News

A further improvement in the situation, including in the banking system, but no rebound yet in corporate lending

Economic growth in the euro area continued in the third quarter of 2016; moderate economic growth is also expected for the last quarter of the year. During the summer months positive developments also continued in Slovenia; the prospects for the last quarter are also favourable. Labour market conditions improved further; employment growth is expected to continue.

Economic growth in the euro area continued in the third quarter of 2016; moderate economic growth is also expected for the last quarter of the year. According to Eurostat’s estimate for the third quarter, GDP in the euro area grew by 0.3% (seasonally adjusted) and was 1.6% higher than in the same quarter of 2015. The values of the Economic Sentiment Indicator (ESI) and the composite Purchasing Managers Index (PMI) suggest a further strengthening of economic activity in the remainder of the year. In its autumn forecast, the European Commission expects 1.7% GDP growth in the euro area for this year. Its forecasts for next year’s growth have been lowered slightly (to 1.5%) owing to the uncertain consequences of Brexit.

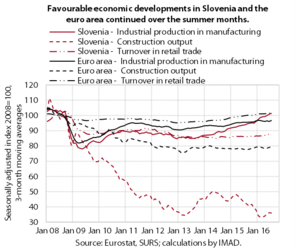

During the summer months positive developments also continued in Slovenia; the prospects for the last quarter are also favourable. Real merchandise exports and manufacturing output have remained high. Activity in construction has stayed almost unchanged after the increase in the second quarter, albeit significantly lower than in the same period of 2015. Turnover is steadily rising across most market services. With the improvement in labour market conditions, turnover expands particularly in some segments of trade and in tourism-related services, where its growth is also underpinned by higher spending by foreign tourists.

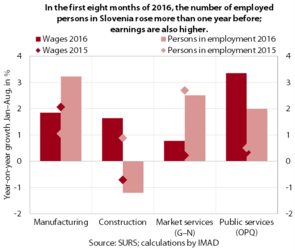

Labour market conditions improved further; employment growth is expected to continue. The number of persons employed increased further in August. In the first eight months, all activities but construction recorded higher year-on-year growth than one year earlier. The number of registered unemployed dropped further, 97,263 persons being registered as unemployed at the end of October, which is 9.5% less than one year earlier. Average gross earnings are steadily rising this year. In the first eight months, the private and the public sector saw much higher year-on-year growth than in the same period of 2015.

After almost two years of deflation, Slovenia has recorded consumer price growth in the last two months. Year-on-year inflation stood at 0.6% in October. The higher year-on-year growth is mainly due to the smaller and smaller energy price declines and stronger food price growth. Prices of semi-durable goods are also up year on year again. Prices of services remain higher relative to the same period last year, while prices of durable goods are lower.

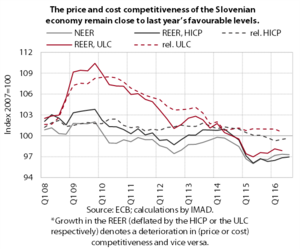

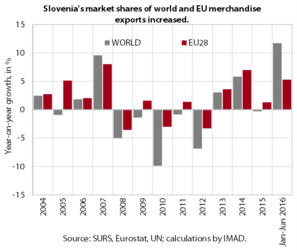

The price and cost competitiveness of the Slovenian economy remain close to the favourable levels seen in 2015. The appreciation of the euro had a smaller impact on Slovenia than on most other euro area countries owing to the geographic structure of Slovenia's trade. Moreover, price competitiveness losses were also mitigated by declining relative consumer prices. The falls in unit labour costs were similar to those in Slovenia's trading partners, but slightly smaller than for the euro area as a whole. Slovenia's market shares of world and EU merchandise exports increased further.

Slovenia has advanced on the scales of international competitiveness this year. According to the WEF’s latest report, its competitiveness has improved as a consequence of more favourable macroeconomic indicators and more positive business executives’ perceptions regarding the ease of doing business in Slovenia. Slovenia has also improved its rankings in other global competitiveness surveys (for example, IMD, WB Governance Indicators), but remains one of the countries that rank lower than before the crisis. According to the latest report on the ease of doing business by the World Bank, Slovenia continues to rank relatively high.

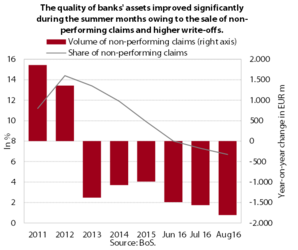

The situation in the banking sector continues to improve; the quality of banks’ assets increased noticeably during the summer months. In the third quarter, the improvement of banks’ asset quality accelerated owing to the sale of a portion of non-performing claims and higher write-offs. Since the beginning of the banking system restructuring, Slovenia has reduced the share of non-performing claims the most of all EU countries that faced similar problems at the onset of the crisis. The structure of sources of funding for banks is changing as well: while banks' reliance on foreign bank financing continues to decrease gradually, non-banking sector deposits are rising. They already account for as much as two-thirds of the banking system’s total assets, which is almost half more than in 2008. Overnight deposits predominate, being almost one-fifth higher year on year.

Nevertheless, the volume of loans to domestic non-banking sectors contracted further. Its decline (of 6.3% in the past year) is a consequence of further corporate and NFI deleveraging, while households are borrowing in the form of housing and consumer loans. Weak lending to the corporate sector is estimated to be due to several factors: it is related to loan supply, with banks remaining cautious amid the still high share of bad loans, as well as to demand side factors, such as the persistent lack of high-quality projects and more and more companies making use of non-bank sources of finance.

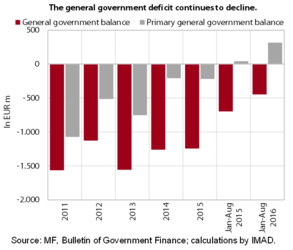

The general government deficit on a cash basis was down EUR 248.8 million year on year in the first eight months of 2016. The year-on-year increase in general government revenue was largely due to higher revenues related to the improving labour market conditions. General government expenditure was lower than in the same period last year mainly as a result of lower investment (during the transition to the new financial perspective). Most of the other expenditures increased, particularly those related to the easing of some austerity measures.