Charts of the Week

Current economic trends from 21 to 25 March 2022: economic sentiment, turnover based on fiscal verification of invoices, Slovenian industrial producer prices and other trends

The value of the economic sentiment indicator fell significantly in March. The situation in the international environment (war in Ukraine, rising prices and supply chain bottlenecks) was mainly reflected in confidence in manufacturing and among consumers, which also fell year-on-year. According to data on fiscal verification of invoices, year-on-year turnover growth in the second and third weeks of March was considerably higher than a year ago. In our assessment, this was the result of higher prices and higher turnover, also related to uncertainty about future price growth and possible shortage of certain goods. Due to high economic activity and the increase in energy and commodity prices, Slovenian industrial producer prices rose again in February, by 16.5% year-on-year, the highest increase in 20 years. Public sector wages were lower year-on-year in January for the third month in a row due to the cessation of epidemic-related allowances. Wage growth remained strong in construction, accommodation and food service activities and transportation and storage, which could already be affected by labour shortages. Construction activity strengthened in January and is also under increasing cost pressure.

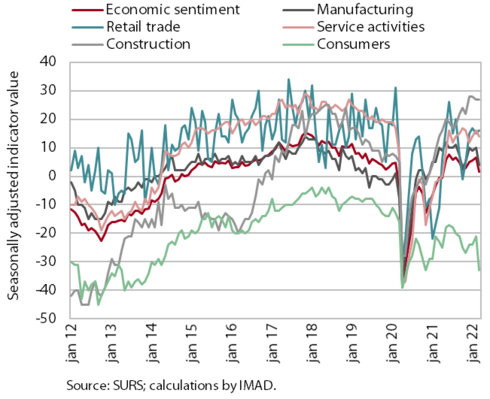

Economic sentiment, March 2022

Rising prices and the Ukraine crisis are probably the main reasons for the decrease in the sentiment indicator in March. Year-on-year, it was lower especially among consumers and in manufacturing. Compared to the previous month, the value of the indicator decreased by 5.2 p.p., i.e. the largest decrease since November 2020. At the monthly level, the value of the consumer confidence indicator decreased the most, by 12 p.p., which is the largest monthly decline since April 2020 (outbreak of the epidemic). Compared to March 2021, the value of the economic confidence indicator was still slightly higher (by 2.1 p.p.). Confidence was significantly higher year-on-year in retail trade (by 27 p.p.) and in service activities and construction (by 15 p.p. and 13 p.p. respectively). However, it was lower among consumers and in manufacturing (by 10 and 6 p.p. respectively). This is due to rising prices and uncertainty about further price increases, and thus country’s economic situation and the households’ financial situation, as well as the impact of the international environment (bottlenecks in the supply of raw materials, rising commodity and energy prices).

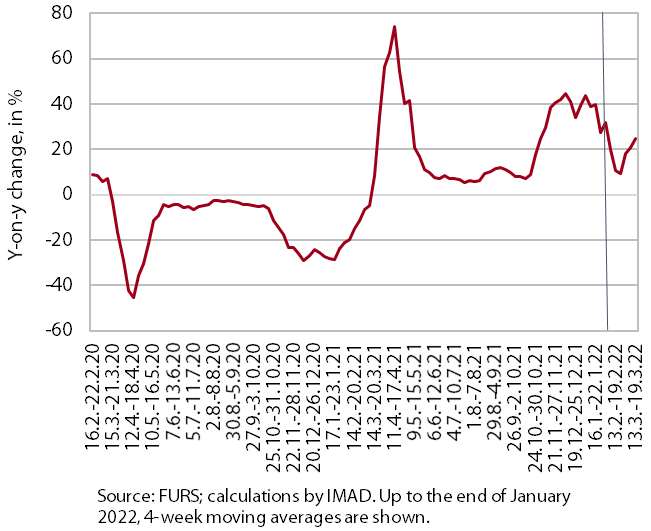

Turnover based on fiscal verification of invoices, 6–19 March 2022

According to data on the fiscal verification of invoices, total turnover between 6 and 19 March 2022 was 23% higher year-on-year in nominal terms and 24% higher than in the same period of 2019. Compared to the same period of 2020, when the epidemic had already been declared and the activity of certain sectors was restricted, turnover was 30% higher. Year-on-year growth was much higher than in the previous two weeks, mainly due to higher turnover in trade. According to our estimates, the high year-on-year growth was the result of higher prices and higher sales due to the expectation of further price increases and possible supply shortages (of automotive fuels, certain foodstuffs), which were largely caused by the Ukraine crisis. Year-on-year growth was still high for activities that were almost completely shut down in the same period of 2021 (especially tourism-related services).

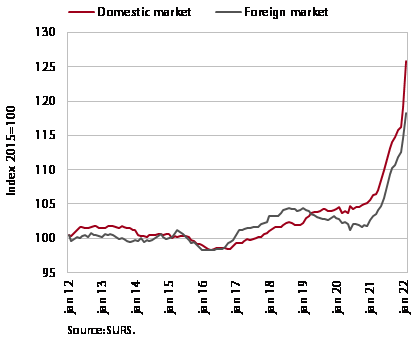

Slovenian industrial producer prices, February 2022

Growth of Slovenian industrial producer prices is still high, i.e. 16.5% year-on-year in January. Prices are rising across all industrial groups, both in the domestic and foreign markets. Overall growth continues to be driven mainly by commodity prices, which increased by almost 22% year-on-year in February. Energy price growth increased significantly to almost 60%. Prices in the domestic market (61.5%) contributed the most to this high year-on-year growth. They increased by almost 45% in February, which we believe was due to the conclusion of new contracts with energy suppliers. Capital goods prices increased by more than 10% year-on-year in February. Given production bottlenecks, and higher energy and other commodity prices, consumer prices are also rising gradually, by 5.6% year-on-year. Prices of non-durable goods rose by 6% year-on-year while prices of durable goods prices rose by about 4% year-on-year.

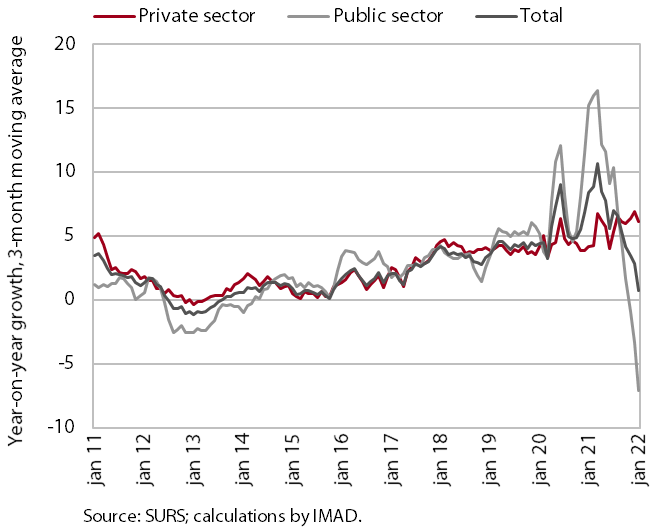

Wages, January 2022

In January, average wages in the public sector were 10.8% lower year-on-year, while they were 3.4% higher in the private sector. Due to the cessation of epidemic-related allowances, year-on-year wage growth in the public sector slowed significantly in the second half of last year and turned negative year-on-year last November. In the private sector, year-on-year growth in January was somewhat more modest than in previous months, partly due to a relatively high base in January last year (with a sharp increase in the minimum wage and the impact of the methodology used to calculate average wages). Growth was still high in construction, accommodation and food service activities and transportation and storage, which could already be the consequence of labour shortages.

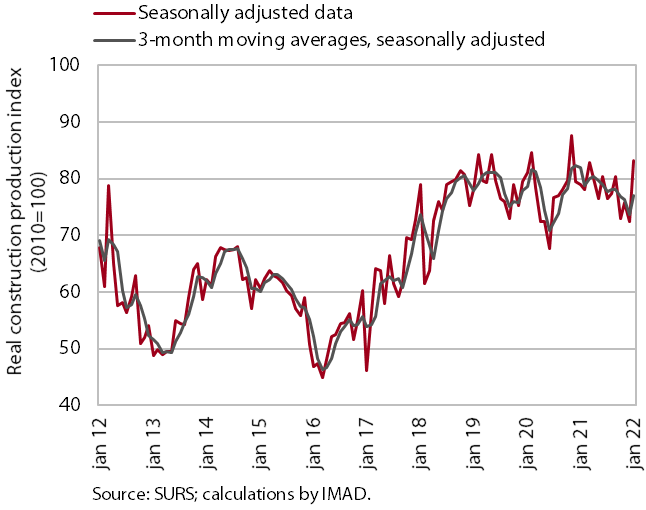

Construction, January 2022

The value of construction output increased in January. After a gradual decline in construction activity in 2021, the value of completed works increased in January and was 5.8% higher year-on-year. The largest increase was seen in residential construction, which is also construction sector to have seen the largest activity drop last year. Activity in this construction sector remains relatively low. Fluctuations in other construction sectors are smaller; activity in civil engineering is still relatively high and was 10% higher in January than a year ago.

Cost pressures are increasing. The implicit deflator of the value of completed construction works (used to measure prices in the construction sector) was above 14% in January, the highest level in the last 20 years. According to business trends in construction, high material costs were reported as a limiting factor by two-thirds of companies in March, while material shortage was reported by 30% of companies. Both indicators increased sharply over the past year and reached their highest levels in the past 20 years.

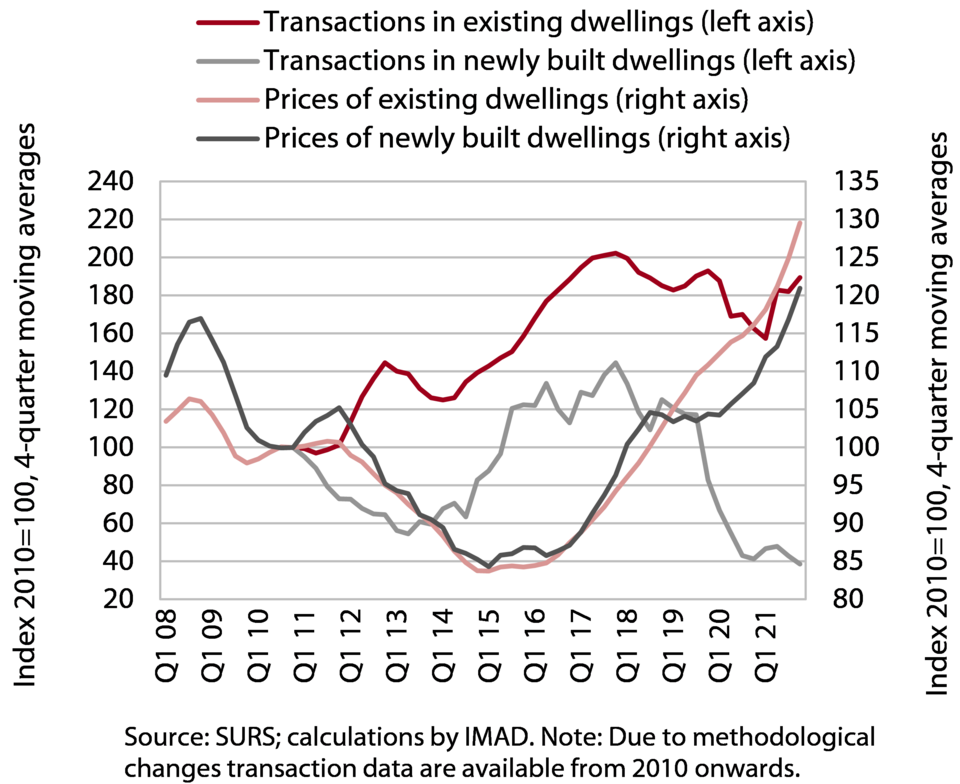

Real estate, Q4 2021

Given the relatively high number of transactions, dwelling price growth accelerated in the fourth quarter. Prices were up 15.7% year-on-year and 11.5% in 2021 as a whole, which is a strong acceleration from the average growth of 4.6% in 2020. Price growth in the fourth quarter and in 2021 as a whole was similar for both existing and newly built dwellings, with the latter accounting for only 2% of all transactions in the year as a whole. In nominal terms, prices at the end of 2021 were 26% above the record average prices of 2008. Even taking into account overall price growth (inflation), dwelling prices were above the 2008 peak – prices of existing dwellings were 12% above this level in the last quarter of 2021, while prices of newly built dwellings were still 6% lower. Prices deflated by growth in nominal gross wages were lagging more significantly behind, i.e. 9%, but were well above the long-term average last year (average between 2007 and 2021).