Charts of the Week

Current economic trends from 9 to 13 September 2019: manufacturing production, construction, current account

Manufacturing production remains close to the levels achieved after the surge at the beginning of the year, which is mainly due to the strengthening of production in high-technology industries. Activity also remains high in construction, which is related to increased investment activity of the public and private sectors.

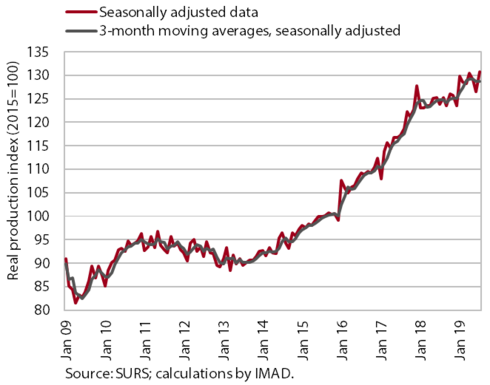

Manufacturing production, July 2019

The volume of production in manufacturing has remained practically unchanged after the increase at the beginning of the year. Production has strengthened particularly in high-technology industries. Amid further growth in the ICT manufacturing sector, growth has also strengthened in the pharmaceutical industry according to our estimate. Production in more export-oriented medium-low- (metal and rubber) and most medium-high-technology industries remains almost unchanged. Production in those medium-low-technology industries that are less dependent on foreign demand, i.e. less integrated in global value chains, is rising (the repair and installation of machinery and equipment and the manufacture of other non-metal mineral products). Low-technology production has dropped somewhat in recent months, after a longer period of steady growth.

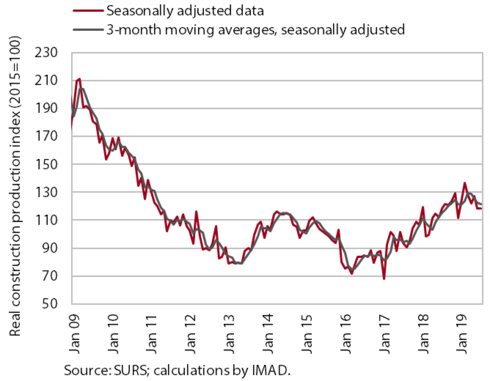

Construction, July 2019

The value of construction output declined in the middle of the year, but remained high. This year’s fluctuations in construction output are related to weather conditions, which were also the reason for the mid-year decline. The relatively high level of activity is attributable both to higher investment on the part of the government, municipalities and infrastructure companies, and to favourable results of the corporate sector and the lack of building in previous years.

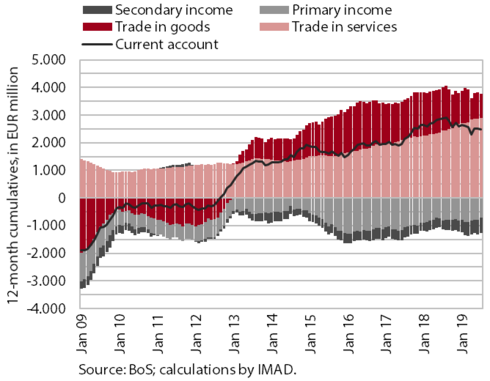

Current account, July 2019

The current account surplus in the last 12 months to July was down year on year, totalling EUR 2.5 billion (5.2 % of estimated GDP). With imports rising faster than exports, the decline was mainly due to the lower surplus of trade in goods. Also, the deficit in secondary income was higher year on year, primarily on account of higher payments into the EU budget (VAT-based and GNI-based contributions). Meanwhile, the surplus in services trade rose further, especially in trade in road transport, travel, and construction services and in research and development services. Moreover, the net outflows of primary income also declined, mainly owing to lower external debt servicing costs.