Charts of the Week

Current economic trends from 29 July to 23 August 2019: manufacturing production, exports and imports of goods, construction, trade and other indicators

Export growth eased somewhat in the second quarter; after first quarter growth, activity remained almost unchanged in most sectors. The moderation of production volume in the majority of main trading partners had the greatest effect on industries integrated into global value chains as suppliers of intermediate goods. Slovenian industrial producer prices on foreign markets are declining owing to the easing of foreign demand. Turnover in the sales of food and non-food products continued to grow amid further growth in household consumption, while the strong turnover growth in the sale of motor vehicles eased. Year-on-year consumer price growth has strengthened somewhat. Growth in household consumption is reflected in higher growth in prices of services and some categories of goods; owing to the impact of weather conditions, higher growth is also recorded for prices of food.

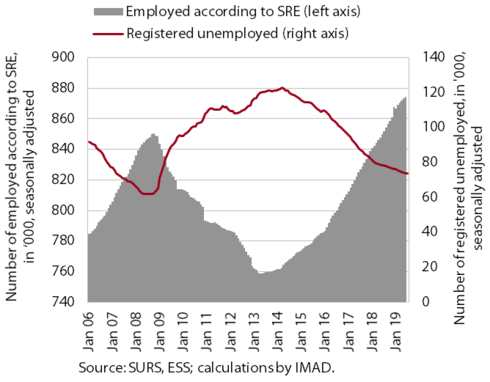

Labour market conditions remain favourable; the hiring of foreign labour continues. Amid the already relatively low level of unemployment, the decline in the number of registered unemployed persons slowed in the middle of the year. The shortage of domestic workers is contributing to wage growth in private sector activities.

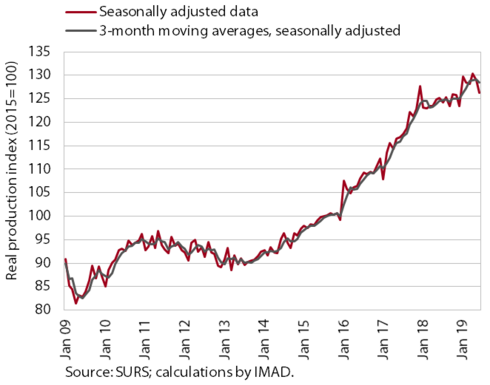

Manufacturing production, June 2019

After the surge at the beginning of the year, manufacturing output maintained its level in the second quarter. Production in high-technology industries increased further. In most other industries it remained almost the same or lower than in the first quarter. Compared with the same period of last year, production growth eased the most in medium-low technology industries, which are integrated in global value chains and were the first to feel the cooling of foreign demand. Particularly the enterprises that produce intermediate goods record lower export orders year on year. Their export expectations have also been deteriorating since the end of the first quarter, as have the expectations of enterprises making investment goods.

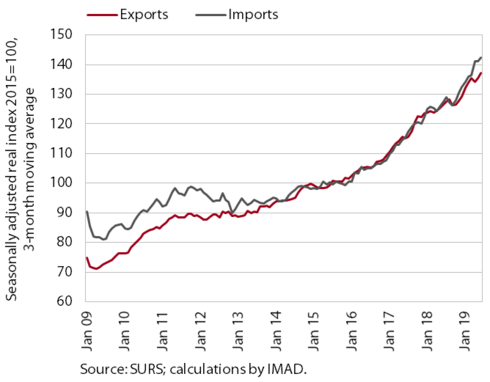

Exports and imports of goods, June 2019

External trade movements remained relatively favourable in the second quarter, despite the more modest growth in Slovenia’s main trading partners. Uncertainty in the international environment was reflected particularly in a decline in export expectations and less so in external trade movements. Imports increased further, while the growth of exports slowed slightly. Year on year, real exports and imports were up 9.6% and 12.8% respectively. Exports were otherwise higher year on year in all main product groups, but their growth was to a great extent related to the increased commercial and distribution activity in medicinal and pharmaceutical products. This, together with the strengthening of private consumption, also contributed to strong growth in consumer goods imports.

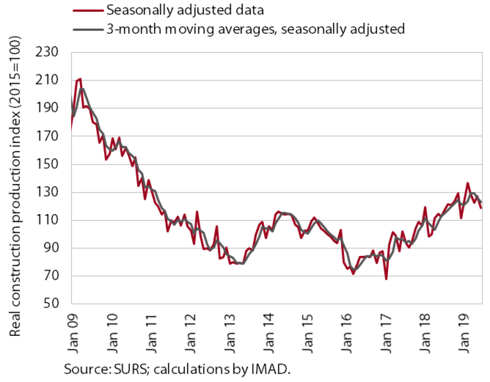

Construction, June 2019

After the strong growth in previous quarters, the value of construction output dropped in the second quarter. Activity declined in all three construction segments (civil-engineering works, residential and non-residential buildings), but remained higher year on year. The higher activity year on year is attributable to increased investments on the part of the government, municipalities and infrastructure companies. In the segment of buildings, it also reflects favourable results of the corporate sector and the lack of building in previous years.

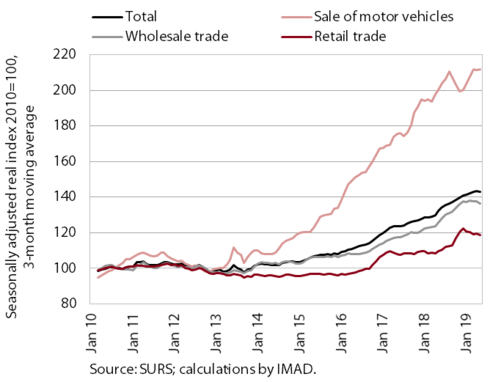

Trade, May 2019

After the increase early in the year, turnover in trade remained roughly unchanged in the spring months. After last year’s acceleration, which had also been partly due to increased sales of pharmaceutical and some energy products, turnover in wholesale trade has been declining in recent months, to some extent as a consequence of more moderate growth in some trade-related activities (transportation, construction, manufacturing). Turnover growth is also slowing in the sale of motor vehicles, after strong growth in the previous four years. In retail trade, otherwise marked by significant fluctuations in the sale of automotive fuels, the sales of non-food and food products have been rising moderately amid further growth in household consumption.

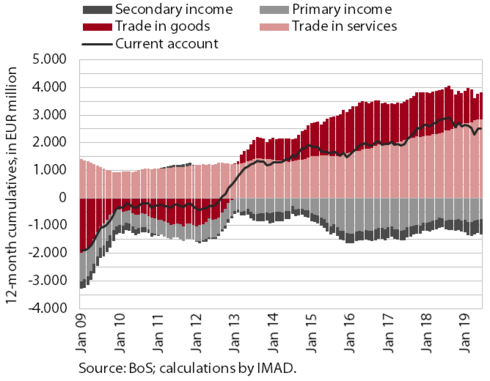

Current account of the balance of payments, June 2019

In the second quarter the surplus of the current account of the balance of payments remained lower year on year. In the last 12 months to June, it totalled EUR 2.5 billion (5.2% of estimated GDP), but this year it is gradually falling. The lower surplus was mainly due to the lower surplus in trade in goods amid faster growth in imports than exports and deteriorated terms of trade. The deficit of secondary income was higher, owing to higher payments into the EU budget. The surplus in services trade increased further, in the second quarter mostly as a result of the surplus in trade in other services and higher revenues from construction works abroad. The deficit of primary income was lower, which is related to lower net outflows of dividends and profits and lower net interest payments on external debt.

Labour market – July 2019

Employment growth remains high amid increased hiring of foreigners. The number of employed persons was up 2.7% in the second quarter (in the first quarter, up 3.2%). It increased the most in construction, transportation, storage and accommodation and food service activities, i.e. activities with a high job vacancy rate. The contribution of foreigners to total employment growth continues to grow. In June it was 71.9%. The falling of the number of registered unemployed persons slowed in the middle of the year, amid the already relatively low level of unemployment. At the end of July, it amounted to 70,747, which is 5.5% less than in the same period of last year.

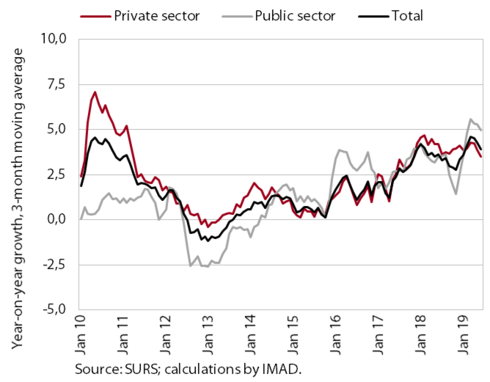

Earnings, June 2019

Year-on-year wage growth in the second quarter (3.9%) was again higher than in the same period of last year (3.6%). In the first half of the year, the year-on-year growth was 4.3%, compared with 3.6% in the same period of last year. The higher growth rate mainly reflects stronger wage growth in the public sector (as a result of the higher valuation of most positions agreed at the end of last year) and promotions. In the private sector, wage growth was – in addition to economic and demographic factors (good business results, labour shortages and thus upward pressure on wages) – also due to the increase in the minimum wage at the beginning of the year. In the second quarter, wage growth was the strongest in accommodation and food service activities, administrative and support service activities, and manufacturing, i.e. the sectors with the greatest labour shortages.

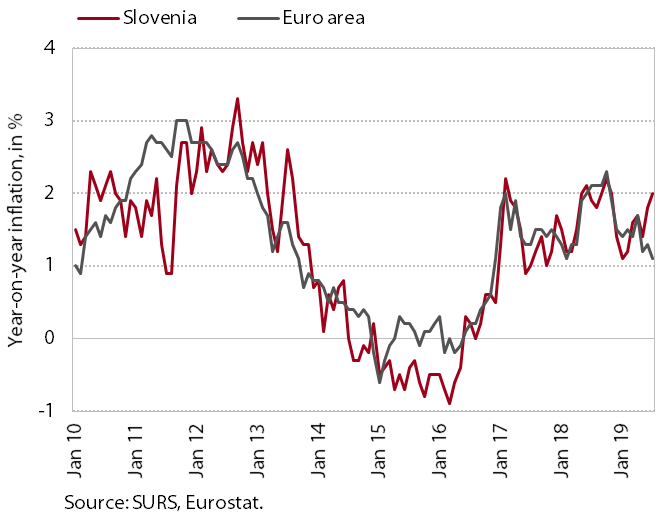

Prices, July 2019

Year-on-year inflation rose slightly in July. The contribution of goods prices to year-on-year growth increased despite lower prices of oil products, which was a consequence of higher growth in prices of fresh food (fruits and vegetables). Owing to the worse weather conditions, these prices have risen considerably in recent months and are almost one tenth higher year on year. Higher prices are also recorded for meat. Solid growth in household consumption is, according to our estimate, contributing to somewhat stronger growth in clothing and footwear prices and to growth in services prices, which remains relatively high (around 3%). Prices of durable goods remained unchanged year on year in July, after falling without interruption for more than ten years.

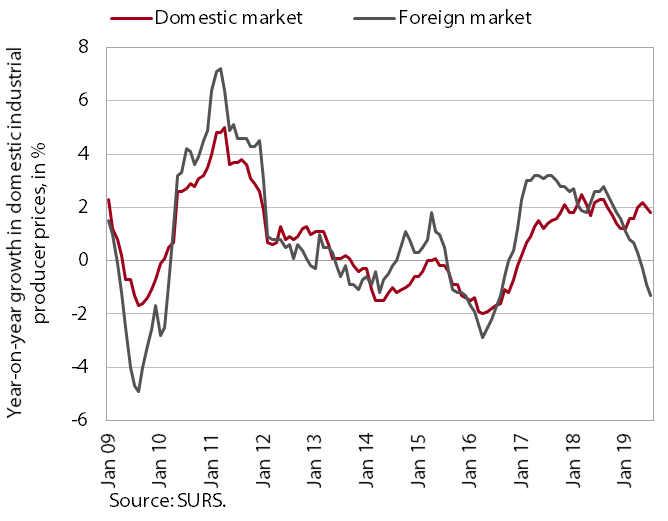

Slovenian industrial producer prices, July 2019

The total year-in-year growth of Slovenian industrial producer prices moderated further in July. The moderation was mainly a consequence of a further fall in prices on foreign markets (for the third consecutive month). Producer prices declined across all product groups, which we estimate is mainly related to the slowdown in foreign demand. Price growth on the domestic market has otherwise dropped slightly, but remains around 2%. This is largely due to strong growth in prices of energy (owing to higher electricity prices), while prices in most other product groups recorded modest growth and prices of durable consumer goods even declined year on year.