on-year in the previous two months. Slightly higher year-on-year growth compared to November was recorded in the sales of motor vehicles (4%). In wholesale trade, the nominal value was similar to December 2023, following a year-on-year decline from May to November. In tourism-related services, growth in the nominal value of fiscally verified invoices, which had doubled in November, remained high (6%).

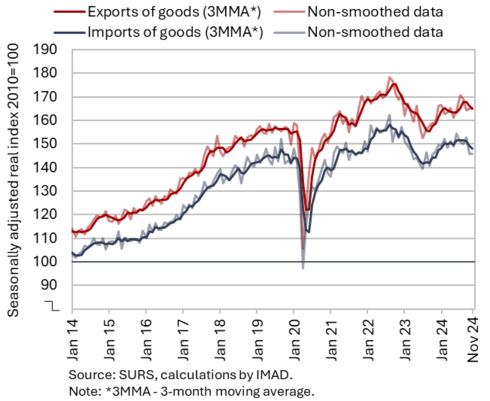

Trade in goods – in real terms, November 2024

In November 2024, exports and imports of goods were lower month-on-month compared to the average for the third quarter (seasonally adjusted); both exports and imports were higher in the first 11 months of 2024 than during the same period in 2023. After a significant decline in September, real exports of goods remained largely unchanged in October and November, but below the third-quarter average. The strongest month-on-month increase in exports in November was recorded in vehicles and equipment, which usually exhibit significant fluctuations. Exports of chemical products, including pharmaceuticals, also increased, while exports of metals and metal products and of machinery and equipment declined. Real imports of goods remained unchanged month-on-month in November, while imports of intermediate goods further declined and imports of consumer goods increased (seasonally adjusted).

In the first 11 months of 2024, both exports and imports of goods increased by 3.5% year-on-year. In a year-on-year comparison, growth in imports and exports was also primarily driven by trade in vehicles, pharmaceuticals and certain chemical products. Sentiment in export-oriented activities slightly deteriorated in December, and despite a modest improvement, export orders remained at a very low level.

Slovenia’s export market share in the EU market, Q3 2024

Slovenia’s export market share in the EU market increased year-on-year in the third quarter, reaching a level comparable to that seen before the epidemic and energy crisis. Amid strong year-on-year nominal growth in the euro value of Slovenian exports of goods to the EU (6.5%) and stagnation in EU goods imports, Slovenia’s share in the EU market rose by 5.8% year-on-year in the third quarter of 2024 and by 5.6% in the first three quarters combined (to around 0.49%). Notably, the growth in market share for certain energy-intensive products (such as chemical products and metals) continued in the third quarter and significantly outpaced the year-on-year growth in market share for some of Slovenia’s key export industries (pharmaceuticals, motor vehicles). Among Slovenia’s key trading partners, the largest year-on-year increase in Slovenia’s market share was recorded in Croatia (rising by 12.4% to 11.82%). Market share also grew in France and Germany, it declined in Austria and Italy. A product-specific and geographical decomposition of market share growth shows that the year-on-year increase was mainly driven by increased competition in the EU market, while the export structure did not differ significantly from the EU demand structure and therefore did not have a significant impact this time.

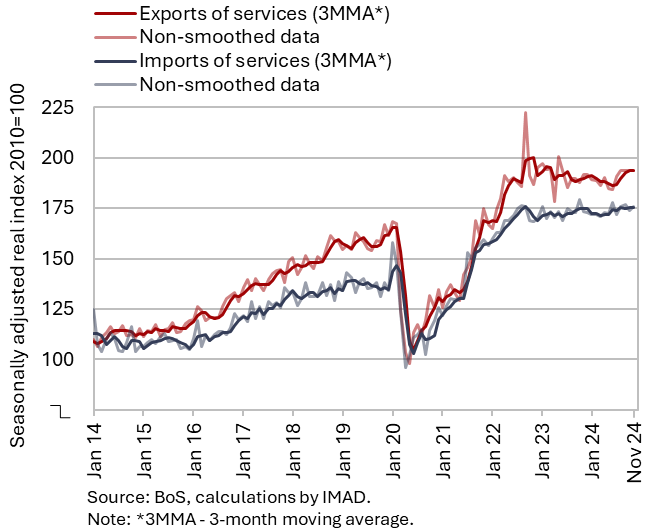

Trade in services – in real terms, November 2024

Real exports of services remained largely unchanged month-on-month in November and were slightly lower year-on-year, while real imports increased both month-on-month and year-on-year. Exports of transport services and tourism-related services have fallen slightly in recent months and were below the average for the third quarter in November. Exports of other business services, which fluctuate significantly on a monthly basis, also fell. After several months of decline, exports of construction services rose sharply, and exports of ICT services also increased. Imports of most main groups of services increased compared to the previous month, with only imports of transport services declining slightly (seasonally adjusted). In the first 11 months of 2024, real exports of services declined year-on-year (-0.5%), although the decline has slowed in recent months. Exports of construction services in particular were significantly lower than in the same period last year, and exports of transport and tourism-related services also fell. On the other hand, real imports of services remained higher than a year ago (rising by 0.4%) in this period.

Production volume in manufacturing, November 2024

Production volume growth in manufacturing increased in the second half of 2024; it was higher year-on-year in the first 11 months. Since mid-2024, production in low- and medium-high-technology industries has remained largely unchanged, while it has predominantly increased in the high- and medium-low-technology industries during this period (seasonally adjusted). In the first 11 months of 2024, manufacturing production was up year-on-year (by 1.2%, working-day adjusted). Production in most energy-intensive industries (with the exception of manufacture of non-metallic mineral products) and activity in the manufacture of electrical equipment were significantly higher than a year earlier, driven by a low base effect. In other medium-high-technology industries, production declined year-on-year – the manufacture of machinery and equipment n.e.c. saw a decrease following growth in previous years, while from mid-2024, production in the manufacture of motor vehicles and other transport equipment, which had largely been contracting over the last five years, also declined. Production in most low-technology industries was also down year-on-year.

Activity in construction, November 2024

Construction activity strengthened month-on-month in November but remained lower year-on-year. After declining gradually until autumn 2024, construction activity increased by 10% in November. In November 2024, the value of construction put in place was 4% lower year-on-year. For the first 11 months combined it declined by 10%. In this comparison, the most significant declines were seen in civil engineering (down 14%) and construction of buildings (down 13%), while specialised construction activities saw the smallest decline (down 4%).

This lower activity was (among other things) related to government investment activity. Capital expenditure (according to the consolidated general government budgetary accounts) fell by 7% year-on-year in the first 11 months of 2024, and expenditure on new construction, reconstruction and renovation, which we consider to be most closely linked to construction activity, was 24% lower.

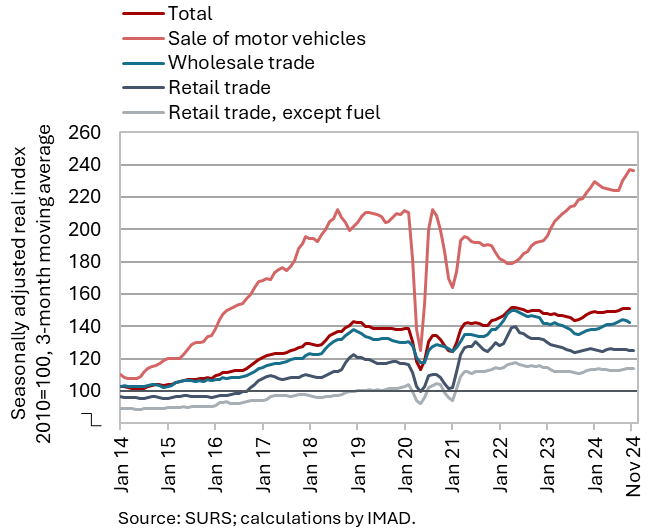

Turnover in trade, October–November 2024

In October 2024, real income continued to rise in some trade sectors while declining in others (seasonally adjusted); year-on-year, it increased across all sectors. Turnover in the sales of motor vehicles continued to rise following a decline in the first half of the year. Similarly, turnover in retail sales of food, beverages and tobacco increased further after stagnating during the first half of the year. In contrast, turnover in retail sales of non-food products decreased slightly. After strong growth in mid-summer, turnover also declined in wholesale trade for the third consecutive month. In the first ten months, turnover in all trade sectors was higher than in the same period of 2023. The highest real growth was recorded in the sales of motor vehicles (8%). It was 2% in wholesale trade and retail sales of food and beverages and 1% in retail sales of non-food products. According to preliminary data from SURS, turnover in retail sales of food rose month-on-month in November, turnover in retail sales of non-food products remained unchanged from the previous month and turnover in the sales of motor vehicles declined.

Turnover in market services, October 2024

Total real turnover in market services continued to decline in October 2024 (by 1.6%, seasonally adjusted), while it was higher year-on-year (by 1.6%). The decline was most pronounced in information and communication, which is attributable to lower sales in both main service groups (computer and telecommunications). Turnover also decreased again in professional and technical activities, this time mainly due to lower turnover in architectural and engineering services. It also decreased slightly in transportation and storage, albeit with an increase in land transport. Turnover in accommodation and food service activities increased significantly again as the number of overnight stays continued to rise. Turnover also increased in administrative and support service activities, breaking the negative trend in employment services, while the favourable trend in travel agencies continued for the third month in a row. In the first ten months of 2024, real turnover decreased year-on-year only in transportation and storage and professional and technical activities.

Road and rail freight transport, Q3 2024

The volume of road and rail freight transport decreased slightly in the third quarter of 2024 (seasonally adjusted). The total volume of road transport by Slovenian vehicles decreased in road traffic performed at least partially on Slovenian territory (exports, imports and national transport), while the growth in cross-trade transport came to a halt. The share of cross-trade in total transport increased to about 49% – a level comparable to pre-COVID-19 figures. The volume of road goods transport fell by 1% year-on-year and by 16% compared to the third quarter of 2019. After experiencing growth in the second quarter of 2024, rail freight transport declined slightly in the third quarter. It remained higher year-on-year (by 3%) but was similarly lower compared to the same quarter of 2019 as road transport.

Selected indicators of household consumption, October–December 2024

The available data indicate that household consumption increased year-on-year in the fourth quarter of 2024. The number of new passenger cars sold to natural persons was 13% higher year-on-year in October and turnover from the sales of motor vehicles rose by an average of 7% in real terms in October and November. During the same period, spending on food, beverages and tobacco also rose year-on-year (by 4% in real terms), while spending on non-food products remained similar to the average for October–November 2023. Spending on tourism services in Slovenia and abroad was also higher year-on-year. Year-on-year growth in household consumption is evident in the year-on-year increase in the nominal value of fiscally verified invoices (used as a proxy for sales), amounting to 2% in the fourth quarter of 2024.

Real estate, Q3 2024

Amid a further decline in the volume of sales, year-on-year growth in dwelling prices remained relatively strong in the third quarter of 2024. After price growth halved in 2023 (to 7.2% on average), prices increased by 7.9% compared to the third quarter of 2023 and by 1.7% compared to the second quarter of 2024. Prices of existing dwellings, where the number of transactions has declined significantly in the last two years (by 28.1% year-on-year and by 57.9% compared to the mid-2021 peak) were 8.4% higher year-on-year. Prices of newly built dwellings were 6.7% higher year-on-year. The number of transactions in this segment, which represents only a small part of total sales (5%), fell sharply year-on-year (by more than one-third), after being relatively high in 2023 (almost 50% higher than in 2022 and at the highest level since 2018).

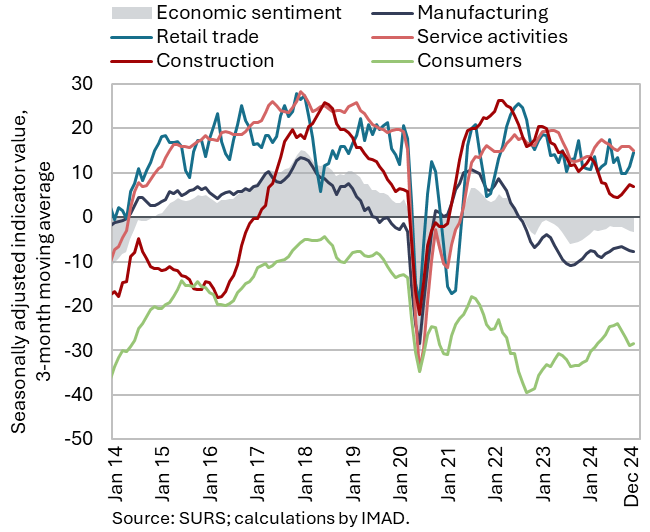

Economic sentiment, December 2024

Following a deterioration in October, economic sentiment remained at a similarly low level until the end of 2024. The economic climate indicator was slightly higher in December than a year earlier but remains below its long-term average. Confidence was higher than a year earlier, particularly in trade and among consumers, both of which also improved slightly at the end of the year, as well as in services. Confidence in manufacturing remained at a low level in December, similar to December 2023. Confidence remained below the previous year’s level in construction, where after an upward trend, it deteriorated significantly towards the end of the year.

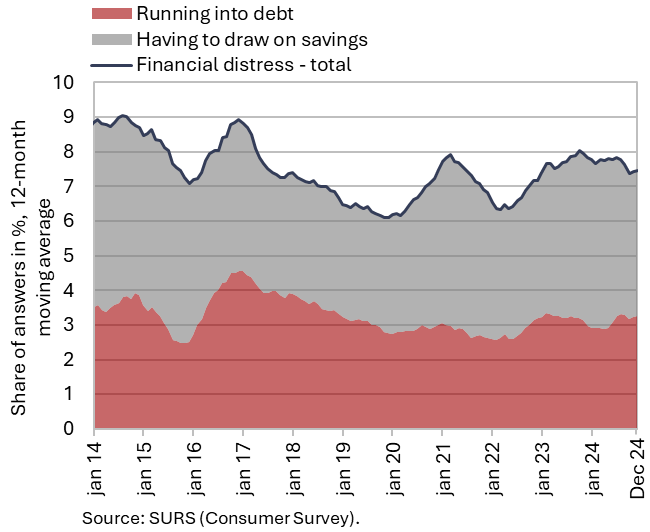

Households facing financial distress, December 2024

The financial situation of households improved slightly over the fourth quarter of 2024, both quarter-on-quarter and year-on-year. The share of households facing financial distress and having to draw on savings to meet their needs and the share of households running into debt deceased slightly year-on-year. According to our estimate, this year-on-year improvement was partly due to positive developments in the labour market (higher employment and wages). Compared to the previous quarter, only the share of households facing financial distress in the lowest income quartile decreased (by 0.5 p.p. to 13.9%), although their financial situation remained largely unchanged year-on-year. The most significant improvement in the financial situation of households was observed among those in the second income quartile (by 2.3 p.p. quarter-on-quarter to 7.9%).

Number of persons in employment, November 2024

The number of persons in employment increased slightly in November 2024 (seasonally adjusted). Their number has shown little variation since mid-2023 (except for the impact of a methodological change at the beginning of 2024), with developments varying across activities. In November, growth in the number of persons in employment continued in the public services, most markedly in human health and social work activities. In construction, the number of persons in employment stagnated year-on-year against a backdrop of lower activity and a persistent shortage of skilled labour. The number is also stagnating in market services, while it is gradually declining in manufacturing (all seasonally adjusted). Year-on-year growth in the overall number of persons in employment in November (1.1%) was consistent with the growth observed in previous months. In the first 11 months of 2024, their number was 1.2% higher year-on-year. Among those in employment, the number of foreign workers continues to rise, whereas the number of Slovenian workers is declining, albeit very slowly, due to retirement. In November, the share of foreign citizens among all persons in employment was 15.9%, 1.2 p.p. higher than a year earlier. The activities with the largest shares of foreigners are construction (50%), transportation and storage (34%), and administrative and support service activities (29%).

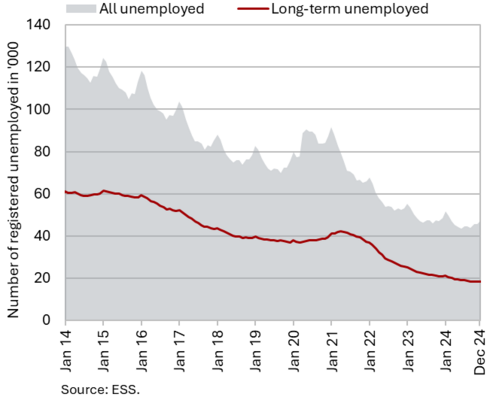

Number of registered unemployed, December 2024

In December 2024, the number of unemployed persons (seasonally adjusted) fell slightly. According to original data, 47,038 people were unemployed at the end of December, 2.9% more than at the end of November. This largely reflects seasonal trends related to a higher inflow into unemployment due to expiry of fixed-term employment contracts. Year-on-year, the number of unemployed was 2.7% lower in December, marking a smaller decrease compared to previous months. This is mainly due to a year-on-year increase in the inflow of unemployed persons attributed to redundancies and bankruptcies. Amid ongoing labour shortages and the retirement of older unemployed, the numbers of long-term unemployed (those unemployed for more than one year) and of unemployed over 55 fell year-on-year at the end of December, by 12.5% and 10.3% respectively. In contrast, the number of unemployed young people (aged 15–29) was slightly higher year-on-year for the third month in a row. In 2024, on average 45,982 persons were registered as unemployed, 5.6% fewer than a year earlier.

Average real gross wage per employee, October 2024

In October, year-on-year real growth in the average gross wage was higher than in previous months (6.8%), which was due to both higher nominal wage growth and low (zero) inflation. In the public sector, wage growth (4.7%) was primarily driven by an increase in the value of the pay scale grades following a partial wage adjustment for inflation in June. In the private sector, where wage growth (7.9%) outpaced that of the public sector, labour shortages continued to play a key role in driving wage increases. In the first ten months, overall average gross wage increased by 6.5% year-on-year in nominal terms – by 7.6% in the public sector and by 4.4% in the private sector. This increase was lower than that observed in the same period last year, when higher inflation led to a higher wage adjustment.

Number of FSA beneficiaries and UB recipients, November 2024

In November 2024, the number of financial social assistance (FSA) beneficiaries fell year-on-year, while the number of unemployment benefit (UB) recipients increased slightly. Amid high employment and a fall in the number of long-term unemployed, who are often eligible for FSA, the number of FSA beneficiaries continued to fall year-on-year, reaching levels among the lowest in the past decade. In November, 70,347 people were entitled to FSA (original data), which is 3.4% less than in November 2023. The number of UB recipients was 14,007 in November (original figure), up by 2.4% year-on-year. This was due to a slightly higher inflow of persons who are eligible for UB into unemployment. 30.6% of all unemployed people received unemployment benefits in November, which is more than a year ago (29%).

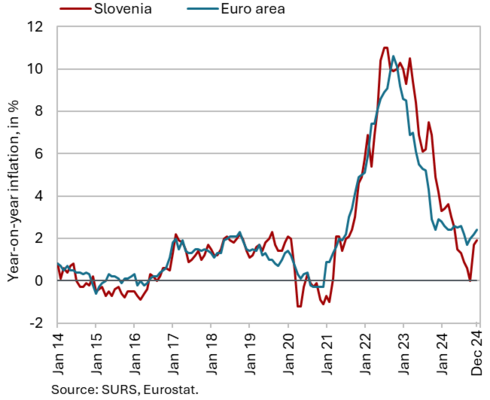

Consumer prices, December 2024

Although prices fell month-on-month, annual inflation edged up slightly in December (to 1.9%), but it was less than half the rate recorded at the end of 2023 (4.2%). The increase in year-on-year inflation was primarily attributed to a lower base effect, driven by a decline in petroleum product prices at the end of 2023, with prices in the food and non-alcoholic beverages group rising again in December 2024 (by 0.5%). Year-on-year, prices in this category were 2.6% higher, contributing roughly a quarter to total year-on-year inflation and marking the highest contribution among the 12 groups of goods and services in the CPI basket. Energy prices rose by 0.5% in 2024. With a slightly more pronounced price drop in the clothing and footwear group, the year-on-year price increase for semi-durable goods slowed at the end of 2024 (to 2.0% from 3.0% in November). The year-on-year price decline for durable goods remained steady at around 1% throughout most of 2024. After declining during the year, the year-on-year growth in services prices in December (2.7%) was similar to that recorded in November. Higher prices in the restaurants and hotels group (up by 4.1%) accounted for roughly one-third of the overall growth.

Slovenian industrial producer prices, November 2024

In November, Slovenian industrial producer prices rose by 0.5% month-on-month, while the year-on-year decline eased to -0.4% (compared to -1.3% in October). The year-on-year decline in prices was still primarily driven by a 1.2% decline in the intermediate goods group, although the pace of this decline has been gradually slowing. Prices of capital goods also saw a year-on-year decline (of 0.7%). Energy prices, which were nearly 15% lower year-on-year in October, rose by 1% in November, primarily due to a sharp monthly rise (of 12.7%). Prices of electricity, gas, steam and air- conditioning supply rose by more than a tenth month-on-month but were still 2.1% lower year-on-year. Prices of coke and refined petroleum products increased by almost a fifth compared to October (by 9.6% year-on-year). The year-on-year growth of consumer goods prices remains steady at approximately 1%. Prices on the domestic market fell by 0.9% year-on-year in November, and prices on foreign markets also recorded a slight decline (-0.1%).

Loans to domestic non-banking sectors, November 2024

Growth in the volume of loans to domestic non-banking sectors increased slightly in November (to 5.3%). The main contribution to growth (3.1 p.p.) was the around 70% increase in NFI loans, rising by almost 60% month-on-month in September. After falling month-on-month since May, the volume of loans to non-financial corporations rose in November (by 0.4%), while the year-on-year decline slowed by more than one percentage point (to 3.2%) compared to October. Loans to households rose by 6.1% year-on-year; their year-on-year growth has remained roughly at the level achieved in the second half of the year, with year-on-year growth in consumer loans slowing (14.4%) and housing loans gradually increasing (3.7%). Deposit growth in the domestic non-bank sector was the lowest since 2016 (1.5%). Overnight deposits (2%), which account for around 80% of total non-banking sector deposits, have been on the rise again since September. In November, short-term deposits were lower year-on-year (by 1%) for the first time since August 2022. Long-term deposit growth also fell sharply over the year (to 10%, down from 50% in January). The quality of banks’ assets remains solid, with the share of non-performing loans holding steady at 1% for more than a year and a half.

Government bond, Q4 2024

Yields to maturity of euro area government bonds further decreased slightly in the fourth quarter of 2024. This was still mainly due to the ECB’s monetary policy, which lowered its key interest rates twice in the fourth quarter – by a total of 50 basis points – as inflationary pressure eased. Quarter-on-quarter, the yield to maturity of the Slovenian government bond decreased by 9 basis points, reaching 2.98%. The spread to the German bond narrowed by 5 basis points, decreasing to 72 basis points.

Current account of the balance of payments, November 2024

The current account surplus amounted to EUR 3.3 billion in the first 11 months of 2024 and was 0.5 billion higher than in the same period of 2023. The main reason for the year-on-year change in the current account balance was the goods trade balance, with exports rising more sharply than imports. The surplus in trade in services further increased slightly, especially in trade in technical, trade-related services, but partly also in certain knowledge-based services (telecommunications, computer and information services, financial services, and R&D services). The deficits in the primary and secondary income balances have narrowed. The former decreased due to lower net payments of taxes on production and imports and higher net interest income from financial investments in securities and from deposits in foreign accounts. The lower secondary income deficit was mainly due to lower GNI- and VAT-based contributions to the EU budget.

Revenue (top figure) and expenditure (bottom figure) of the consolidated general government budgetary accounts, November 2024

The deficit of the consolidated general government budgetary accounts amounted to EUR 485.6 million in the first 11 months of 2024 and was 595.5 million lower than in the same period of 2023. Revenues in the first 11 months were 10.8% higher year-on-year. This growth was driven not only by revenue from social contributions, following the transformation of the complementary health contribution into a mandatory contribution, but also mainly by corporate income tax revenues, resulting from higher balancing payments last year and a higher tax rate and non-tax revenue (profit sharing of SSH and property income). Income tax receipts also contributed notably to the growth in general government revenue. The contribution from consumption-related taxes was lower year-on-year. Total receipts from the EU budget were lower year-on-year. Expenditure in the first 11 months was 7.8% higher year-on-year. The main contributors to growth were transfers to individuals and households, mainly due to the effect of high regular annual adjustment of pensions, and allocations to the budget funds (mainly the Fund for the Reconstruction of Slovenia and the RRP Fund). Expenditure on goods and services (among others ongoing maintenance on watercourses under the emergency Flood Recovery Act) and expenditure on salaries, wages and other personnel expenditure also made a significant contribution to growth in general government expenditure. Investment expenditure was significantly lower year-on-year. According to preliminary data from the Ministry of Finance, the state budget deficit, which constitutes the largest part of the consolidated balance sheet, increased in December. This was primarily due to the allocation of funds to the Fund for the Reconstruction of Slovenia to finance flood recovery measures in the coming years and higher investment expenditure. However, the deficit was lower than estimated during the adoption of the 2025 and 2026 budgets and was the lowest in the last five years (EUR 800 million, i.e. 1.2% of the projected GDP).

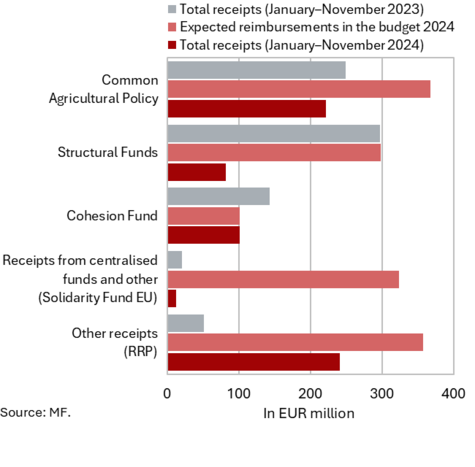

EU budget receipts, November 2024 (top figure) and absorption of funds under the Cohesion policy programme 2021–2027 (EU part) for the period 1 January 2021–30 November 2024 (bottom figure)

Slovenia’s net budgetary position against the EU budget was positive in the first 11 months of 2024 (at EUR 87.2 million). In this period, Slovenia received EUR 659.2 million from the EU budget (45.6% of receipts envisaged in the adopted state budget for 2024) and paid EUR 572.2 million into it (79.6% of planned payments). The bulk of receipts (36.6% of all reimbursements to the state budget, 67.5% of the planned reimbursements in 2024) were other receipts from the EU budget related to the payment of the third payment request from the Recovery and Resilience Facility and appropriations for the implementation of the Common Agricultural and Fisheries Policies (33.6% of all reimbursements to the state budget, 60.3% of the planned reimbursements in 2024). Resources from the Cohesion Fund accounted for 15.4% of total reimbursements to the state budget (100.4% of the planned reimbursements in 2024) and resources from the Structural Funds for 12.4% of all reimbursements (27.4% of the planned reimbursements in 2024). The highest payments into the EU budget came from GNI-based payments (49.5 % of all payments).

According to the MKRR data, under the Operational Programme for the Implementation of EU Cohesion Policy 2021–2027, payments from the state budget totalled EUR 57.9 million (EU share) up to the end of November 2024, representing 2% of the available funds.