Slovenian Economic Mirror

Slovenian Economic Mirror 3/2022

In view of the significant increase in uncertainty in the international environment, business expectations point to a further slowdown in the growth of exports and export activities. Trade in goods and manufacturing output declined in the first two months as supply chain disruptions continued. Following Russia’s military aggression against Ukraine, export sentiment deteriorated in the face of significantly lower export expectations. Activity in sectors relying on domestic demand remained favourable at the beginning of the year. With the lifting of the recovered/vaccinated/tested rule, along with expected further price increases and the fear of a possible shortage of some goods due to the crisis in Ukraine, activity was higher in the first quarter in trade and most other services. Consumer confidence fell sharply in March, while confidence remained high in trade and services and in construction. Inflation fell slightly in March due to a temporary drop in electricity prices. Conditions in the labour market continue to be very favourable, but labour shortages have put upward pressure on wage growth in some activities.

Contributions to GDP growth in 2021 in Slovenia’s main trading partner

Economic growth in the euro area and in Slovenia’s main trading partners accelerated significantly in 2021, mainly due to the easing of containment measures, but also to a strong low base effect from 2020. Given the deterioration in the epidemiological situation, ongoing supply chain disruptions and high energy prices and resulting high inflation, growth in the euro area, which had picked up strongly in the second and third quarters of last year, slowed to 0.3% quarter-on-quarter in the last quarter and rose to 4.6% year-on-year (both seasonally adjusted) given the low base of last year. After a significant downturn in 2020 (-6.4%), euro area economy recovered last year (5.3% growth, seasonally adjusted), and reached its pre-crisis level. Given a significant easing of containment measures and adaptation of businesses to the pandemic situation, all GDP components recovered, with private consumption contributing the most to growth. The majority of Slovenia’s main trading partners recorded high and broad-based economic growth, the highest by Croatia and France.

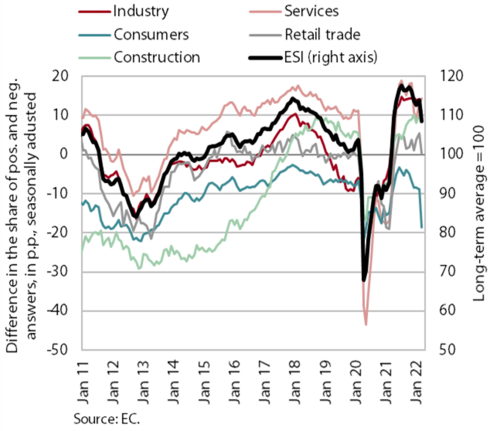

Economic sentiment indicator (ESI)

Following the outbreak of war in Ukraine, survey indicators for the euro area point to a further slowdown in economic growth, and international institutions’ forecasts for this year were revised significantly downward. The value of the composite Purchasing Managers’ Index (PMI) fell in March and was slightly lower in the first quarter as a whole than in the last quarter of 2021. Due to the extension of delivery times and the sharp rise in input prices, the manufacturing PMI in particular was lower than in February. The ESI value was also down in March, recording the largest monthly decline since the outbreak of the epidemic. Economic sentiment deteriorated, especially among consumers and in trade and industry. Given the tense geopolitical situation, international institutions expect a sharper slowdown in economic growth in the euro area and in Slovenia’s main trading partners this year than was expected in the autumn and at the beginning of the year. Before the outbreak of war, growth in the euro area was expected to reach 4% this year and slow to 2.5% in 2023. According to March Consensus average forecasts, growth will reach 3.2% this year and slow to 2.3% next year.

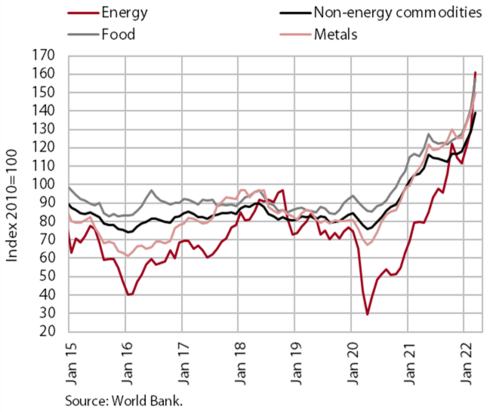

Commodity prices

With the escalation of geopolitical tensions, commodity prices on world markets rose sharply in March. Amid great uncertainty about the continued export of energy from Russia, the average dollar price of Brent Crude rose 20.7% month-on-month (79.3% year-on-year) to USD 117.3 per barrel, its highest level in ten years. The prices for natural gas rose even more. They were 55.7% higher on the European market than in February and as much as 591.9% higher year-on-year. In March, non-energy commodity prices on international markets also rose sharply. According to the World Bank, they rose by 8% compared to the previous month and by 32% year-on-year. Food and fertiliser prices rose the most, up 37% and 128% respectively year-on-year. Energy prices are the biggest contributor to the high year-on-year inflation, which stood at 7.5% in the euro area in March.

Nominal and real effective exchange rates

With a weaker euro and higher inflation, price competitiveness in the first quarter remained at the level of the end of last year. In the first few months of 2022, the euro continued to depreciate against most currencies of Slovenia’s main trading partners – especially the Chinese yuan, the US dollar and the Swiss franc. Overall, the nominal effective exchange rate of the euro against a basket of 37 trading partners’ currencies (weighted by their importance in Slovenia’s trade in goods) fell in the first quarter by 0.4% and was below pre-epidemic levels for the first time in two years. The price competitiveness indicator (REER hicp), which takes into account the movements of final prices (measured by the HICP) in addition to the changes in exchange rates, remained at a similar level as in the previous quarter due to slightly higher inflation in Slovenia compared to the average in its trading partners.

Short-term indicators of economic activity in Slovenia

In view of the significant increase in uncertainty due to the deteriorated international environment, business expectations in Slovenia point to a further slowdown in growth in the export part of the economy. Economic sentiment deteriorated markedly in March. Confidence was lower among consumers and in manufacturing, and export expectations were the lowest since mid-2020. Amid the ongoing supply chain disruptions, activity in the export-oriented part of the economy declined in current terms in the first two months of 2022, but year-on-year growth remained high. Given the low base from last year and higher activity this year related to the COVID-19 measures, expected further price increases and fear of possible shortages of some goods due to the crisis in Ukraine, the beginning of this year saw further year-on-year growth in trade and most other services sectors. After a gradual decline in 2021, activity in construction also increased in January, especially in the construction of non-residential buildings.

Electricity consumption

Electricity consumption in March was about the same as in the same period of 2021 but 4% lower than in March 2019. The gap with the same period before the epidemic was most likely due to the effect on industrial electricity consumption of supply chain disruptions and material shortages. Among Slovenia’s main trading partners, consumption was higher year-on-year in France (1%), Italy (3%) and Croatia (2%), while it was lower in Austria (-2%) and Germany (-4%). In addition to supply problems, the lower year-on-year consumption in Austria and Germany could also be a result of staff absences because of COVID-19 infections, the number of which in March was the highest since the beginning of the epidemic. Compared to March 2019, consumption was lower in Austria (-8%), Germany (-4%) and Italy (-1%), while it was higher in Croatia (6%). Consumption in France was about the same as in March 2019.

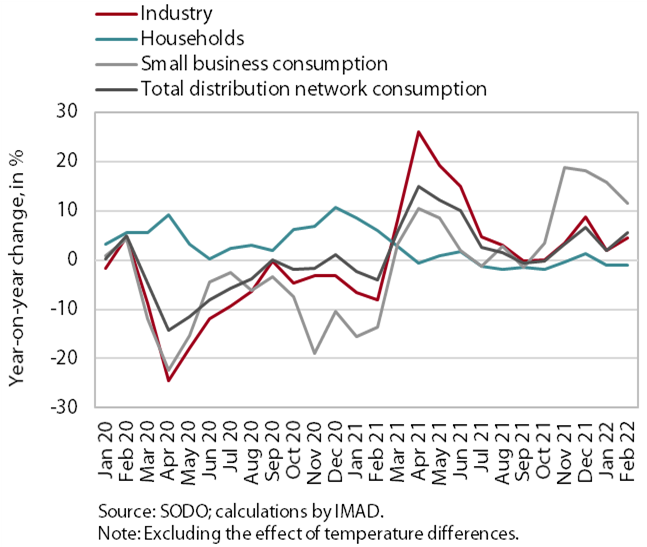

Electricity consumption by consumption group

Industrial electricity consumption and small business electricity consumption were higher year-on-year in February, while the gap with the same period of 2020 was similar as in January. Industrial electricity consumption was 4.4% higher year-on-year in February and small business electricity consumption was 11.6% higher due to the low base last year. Household consumption was slightly lower year-on-year in February (-1.1%). Compared to February 2020, small business consumption was 3.4% lower and industrial consumption was 4.1% lower. This could be related to supply problems and a shortage of raw materials, which, according to the survey data, remains one of main factors limiting business activity. Household consumption was also higher in February than in the same period of 2020 (4.8%), but the surplus was lower than in the previous month (7.4%) due to the improved epidemiological situation.

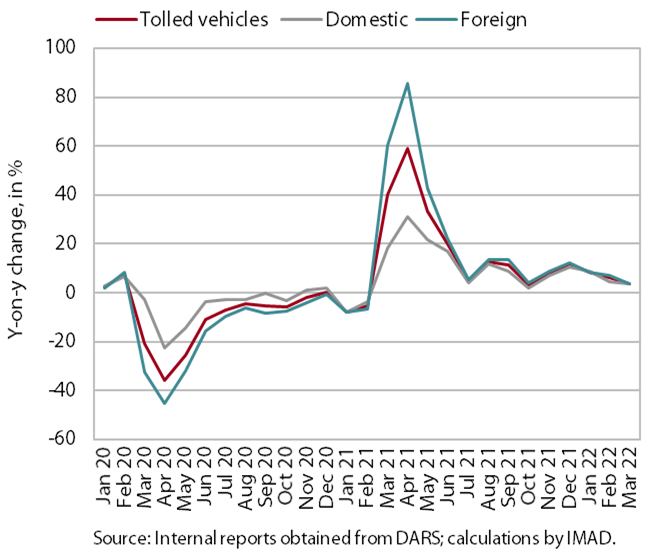

Traffic of electronically tolled vehicles on Slovenian motorways

In March, the volume of freight traffic on Slovenian motorways increased by 4% year-on-year. Compared to the same month last year, which had the same number of working days, the increase was significant, but the trend is no longer closely linked to the impact of the epidemic. Compared to the same period of 2019, freight traffic volumes were 5% higher in March (adjusted for working days). The share of foreign vehicle traffic, which changes slightly from month to month, was over 60% in March, close to the usual averages for that month (in the first year of the epidemic, it was much lower in March, at 52%). In March, which is one of the busiest months, traffic was more than a quarter higher than in January.

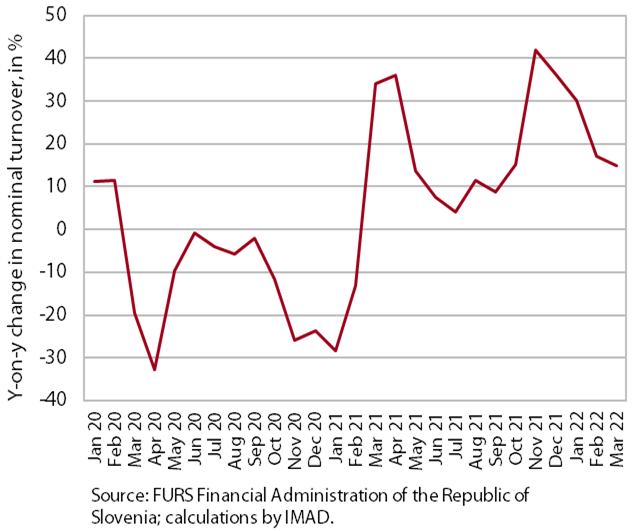

Turnover based on fiscal verification of invoices, in nominal terms

According to data on the fiscal verification of invoices, turnover in March was 15% higher year-on-year in nominal terms and 24% higher than in the same period of 2019, which had two fewer working days. Compared to the same period of 2020, when activity of certain sectors was restricted due to the epidemic, turnover was more than 50% higher. Year-on-year growth in March, which was similar to that in February, was influenced by several factors. The lifting of the recovered/vaccinated/tested rule on 21 February this year was reflected in increased turnover in some sectors in March, particularly in the sale of non-food products and gambling and betting. Higher turnover due to expected further price increases and the fear from a possible shortage of goods in the wake of the crisis in Ukraine, together with higher prices, led to a higher nominal level of turnover in the sale of automotive fuels and food. Year-on-year growth was still high for activities that were almost completely shut down in March 2021 – especially tourism-related services.

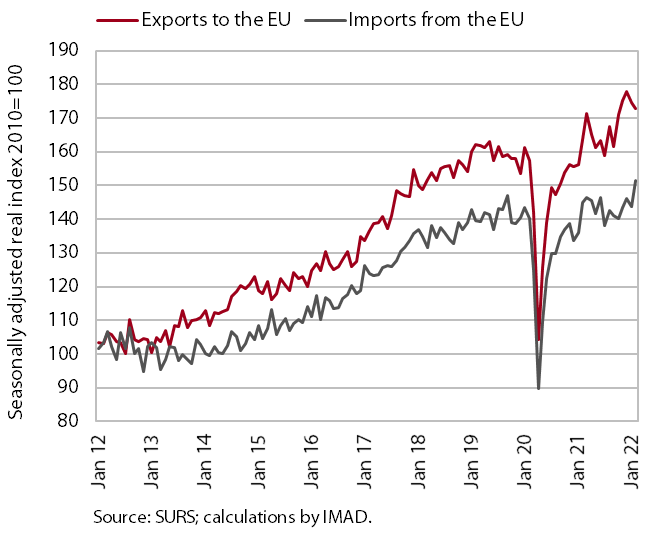

Trade in goods – real

Trade in goods declined slightly in the first two months of 2022. The decline in real exports, especially to EU Member States (seasonally adjusted), was largely influenced by ongoing supply chain disruptions and heightened uncertainty among our major trading partners, due in particular to rising inflation. Imports, especially from EU Member States, were higher than in previous months, which we believe could also be related to the search for alternative sources of supply for products within the EU and thus the shortening of supply chains. Year-on-year growth in trade with EU Member States remained high in the first two months, significantly exceeding the level of the same period in 2020. Due to the war in Ukraine, export expectations fell in March to their lowest level since mid-2020, while export orders remained relatively high.

Slovenia’s export market share in the EU market

Slovenia’s export market share in the EU market fell again year-on-year in the last quarter of 2021. According to initial estimates, it was down by 3% and by 1% in 2021 as a whole. Although the value of Slovenia’s exports to the EU market recorded a strong year-on-year increase, it was lower than the growth of EU imports in the second half of 2021. Slovenia’s market share in the EU market thus decreased last year for the first time since 2012. The unfavourable trends in the automotive industry contributed most to this decline. At the same time, previously growing market shares of the two groups that follow road vehicles in terms of their share in exports, pharmaceutical products and electrical machinery and equipment, began to decline in 2021. Non-ferrous metals and iron and steel made the largest positive contribution among manufacturing goods in the last quarter of 2021 and in 2021 as a whole – the growth in the value of Slovenia’s exports to the EU exceeded the high growth in the value of imports from EU Member States. Among EU Member States, the main reason for the decline in market share in the last quarter was the deterioration in export trends in Slovenia’s largest trading partner, Germany, while the main reason for 2021 overall was modest exports to France, largely related to subdued exports of road vehicles.

Trade in services – nominal

After a pronounced downturn in December, trade in services picked up in January and again exceeded pre-epidemic levels. The recovery in transportation services contributed most to the increase (seasonally adjusted), and trade in ICT and tourism-related services was also higher. Given the low base last year, year-on-year growth of trade in services was still extremely high in January (37%) and was about 2% above the level of the same period of 2020. Most services have been above pre-epidemic levels for several months, but those that were severely affected by the containment measures (trade in travel and trade in personal, cultural and recreational services) continue to lag behind.

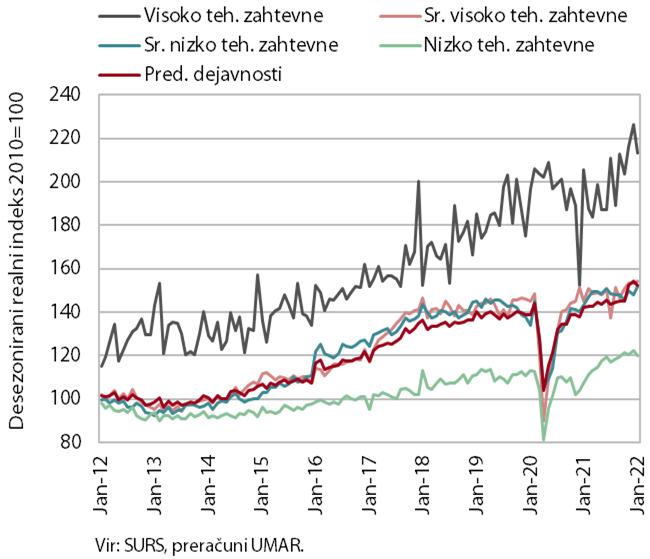

Production volume in manufacturing

Manufacturing output fell for the second month in a row in February. Given the ongoing supply chain disruptions, the volume of production compared to January declined in high- and medium-high-technology industries, while it increased slightly in medium-low- and low-technology industries. Year-on-year, manufacturing growth was 2.4%, the lowest since October last year, with production volume rising the most in high-technology industries and falling in medium-high-technology industries. The decline was mainly due to the automotive industry, which recorded the sharpest year-on-year decline since September last year (22.1%), while contributions of the manufacture of electrical equipment and the manufacture of machinery and equipment n.e.c. were also negative.

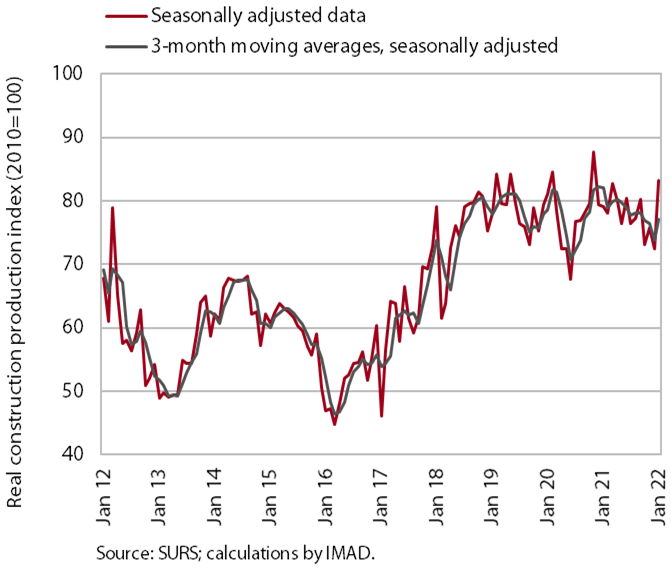

Activity in construction

The value of construction output increased in January after falling gradually in 2021. After a gradual decline in construction activity in 2021, the value of completed works increased in January and was 5.8% higher year-on-year. The largest increase was seen in the construction of non-residential buildings, which was also the construction sector to have contracted most markedly last year. Activity in this construction sector remains relatively low. Fluctuations in other construction sectors are smaller; activity in civil engineering is still relatively high and was 10% higher in January than a year ago.

Cost pressures are increasing. The implicit deflator of the value of completed construction works (used to measure prices in the construction sector) was above 14% in January, the highest level in the last 20 years. According to business trends in construction, high material costs were reported as a limiting factor by two-thirds of companies in March, while material shortage was reported by 30% of companies. Both indicators increased sharply over the past year and reached their highest levels in the past 20 years.

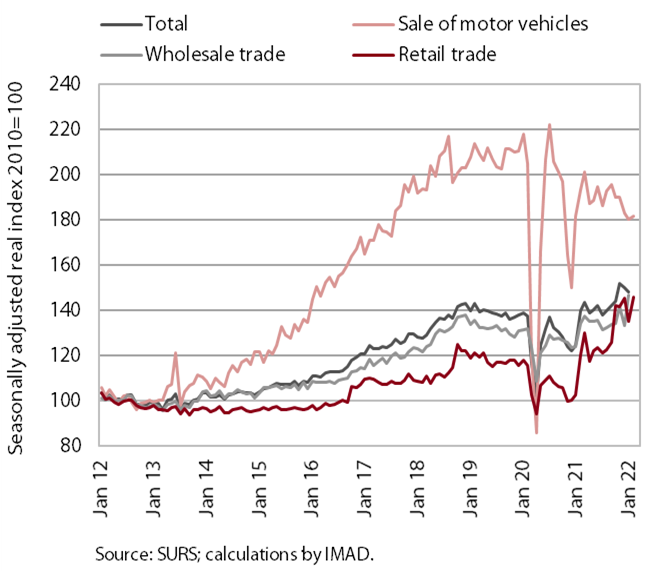

Turnover in trade

Turnover in trade fell in January from the previous month but was more than a fifth higher year-on-year, partly due to the low base. The monthly decline was mainly the result of a sharp fall in retail trade, the dynamics of which have been determined by strong fluctuations in real turnover in the sale of automotive fuels in recent months. After high growth in December, it fell sharply in January but picked up again in February, according to preliminary data. Turnover in the sale of motor vehicles further decreased slightly in January. Due to delays in vehicle deliveries, this was the only main segment to fall short of pre-epidemic turnover. However, after a significant decline in the previous month, growth of turnover in wholesale trade gained momentum.

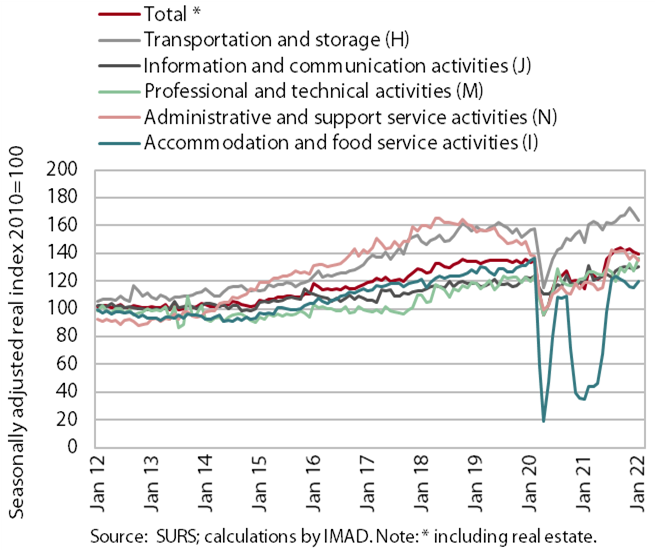

Turnover in market services

Compared to the previous month, real turnover increased again in most market services in January. Given the renewed strong growth in architectural and engineering services, the highest increase in turnover in current terms was observed in professional and technical activities. It increased again in accommodation and food service activities and was higher in information and communication activities due to higher turnover in computer and telecommunication services. Turnover in transportation and storage has been declining for the last two months, with the largest decline in land transport and support transportation activities. Since November 2021, it has also mostly declined in administrative and support service activities, due to lower income in all segments except employment services. Compared to the previous month, total real turnover fell slightly (by 0.7%), but was 25% higher year-on-year due to the low base last year. In January, turnover was higher year-on-year in all market services, while compared to the same period in 2020, it was still significantly lower in travel agencies (by 60%) and in motion picture activities, rental and leasing activities, and food and beverage service activities (by 23% on average).

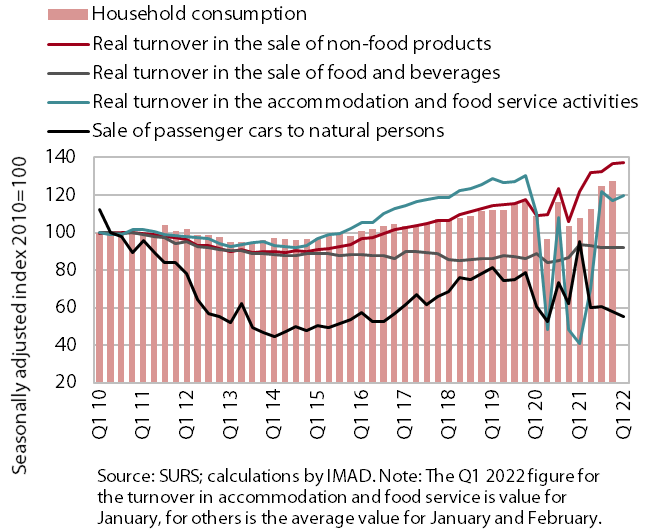

Selected indicators of household consumption

At the beginning of the year, household consumption was significantly higher year-on-year, partly due to the low base. In January and February, household spending on non-food products, food and beverages remained at a similar level as at the end of 2021. The already low sales of passenger cars to households further decreased, which was also affected by the extended delivery times due to supply chain disruptions. Domestic consumption for accommodation and food service activities increased in January and was also much higher year-on-year, as was consumption for some other, mainly tourism-related services, due to the almost complete shutdown in the first quarter of last year. Given the low base last year and higher sales this year related to the lifting of the recovered/vaccinated/tested rule and the expected further price increases, and also fear of possible shortages of goods (especially of automotive fuels and certain food products), we expect year-on-year growth in private household consumption to be high in the first quarter. According to our estimates, the savings rate, which fell by 6.4 p.p. to 16.2% last year, could thus approach its pre-epidemic level in the first quarter.

Real estate

Given the relatively high number of transactions, dwelling price growth accelerated in the fourth quarter. Prices were up 15.7% year-on-year and 11.5% in 2021 as a whole, which is a strong acceleration from the average growth of 4.6% in 2020. Price growth in the fourth quarter and in 2021 as a whole was similar for both existing and newly built dwellings, with the latter accounting for only 2% of all transactions in the year as a whole. In nominal terms, prices at the end of 2021 were 26% above the record average prices of 2008. Even taking into account overall price growth (inflation), dwelling prices were above the 2008 peak – prices of existing dwellings were 12% above this level in the last quarter of 2021, while prices of newly built dwellings were still 6% lower. Prices deflated by growth in nominal gross wages were lagging more significantly behind, i.e. by 9%, but were well above the long-term average last year (average between 2007 and 2021).

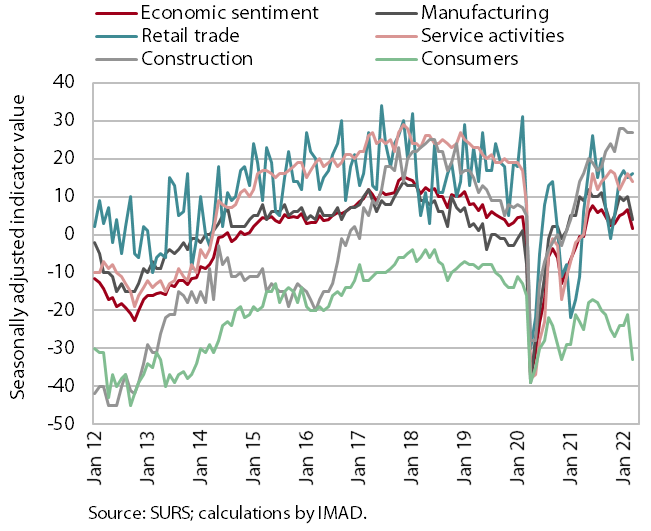

Economic sentiment

Rising prices and the crisis in Ukraine are probably the main reasons for the decrease in the sentiment indicator in March. Year-on-year, it was lower especially among consumers and in manufacturing. Compared to the previous month, the value of the indicator decreased by 5.2 p.p., this being the largest decrease since November 2020. At the monthly level, the value of the consumer confidence indicator decreased the most, by 12 p.p., which is the largest monthly decline since April 2020 (i.e. the outbreak of the epidemic). Compared to March 2021, the value of the economic confidence indicator was still slightly higher (by 2.1 p.p.). Confidence was significantly higher year-on-year in retail trade (by 27 p.p.) and in service activities and construction (by 15 p.p. and 13 p.p. respectively). However, it was lower among consumers and in manufacturing (by 10 and 6 p.p. respectively). This is due to rising prices and uncertainty about further price increases, and thus the country’s economic situation and households’ financial situation, and to the impact of the international environment (bottlenecks in the supply of raw materials and rising commodity and energy prices).

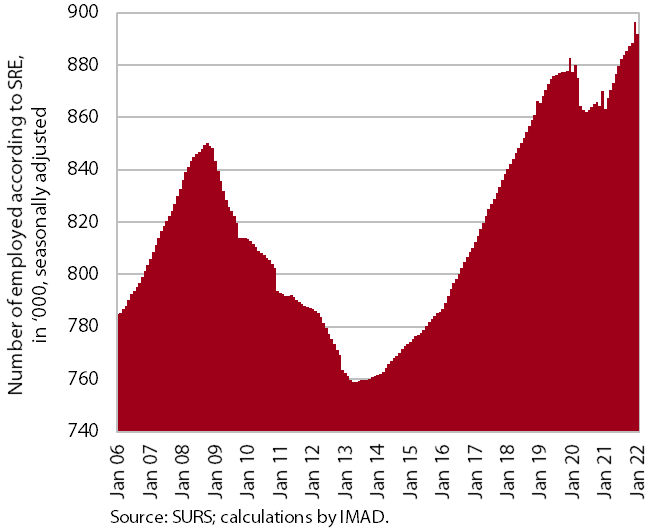

Number of employed persons

Employment fell slightly in January compared to the previous month (-0.7%), mainly due to seasonal trends; year-on-year growth strengthened slightly (3.3%). Year-on-year growth was strongest in accommodation and food service activities and in construction. Employment in the latter was significantly higher than before the epidemic, while employment in the former remained slightly below the level of two years ago. Amid strong economic recovery, employment growth still depended largely on the hiring of foreign workers, whose contribution to overall growth in January was almost 50% year-on-year. The high share of foreign workers is also related to the shortage of domestic labour, which is the most pronounced in construction and administrative and support service activities (both having a high job vacancy rate). The economic sectors with the highest share of employed foreign workers in January were construction (45%), transportation and storage (31%), and administrative and support service activities (24%).

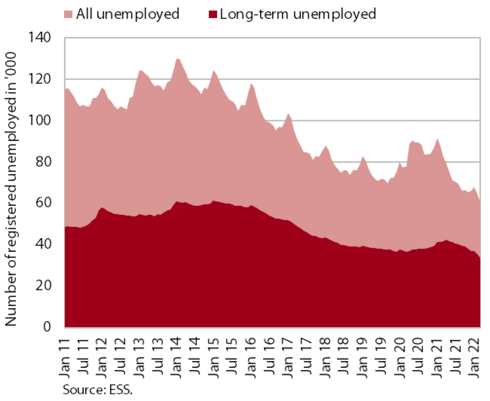

Number of registered unemployed persons

Given the low unemployment rate, the decline in the number of registered unemployed in March was somewhat smaller than in previous months (-2%), according to seasonally adjusted data. According to original data, 60,534 people were unemployed at the end of March, 6.6% fewer than at the end of February and 26.7% fewer than a year earlier. The number of unemployed was also significantly lower (by 22.2%) than at the end of March 2020. Among the unemployed, the number of long-term unemployed increased in the first four months of last year but then decreased again by the end of the year, given the high demand for labour, which is also reflected in the high rate of job vacancies. The number of long-term unemployed, more than half of whom have been unemployed for more than two years, continued to fall in the first three months of 2022 – in March, their number fell by 19.2% compared to March 2021 and by 7.9% compared to the same period at the beginning of the epidemic.

Average gross wage per employee

In January, average wages in the public sector were 10.8% lower year-on-year, while they were 3.4% higher in the private sector. Due to the cessation of epidemic-related allowances, year-on-year wage growth in the public sector slowed significantly in the second half of last year and turned negative year-on-year last November. In the private sector, year-on-year growth in January was somewhat more modest than in previous months, partly due to a relatively high base in January last year (with a sharp increase in the minimum wage and the impact of the methodology used to calculate average wages). Growth was still high in construction, accommodation and food service activities and transportation and storage, which could already be the consequence of labour shortages.

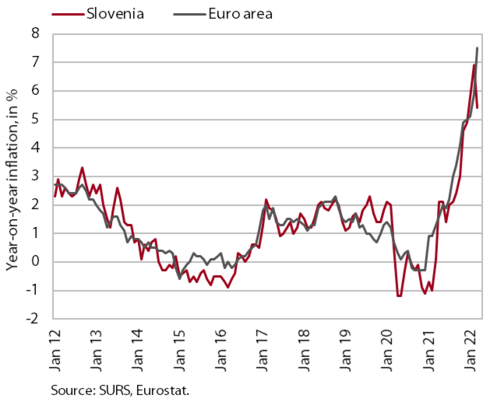

Consumer prices

After a sharp increase at the beginning of this year, consumer price inflation eased slightly to 5.4% year-on-year in March. The lower inflation was mainly due to the passing of the Act on Intervention Measures to Mitigate the Consequences of High Energy Prices, which allowed for a temporary exemption from the payment of certain contributions, leading to a significant decrease in electricity prices (by 38.6% month-on-month and 29.8% year-on-year). The reintroduction of administered fuel prices also somewhat slowed the rise in petroleum product prices, which were nevertheless more than a quarter higher year-on-year. As the prices for package holidays fell significantly due to seasonal factors, the increase in service prices was lower year-on-year. Growth in prices for semi-durable goods remained at around 4.5% year-on-year, while growth in durable goods prices remained high (8.8%). Given the geopolitical tensions, cost pressures are intensifying due to high prices for energy and inputs, leading to an increase in food prices. These were almost 7% higher year-on-year in March, which is the highest increase since 2008.

Slovenian industrial producer prices

Growth of Slovenian industrial producer prices is still high, i.e. 16.5% year-on-year in January. Prices are rising across all industrial groups, both in the domestic and foreign markets. Overall growth continues to be driven mainly by commodity prices, which increased by almost 22% year-on-year in February. Energy price growth increased significantly to almost 60%. Prices in the domestic market (61.5%) contributed the most to this high year-on-year growth. They increased by almost 45% in February, which we believe was due to the conclusion of new contracts with energy suppliers. Capital goods prices increased by more than 10% year-on-year in February. Given production bottlenecks, and higher energy and other commodity prices, consumer prices are also rising gradually, by 5.6% year-on-year. Prices of non-durable goods rose by 6% year-on-year, while prices of durable goods prices rose by about 4% year-on-year.

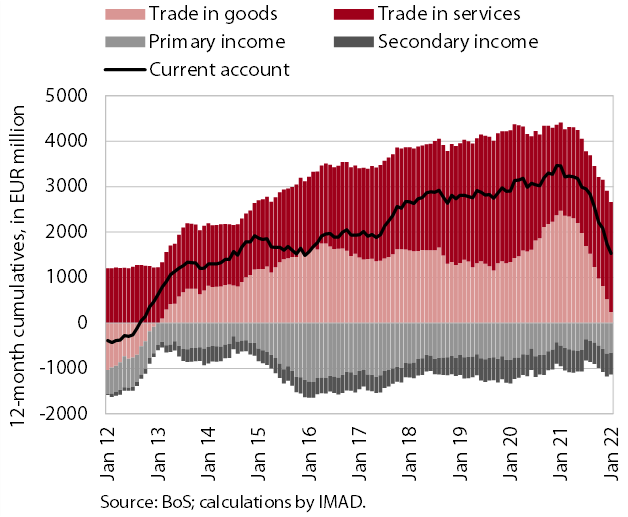

Current account of the balance of payments

The current account surplus fell again in January, mainly due to a decline in the surplus in goods trade. Over the past 12 months, the current account surplus totalled EUR 1.5 billion (2.7% of estimated GDP). The lower year-on-year surplus was mainly a result of a lower surplus in trade in goods, which is related to the rising prices of energy and other primary commodities, which have the largest impact on the price increase of imported products. The deficits in primary and secondary income were up year-on-year. Net outflows of primary income were higher year-on-year, mainly due to higher payments of dividends and profits to foreign investors, while net outflows of secondary income were higher mainly due to higher VAT- and GNI-based contributions to the EU budget. The surplus in services trade continued to increase, especially in trade in travel and other business services.

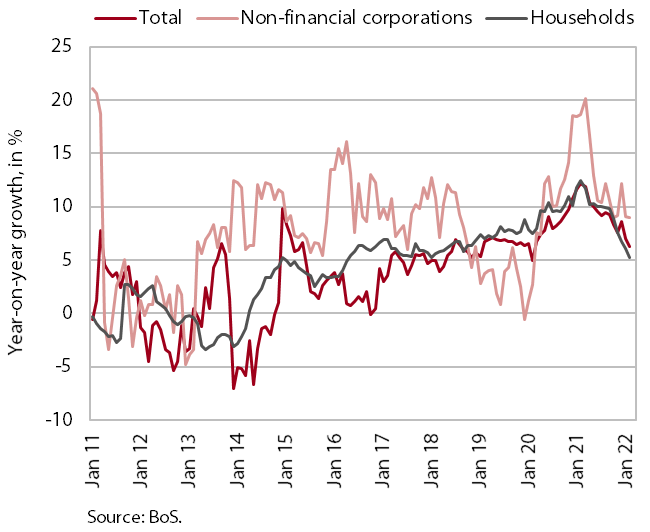

The volume of deposits by domestic non-banking sectors

The year-on-year growth in the volume of bank loans to domestic non-banking sectors increased further in February and approached 7%. Given the high economic activity and favourable financing conditions, the growth in the volume of corporate and NFI loans has been increasing since the end of last year, reaching 8.7% in February amid increased new borrowing. Growth in loans to households has also been steadily strengthening, especially in housing loans, which in February was already a tenth higher year-on-year. The decline in the volume of consumer loans gradually eased off to 3.2% year-on-year in February. Growth in domestic non-banking sector deposits is further slowing in line with the reduction in the savings rate. Amid higher spending, household deposits increased by about 5% year-on-year, which is more than half less than in the same period last year. The growth of deposits by non-financial corporations has been around 9% in recent months. The quality of banks’ assets remains solid and the share of non-performing loans is still relatively low (1.2%).

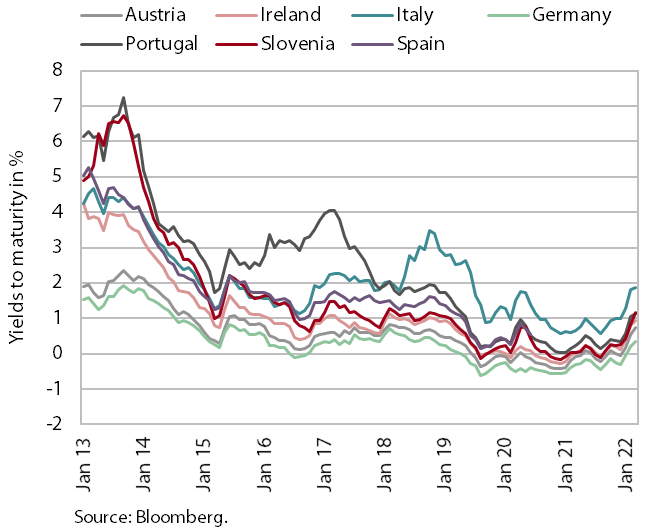

Bonds

Yields to maturity of euro area government bonds rose significantly in the first quarter. The higher yield was influenced by the further rise in inflation in the euro area and the decision by the ECB to slightly accelerate the scaling back of expansionary monetary policy measures. The yield to maturity of the Slovenian 10-year government bond was 0.81% in the first quarter, the highest figure in the last three years. The spread to the German bond was 65 basis points, about 15 basis points higher than in the previous quarter, which is slightly above the pre-epidemic period.

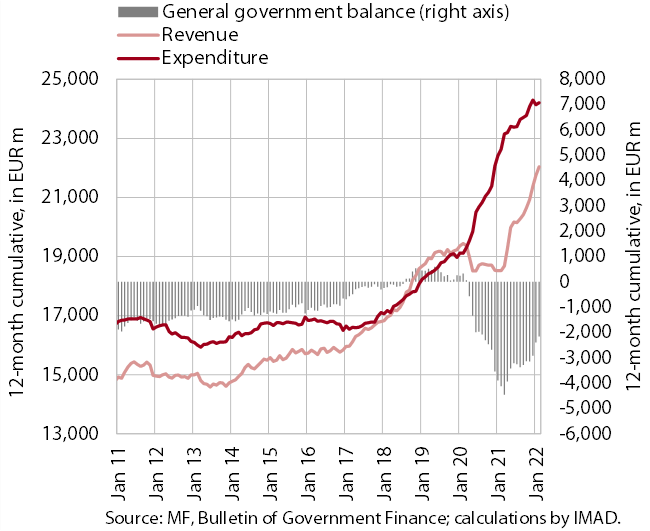

General government deficit and debt

The general government’s fiscal position improved in 2021 amid a rapid economic recovery and lower expenditure on measures to mitigate the impact of the epidemic. The deficit and public debt decreased slightly (from 7.8% to 5.2% of GDP and from 79.8% to 74.7% of GDP respectively), the latter also being affected by the decline in the country’s cash reserves, which still remain high. IMAD estimates that expenditure on measures to mitigate the impact of the epidemic fell from 5.2% of GDP in 2020 to 4.5% of GDP. In contrast to lower expenditure on measures to mitigate the impact of the epidemic, growth in other expenditure increased in 2021. This was due to stronger investment growth as part of a broader European response to support the recovery and to other expenditure, some of which is of a permanent nature.

Consolidated general government budgetary accounts

The surplus of the consolidated balance of public finances totalled EUR 117.5 million in the first two months of 2022. The deficit in the same period last year was EUR 632 million. Revenue in the first two months of this year exceeded last year’s level (by 20.9%) due to further growth in economic activity and favourable conditions in the labour market. Revenue growth arose mainly from higher VAT receipts, while receipts from the EU budget also saw a sharp increase, mainly due to the inflow of funds from the Recovery and Resilience Facility and from structural funds, as funding under the 2014–2020 Financial Perspective is coming to an end. Expenditure decreased in the first two months (by 2.4% year-on-year), reflecting lower payments related to measures to mitigate the consequences of the epidemic. This was reflected in lower transfers to individuals and households (-7.6%), subsidies (-39.1%) and funds for wages (-8.6%). This year's expenditure on measures to mitigate the impact of the epidemic is mainly arising from the tenth anti-corona package (PKP10) and expenditure on containment measures (testing, vaccination, etc.), and in January and February payments from the state budget for these purposes totalled EUR 184 million (EUR 535 million in the same period last year). On the expenditure side, investments and expenditure on goods and services have increased year-on-year.

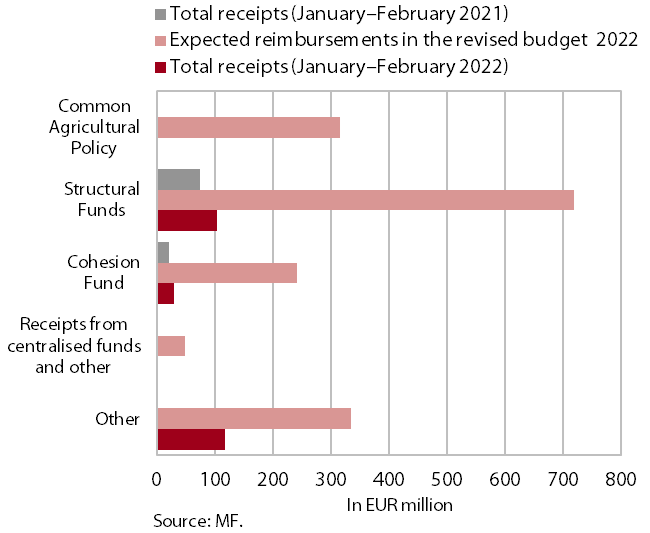

Receipts from the EU budget

Slovenia’s net budgetary position against the EU budget was positive in the first two months (at EUR 113.8 million). In this period, Slovenia received EUR 255.1 million from the EU budget (15.4% of receipts envisaged in the state budget for 2022) and paid EUR 141.3 million into it (25.1% of planned payments). The bulk of receipts were resources from the Recovery and Resilience Facility (46.4% of all reimbursements to the state budget) and resources from structural funds (25.1%), while the shares of resources from the Cohesion Fund (11.6%) were significantly lower. The highest payments into the EU budget came from GNI-based payments (53.2% of all payments). According to SVRK data, by the end of February, operations confirmed under the 2014–2020 MFF (including funds under React-EU) accounted for 110.5% of all allocated funds and disbursements accounted for 68.6% of all allocated funds.