Charts of the Week

Current economic trends from 26 to 30 August 2019: GDP, labour market, trade, market services and other indicators

GDP growth slowed in the second quarter with the moderation of international trade, while growth in domestic consumption remained somewhat higher than in previous quarters. Employment growth also eased off, while unemployment was the lowest in twenty years. Expectations of businesses in manufacturing are deteriorating, especially with regard to export demand. The prospects for market service activities and retail trade remain favourable, partly owing to growth in private consumption. With rising household consumption, household borrowing remains high. Year-on-year growth in consumer prices also rose further in August.

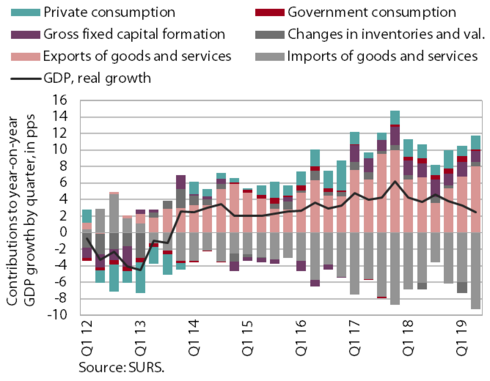

GDP, Q2 2019

Real GDP in the second quarter was 2.5% higher year on year. The main contribution to growth – which slowed relative to previous quarters – came from domestic consumption. Household consumption picked up somewhat. A further increase was also recorded for investment, particularly construction investment. The growth of total exports increased further amid strong support of accelerated growth in exports of pharmaceutical and medicinal products. Imports of these products strengthened as well, which, together with higher growth in domestic consumption, contributed to faster growth in total imports. The contribution of net exports to GDP growth thus turned negative.

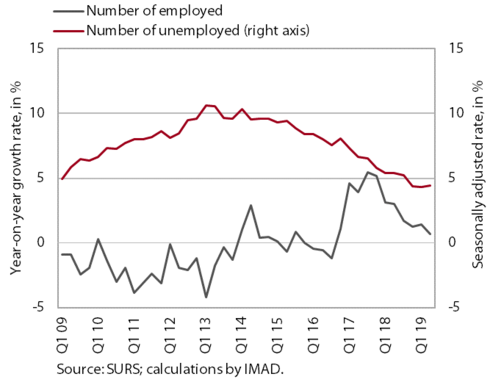

Labour market, active and non-active population, Q2 2019

Growth in employment slowed, while unemployment was the lowest on record. In the second quarter the number of persons in formal employment increased further. With the moderation of economic growth, its growth slowed, while in other employment forms the number of employed persons fell. The survey-based unemployment remains low, in terms of both number and rate, but the share of the long-term unemployed is still high.

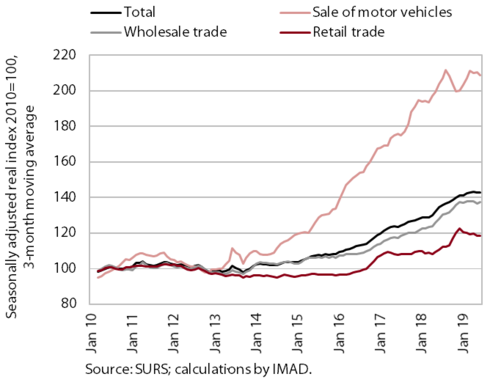

Trade, June 2019

After increasing early in the year, turnover in trade remained roughly unchanged in the second quarter. In retail trade, otherwise marked by significant fluctuations in the sale of automotive fuels, the sales of non-food and food products have been rising moderately amid further growth in household consumption. Turnover in wholesale trade remained at the level seen at the end of last year, partly as a consequence of more moderate activity growth in some trade-related sectors (transportation, construction and manufacturing). Meanwhile, turnover in the sale of motor vehicles has been slowing in recent months, after strong growth rates in the previous four years.

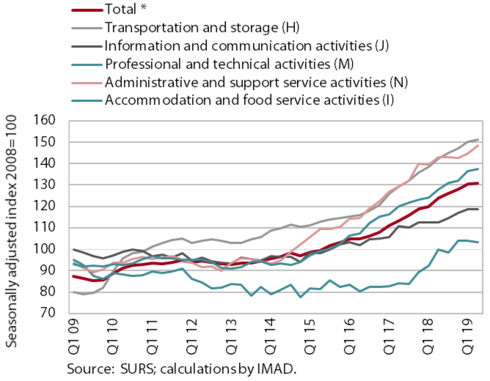

Market services, June 2019

Turnover growth in market services eased off in the second quarter. After a period of considerable growth, a moderation of growth was recorded in accommodation and food service activities (owing to a smaller number of tourist overnight stays because of bad weather in May) and transportation, where exports of road transport services are on the rise. Turnover in information and communication activities remained unchanged; amid a significant strengthening in computer services, its growth is hampered by a decline in telecommunications services. Turnover was also down in professional and technical activities, chiefly owing to May’s significant decline in architectural and engineering services. Turnover growth in administrative and support service activities remains high, this year under the impact of growth in services that businesses tend to outsource to external providers.

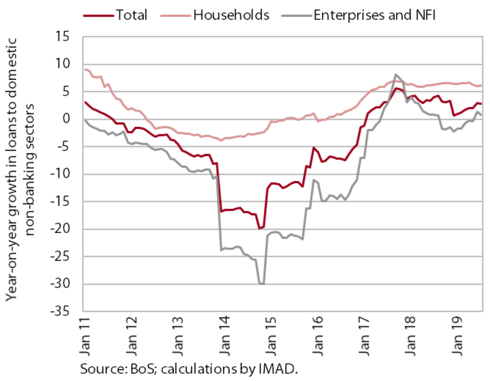

Financial markets, July 2019

The gradual growth of the banking system’s total assets continues. The somewhat higher year-on-year loan growth during the summer months is, according to our estimate, largely due to lower corporate and NFI deleveraging, as the volume of new loans remains modest. Amid rising consumption, household borrowing remains relatively high. Among sources of liabilities, overnight deposits continue to rise at the fastest pace, given the near-zero interest rates, and represent almost half of the banking system’s liabilities. Following the intense deleveraging since the onset of the international financial crisis, liabilities to foreign banks have also increased somewhat in recent months, but their share is still low (below 5%).

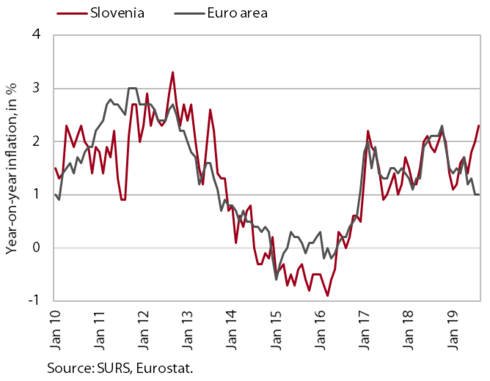

Prices, August 2019

Year-on-year consumer price growth rose somewhat again in August. The increase was to a great extent a consequence of significantly higher clothing prices, which rose more and earlier month on month than in previous years. With rising household consumption and unit labour costs, prices of other non-energy industrial goods have also recorded stronger growth in recent months. Prices of durable goods were thus somewhat higher year on year in August (0.2%) after more than ten years of uninterrupted decline. Price growth in services continues to hover at around 3%. The contribution of food prices to total inflation remains around 0.5 pps.

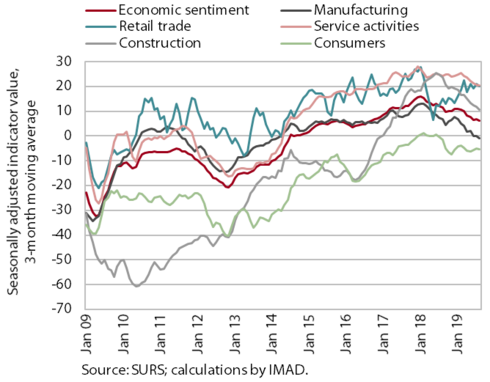

Economic sentiment indicator, August 2019

Economic sentiment has deteriorated since the beginning of the year; the prospects for service activities and retail trade are still favourable. Confidence in manufacturing and construction has been dropping from the peak reached in the beginning and middle of 2018. While being still relatively high in construction, it fell below the long-term average in manufacturing, mainly due to deteriorated expectations in the export-part of the economy. Confidence in service activities has also dropped somewhat in the recent period, but remains relatively high. Confidence in retail trade is also still high, with monthly fluctuations. Consumer confidence remains more or less unchanged, after worsening in the second half of last year.