Charts of the Week

Current economic trends from 23 to 27 September 2019: exports and imports of goods, market services, economic sentiment indicator and housing price indices

The volume of external trade increased somewhat further at the beginning of the third quarter. The strong growth in goods exports and imports is largely related to higher trade and distribution activity in medicinal and pharmaceutical products, according to our estimate. Economic sentiment in Slovenia has not changed significantly after a decline at the beginning of the year and remains above the long-term average. Prospects remain favourable particularly in market services, where turnover growth continued at the beginning of the third quarter in most activities. Export expectations, on the other hand, are declining. Property prices continue to rise, particularly the prices of existing flats; the number of transactions in existing flats also rose.

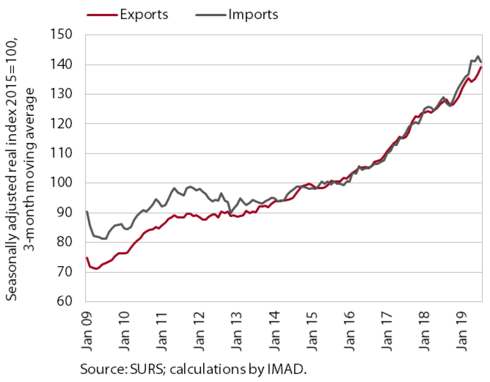

Exports and imports of goods, July 2019

The volume of external trade increased at the beginning of the third quarter. In the seven months to July, real goods exports were up 9.4% year on year, their growth being mainly driven by exports of medicinal and pharmaceutical products. The growth of exports of other main manufactured goods was significantly lower, which is related to cooling growth in Slovenia’s main trading partners, particularly Germany. Import growth remains high, driven by factors similar to those in exports.

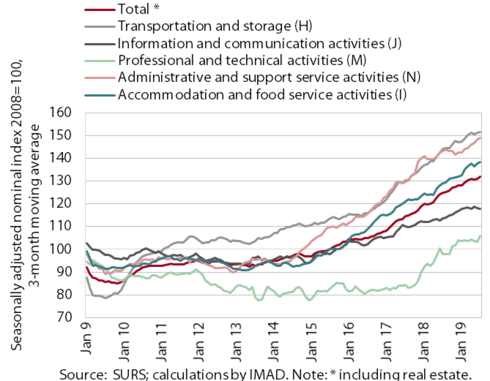

Market services, July 2019

At the beginning of the third quarter, turnover growth continued across most market services. In professional and technical activities, turnover strengthened on account of July’s considerable growth in architectural and engineering services. Turnover growth continued in transportation (amid slower growth in exports of road transport services). With rising turnover in services that businesses tend to outsource to external providers, the growth of turnover in administrative and support service activities remained high. Turnover in ICT activities has stagnated since the beginning of the year, its growth being impeded by a decline in telecommunication services, amid a significant strengthening in computer services. Meanwhile, turnover growth eased in accommodation and foods service activities, largely owing to a decline in the number of tourist overnight stays.

Economic sentiment indicator, September 2019

Economic sentiment has not changed significantly after a decline at the beginning of the year and remains above the long-term average. Prospects for retail trade and service activities remain favourable. The outlook for manufacturing remains unchanged. Business expectations about production and exports have stayed at the achieved levels, while expectations about orders, particularly export orders, have declined with slowing growth in the international environment. Confidence in construction and among consumers has worsened slightly in recent months.

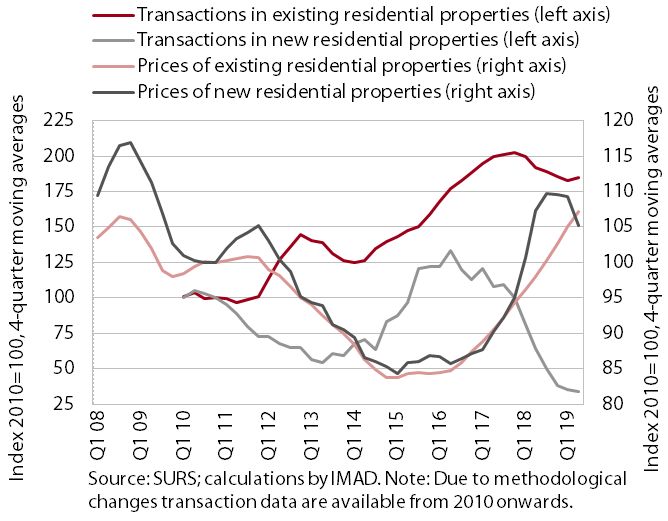

Housing price indices, Slovenia, Q2 2019

The average residential property prices increased further in the second quarter; the number of transactions also rose after a decline in the previous year. Prices were up 5.8% year on year. Their growth arose from the increased number of transactions and a rise in the prices of existing dwellings (8.3%). Among these, the prices of existing family houses rose the most, but they remained below their pre-crisis levels. The average price of existing flats in Ljubljana, having grown at above-average rates in the previous four years, remained the same as one year before, while prices in the rest of Slovenia increased more notably. The average price of new residential properties, which accounted for only 2% of all transactions, was more than a tenth lower than one year before, when it had risen strongly (by more than a quarter).