Charts of the Week

Current economic trends from 20 to 24 September 2021: Fiscal verification of invoices, economic sentiment, wages, Slovenian industrial producer prices and other

Uncertainty about the future development of the COVID-19 epidemic and the possible adoption of containment measures contributed to the deterioration of the economic sentiment indicator in September, although most confidence indicators remain higher than a year ago. According to the data on the fiscal verification of invoices, the relatively favourable trend in trade and tourism-related activities continued in the first half of September. Total turnover was higher than in the same period before the epidemic. Year-on-year growth in average wages was high in the first seven months, mainly due to strong growth in the public sector (payment of epidemic-related allowances). Due to higher prices of intermediate goods and capital goods, the Slovenian industrial producer price growth continued to rise strongly in August, reaching its highest level in the last decade.

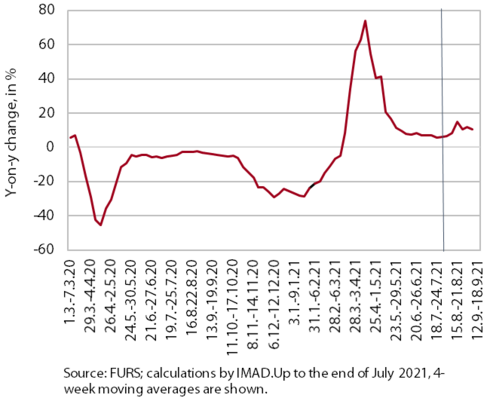

Fiscal verification of invoices, September 2021

According to data on the fiscal verification of invoices, total turnover between 5 and 18 September was 11% higher year-on-year and 6% higher than in the same period of 2019. The growth was primarily a result of higher turnover in trade (up 10% and 6%, respectively), which accounts for about three-quarters of total turnover. Turnover growth in travel agencies, accommodation, food and beverage service activities and sports activities was even higher year-on-year (due to the low base). In some activities, turnover growth was driven by a larger number of foreign tourists as well as by the redemption of vouchers introduced last year and this year. Turnover in certain services (accommodation and food service activities, sports activities) was also higher than in the same period of 2019, while turnover in other services (travel agency activities, creative, arts and entertainment activities, and casinos) was significantly lower (by around half and a third, respectively).

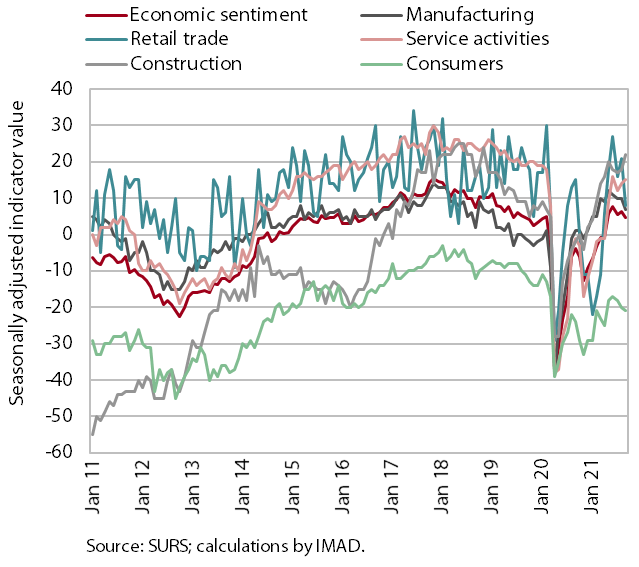

Economic sentiment, September 2021

In September, the value of the sentiment indicator deteriorated slightly. On a monthly basis, confidence in trade fell significantly, with indicators of expectations about selling prices, sales, and expected employment declining the most. Confidence also fell slightly in manufacturing and among consumers, who are particularly concerned about future economic conditions. Confidence in services and construction improved slightly, with the latter reaching its highest level in three years. Year-on-year, the value of most confidence indicators is significantly higher, with the exception of retail trade, where confidence fluctuated sharply on a monthly basis due to containment measures. Compared to the same period in 2019, the economic sentiment indicator remains at a similar level.

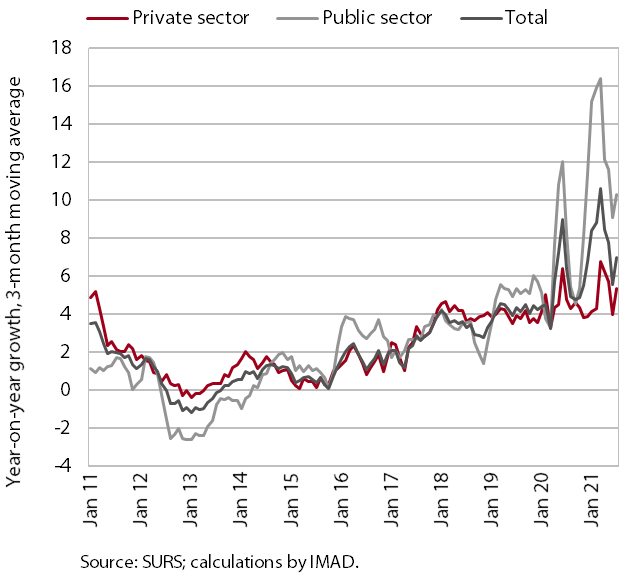

Wages, July 2021

Year-on-year wage growth remained high in July (7.1%). In the public sector, it was 9.3%, slightly higher than in June. In both months, year-on-year wage growth was lower than in previous months, when it was affected by epidemic-related allowances. In the private sector, average wages rose 5.5% year-on-year in the first seven months, reflecting labour shortages, the increase in the minimum wage at the start of the year, and a new wage calculation method related to the intervention job retention measures.

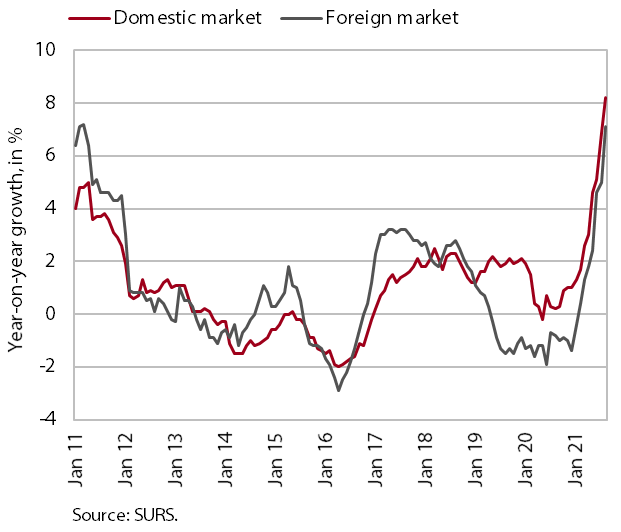

Slovenian industrial producer prices, August 2021

The year-on-year growth of Slovenian industrial producer prices strengthened further to 7.7% in August. Prices in domestic and foreign markets are recording high growth rates. Further growth in prices of intermediate goods, which were almost 12% higher year-on-year, and capital goods, which were 7.5% higher, contributed the most to overall growth. Given the stronger growth in foreign markets (almost 65% year-on-year), year-on-year growth in energy prices also strengthened significantly in August (to 8.3%), but its contribution to overall growth was relatively modest due to its small share. Consumer goods price growth remained subdued year-on-year, hovering around 1% for the third month in a row. In the last two months, prices of non-durable consumer goods have risen somewhat more sharply (1.3%) than in previous years, while growth in prices of durable consumer goods has actually slowed somewhat (to 0.2%).

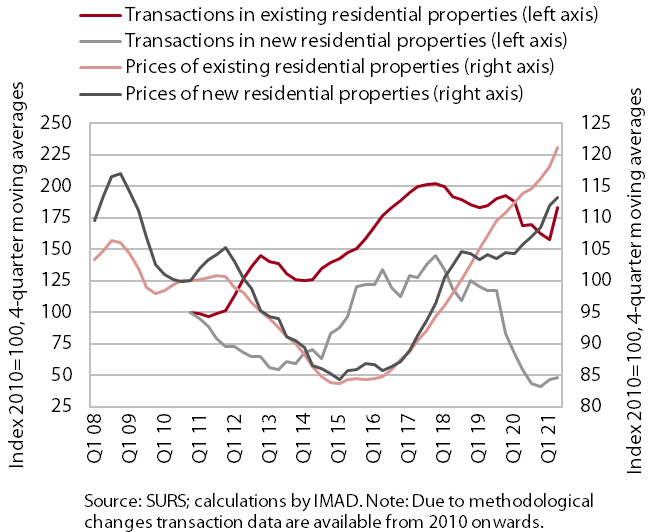

Real estate, Q2 2021

With sales at their highest level in the last four years, growth in the average dwelling prices accelerated in the second quarter. After growing 4.6% in 2020 as a whole, prices rose 7.3% year-on-year in the first quarter and 9.9% in the second quarter. The high growth was driven by higher prices of existing dwellings (by more than a tenth), with a record number of transactions taking place in the second quarter of this year. Prices of newly built dwellings were also higher (4.9%). However, their sales was the lowest since 2010, with the exception of the second quarter of last year (66 out of a total of 3993 transactions).