Charts of the Week

Current Economic Trends from 25 to 29 March 2019: turnover in trade, nominal turnover in market services, prices, economic sentiment and other indicators

At the beginning of the year turnover growth continued in most market services. It was mainly driven by stronger private consumption, which also affected the growth of consumer prices. Households continued to borrow in the form of consumer and housing loans. Real estate sales declined last year after several years of growth, while real estate prices continued to rise.

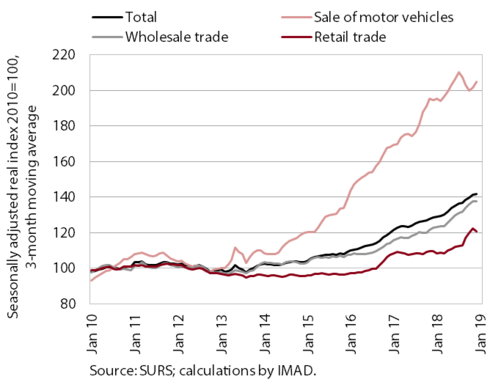

Turnover in trade, January 2019

Turnover in trade continued to rise at a moderate pace at the beginning of the year. Last year’s turnover growth in wholesale trade was affected not only by stronger domestic consumption, but also vigorous trade in some primary goods. Since the end of last year, motor vehicle sales have also been picking up, following a considerable decline after September’s introduction of the new global standard for measuring fuel consumption and emissions. In retail trade – which is otherwise marked by significant fluctuations in the sales of automotive fuels – the sales of non-food products are still on the rise, boosted by further growth in household consumption, while the sales of food, beverages and tobacco products continue to stagnate.

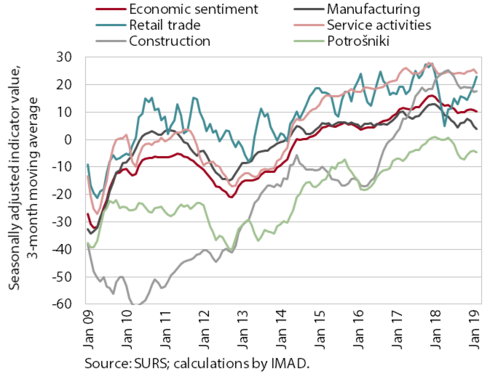

Economic sentiment indicator, March 2019

Economic sentiment has not changed much since the middle of last year. At the beginning of the year, confidence remained basically unchanged in most sectors and also among consumers. A significant increase was recorded only for retail trade, where sales expectations were also up owing to higher sales. Confidence in manufacturing dropped again. Amid slower growth in foreign demand, manufacturing firms are faced with lower export orders and their expectations about future orders are deteriorating.

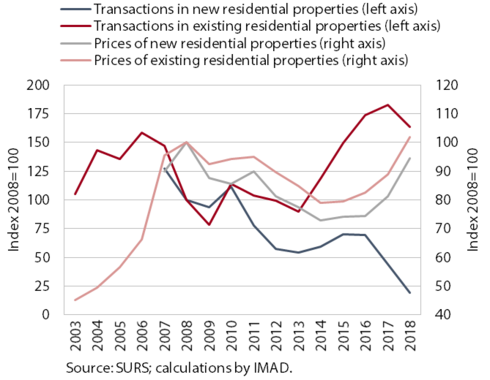

Real estate, 4th quarter of 2018

The growth of average dwelling prices accelerated further in 2018, while the number of dwelling transactions moderated after increasing strongly in previous years. On average, prices were up 15.1% year on year. Prices for all residential property categories went up. The average price of existing flats, which account for 70% of all transactions, rose by around one tenth for the second consecutive year. Prices of existing family houses otherwise rose the most (by one fifth), this being the only category (alongside new family houses) where prices still lag behind the average price from 2008. With limited supply, the number of transactions in new flats dropped the most again in 2018 and accounted for only one tenth of the highest number in 2007. The number of transactions in existing flats also dropped last year for the first time after four years of strong growth, but remained relatively high.

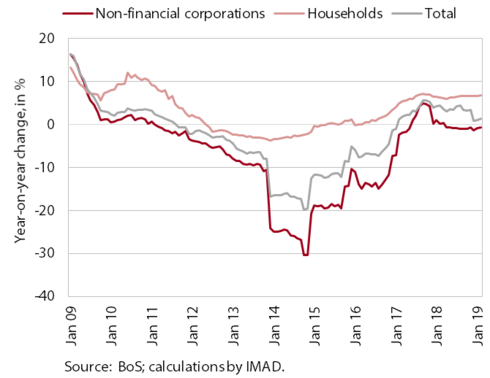

Financial markets, February 2019

The situation in the banking system remains stable; the volume of loans to domestic non-banking sectors continues to strengthen steadily; the quality of banks’ assets is improving. Year-on-year growth in the volume of loans to domestic non-banking sectors continues to arise from household borrowing in the form of consumer and housing loans. The year-on-year fall in the volume of loans to domestic non-financial corporations is gradually easing, which is a consequence of slightly more pronounced net borrowing early in the year. Besides on bank loans, firms are also relying on other sources for financing current operations and investment. The quality of banks’ assets keeps improving. In 2018 the share of arrears of more than 90 days dropped by more than one third, to 2.3%. We estimate that this is a consequence of a gradual repayment of bad claims and better credit ratings of individual borrowers amid good business results.

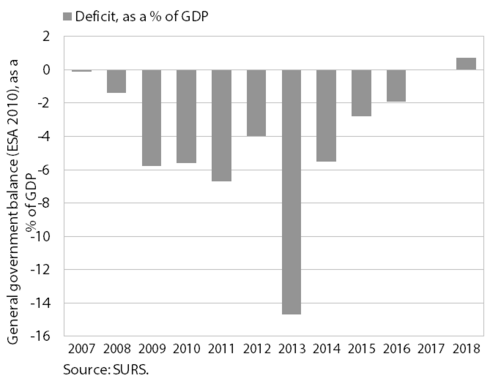

General government balance (ESA 2010), 2018

The public finance position continued to improve in 2018. In 2017 it was balanced, while in 2018 revenue exceeded expenditure by EUR 303 million (0.7% of GDP). The steady improvement in Slovenia's balance since 2013, when the general government deficit was at its highest, is a consequence of stabilisation measures, improved economic conditions and measures for increasing revenue and containing expenditure. In the last two years, the decline in flexible expenditure, particularly investment, came to a halt. Investment increased strongly last year (24.8%), partly also as a result of faster implementation of projects financed from EU funds.

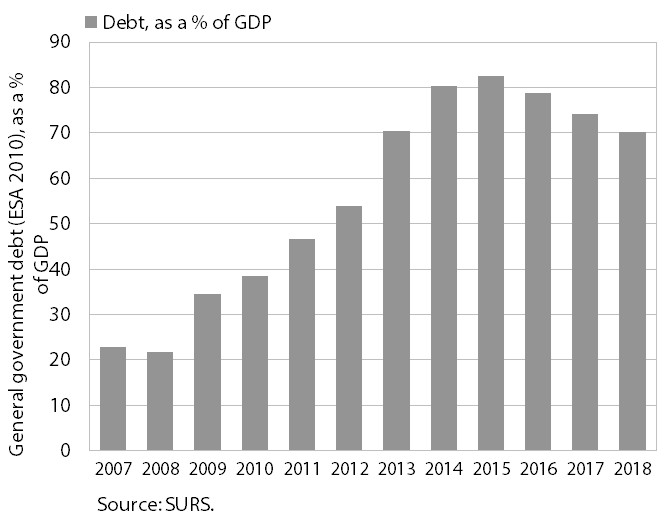

Consolidated general government debt (ESA 2010), 2018

The improvement in the general government balance in the circumstances of strong economic growth has led to a rapid decline in the general government debt as a share of GDP in recent years. The rising of Slovenia’s indebtedness after 2008, which was one of the highest in the EU amid double-dip recession and a longstanding persistence of high general government deficits and due to one-off factors, came to a stop in 2015 (at 82.6% of GDP). Since then the debt-to-GDP ratio has been rapidly falling, also when compared with other countries and faster than required by the Stability and Growth Pact. In 2018 it totalled 70.1% of GDP. The decline in the debt-to-GDP ratio took place under the impact of an improvement in the primary balance (surplus); the contribution of economic growth was also positive – in the last three years it has exceeded the counter-effect of interest expenditure, which is also declining.