Charts of the Week

Current economic trends from 9 to 20 March 2020: exports and imports of goods, production volume in manufacturing, construction, current account, labour market and wages

The commented data do not yet cover the period of the coronavirus spread in Italy and other European countries. External trade movements slowed last year amid weak foreign demand and stagnation in manufacturing production; similar movements continued in January. The current account surplus widened further, particularly on account to a higher trade surplus in services. Activity also strengthened further in construction, especially in the residential buildings segment. Employment growth at the beginning of the year mainly reflected the increased hiring of foreign workers, while higher wage growth arose largely from wage rises in the private sector (the increase in the minimum wage).

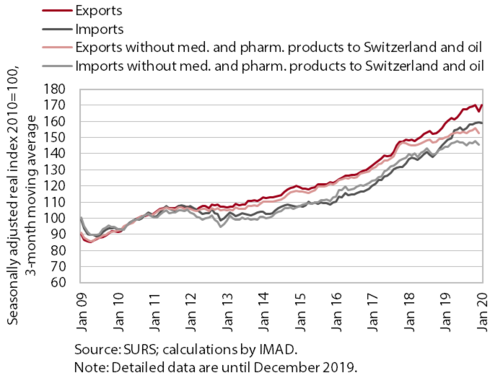

Exports and imports of goods, January 2020

The slowdown in external trade movements seen from the second half of last year continued in January.* Last year’s moderation reflected lower growth in exports of most key manufactured goods as a consequence of weak growth in global trade and economic activity in our main trading partners (particularly Germany, Italy and Austria). At the end of the year modest foreign demand also contributed to a pronounced decline in export orders (to the lowest level in six years), which had remained low after the improvement at the beginning of this year. Owing to stagnant manufacturing production, import growth also eased more noticeably last year.

_______

* The strong monthly fluctuations of exports and imports are mainly related to the distribution of medicinal and pharmaceutical products via Switzerland and, partly, trade in oil and oil products.

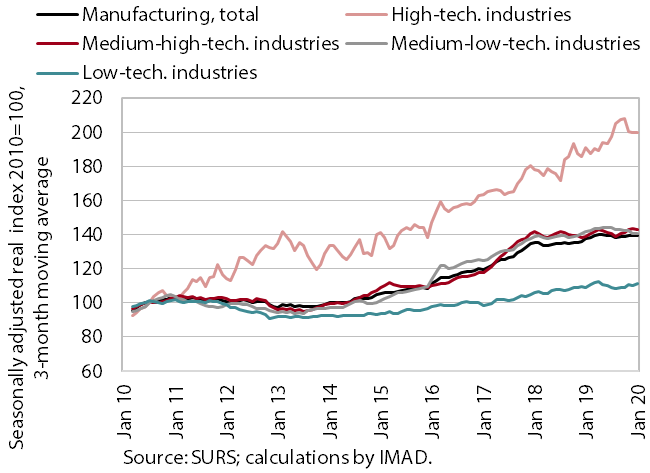

Production volume in manufacturing, January 2020

Production volume in manufacturing increased in January after a decline at the end of the year. For several months it has been hovering close to the level reached at the beginning of last year, with monthly fluctuations. Following a pronounced downswing in the previous two months, production in high-technology industries rose significantly in January. High-technology production is otherwise characterised by significant monthly fluctuations, which are mainly related to the pharmaceutical industry. In January production in other industry categories remained close to the level of the end of last year, but it was mostly higher year on year. Only production volume in medium-low-technology industries, which are highly integrated into global value chains, was similar to that last year, which is related to modest production growth in trading partners during this period.

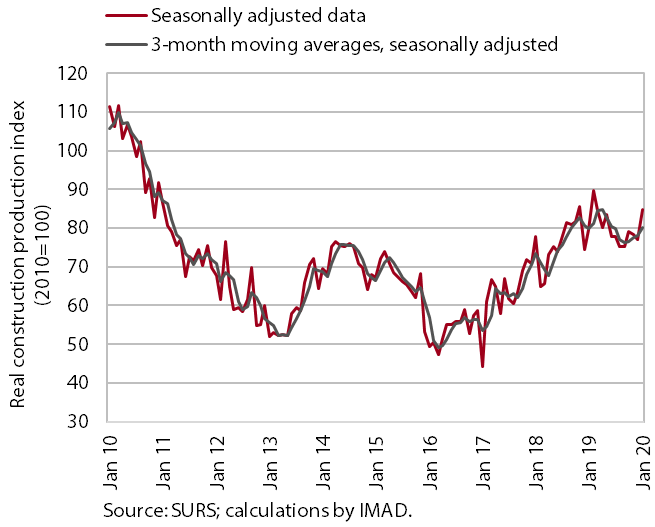

Construction, January 2020

After a decline in the middle of last year, construction activity increased towards the end of last year and intensified further in January. Activity strengthened the most in the construction of residential buildings and also increased in the construction of non-residential buildings and civil-engineering works.

New contracts and the stock of contracts, the indicators of future activity in construction, dropped in the first half of last year before strengthening in the second. Favourable developments also continued in January, when the coronavirus had not yet spread to Europe.

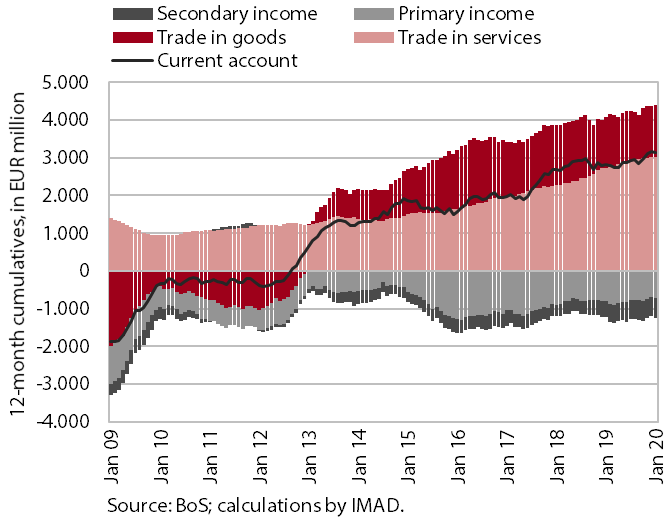

Current account, January 2020

The current account surplus in the 12 months to January was higher year on year, at EUR 3.1 billion (6.3% of estimated GDP). This was still mainly attributable to a higher trade surplus in services, particularly construction, travel and telecommunication, computer and information services. The surplus in goods trade was also higher, reflecting stronger net exports of merchanting. The net outflow of primary income declined, largely due to lower net interest payments on external debt. Meanwhile, the growth of the current account surplus was lowered by a net outflow of secondary income, particularly higher VAT - and GNI-based payments into the EU budget.

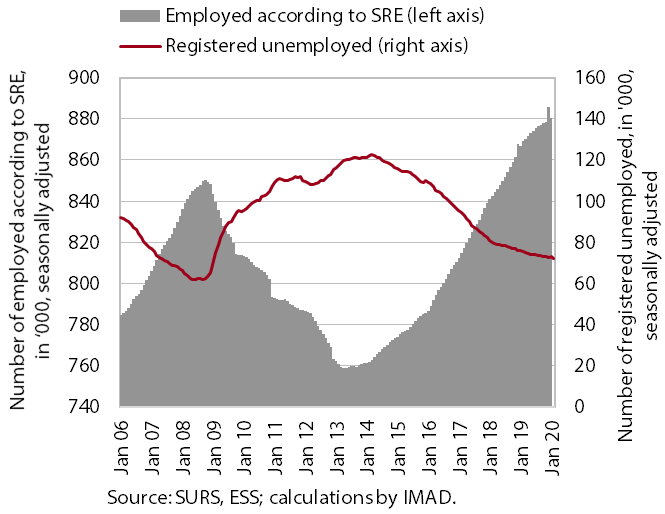

Labour market, January–February 2020

Employment growth slowed at the beginning of the year. In January this year, the number of persons employed increased by1.6% year on year (the most in construction, transportation and storage and accommodation and food service activities), which is almost half less than in the same period of 2019. Demographic change and the shortage of domestic workers continued to support the hiring of foreigners, who contributed three quarters to total employment growth. The number of unemployed persons declined further at the beginning of the year, despite a slowdown in economic activity and the low unemployment rate. At the end of February, it stood at 77,484, which is 4.1% less than in the same period of 2019.

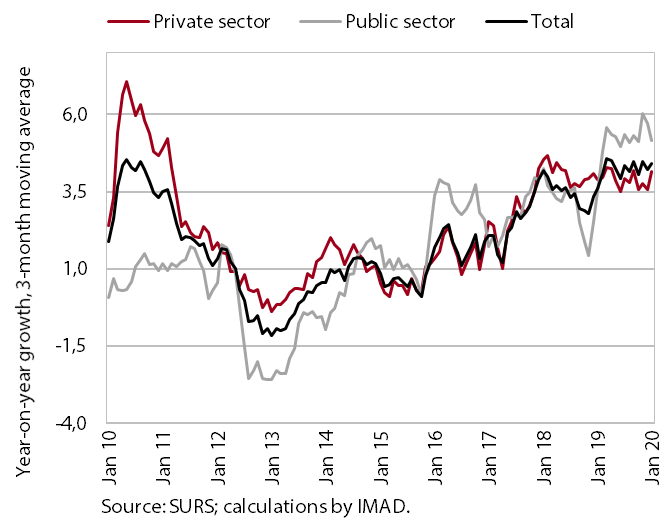

Wages, January 2020

Year-on-year wage growth continued at the beginning of the year. In contrast to last year, this was true particularly for the private sector where, amid relatively low unemployment and labour shortages, growth was also attributable to January’s increase in the minimum wage agreed at the end of 2018. Wages rose the most in activities with a large number of workers with below-average wage (trade, accommodation and food service activities, manufacturing and administrative and support service activities). The increase in the minimum wage also influenced wage growth in the public sector, but this was somewhat lower than last year due to a lower volume of promotions at the end of last year (3.2%; last year 4.9%).