Charts of the Week

Current economic trends from 21 to 24 June 2021: economic sentiment, traffic of electronically tolled vehicles, electricity consumption, Slovenian industrial producer prices and real estate

The easing of containment measures in May and June had a positive impact mainly on confidence in retail trade and services, while consumer confidence has improved but is still lower than before the crisis. The volume of freight traffic on Slovenian motorways remained high in the third week of June, reaching pre-crisis levels. Electricity consumption was also higher year-on-year, but was a tenth lower than the same period in 2019, mainly due to reduced tourism activities. The growth of Slovenian industrial producer prices continued to strengthen, due in particular to higher commodity prices.

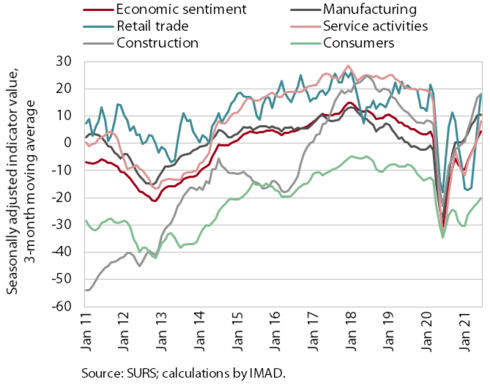

Economic sentiment, June 2021

Economic sentiment improved in June, mainly due to improvements in retail trade and services. The latter is a consequence of the gradual lifting of containment measures in May and June and, in particular, the opening of hotels and restaurants. On a monthly basis, confidence in manufacturing and construction deteriorated slightly, but remains high compared to a year ago. Consumer confidence remains low but has improved in recent months. However, the proportion of those who believe that prices will rise in the future has increased significantly over the last three months.

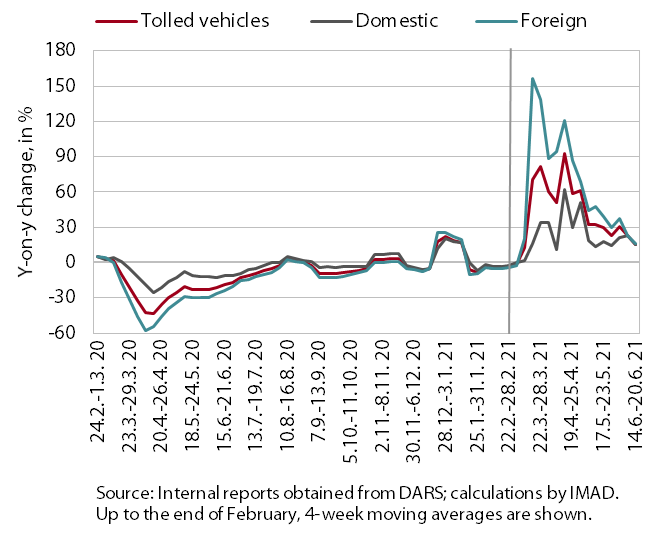

Traffic of electronically tolled vehicles on Slovenian motorways, June 2021

Freight traffic on Slovenian motorways in the third week of June was 16% higher than in the same period of last year and the same as in the same period of 2019. The volume of freight traffic was very high, as in the previous week. The significant difference from last year is still mainly due to the lower traffic volume in the same period last year after the first wave of the epidemic. Compared to the same week of the pre-crisis year 2019, domestic vehicle volume was 6% higher and foreign vehicle volume was 3% lower, which is still within the normal variation in the ratio of domestic to foreign vehicles.

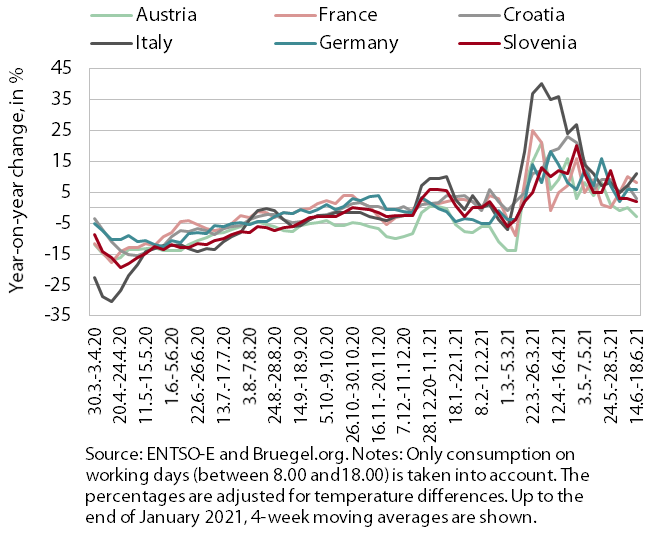

Electricity consumption, June 2021

In the week between 14 and 18 June, electricity consumption was 2% higher than the same week in 2020, but 10% lower than the same week of the pre-crisis year 2019. We estimate that the reason for the higher year-on-year consumption was in particular the low base of last year. However, although many containment measures were lifted, consumption remained lower than before the crisis. Particularly due to the base effect, year-on-year higher consumption was also recorded in the majority of Slovenia’s main trading partners (from 3% in Croatia to 11% in Italy), except in Austria, where it was 3% lower. Compared to the same week of 2019, consumption was down in Austria (5%), France (2%), and Italy and Croatia (7%), while consumption in Germany was 1% higher.

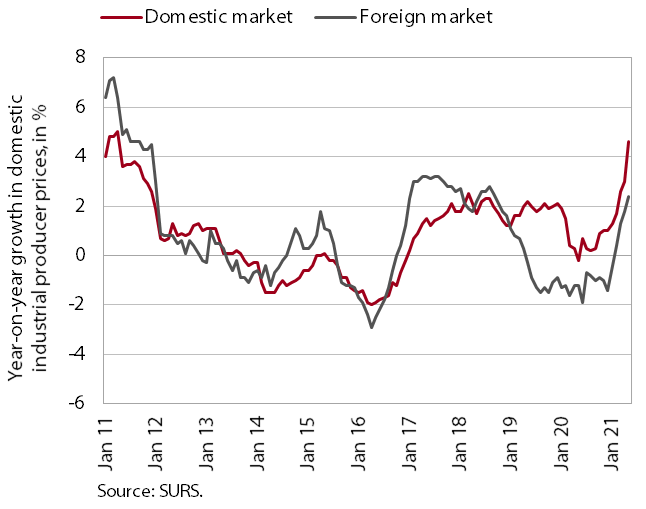

Slovenian industrial producer prices, May 2021

Year-on-year growth in Slovenian industrial producer prices continued to strengthen in May, reaching 3.5%, the highest level since 2011. Price growth in the domestic market continued to increase (4.6%), as did price growth in foreign markets. However, price growth in foreign markets was only half as strong as in the domestic market. The difference in growth is largely due to price trends over the past year. However, year-on-year price growth in the five months of this year was comparable in the domestic and foreign markets (about 3%). Higher commodity prices contributed the most to the growth, rising by 5% year-on-year in May. Prices in the manufacture of metals were 15% higher year-on-year. Growth of energy and capital goods prices has also been strengthening. The combined increase in consumer goods prices in the domestic and foreign markets remains modest year-on-year (0.2%). Only domestic prices of durable goods were higher year-on-year (2.1%).

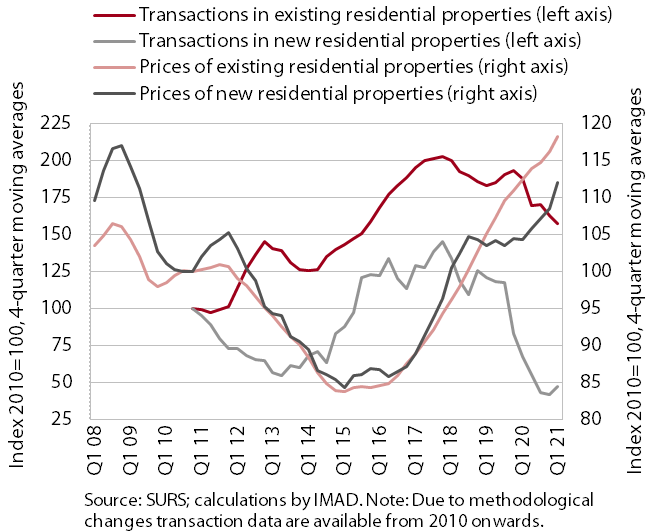

Real estate, Q1 2021

Average residential real estate prices increased further in early 2021, while the number of transactions declined in the face of limited supply and restrictions on business activity due to the epidemic. After growing by 4.6% in 2020 as a whole, prices rose by 7.3% year-on-year in the first quarter of 2021. Prices of newly built dwellings increased the most (by 13.1%), accounting for less than 5% of all transactions, despite an increase in the number of sales compared to the first quarter of last year. Prices of existing dwellings rose by 7% though the number of sales was the lowest in six years, with the exception of the second quarter of last year.