Charts of the Week

Current economic trends from 28 March to 1 April 2022: inflation, turnover in trade, turnover in market services and other trends

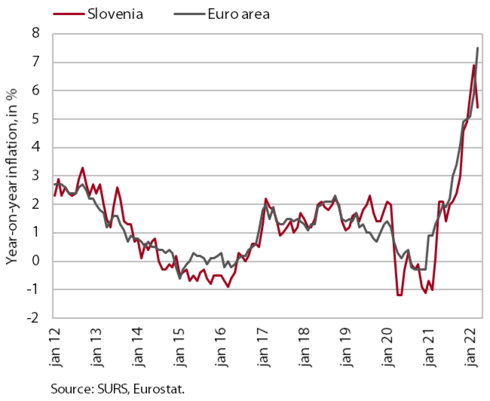

Consumer price inflation moderated slightly to 5.4% year-on-year in March, reflecting a temporary exemption from the payment of certain electricity contributions. Inflation in the euro area rose to 7.5% in March. High price growth and the decision by the ECB to slightly accelerate the scaling back of expansionary monetary policy measures led to higher yields to maturity for euro area government bonds, while the increase in Slovenian government bond spreads over Germany remained moderate. In January, turnover in trade fell compared to the previous month. The monthly dynamics in recent months is mainly due to strong fluctuations in real turnover in the sale of automotive fuels; year-on-year, turnover in trade increased by more than a fifth. In January, turnover was higher year-on-year in all market services, and compared to the same period before the epidemic, it was significantly lower only in travel agencies, motion picture activities, rental and leasing activities and food and beverage service activities.

Inflation, March 2022

After a sharp increase at the beginning of this year, consumer price inflation eased slightly to 5.4% year-on-year in March. The lower inflation was mainly due to the passing of the Act on Intervention Measures to Mitigate the Consequences of High Energy Prices, which allowed for a temporary exemption from the payment of certain contributions, leading to a significant decrease in electricity prices (by 38.6% month-on-month and 29.8% year-on-year). The reintroduction of administered fuel prices also somewhat slowed the rise in petroleum product prices, which were nevertheless more than a quarter higher year-on-year. As the prices for package holidays fell significantly due to seasonal factors, the increase in service prices was also lower year-on-year. Prices for semi-durable goods remained at around 4.5% year-on-year, while growth in durable goods prices remained high (8.8%), Given the geopolitical tensions, cost pressures are intensifying due to high prices for energy and inputs, leading to an increase in food prices. These were almost 7% higher year-on-year in March, which is the highest increase since 2008.

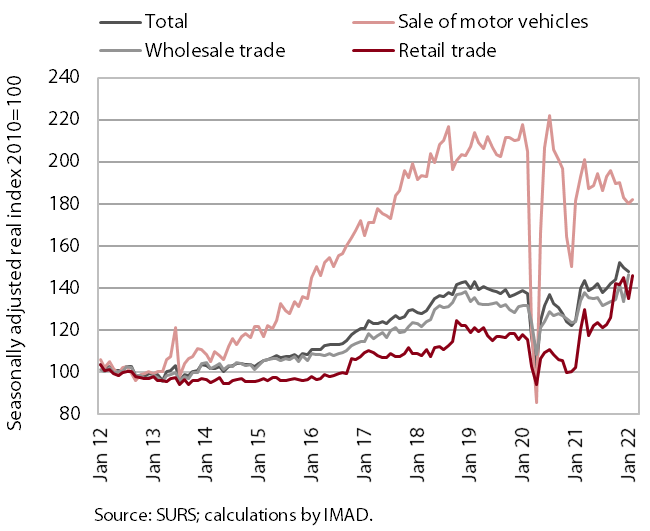

Turnover in trade, January–February 2022

Turnover in trade fell in January from the previous month but was more than a fifth higher year-on-year, partly due to the low base. The monthly decline was mainly the result of a sharp fall in retail trade, the dynamics of which have been determined by strong fluctuations in real turnover in the sale of automotive fuels in recent months. After high growth in December, it fell sharply in January but picked up again in February, according to preliminary data. Turnover in the sale of motor vehicles further decreased slightly in January. Due to delays in vehicle deliveries, this was the only main segment to fall short of pre-epidemic turnover. However, after a significant decline in the previous month, growth of turnover in wholesale trade gained momentum.

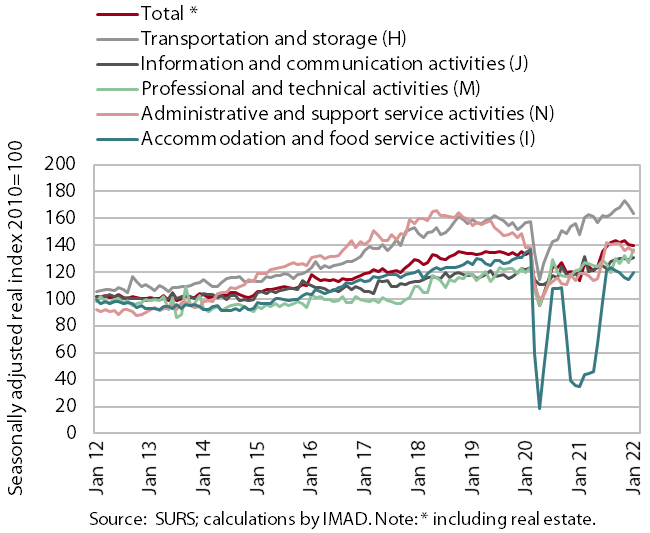

Turnover in market services, January 2022

Compared to the previous month, real turnover increased again in most market services in January. Given the renewed strong growth in architectural and engineering services, the highest increase in turnover in current terms was observed in professional and technical activities. It increased again in accommodation and food service activities and was higher in information and communication activities due to higher turnover in computer and telecommunication services. Turnover in transportation and storage has been declining for the last two months, with the largest decline in land transport and support transportation activities. Since November 2021, it has also mostly declined in administrative and support service activities, due to lower income in all segments except employment services. Compared to the previous month, total real turnover fell slightly (by 0.7%), but was 25% higher year-on-year due to the low base last year. In January, turnover was higher year-on-year in all market services, while compared to the same period in 2020, it was still significantly lower in travel agencies (by 60%) and in motion picture activities, rental and leasing activities and food and beverage service activities (by 23% on average).

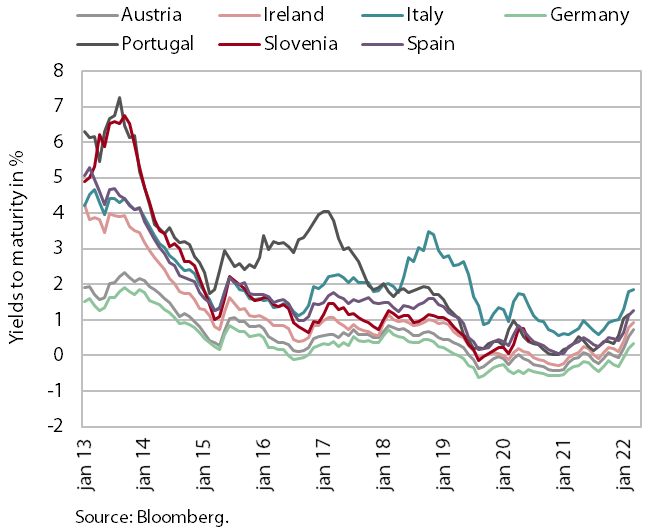

Bond, Q1 2022

Yields to maturity of euro area government bonds rose significantly in the first quarter. The higher yield was influenced by the further rise in inflation in the euro area and the decision by the ECB to slightly accelerate the scaling back of expansionary monetary policy measures. The yield to maturity of the Slovenian 10-year government bond was 0.81% in the first quarter, the highest figure in the last three years. The spread to the German bond was 65 basis points, about 15 basis points higher than in the previous quarter, which is slightly above the pre-epidemic period.

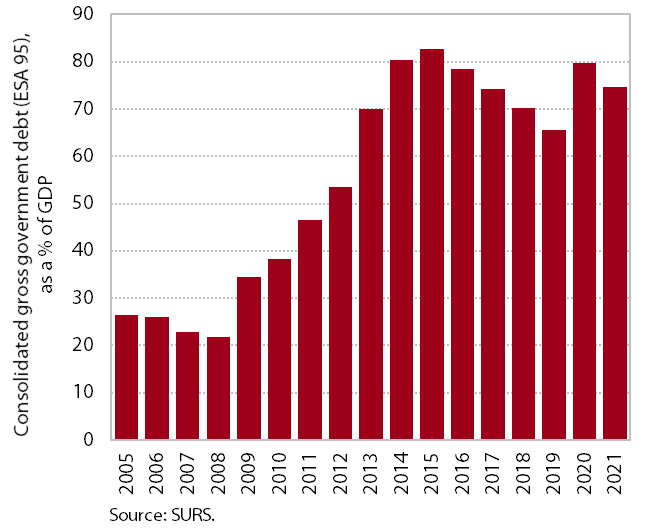

General government deficit and debt in 2021, April EDP reporting

The general government’s fiscal position improved in 2021 amid a rapid economic recovery and lower expenditure on measures to mitigate the impact of the epidemic. The deficit and public debt decreased slightly (from 7.8% to 5.2% of GDP and from 79.8% to 74.7% of GDP respectively), the latter also being affected by the decline in the country's cash reserves, which still remain high. IMAD estimates that expenditure on measures to mitigate the impact of the epidemic has fallen from 5.2% of GDP in 2020 to 4.5% of GDP. In contrast to lower expenditure on measures to mitigate the impact of the epidemic, growth in other expenditure increased in 2021. This was due to stronger investment growth as part of a broader European response to support the recovery, as well as other expenditure, some of which is of a permanent nature.