Slovenian Economic Mirror

Slovenian Economic Mirror 1/2020

Towards the end of last year, signs of stabilisation started to show in the global economy amid slightly less pronounced negative risks. The moderation of growth in foreign demand in the euro area in the course of last year was in Slovenia reflected mainly in lower growth in exports of some main manufactured goods. Private consumption was strengthening further at the beginning of the last quarter of 2019.

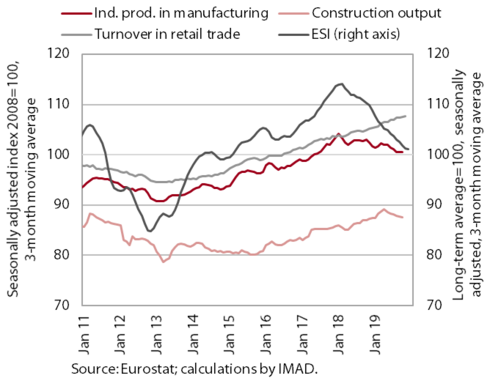

Indicators of economic activity in the euro area and the Economic Sentiment Indicator (ESI)

Moderate activity growth in the euro area continued towards the end of 2019; expectations for the beginning of 2020 show a similar picture. Reflecting favourable labour market conditions, solid activity in retail trade continued in the last quarter of 2019. Weak global trade in circumstances of increased uncertainties continued to be reflected in the stagnation of activity in manufacturing. Activity in construction remained relatively robust, despite the slowdown. The Economic Sentiment Indicator (ESI) and the composite Purchasing Managers’ Index (PMI) remained weak in December. They did not deteriorate in the last months of the year, which could indicate a moderate increase in economic activity at the beginning of this year. Expectations are rising in our main trading partner, Germany, where the situation is expected to improve shortly in both manufacturing and service activities.

Prices of Brent crude oil per barrel and the USD/EUR exchange rate

The price of Brent crude strengthened with the escalation of geopolitical tensions at the beginning of 2020. Due to a decline in oil supply, the dollar price of Brent crude had already risen noticeably in December 2019 and exceeded the annual average, which was almost 10% lower than in 2018. With the escalation of tensions in the Middle East at the beginning of 2020, the oil price increased further, to over 70 USD per barrel.

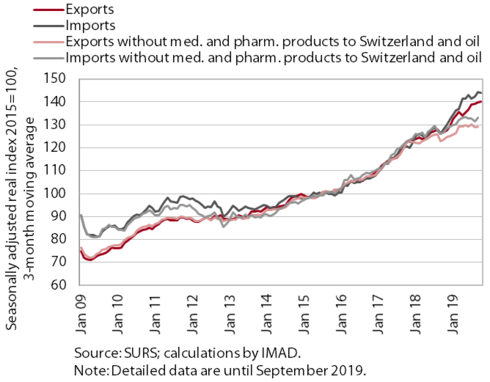

Trade in goods

The moderation of growth in Slovenia’s main trading partners in the euro area is reflected in lower growth in Slovenia’s external trade. The slowdown in growth of foreign demand from the euro area has already been reflected in less favourable export expectations and movements of exports of some main manufactured goods, particularly for intermediate consumption, for several months. Exports to Germany have slowed in particular. In the third quarter, they were lower year on year, which was related to lower exports of machinery and transport equipment (particularly vehicles and vehicle-related products, which account for almost one third of all exports to Germany). Slower growth was also recorded for imports of intermediate goods, which is related to the moderation of growth in manufacturing.Total growth in goods trade otherwise remained high primarily due to strong activity in the distribution of medicinal and pharmaceutical products (re-exports to Switzerland).

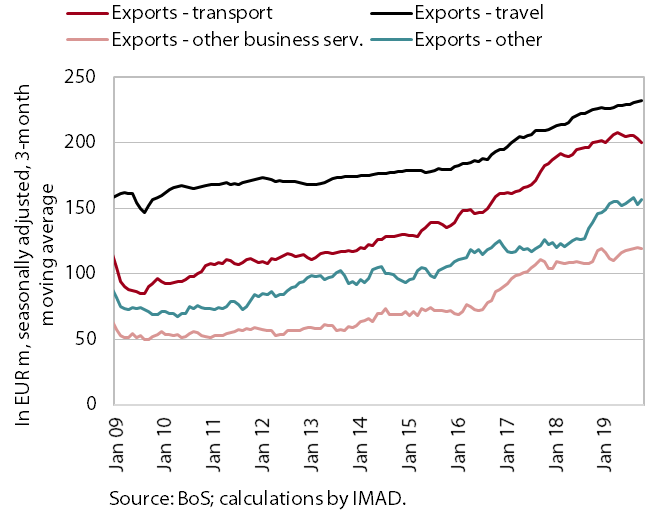

Trade in services

Growth in exports and imports of services has slowed notably in recent months. In the first ten months, nominal exports were 7.6% higher year on year. Their growth thus remained lower than in the same period of 2018. While all main groups of services contributed almost equally to growth, the growth of exports of processing services (related to the distribution activity in the area of medicinal and pharmaceutical products), ICT services and technical, trade-related services was strengthening in particular. Spending by foreign tourists increased as well, albeit less than in previous years. In the third quarter, year-on-year growth in exports of transport and construction services, the main drivers of exports in the first half of 2019, slowed down significantly. This is mainly related to the moderation of growth in economic activity and investment in our main trading partners. The growth of imports of services (3.9%) also eased, on account of factors similar to those in exports.

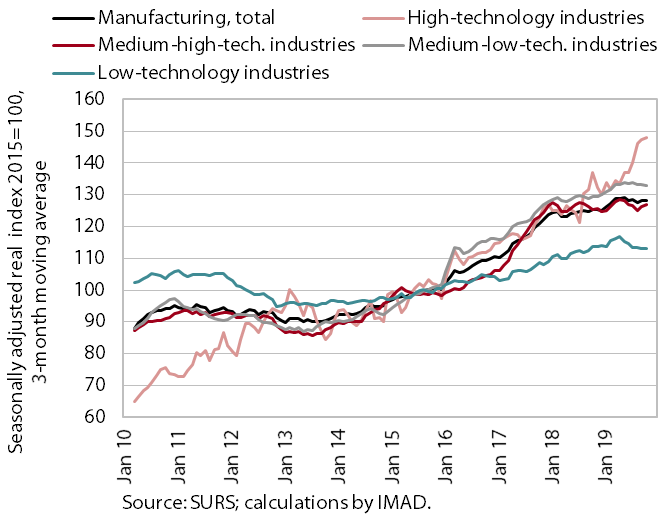

Production volume in manufacturing

Production volume in manufacturing remained at the first-quarter level at the beginning of the last quarter of 2019. At the beginning of the last quarter, production increased further in high-technology industries, while in the last months of the year, it also rose slightly in medium-high technology industries. Production in high-technology industries was 11.4% higher year on year in the first ten months; in most other industries it was similar to that in 2018 or only slightly higher. According to the Business Tendency Survey, higher production growth is impeded particularly by insufficient demand. Year-on-year growth in turnover from sales on foreign markets slowed in the last two years (from around 10% in 2016 and 2017 to around 3% in 2019). Significantly more modest growth was also recorded on the domestic market, where most activities otherwise generate a smaller share of turnover than abroad.

Activity in construction

The value of construction output increased in October after several months of decline, but was lower than at the end of 2018 and the beginning of 2019. Following strong growth at the beginning of 2019, which was also boosted by favourable weather conditions, the value of construction output fell in the middle of the year. The decline was the most pronounced in the construction of non-residential buildings, which is related to deteriorated expectations of the business sector and its investment activity. The slowdown in civil-engineering works was more moderate, while activity in the construction of residential buildings increased further, with significant monthly fluctuations. The indicators of the stock of contracts and new contracts in construction declined towards the end of 2018, before strengthening again in 2019 and exceeding the 2017 level.

Residential property prices and transactions

The average residential property prices increased further in the third quarter, as did the number of transactions. In the first nine months, prices were 7.5% higher year on year on average (in 2018 as a whole, 9.8% higher). Price growth in 2019 was driven by price rises in existing family houses and flats outside Ljubljana. In 2019, the average price of existing flats in Ljubljana – which had been growing at above-average rates in the previous four years – was only slightly higher than the average price in 2018. The average price of new residential properties, which accounted for only 2.2% of all transactions, was lower year on year after two years of strong growth. After a decline in 2018, the number of residential property transactions increased again in the first three quarters of 2019.

Turnover in trade

In October, turnover in trade was at the level seen at the beginning of the year. In retail trade, which is otherwise significantly marked by fluctuations in automotive fuel sales, only the sales of non-durable non-food products have been rising moderately amid further growth in household consumption. Turnover in wholesale trade was similar to that at the beginning of 2019, which was also a consequence of more moderate growth in activity in some trade-related activities (transportation, construction, manufacturing). Motor vehicle sales also stagnated up to October 2019, after strong growth rates in the previous four years.

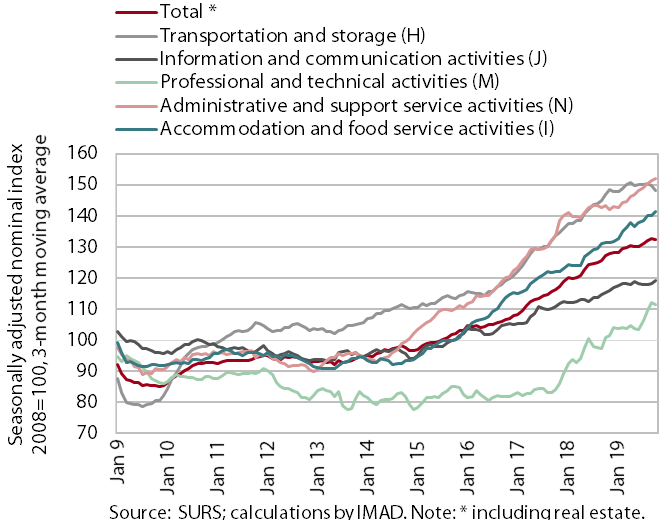

Nominal turnover in market services (excluding trade)

Turnover in market services stopped growing at the beginning of the last quarter of 2019. October recorded further strong growth in accommodation and food service activities, which mainly arose from the sale of food and beverages. Turnover growth in information and communication activities was driven by both telecommunication services (where turnover has otherwise been falling since the beginning of the year) and computer services (with higher export turnover in particular). Turnover in administrative and support service activities maintained its high level seen in the last few months. In professional and technical activities, turnover declined, mostly due to a fall in architectural and engineering services. A more pronounced turnover decline was recorded in most transportation activities, especially in air transport as a consequence of the airline bankruptcy.

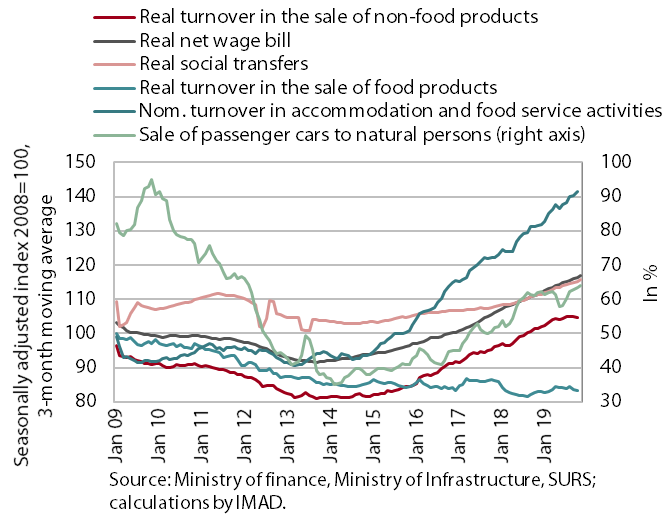

Selected indicators of household consumption

With further growth in disposable income and consumer loans, household consumption continued to increase at the beginning of the last quarter of 2019. The increase in household resources was, in addition to the further growth of the net wage bill and social transfers (including pensions), also due to the high year-on-year growth of newly granted consumer loans in October, which is related to the announced introduction of tighter borrowing conditions in November. With more money available, households increased spending on some non-food non-durable goods and leisure-related services at home and abroad. After strong growth rates in the previous five years, purchases of household equipment and furniture have been falling since the beginning of 2019, while passenger car purchases rebounded at the end of 2019 following the decline in the middle of the year. After rising in the first half of 2019, purchases of food, beverages and tobacco stagnated in the second half of the year.

Economic sentiment indicator

Economic sentiment stopped deteriorating at the end of the year. In December confidence improved somewhat following four consecutive months of decline. The improvement was a consequence of noticeably higher confidence in retail trade, where the assessments of current sales improved significantly. Other confidence indicators were stable in the last quarter of the year, but their values were lower than at the beginning of the year.

The number of employed persons and the number of registered unemployed persons

The growth of employment and the decline in unemployment were less intense last year than in 2018. The number of persons employed increased 2.6% year on year in the first ten months of 2019 (the most in construction, transportation and storage, and accommodation and food service activities), which is less than in the same period of 2018. Labour shortages accompanied by the still high demand for labour were reflected in a further increase in the hiring of foreigners. Their contribution to total employment growth is significant, over 70%. The number of registered unemployed persons decreased further, albeit more slowly than at the beginning of the year. At the end of November it amounted to 72,395, which is 4.9% less than one year before.

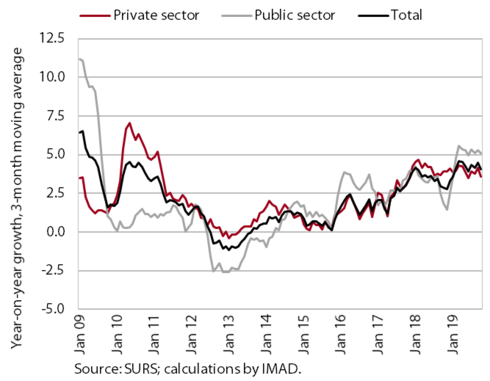

Average gross wage per employee

The strengthening of wage growth in 2019 was mainly a consequence of wage rises in the general government sector. In the first ten months, year-on-year wage growth was 4.3%, compared with 3.4% in the same period last year. Higher growth mainly reflected higher growth in the general government sector on account of the agreed wage rises and promotions and, to a lesser extent, the increase in the minimum wage. Somewhat more moderate growth also continued in in the private sector, where wages increased the most in administrative and support service activities (such as security and investigation activities), accommodation and food service activities, and trade.

Year-on-year price growth in Slovenia and in the euro area

In December-on-year price growth was 0.4 pps higher than one year earlier. The contribution of prices of goods increased, largely owing to higher prices of food, particularly fruit and meat at the end of the year. The higher prices of meat are mainly related to growth in pork prices due to the outbreak of the African swine fever in Asia. Prices of non-energy industrial goods were also somewhat higher, while prices of durable goods dropped further. The growth of energy prices eased in 2019, to 1.2%, which is only one third of that in 2018. Price growth in services slowed towards the end of the year, but was still more than twice that in goods. Prices of services related to housing, health insurance and hotels and restaurants continued to rise rapidly. Core inflation strengthened slightly in 2019, but remained below 2%.

Year-on-year growth in Slovenian industrial producer prices on the domestic and foreign markets

The total year-on-year growth of Slovenian industrial producer prices rose somewhat in November, but remained modest. The fall in prices on foreign markets was less pronounced than in previous months, primarily owing to a somewhat smaller decline in raw material prices, which account for almost half of the index value. Price growth on the domestic market remained around 2%, which was still largely due to strong growth in energy prices (on account of higher prices in electricity, gas and steam supply, where year-on-year growth totals around 15%). Year-on-year growth in non-durable consumer goods is hovering around 2%. Growth in investment goods is also stable.

Components of the current account balance

The current account surplus increased in October and was higher year on year in the last twelve-month period (at 5.9% of estimated GDP). The higher surplus in comparison with the previous 12-month period was mostly due to a higher surplus in trade in transport, construction and processing services. The surplus in goods trade was also higher, which is attributable to volume factors amid the otherwise unchanged terms of trade. On the other hand, the net outflows of primary and secondary incomes increased further owing to higher payments of dividends to foreign investors (primary income) and higher VAT- and GNI-based contributions to the EU budget (secondary income).

Year-on-year growth rates of loans in the Slovenian banking sector

The growth of loans in the banking system remained moderate in November. Year-on-year growth in loans to domestic non-banking sectors strengthened somewhat in November for the second consecutive month, but remained moderate. After modest growth or even decline at the beginning of 2019, the volume of corporate loans has been steadily strengthening from June onwards. This has mainly been a consequence of slower deleveraging, while the volume of new corporate borrowing has remained modest. The growth of household loans has already been stable since 2018 (at around 6%). The year-on-year growth of consumer loans has otherwise slowed slightly. In November their volume dropped at the monthly level, in our estimation largely as a consequence of stronger borrowing in October, i.e. before the introduction of a binding macroprudential instrument. Meanwhile, the growth of housing loans strengthened in November, which may indicate a shift of a portion of consumer lending to lending for housing purposes. The quality of banks’ assets was good, the share of claims more than 90 days in arrears having stabilised at around 1.5% in recent months.

Yields to maturity of euro area bonds, selected countries

The yields to maturity of government bonds increased somewhat in the last quarter of 2019 but remained low. We estimate that this could be a consequence of increased uncertainties in the international environment in the last quarter of 2019. In the last quarter, the yield to maturity of the Slovenian bond thus rose by slightly more than 10 basis points to 0.13%, while the spread to the German bond remained at around 50 basis points.

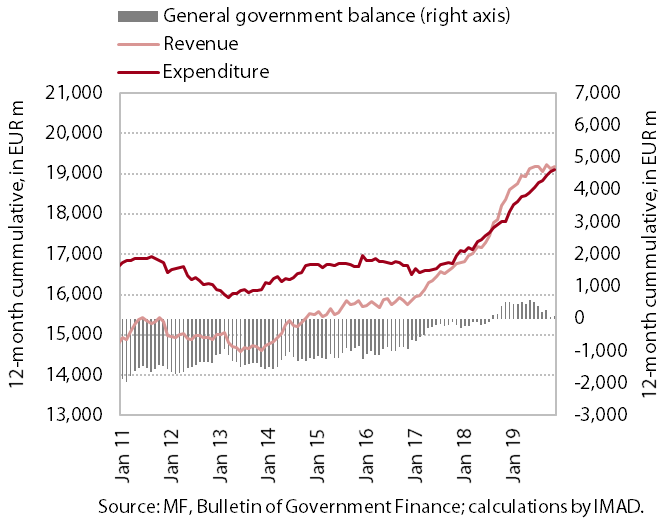

Revenue, expenditure and balance of the consolidated general government budgetary accounts

In the absence of one-off revenues and amid measures that accelerated expenditure growth, the surplus of the consolidated balance in the first eleven months of 2019 was lower than in the same period of 2018. Revenue growth was considerably lower in this period, primarily on account of year-on-year lower non-tax revenues (which were at a high level in 2018 due to high dividend payments in October) and lower receipts from the EU budget (also as a consequence of one-off payments in 2018). The weaker revenue growth was also due to lower growth in revenues from taxes (personal income tax and VAT). Expenditure growth has already been stronger since the beginning of the year. It is mainly related to the adopted agreements on wage rises and further growth in employment, but also to measures in the area of transfers to individuals and households. Payments into the EU budget increased as well. Investment growth declined somewhat more year on year than planned. We expect that the surplus will decline from its current level (EUR 346 million) in December, with an increase particularly in some flexible expenditures (expenditure on goods and services) and expenditure related to the financing of EU projects (particularly investment).

Receipts from the EU budget

Slovenia’s net budgetary position against the EU budget was positive in the first eleven months of 2019 (at EUR 49.2 million). During this period, Slovenia received EUR 535.6 million from the EU budget (52.7% of the revenue planned in the budget for 2019). The bulk of revenue was accounted for by funds for the implementation of the Common Agricultural and Fisheries Policy (81.0% of planned revenue), while reimbursements from structural funds were somewhat lower (48.8%). Significantly lower were reimbursements from the EU Cohesion Fund (27.6%). In the same period, Slovenia paid EUR 486.4 million into the EU budget (98.1% of planned payments into the EU budget). In 2019, the differences between the amounts of EU funds paid and certified expenditures declined significantly. The still low reimbursements from the EU budget into the state budget are a consequence of delays in implementing EU projects.