Charts of the Week

Current economic trends from 21 to 25 September 2020: electricity consumption, traffic of electronically tolled vehicles, economic sentiment, real estate, market services, Slovenian industrial producer prices

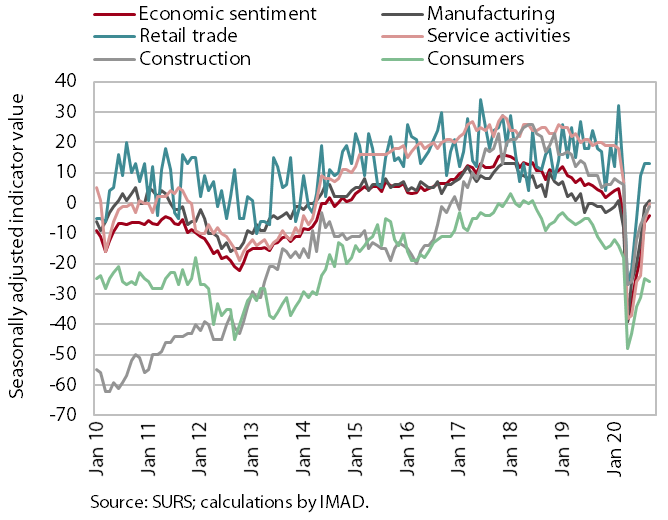

Economic sentiment improved in September for the fifth consecutive month but remained lower than at the beginning of the year.

Electricity consumption was comparable to that in the same period of last year for the second week in a row, while freight traffic was around a tenth lower year on year.

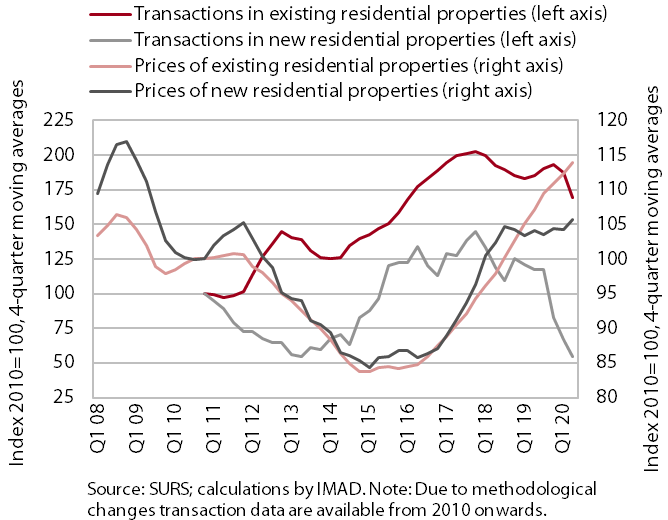

In the second quarter, dwelling prices continued to increase, but this year their growth is somewhat more modest than in previous years. The number of dwelling transactions declined further, mostly as a result of restrictions on business activity due to the epidemic.

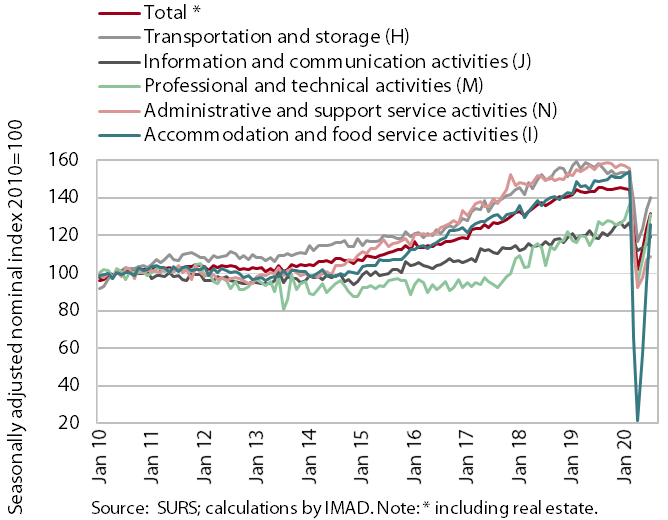

In July, turnover in all market services increased for the third consecutive month, the most in accommodation and food service activities, which is partly due to the introduction of tourism vouchers.

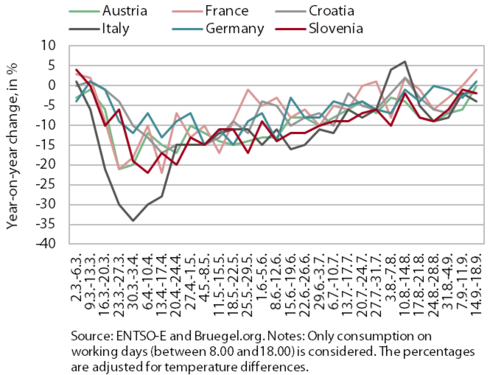

Electricity consumption, September 2020

Weekly electricity consumption in the third week of September was very close to last year’s level, as in the preceding week. Year on year, it was down 2% (one week before, 1%). Among Slovenia’s main trading partners, Croatia recorded the same decline, while the decline in Italy was larger (4%). In Austria, in the third week of September electricity consumption reached the level of the same period last year, for the first time since the outbreak of the epidemic in March. In other EU countries, consumption was higher than last year, in Germany by 1% and in France by 4%.

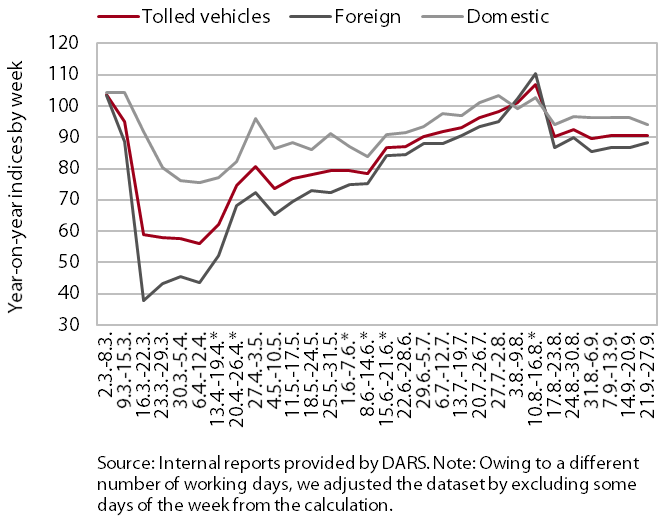

Traffic of electronically tolled vehicles on Slovenian motorways, September 2020

As in several previous weeks, freight traffic on Slovenian motorways was around a tenth lower in mid-September than before the epidemic. After falling sharply with the declaration of the epidemic, it has increased more strongly since the middle of June. In mid-August, it was already higher year on year (adjusted for the holiday effect). Then it fell again and lagged 9% behind the comparable last year’s level in the third week of September. The number of kilometres travelled by foreign hauliers fell more than that travelled by domestic ones (by 13% and 4% year on year respectively).

Economic sentiment, September 2020

Economic sentiment improved somewhat again in September but remained lower than at the beginning of the year. The sentiment indicator improved for the fifth consecutive month but was still lower year on year (difference: -8.7 p.p.); the year-on-year difference has narrowed considerably since April, when the decline was largest (-46.1 p.p.). Relative to the previous month, confidence indicators in service activities and construction improved the most. Only consumer confidence indicator deteriorated.

Real estate, Q2 2020

Dwelling prices increased again in the second quarter, while the number of transactions declined further, mainly due to restrictions on business activity during the epidemic. Prices were up 5.2% year on year, indicating a moderation with regard to price rises in the last three years (almost 8% average annual growth). This year’s increase was mainly due to higher prices of existing dwellings, the sales of which were otherwise the lowest since the first quarter of 2014 amid the conditions of the epidemic. Prices of newly built dwellings were also higher year on year, but the number of transactions in these dwellings accounted for less than 3% of all transactions.

Market services, July 2020

In July, turnover growth continued for the third consecutive month in all market services, while total turnover was around 9% lower than before the outbreak of the epidemic. After the sharp decline during the epidemic, the highest monthly growth was again recorded in accommodation and food service activities, partly due to the introduction of tourism vouchers, which contributed to an increase in overnight stays by domestic tourists; the number of foreign tourists remained low. The growth of turnover in professional and technical activities was supported particularly by a significant increase in turnover in architectural and engineering services. Turnover growth strengthened in information and communication activities, while it was more moderate in transport and administrative and support service activities.

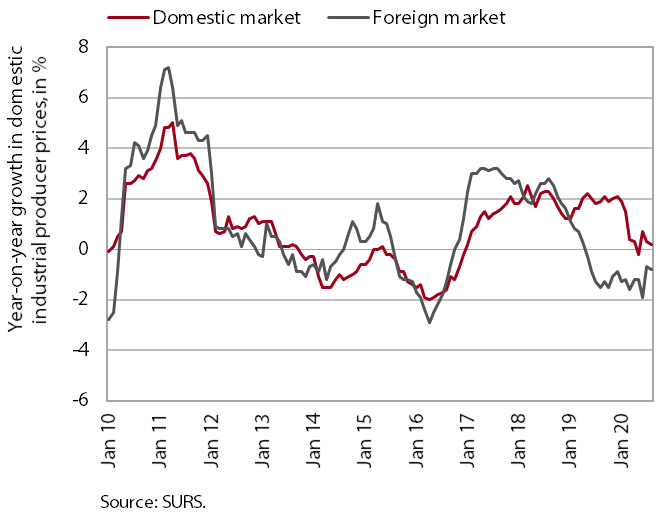

Slovenian industrial producer prices, August 2020

Slovenian industrial producer prices on foreign markets remained lower year on year in August. Prices on foreign markets remained down year on year, in all industrial groups. The decline was larger in countries outside the euro area, while in the euro area it slowed in the last two months to August. Year-on-year price growth on the domestic market remained modest. Energy (electricity) prices and prices of consumer goods rose the most, the latter somewhat more in the non-durable goods segment. Industrial producer prices in the group of intermediate goods were lower year on year amid moderate economic activity.