Charts of the Week

Current economic trends from 6 to 10 April 2020: exports and imports of goods, production volume in manufacturing and Slovenian industrial producer prices

February’s data on production volume in manufacturing and on goods trade do not yet show any noticeable impact of the coronavirus, as it only started to spread in Europe. In the first two months of this year, both production and goods exports and imports recorded a continuation of similarly moderate developments as last year. In March, however, we expect a deterioration in the export-oriented part of the economy due to the impact of the epidemic, as already indicated by the deteriorated March expectations of enterprises regarding exports and production in the next months.

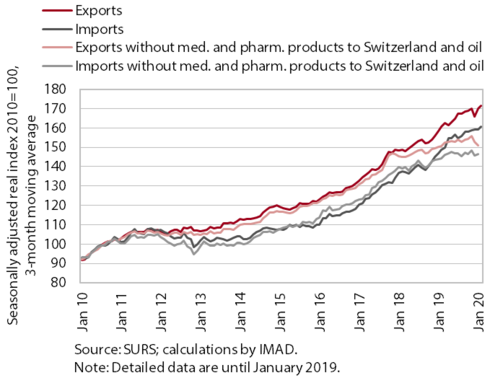

Exports and imports of goods, February 2020

Growth in exports and imports continued to weaken in the first two months of this year. Exports were mainly affected by a slowdown in activity in our main trading partners (Germany, Italy and Austria), which has continued from the end of last year. In February no significant impact of the coronavirus spread in Europe on our exports was yet observed. However, the negative consequences of the coronavirus epidemic already significantly affected export expectations in March. In the first two months imports remained at a similar level to the end of last year. The stronger monthly fluctuations in exports and imports in recent months have been largely related to the distribution of medicinal and pharmaceutical products via Switzerland and, to some extent, to trade in oil and oil products.

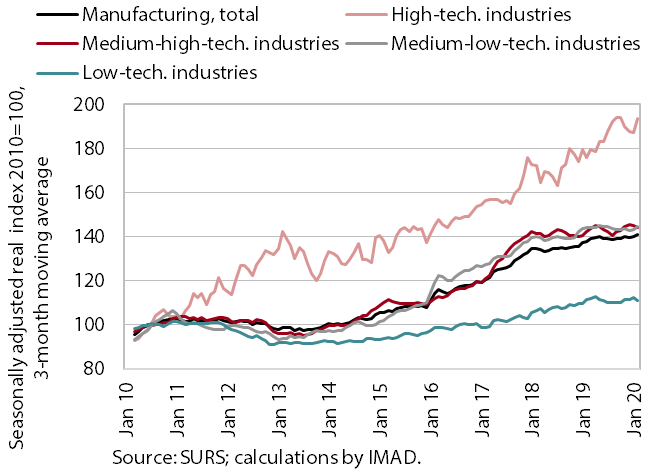

Production volume in manufacturing, February 2020

Manufacturing production volume was still high in February. The main contribution came from high-technology industries, which we estimate will be less affected by the coronavirus spread (particularly the largest, the pharmaceutical industry). In other industries, production remained largely unchanged from previous months.

Business expectations, most of which had not yet deteriorated at the beginning of the year, fell sharply in March (with the coronavirus spread in Slovenia and neighbouring countries and in main trading partners and due to the adoption of containment measures). Owing to lower foreign demand, in March most of the enterprises surveyed expected a decline in production in the following months.

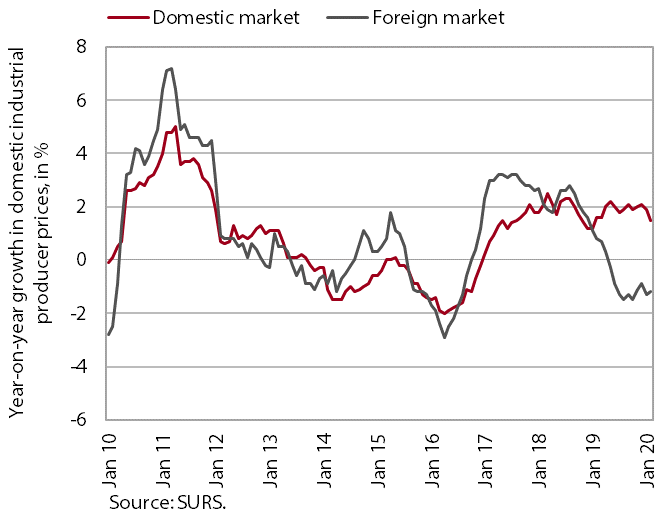

Slovenian industrial producer prices, February 2020

February saw the lowest year-on-year growth in Slovenian industrial producer prices in the last three years (0.1%). Growth moderated on the domestic market, where it was otherwise still relatively high (1.5%). The slowdown was mainly due to somewhat weaker growth in energy prices (9.6%), which, like prices of non-durable consumer goods (3.2%), were still rising at above-average rates. On the domestic market, somewhat higher prices were also recorded for other industrial groups, except for raw materials. Slovenian producer prices on foreign markets remained lower year on year. On euro area markets they were lower, while on non-euro area markets they remained unchanged year on year after nine months of decline.