Charts of the Week

Current economic trends from 22 to 26 August 2022: average gross wage per employee, value of fiscally verified invoices and economic sentiment

In June, the average gross wage fell again year-on-year in real terms, more markedly in the public sector, where the high base effect of last year is fading. In the second and third week of August, the year-on-year nominal growth of the value of fiscally verified invoices slowed down, amid one less working day and a high base from last year. The value of the economic sentiment indicator rose slightly month-on-month in August but remained lower year-on-year for the fourth month in a row.

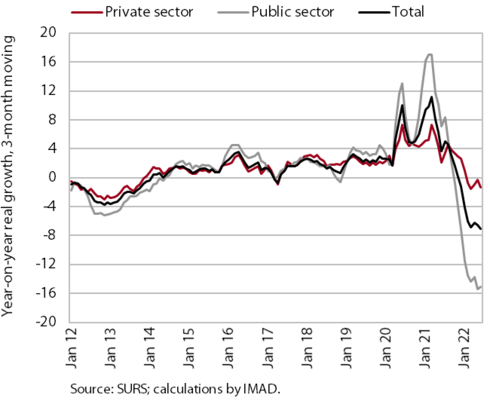

Average gross wage per employee, June 2022

Under the impact of high inflation, average wages in both the public and private sectors fell year-on-year in real terms in June (by 12.3% and 3.1% respectively; 6.8% overall). The year-on-year real growth of public sector wages has been markedly negative since November last year. This is related to the payment of bonuses during the declared epidemic, whose impact in the form of a high year-on-year base faded by mid-June this year. In the private sector, the year-on-year decline was larger than in the previous month.

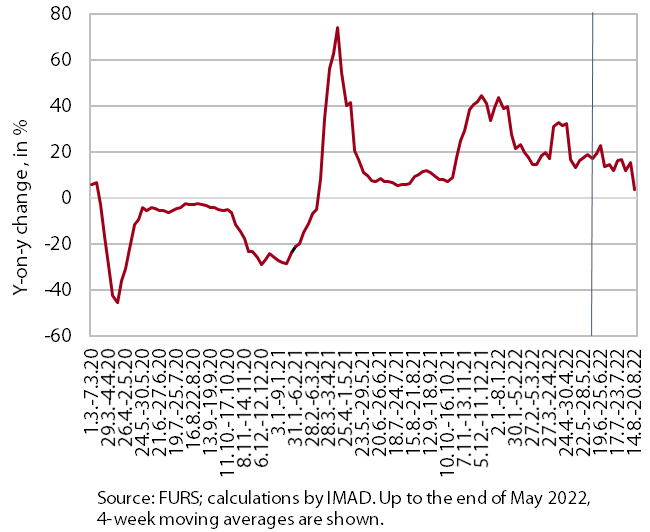

Value of fiscally verified invoices – in nominal terms, 7–20 August 2022

Amid high price growth, the value of fiscally verified invoices between 7 and 20 August was 9% higher year-on-year in nominal terms and 20% higher than in the same period of 2019. The year-on-year increase was significantly lower than in the previous two weeks, partly due to one less working day this year and rising last year’s base in some sectors. Growth of turnover in trade thus fell to 9% (from 14%). Growth in retail and wholesale trade was lower and the decline of growth in the sale of motor vehicles intensified further. Year-on-year growth in accommodation and food service activities halved to 8% as the number of overnight stays by tourists last August exceeded the results from the same month of 2019 for the first time since the epidemic began.

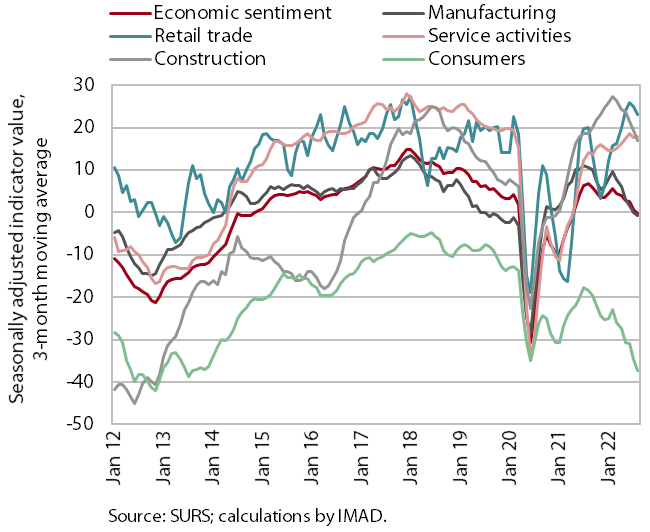

Economic sentiment, August 2022

After a three-month decline, the value of the sentiment indicator rose slightly in August, although it remained negative. It has also been lower year-on-year since May. Compared to July, confidence rose in services and construction and fell in retail trade, while it remained unchanged among consumers and in manufacturing. The confidence indicator thus remained well below the long-term average among consumers and slightly below it also in manufacturing. The lower confidence among consumers is related to the weakening of household purchasing power due to rising prices, especially for energy and food, while in manufacturing it is related to the current conditions in the international environment (bottlenecks in the supply of raw materials, rising prices for raw materials and energy).