Slovenian Economic Mirror

Slovenian Economic Mirror 1/2022

In Slovenia, most economic indicators suggest that the relatively favourable trends in the export-oriented part of the economy and in domestic consumption continued in the last quarter of last year; the worsening of the epidemic situation has had a particular impact on confidence indicators in service activities. Due to the low base in 2020, activity in most sectors was significantly higher year-on-year at the beginning of the last quarter and was above pre-epidemic levels. Tourism-related activities and construction in particular still lag well behind these levels. Uncertainty related to the deterioration in the epidemiological situation affected overall confidence in the economy, especially at the beginning of the last quarter, and in the services sector until the end of the year. Labour market conditions remain favourable; employment is at historically high levels and unemployment continues to decline. Inflation increased further in December, mainly due to year-on-year higher energy prices. As a result of high commodity and energy prices on world markets and supply chain problems, prices for non-energy durable and non-durable industrial goods and food also increased.

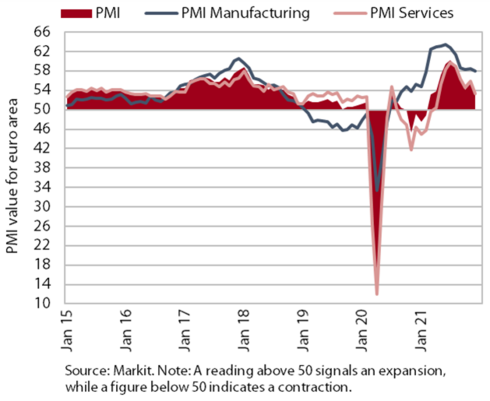

The euro area composite Purchasing Managers’ Index (PMI)

After a strong increase in the previous two quarters, growth of economic activity in the euro area slowed in the final quarter last year, according to available indicators. This is also indicated by the average quarterly value of the composite PMI, which fell significantly compared to the third quarter. With the worsening epidemic situation, economic growth in the services sector is slowing and ongoing supply chain disruptions are hampering the manufacturing sector, especially the automotive industry. The economy is also affected by high commodity and energy prices and a lack of skilled labour. This is also having a significant impact on rising inflation in the euro area, which stood at 5% in December. In its December forecast, the ECB estimates that economic growth in the euro area was 5.1% last year and predicts relatively strong growth in 2022 and 2023 (4.2 and 2.9% respectively), despite various current constraints. According to the ECB, economic activity will pick up from mid-2022 onwards, as supply chain disruptions and containment measures are expected to ease, the associated uncertainty to decrease and inflation to fall. The main driver of growth will continue to be private consumption, supported by the strengthening of real disposable income, the accumulated savings and the favourable development of the labour market.

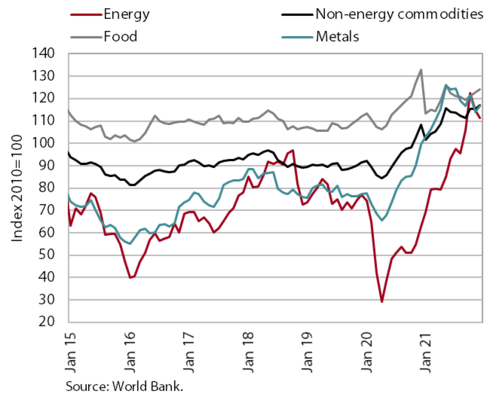

Commodity prices

The average price of energy products on international markets remained significantly higher year-on-year in December (by 77%). The average dollar price of Brent Crude decreased by 8.4% to USD 74.3 per barrel (it was 48.6% higher year-on-year), mainly due to the spread of the new COVID-19 variant. In December, natural gas prices on the European market increased by 38% compared to the previous month and by as much as 549% year-on-year. As a result, the price of electricity on the European market rose significantly in December, as its price is largely determined by gas-fired power plants. Based on futures prices on the wholesale markets, gas and electricity prices are expected to fall after the end of the winter. According to the World Bank, prices of non-energy commodities increased slightly in December from the previous month and remained 8% higher year-on-year. The strongest month-on-month price increase was recorded for metals and minerals, while year-on-year, fertiliser prices rose particularly sharply (by 164%). After rising 34% last year, non-energy commodity prices are expected to rise about 6% this year and fall again in 2023, according to the December ECB forecast.

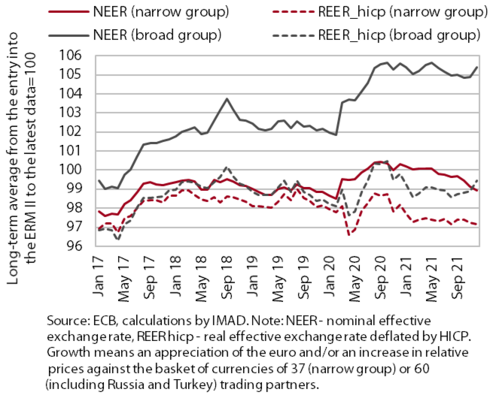

Nominal and real effective exchange rates

The value of the euro against a basket of currencies is approaching the levels seen before the outbreak of COVID-19. In the last months of 2021, the euro depreciated further against most of the currencies of Slovenia’s main trading partners, mostly approaching the levels before the outbreak of the COVID-19 pandemic and already below the February 2020 level against the Chinese yuan and the Swiss franc. On the other hand, the euro to Turkish lira exchange rate is 133% higher than the pre-epidemic value, and a strong depreciation of the Turkish lira was also recorded in December 2021. This has led to growth, i.e. a deterioration in the nominal (NEER) and consequently the real (REER hicp) effective exchange rate. However, the price competitiveness indicator (REER hicp) for a narrow group of countries, which does not include Turkey, remains stable. Growth in final prices (measured by inflation or the HICP) in Slovenia was somewhat higher than the average growth in Slovenia’s 37 trading partners, but these negative effects on price competitiveness were mitigated by the depreciation of the euro.

Short-term indicators of economic activity in Slovenia

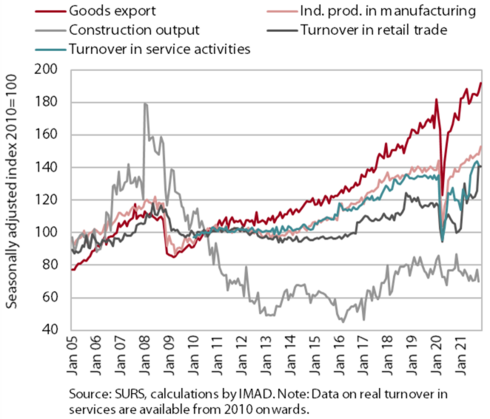

In Slovenia, most economic indicators suggest that the relatively favourable trends in the export-oriented part of the economy and in domestic consumption continued in the last quarter of last year. Manufacturing production increased significantly in November after stagnating in October. After several months of marked monthly fluctuations, foreign trade in goods also increased in October and November. The relatively favourable trend in trade and tourism-related activities continued in October, and according to data on fiscal certification of invoices, turnover in December was also slightly higher than in the same periods of 2019 and 2020. Activity in construction, which has fluctuated widely across segments in recent months, fell sharply in October. After several months of growth, turnover in market services declined from the previous month, especially in professional and technical activities, and growth in foreign trade in services also came to a halt. Due to the low base in 2020, activity in most sectors was significantly higher year-on-year at the beginning of the last quarter and was above pre-epidemic levels. Tourism-related activities and construction in particular still lag well behind these levels. Uncertainty related to the deterioration in the epidemiological situation affected overall confidence in the economy, especially at the beginning of the last quarter, and in the services sector until the end of the year.

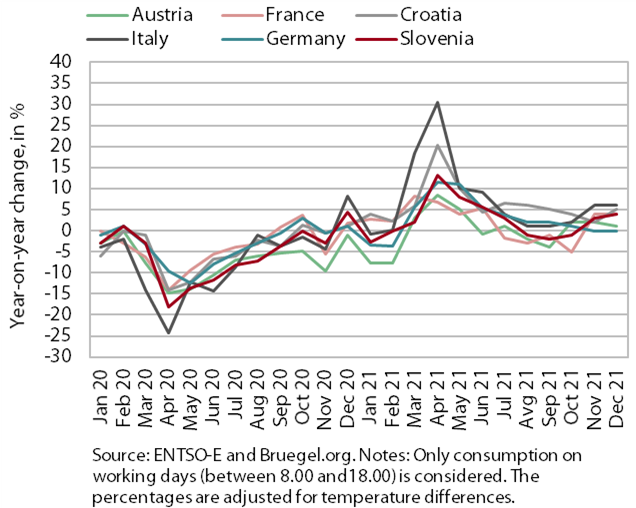

Electricity consumption

Electricity consumption in December was about 4% higher than in December 2019 and 2020. The growth in consumption is mainly due to the low base in December 2020 related to the strict containment measures and the less favourable timing of holidays in terms of the functioning of the economy in December 2019. Among Slovenia’s main trading partners, France (4%), Croatia (5%) and Italy (6%) recorded higher consumption than in December 2020. Consumption in Austria and Germany remained about the same as in December 2020, which was related to the imposition of a new full national lockdown in Austria and the lockdown in some federal states in Germany. Compared to December 2019, consumption was higher by 6% in France and Croatia, by 8% in Italy, and by 2% in Germany, while consumption in Austria remained about the same.

Traffic of electronically tolled vehicles on Slovenian motorways

In December 2021, freight traffic volumes on Slovenian motorways increased by 12% year-on-year. The high year-on-year increase is due to the lower traffic volumes in the second wave of the epidemic in 2020 and the fact that December 2021 had one more working day. Freight traffic volumes were also significantly higher than in December 2019, but after adjusting the data to take into account working days (there were three more working days in 2021), they were about 3% lower. Overall, traffic volumes in 2021 were 14% higher than in 2020 and 1% higher than in 2019 (adjusted for working days). The share of foreign vehicle traffic, which had fallen slightly in 2020, returned close to the pre-epidemic level of 60%.

Turnover based on fiscal verification of invoices

According to data on the fiscal verification of invoices, turnover in December was 36% higher year-on-year and 2% higher than in the same period of 2019. Year-on-year growth was lower than in November, mainly due to a higher base resulting from temporary partial relaxation of operating restrictions between 15 and 23 December 2020. This was mainly reflected in lower year-on-year turnover growth in trade and some personal services. However, year-on-year growth was still very high for activities that were almost completely shut down in December 2020 – mainly tourism-related services. Total turnover was 2% higher than in December 2019, with three more working days in December 2021. This was due to 6% higher turnover in trade (higher turnover in retail and wholesale trade, while turnover in the sale of motor vehicles was lower). After an increase in the summer months, the decline in the accommodation and food sector activities intensified (to 26%), while the gap with pre-crisis levels remained very high in creative, arts and entertainment activities, in gambling and betting, and for travel agencies.

Slovenia’s export market share on the EU market

Slovenia’s export market share in the EU market fell significantly in the third quarter of 2021. According to initial estimates, it was 2.8% lower year-on-year and also lower than before the epidemic. The unfavourable trend in international trade of road vehicles, which account for the largest share of Slovenian goods exports (16.7% in the EU market in 2020), continued. Previously growing market shares in the pharmaceutical products and electrical machinery and equipment (two groups that follow road vehicles in terms of share of exports) also began to decline in the first and third quarters of 2021, respectively. The market shares of power-generating machinery and equipment and of machinery and equipment specialised for particular industries have continued to increase. The market share of iron and steel has also increased – the growth in the value of exports in the EU market exceeded the high growth in the value of EU imports. Large differences in export/import trends among product groups are also reflected in the geographic markets. With unfavourable trends in the automotive sector, Slovenia's market share in France was 15% lower in the third quarter than in the same quarter before the outbreak of the epidemic. It was also lower in the Croatian (-8.1%) and Italian markets (-3.3%), though it is gradually strengthening in the latter. Compared to the pre-epidemic level, it increased in Slovenia’s largest trading partner, Germany (+1.6%), despite a somewhat less favourable development in the third quarter.

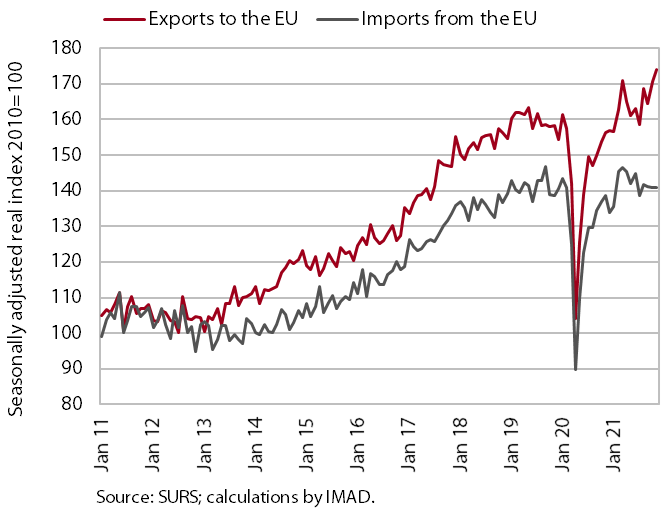

Trade in goods – real

Trade in goods continued to increase in November; uncertainty in the international environment has a noticeable effect on the fluctuations in export and import activity in Slovenia. Exports of goods, especially to other EU Member States, increased in November for the second month in a row, while imports remained the same (seasonally adjusted). At the same time, there have been stronger monthly fluctuations in trade in goods with other EU Member States (Germany, France and Austria) in recent months, which we believe were mainly related to exports of vehicles and vehicle parts and accessories. Trade in goods, especially trade in automotive industry products, continues to be particularly affected by uncertainties related to supply chain disruptions (especially in the automotive industry) and high commodity prices. In the first 11 months, goods exports to the EU increased by 13.8% compared to the same period in 2019 and imports from the EU by 1.8% (by 13.8% year-on-year, imports by 11.8% year-on-year). Export expectations and orders rose further in December, well above long-term averages.

Trade in services – nominal

The several months of growth in foreign trade in services was interrupted in October (seasonally adjusted). Trade in travel and in administrative and support service activities, accounting for 40% of all trade in services, was lower, and trade in ICT and construction services fell sharply. Relatively favourable developments continued in transportation and travel. Year-on-year, total trade in services was significantly higher in October, mainly due to the very low base in 2020, when the activities of several sectors of the economy were still severely constrained, while trade remained at a similar level compared to the same period before the crisis. Lower trade is particularly evident in tourism and in personal services, arts and recreation, while other important groups of services are mostly already well above comparable pre-crisis levels.

Production volume in manufacturing

Manufacturing production growth was relatively strong again in November, after stagnating in the previous month. Growth continued in medium-technology industries, and high-technology industries also recorded an increase. However, growth in low-technology industries was interrupted and recorded a moderate decline. Year-on-year increase in production volume in manufacturing was again quite high, strongest in low-technology industries and lowest in medium-high technology industries. In the case of the latter, growth was mainly affected by developments in the automotive industry, where production volumes are even lower year-on-year due to supply chain disruptions and uncertainty about the future development of the industry in the context of the green transition. The year-on-year growth of low-technology industries was mainly due to other manufacturing activities, which achieved extremely high year-on-year growth, largely due to the low base in 2020, as the increase in production volume is significantly lower compared to the same period in 2019.

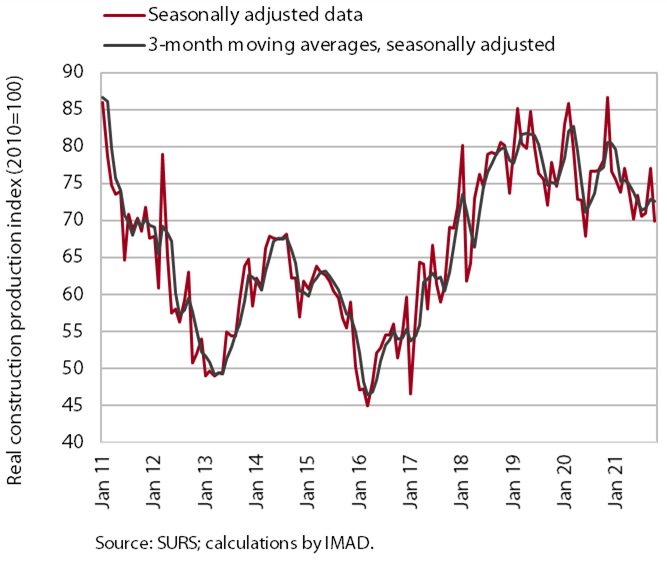

Activity in construction

Fluctuations in construction activity continued in October. After an increase in September, the value of construction output fell by 9.2% in October and was 10.7% lower than in October 2020. At the monthly level, activity in the individual construction segments has fluctuated markedly. Despite these fluctuations, activity in civil engineering works and specialised construction remains at the levels reached at the beginning of the year. Activity is declining in residential construction and especially in non-residential construction. The stock of contracts has also fluctuated similarly on a monthly basis. It peaked in July, but after a sharp decline in August, it has increased again slightly in the last two months.

Construction prices increased sharply in the last year under the pressure of rising commodity prices and shortage of labour. The implicit deflator of the value of completed construction works (used to measure prices in the construction sector) was 7.6% in October and over 10% in building construction.

Turnover in trade

In October, turnover in trade increased for the third month in a row. The month-on-month growth was mainly due to high growth in retail trade, where, in addition to a steady increase in non-food and food sales, sale of automotive fuels increased by as much as a third. Due to low turnover following the declaration of the epidemic and the introduction of restrictions on the sales of goods and services in October 2020, turnover in this sector almost doubled year-on-year; it was also almost a third higher than in October 2019. In total, turnover in trade in October was 12% higher year-on-year and 4% higher than in October 2019. Of all the main segments, turnover remained lower only in the sales of motor vehicles. According to the preliminary data, turnover in this segment increased in November, while it decreased slightly in retail trade.

Turnover in market services

In October, real turnover in market services decreased. After five months of growth, it fell by 1.7% month-on-month and was 16.8% higher year-on-year. The decline was most pronounced in professional and technical activities, mainly due to a renewed drop in turnover in architectural and engineering services. Turnover in transportation, accommodation and food service activities, and administrative and support service activities also remained at a high level, increasing again for travel agencies while decreasing for employment agencies. Turnover growth continued only in information and communication activities, due to higher sales of computer services in the domestic and foreign markets. Turnover in October was higher year-on-year in all market services, but compared to the same month in 2019, only travel and employment agencies saw significantly lower turnover (by 46% and 22% respectively).

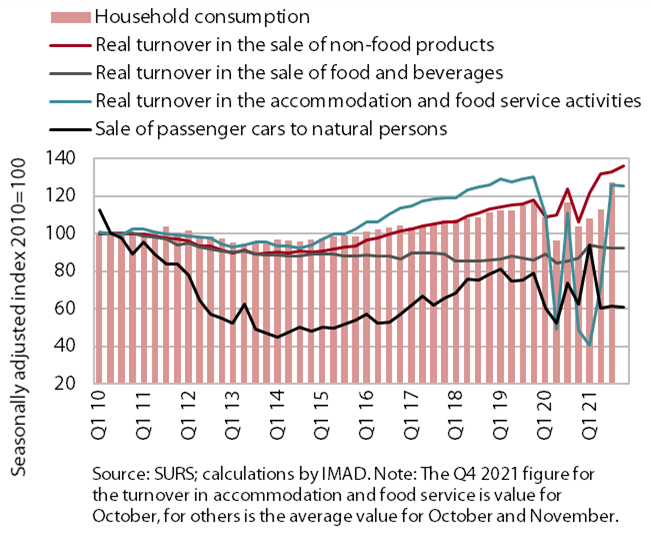

Selected indicators of household consumption

Household consumption remained stable at the beginning of the final quarter and was significantly higher than a year ago, partly due to the low base. Compared to the third quarter, spending on non-food products further increased, and sales of automotive fuels also rose strongly, due to higher sales both to households and legal entities and to transit customers. Relatively high household spending on food and beverages and on accommodation and food service activities in the domestic market, which was also influenced by the redemption of vouchers, and in foreign markets also continued. Year-on-year consumption growth strengthened significantly in most segments compared to the third quarter, mainly due to low sales caused by the restrictions on the sale of goods and services in the final quarter of 2020.

Real estate, Q3 2021

Given the relatively high number of transactions, dwelling price growth accelerated in the third quarter. Prices were up 12.9% year-on-year and 10.1% overall in the first nine months, which represents a strong acceleration from the average growth of 4.6% in 2020. In the third quarter, the year-on-year price increase was similar (by about 13%) for both existing and newly built dwellings (the latter account for only 1% of all transactions). According to our estimates, the growth of prices in 2021 was influenced by several factors. On the supply side, the main factors affecting prices for several years have been the low supply of newly built dwellings and, more significantly this year, higher prices for raw materials for construction. Meanwhile, the price increase was also influenced by increased household demand stimulated by the rise in total savings during the epidemic, the maintenance of relatively high disposable income and the persistence of favourable credit conditions (new housing loans rose by more than a third year-on-year in the year to October).

Economic sentiment

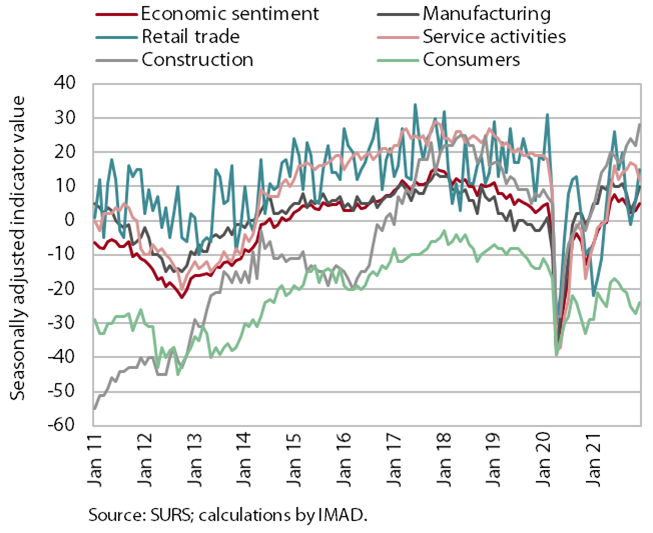

The Economic Sentiment Indicator improved in December, but the average value for the last three months points to a slowdown in economic activity in the last quarter. At the monthly level, confidence improved in most activities and among consumers. Confidence thus remained significantly higher in December than in the same period last year; it was also higher in manufacturing and construction than in the same period in 2019. Despite the improvement in the last two months, however, confidence in most activities deteriorated compared to the previous quarter. The deterioration in manufacturing is the result of the current situation in the international environment (supply bottlenecks, rising non-energy commodity and energy prices), while the deterioration in the retail trade and among consumers was caused by uncertainty about the epidemic situation and measures. On the positive side, confidence in construction stands out; this increased significantly in the last quarter and is well above the long-term average.

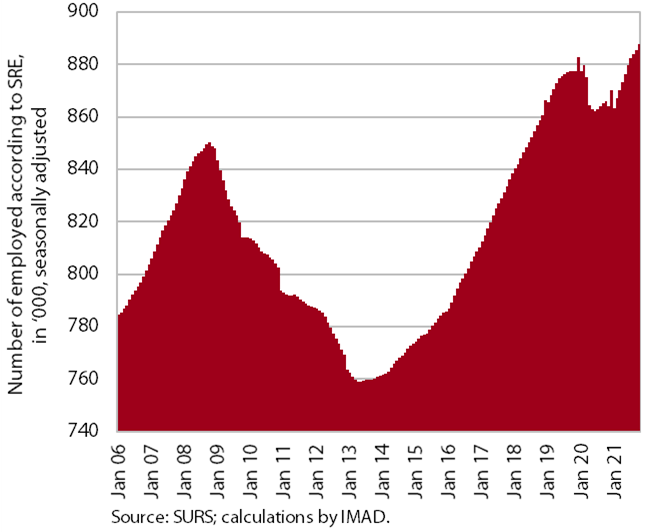

Number of employed persons

Employment rose further in October, reaching its highest level measured to date. The highest year-on-year increases were recorded in accommodation and food service activities and construction, with employment in the latter significantly higher than in October 2019, while employment in the former remained below the level of two years ago. The containment measures also had a strong impact on the arts, entertainment and recreation, where, however, the number of employed people also remained lower this October than in the same period of 2019. In the first ten months, the number of employed persons was 1.1% higher than last year and 0.4% higher than in the same period of 2019. In the midst of a rapid economic recovery, employment growth is still largely dependent on the hiring of foreigners (their contribution to total employment growth was over 50% in October), as was the case before the outbreak of the COVID-19 epidemic. This is a consequence of demographic change and the related shortage of domestic labour. The economic sectors with the highest share of employed foreigners in the first ten months were construction (43%), transportation and storage (31%), and administrative and support service activities (24%).

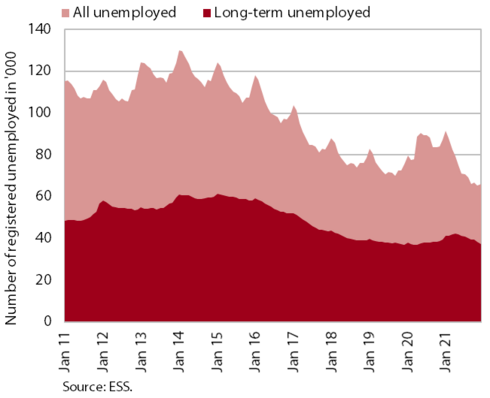

Number of registered unemployed persons

Seasonally adjusted data continue to show a decrease in the number of registered unemployed in December (by 2.9%), which was more pronounced than in previous months. According to original data, 65,969 people were unemployed at the end of December, 0.9% more than at the end of November. This largely reflects seasonal trends related to a higher inflow into unemployment due to the expiry of fixed-term employment contracts. The number of unemployed was 24.4% lower than a year ago and 12.4% lower than in December 2019. On average, 74,316 persons were unemployed in 2021, 12.6% less than in 2020 and 0.2% more than in 2019. Among the unemployed, the number of long-term unemployed rose in the first four months of last year but then fell slightly again by the end of the year in view of the high demand for labour, which is also reflected in the high rate of job vacancies. At the end of December 2021, there were 5.6% fewer long-term unemployed than at the end of 2020 and 1% more than at the end of 2019. Of the long-term unemployed, more than half have been unemployed for more than two years.

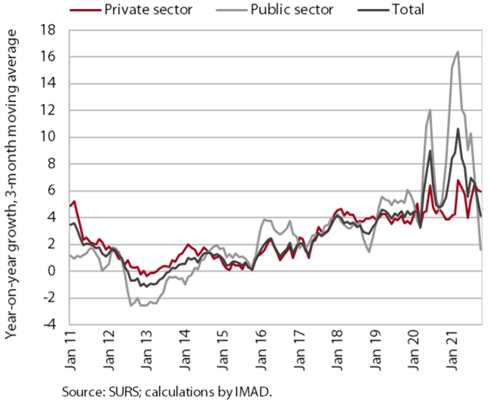

Average gross wage per employee

Year-on-year wage growth in the public sector was low in October (0.5%), while it remained relatively high in the private sector (5.7%). Year-on-year public sector wage growth slowed significantly in the second half of the year due to the cessation of epidemic-related bonus payments. In the first ten months, public sector wages were 9.1% higher than in the same period of 2020. In the private sector, average wages increased by 5.7% year-on-year in the first ten months, mainly due to the impact of the minimum wage increase at the beginning of the year, but also to the return to employment of workers who had participated in job-retention measures. According to our estimates, wage growth in some private sector activities (administrative and support service activities, construction, and accommodation and food service activities) may already be affected by labour shortages.

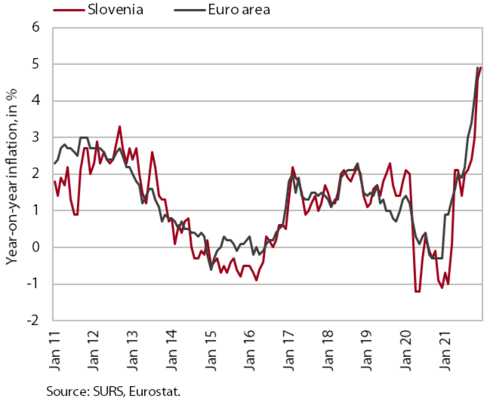

Consumer prices

Year-on-year consumer price inflation continued to rise, reaching 4.9% in December 2021. Inflation continues to be driven mainly by higher energy prices and supply chain problems. Although the year-on-year increase in oil product prices slowed slightly towards the end of the year in the face of falling oil prices on international markets and the government’s decision to re-regulate heating oil margins, the year-on-year increase was still around 30%. The rise in heat energy prices continued to accelerate rapidly, reaching a 70% year-on-year increase in December. At the end of last year, food prices also rose sharply year-on-year (by 4%), amid the lower base and a significant monthly increase (2.1%). Due to rising car prices, prices of durable goods are also rising, by 6.5% year-on-year, and prices of semi-durable goods increased by 4.8%. At the end of last year, the year-on-year increase in services prices (1.5%) was sustained.

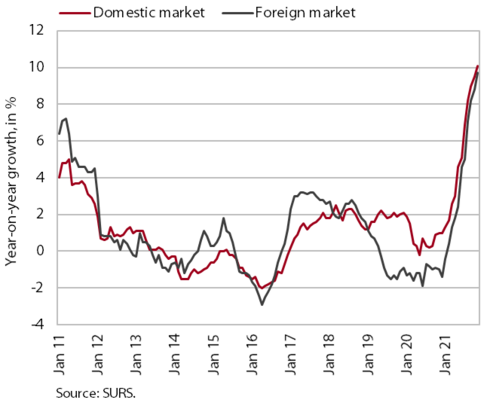

Slovenian industrial producer prices

Slovenian industrial producer prices continue to rise. They increased by almost a tenth year-on-year in November. Prices are rising across all industrial groups, both in the domestic and foreign markets. Overall growth continues to be driven mainly by prices in the intermediate goods group, which rose by around 15% year-on-year. The increase in prices for capital goods has stabilised at around 8.5% over the past three months. Energy prices have also risen but, despite the increase in the last two months, their year-on-year growth in the domestic market remains relatively modest (3.7%). In the face of production bottlenecks and higher non-energy commodity and energy prices, prices for consumer goods, which rose by 3% year-on-year, increased more in November than in previous months. Prices in the durable goods group rose somewhat more markedly, by about 4%, while prices for non-durable consumer goods increased by about 3% year-on-year.

Current account

The current account surplus fell again in October. In the last 12 months, it amounted to EUR 2.3 billion (4.6% of GDP), which was lower than in the previous year. The lower year-on-year surplus is entirely due to a lower trade surplus, as the real growth of imports was higher than that of exports. The terms of trade also deteriorated. As the increase in import prices (7.5%) was higher than that of export prices (3.1%), the operating costs of Slovenian exporters increased. The surplus in services trade continued to increase, especially in trade in construction services and trade in higher value-added services (research and development services and telecommunications, computer and information services). The primary income deficit decreased year-on-year, mainly due to higher subsidies from the EU budget for agricultural and fisheries policies and lower costs of external debt servicing. The lower deficit in secondary income is mainly due to higher government sector receipts from the European Social Fund and ongoing international cooperation.

Loans to domestic non-banking sectors

The year-on-year growth in the volume of bank loans to domestic non-banking sectors, which increased considerably in October, remained at around 3.6%. Lending to enterprises and NFIs remains moderate, growing by about 4% year-on-year. Similar year-on-year growth was observed in loans to households, mainly due to the high growth (8.6%) in housing loans. Lending in the form of consumer credit has continued to decline year-on-year, with a year-on-year decline of around 5% since the middle of last year. Growth in the volume of household deposits is still relatively high year-on-year (7.6%), but it slowed in the second half of the year as inflow of deposits in banks moderated. The share of non-performing claims is no longer declining and has stabilised at 1.3% in recent months. Among all groups and sectors, the share of non-performing loans increased compared to the pre-outbreak period only in accommodation and food service activities (by a half to 12.6%) and in consumer loans (to 3.7%).

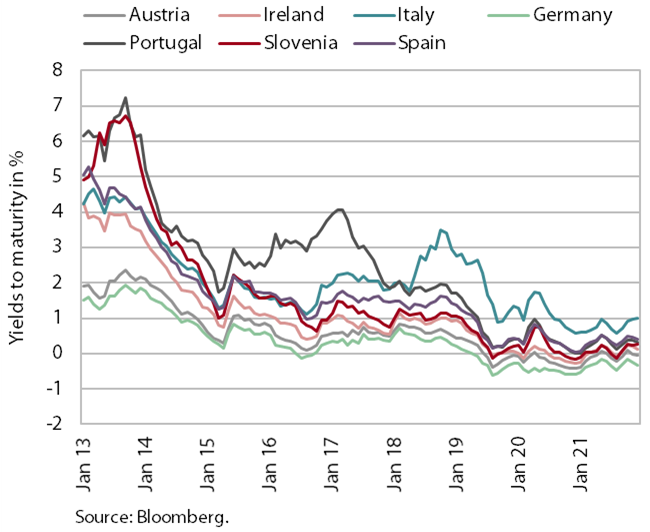

Bond, Q4 2021

Yields to maturity of euro area government bonds rose slightly in the last quarter of last year but still remain very low. The higher yield to maturity of government bonds was influenced by the further rise in inflation in the euro area and the decision by the ECB to gradually scale back expansionary monetary policy measures. The yield to maturity of the Slovenian bond was thus 0.25% in the last quarter. The spread to the German bond was 49 basis points, about 15 basis points higher than in the previous quarter, which is comparable to the pre-epidemic period.

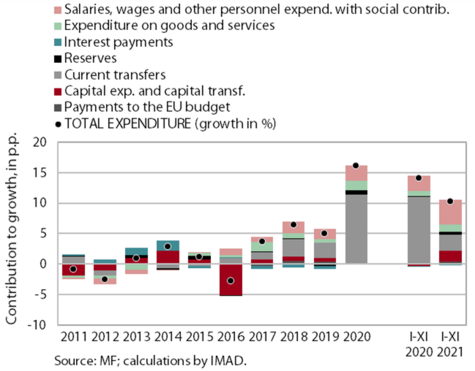

Consolidated general government budgetary accounts

The deficit of the consolidated general government budgetary accounts amounted to EUR 2.2 billion in the first 11 months of 2021 and was 0.3 billion lower than in the same period of 2020. This reflects the high growth in revenue (14.2%), which fell in the same period of 2020, and the slower growth in expenditure (10.3%). Revenue growth is the result of a recovery in economic activity, especially domestic demand, and more favourable labour market conditions. In particular, the growth of tax revenues and revenues from social contributions strengthened in 2021. Compared to the same period of 2020, growth in non-tax revenues has also strengthened, this due to extraordinary revenues from new borrowing and concessions granted for mobile telephony licences. Growth in EU revenue was modest during most of the year but strengthened in November 2021. In addition to lower expenditure growth than in 2020, the structure of growth is also different. The contribution of public servants’ wages to the growth of total expenditure has increased (payments for allowances for work in hazardous conditions during the epidemic, promotions and implementation of the agreement on wages), as did the contribution of investment, while expenditure on subsidies, which had increased a year earlier, fell sharply. In the first 11 months of 2021, total expenditure on measures to mitigate the consequences of COVID-19 amounted to EUR 2.6 billion (EUR 1.7 billion in the first eleven months of 2020), most of this on allowances for public sector workers and reimbursement of fixed costs to companies. According to the preliminary data, the deficit of the state budget, which accounts for the largest part of the consolidated balance sheet, increased sharply in December and amounts to EUR 3.1 billion in 2021, which is 6.1% of GDP. However, as expected, it did not reach the autumn estimate (EUR 3.9 billion or 7.9% of GDP) from the adopted Ordinance, due to higher tax revenues and lower expenditure, especially on investment.

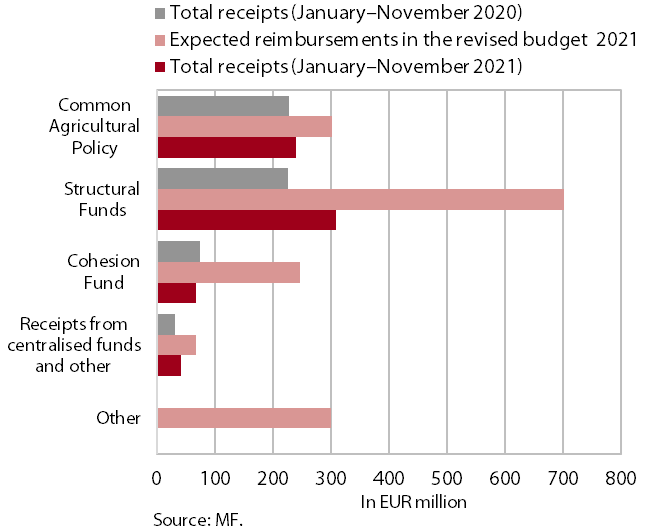

Receipts from the EU budget

Slovenia’s net budgetary position against the EU budget was positive in the first 11 months of 2021 (at EUR 100.6 million). In this period, Slovenia received EUR 658.6 million from the EU budget (40.7% of revenue envisaged in the state budget for 2021) and paid EUR 558 million into it (98.7% of planned payments). The bulk of receipts were resources from structural funds (46.8% of all reimbursements to the state budget) and resources for the implementation of the Common Agricultural and Fisheries Policy (36.5%), while the shares of resources from the EU Cohesion Fund and resources for the implementation of centralised and other programmes were significantly lower (10.3% and 6.3% respectively). According to SVRK data, by the end of November, projects confirmed accounted for 102% and disbursements for 65% of the allocated funds.