Charts of the Week

Current economic trends from 20 to 24 June: slovenian industrial producer prices, economic sentiment, real estate and wages

Year-on-year growth of Slovenian industrial producer prices continued to strengthen in May. Prices increased in all industrial groups, most strongly in the domestic market. This was impacted by geopolitical tensions, the tight situation in the market for energy and non-energy commodities and supply chain bottlenecks. According to our estimate, these factors are also the main reason for the deterioration in the economic sentiment indicator, which deteriorated further in June and was also lower year-on-year, but still above the long-term average. Prices of dwellings, especially of existing dwellings, have also risen significantly as the supply of newly built dwellings and thus the number of transactions have been severely limited. In April, year-on-year growth of the average gross wage increased in the private sector. Growth remained strong in activities affected by labour shortages (accommodation and food service activities, trade, and transportation and storage). In the public sector, average gross wage remains lower year-on-year due to the cessation of COVID-19 allowances. In real terms, the average wage was lower both in the public and private sector.

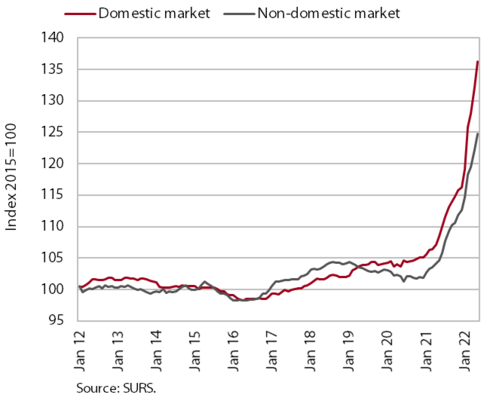

Slovenian industrial producer prices, May 2022

Geopolitical tensions, tighter conditions in energy and non-energy commodity markets and supply chain bottlenecks continue to drive growth in Slovenian industrial producer prices, which already reached 22.5% in May. Price growth has increased in all industrial groups, especially in the domestic market, where it reached 25.7% year-on-year (19.3% in non-domestic market). Overall price growth continues to be driven mainly by prices of intermediate goods, which were 28.5% higher year-on-year. The strongest year-on-year increase was still recorded by energy prices, which rose by almost 75%, but due to their lower weight, their contribution to overall growth was smaller than that of intermediate goods. Compared to energy and intermediate goods, the increase in Slovenian industrial producer prices of capital goods and consumer goods (12.8% and 10.4%, respectively) was relatively small, but still well above the long-term average. Prices of durable consumer goods and non-durable goods were higher year-on-year (by 8.9% and 10.8%, respectively).

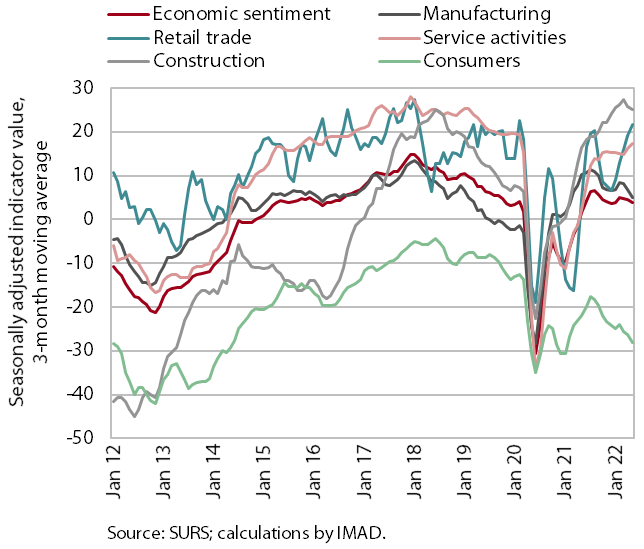

Economic sentiment, June 2022

The value of the economic sentiment indicator deteriorated further in June and was also lower year-on-year, but still above the long-term average. Compared to May, confidence was lower everywhere, especially in construction and retail trade, and compared to June last year, it was significantly lower among consumers and in manufacturing. It was higher year-on-year only in services. The value of the consumer confidence indicator remains below the long-term average, while it is the same as the average in manufacturing. Lower confidence among consumers is related to rising prices and the resulting deterioration in household purchasing power, while lower confidence in manufacturing is related to the current situation in the international environment (bottlenecks in the supply of raw materials, rising commodity and energy prices and the Russian-Ukrainian war). Indicators in construction as well as in trade and services remain well above the long-term average, which is related to this year’s revival of construction activity and the lifting of operating restrictions after the COVID-19 epidemic.

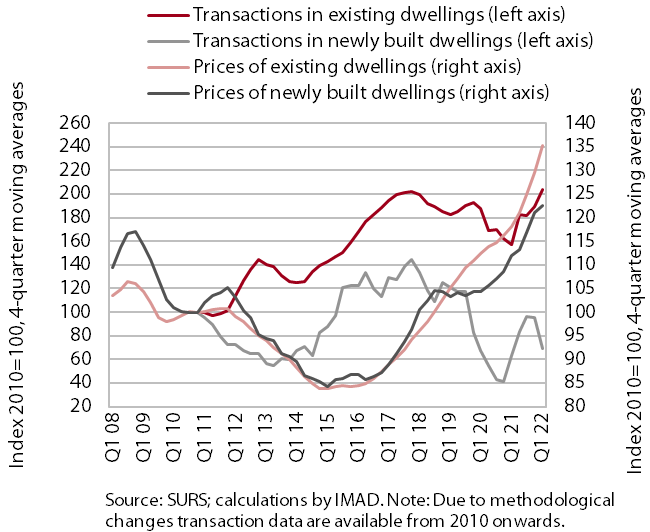

Real estate, Q1 2022

Given the high number of transactions, the high growth of dwelling prices continued in Q1 2022. After growing by 11.5% in 2021 as a whole, prices rose by 16.9% year-on-year. The high growth was driven by higher prices of existing dwellings (by 18.3%), while prices of newly built dwellings, which accounted for only 1% of all transactions due to limited supply, were 1.5% higher. The brisk trading in the real estate market was also reflected in the continued high level of lending to private households – the value of loans granted for the purchase of newly built dwellings was more than 50% higher in the first quarter than in the same period of 2021.

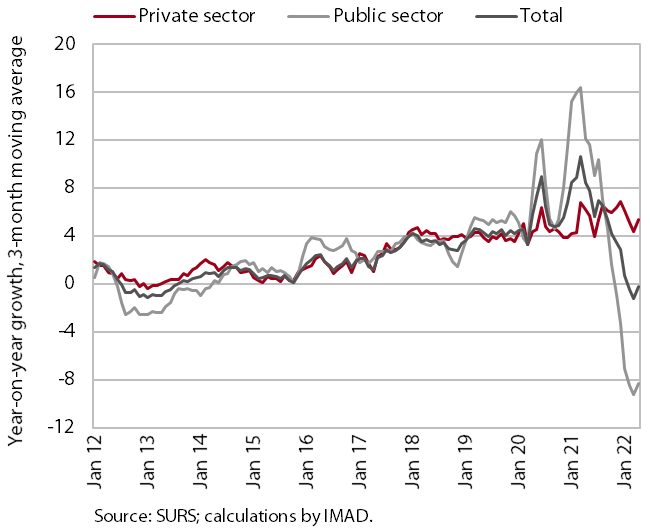

Wages, April 2022

In April, average wages in the public sector were 8.1% lower year-on-year in nominal terms, while they were 6.4% higher in the private sector (0.4% overall). Year-on-year wage growth in the public sector has been negative since November last year. This is related to allowances paid during the period when the epidemic was declared, which are no longer paid this year. In the private sector, year-on-year growth strengthened in April compared to previous months of this year. Wage growth was again the strongest in accommodation and food service activities and it was also strong in trade and transportation and storage. In all these activities, growth is affected by labour shortages. In real terms, the average wage was 6.1% lower year-on-year in April (14% lower in the public sector and 0.5% lower in the private sector).