Charts of the Week

Current economic trends from 23 to 27 May 2022: economic sentiment, turnover in trade and wages

After a sharp decline in March and a temporary increase in April, economic sentiment deteriorated in May, most notably among consumers, in manufacturing and, to a lesser extent, in retail trade. Turnover in trade increased in most sectors in the first quarter and the lifting of the recovered/vaccinated/tested rule is also estimated to have contributed to the positive developments in the retail trade in non-food products, apart from the low base last year. Year-on-year growth in average gross wages in the private sector remains relatively high, which we estimate may already be affected by labour shortages in some sectors (accommodation and food service activities, transportation and storage and construction). The level of public sector wages has remained below the relatively high level of the previous year since November last year, which is related to the payment of COVID-19-related allowances.

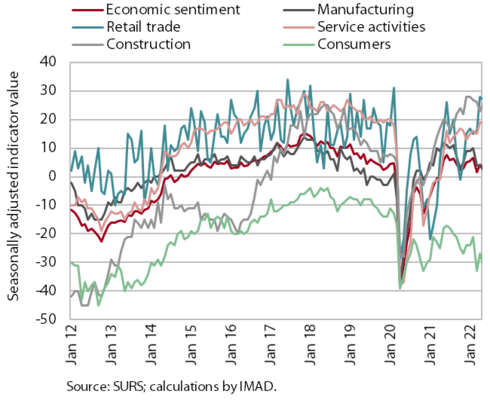

Economic sentiment, May 2022

The value of the economic sentiment indicator has been mostly declining since March and was lower in May among consumers and in manufacturing than a year ago. After a sharp decline in March and a temporary increase in April, the value of the sentiment indicator decreased by 1.4 p.p. in May but remained above the long-term average. On a monthly basis, confidence deteriorated most notably among consumers (by 4 p.p.), in manufacturing (by 2 p.p.) and slightly also in retail trade (by 1 p.p.). In the services sector, it remained at the previous month’s level, while in construction it was noticeably higher (by 3 p.p.). Confidence was significantly higher year-on-year in retail trade and in services (both by 10 p.p.) and in construction (by 6 p.p.). It was slightly lower year-on-year among consumers and in manufacturing (by 13 and 10 p.p. respectively). Lower confidence among consumers is related to rising prices and uncertainty about further price increases and the resulting deterioration in household purchasing power, while lower confidence in manufacturing is related to the current situation in the international environment (bottlenecks in the supply of raw materials, rising commodity and energy prices and the Russian-Ukrainian war).

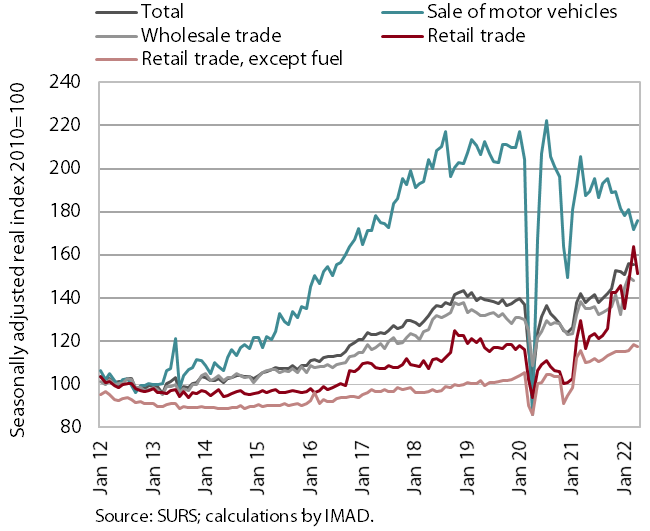

Turnover in trade, March–April 2022

In the first quarter, turnover in trade increased in most sectors. Growth was the highest in wholesale trade, where turnover increased after a sharp decline in December. Compared to the last quarter of 2021, turnover was also higher in retail trade, whose dynamics in recent months has been determined by sharp fluctuations in real turnover from the sale of automotive fuels. With the lifting of the recovered/vaccinated/tested rule, the sales of non-food products also increased, up 14% year-on-year given the low base last year. Sales of food, beverages and tobacco products was slightly lower than a year ago, stagnating in recent months but falling significantly in April, according to preliminary data. Turnover in the sale of motor vehicles fell for the second quarter in a row and was down 8% year-on-year. According to preliminary data, turnover increased slightly in April but still remained low.

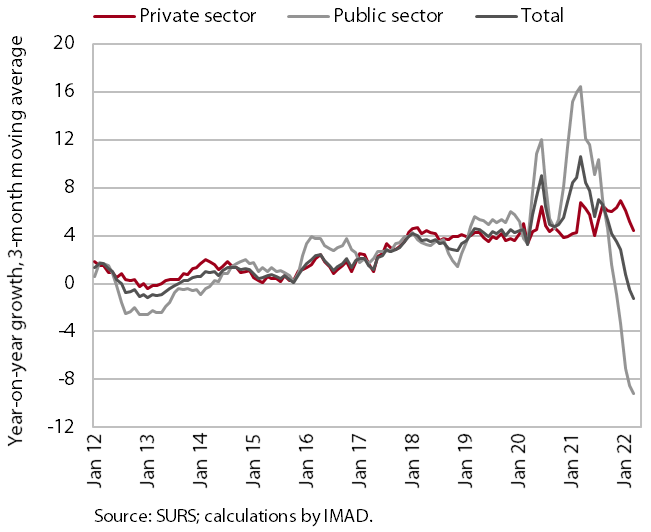

Wages, March 2022

In March, average wages in the public sector were 8.3% lower year-on-year, while they were 5.6% higher in the private sector (-0.1% overall). Due to the cessation of COVID-19-related allowances, year-on-year wage growth in the public sector slowed significantly in the second half of last year and turned negative year-on-year last November. In the private sector, year-on-year growth strengthened in March due to higher extraordinary payments. Wage growth was the highest in accommodation and food service activities and it was also high in transportation and storage and in construction. In all these activities, this could already be the consequence of labour shortages.