Charts of the Week

Current economic trends from 20 July to 24 August 2020: electricity consumption, traffic of electronically tolled vehicles, trade, exports and imports of goods and other charts

Towards the end of the second quarter, economic activity increased relative to previous months in most activities (exports, manufacturing and turnover in trade) but remained markedly lower year on year. A further recovery is indicated by August’s data on freight traffic and electricity consumption in the economy, whose values have already reached the 2019 levels. The exception is construction, where in June activity declined further and was a quarter lower than in February.

Labour market conditions have not deteriorated further since May, which we estimate can be mainly attributed to the extension of the measure of temporary layoffs, the co-financing of short-time work and the lifting of stringent containment measures.

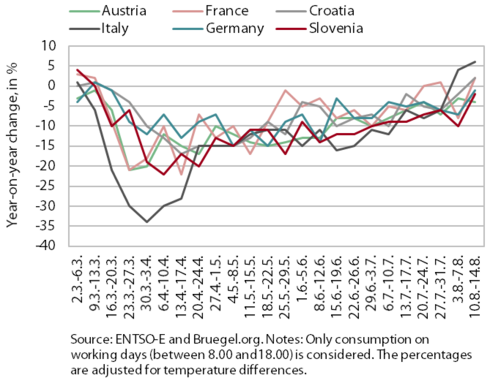

Electricity consumption, August 2020

Weekly electricity consumption came very close to last year’s level in the middle of August. Year on year, it was still 2% lower. Among Slovenia’s most important trading partners, Germany saw a similar decline (by 1%); the decline in Austria was somewhat larger (by 4%). In other countries, consumption exceeded last year’s level, in Italy by 6%, in France and Croatia by 2%.

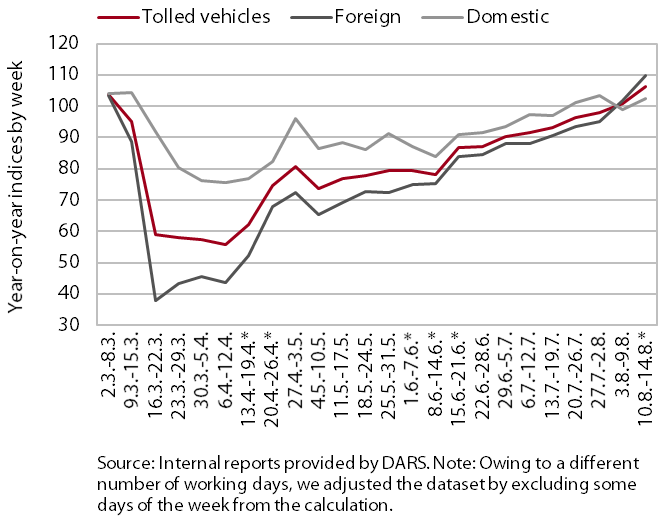

Traffic of electronically tolled vehicles on Slovenian motorways, August 2020

In the third week of August, freight traffic on Slovenian motorways exceeded the pre-epidemic level. A more than 40% year-on-year decline after the declaration of the epidemic decreased slightly in April and stagnated in May. Since mid-June, traffic has again been rising and was 6% higher year on year in the middle of August. The distance travelled by domestic hauliers was 2% higher and the distance travelled by foreign hauliers almost 10% higher year on year.

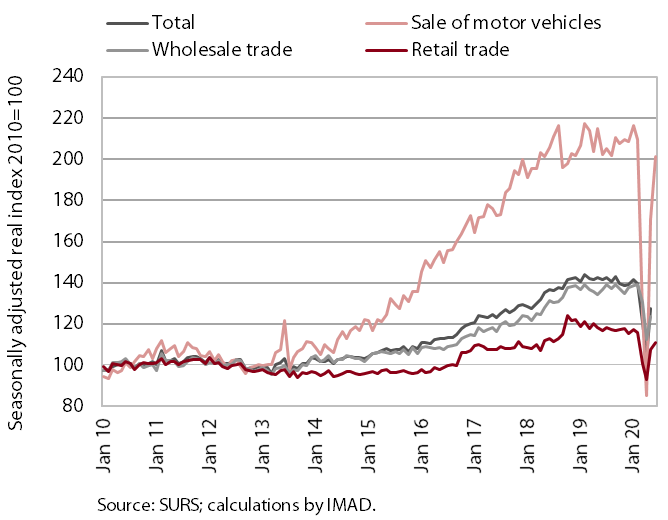

Trade, June 2020

After two months of pronounced decline, turnover in trade strengthened with the loosening of containment measures in May and June. May recorded the strongest growth in the sale of motor vehicles, where turnover had also declined the most in the previous two months. In June, motor vehicle sales were already above the previous year’s level according to preliminary data. Owing to higher activity in transportation and manufacturing, turnover also strengthened significantly in wholesale trade. In retail trade, sales of non-food products increased strongly with the reopening of stores. This was the only sector to exceed the level of May last year. According to preliminary data, growth also continued in June.

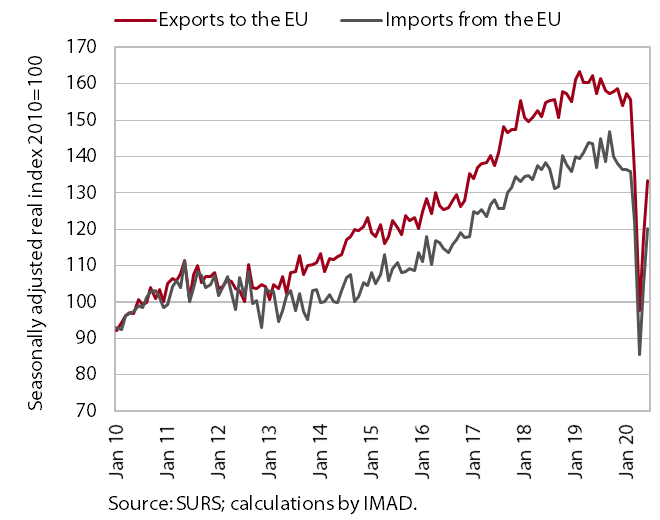

Exports and imports of goods, June 2020

Goods trade increased in May and June relative to previous months but remained markedly lower than one year earlier. Since the beginning of the spread of the epidemic in Europe, exports to EU countries have dropped the most, particularly exports to Italy, Austria and Croatia. With the lifting of containment measures and a gradual recovery of production in Slovenia and its main trading partners, in June exports increased but remained around a tenth lower year on year. In June, the impact of the recovery of economic activity in Germany was particularly positive. Export expectations also improved and reached the levels from the beginning of the year, while new export orders remained at the low levels of April. Imports were also up in May and June, but they were still markedly lower than in the month before the outbreak of the epidemic. Since February, imports of intermediate goods have dropped the most.

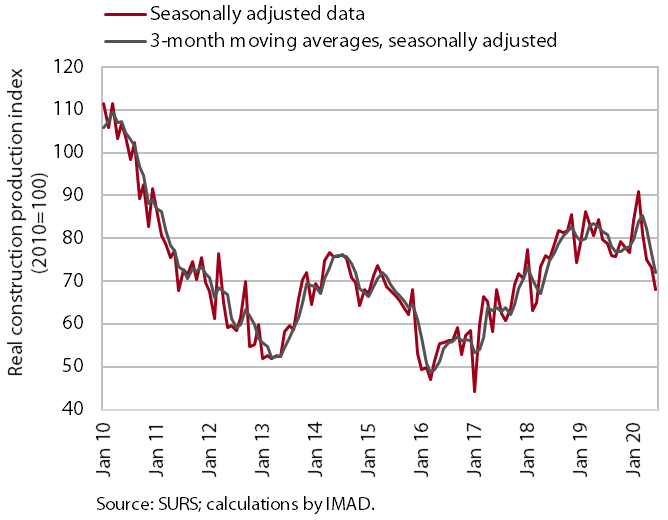

Construction, June 2020

Construction activity declined further in June. Relative to February, the last month before the outbreak of the epidemic, it fell by 25.2%. In the second quarter as a whole, activity dropped by 15.6%, the decline being the most intense in the construction of non-residential buildings (-28.8%) and smaller in the construction of civil-engineering works and residential buildings (-14.5% and -8.3% respectively).

The indicators of the stock of contracts and the number of new contracts strengthened this year, being higher year on year in June. A somewhat worse picture is indicated by data on issued construction permits, which dropped significantly this year, and business trends in construction, which improved in July but remained markedly lower than before the outbreak of the epidemic.

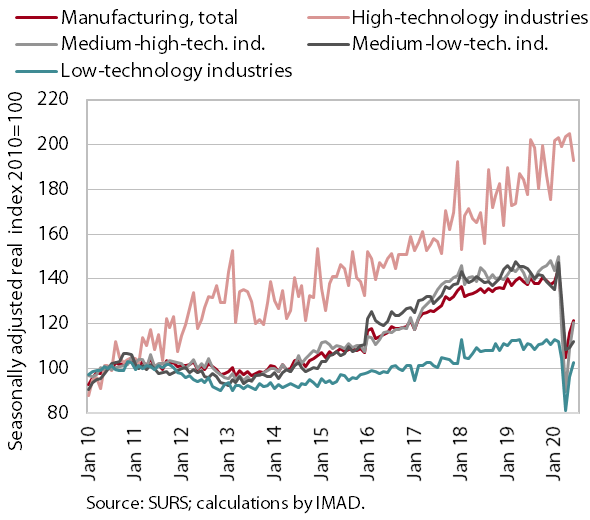

Production volume in manufacturing, June 2020

Manufacturing production increased further in June but remained significantly lower than before the epidemic. In all groups of industries according to technology intensity, the strengthening of production in June was more modest than in May. At the end of the second quarter, production remained lower than before the introduction of measures in all groups except high-technology industries, which were, as expected, the least affected by the containment measures. The largest lags were recorded by some more important medium-technology industries, which are on average more export-oriented (vehicles and electrical appliances) and integrated in global value chains (the metal and rubber industries), and by some smaller low-technology industries (leather and textiles). Compared with the first half of the previous year, manufacturing output was a tenth lower year on year.

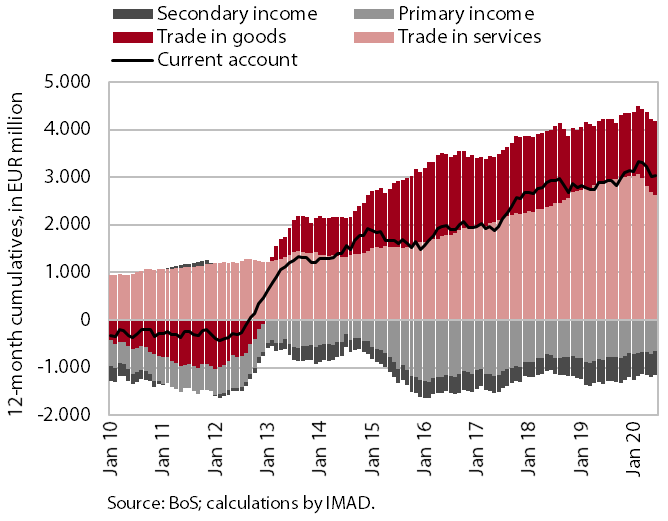

Current account of the balance of payments, June 2020

The current account surplus was lower year on year in the second quarter. This was mainly due to a lower surplus in services. The surplus in travel services dropped the most, reaching the lowest level since 1995 in the second quarter this year (EUR 35.9 million). The trade surplus in road and air transport services also declined more markedly as a consequence of lower flows of goods. The surplus in goods trade increased further due to a larger nominal decline in imports than exports, which is also related to a larger drop in import prices of industrial products and energy. The net outflows of primary income in the second quarter were lower year on year, mostly due to a lower amount of companies’ distributed profits. The higher net outflows of secondary income were marked particularly by higher payments into the EU budget (VAT-based and GNI-based contributions).

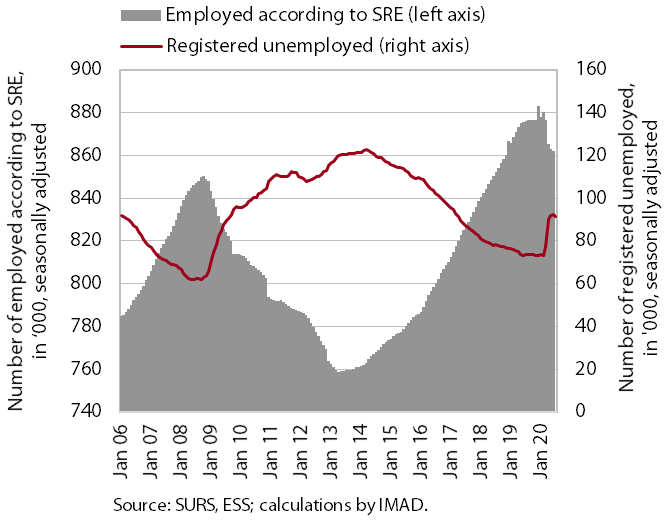

Labour market, June – July 2020

In June, employment remained similar to that one month earlier; this is also true for the number of the unemployed in July. The number of employed persons was 1.6% lower year on year in June and 1.4% lower in the second quarter as a whole, where accommodation and foods service activities and administrative and support service activities stood out with a decline of around 10%. At the end of July, the number of unemployed persons was 89,397 (24.4% higher than one year earlier), which is very similar to that at the end of June. We estimate that such movements are related particularly to the extension of the measure of temporary laid-offs, the co-financing of short-time work and the lifting of stringent containment measures.

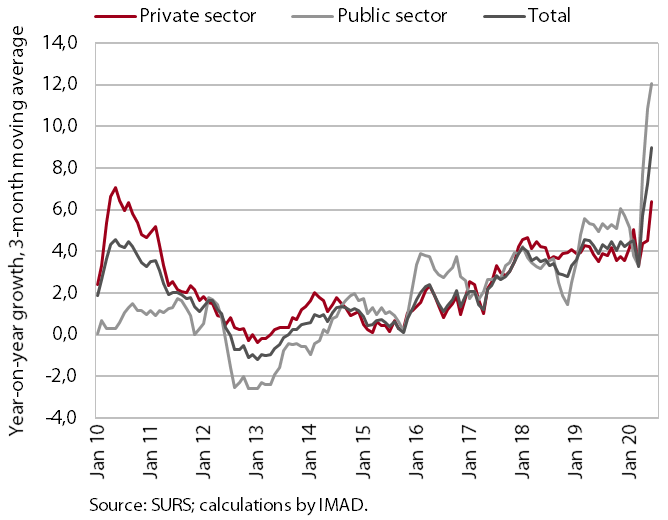

Wages, June 2020

In June, the year-on-year growth of the average gross wage strengthened further (5.5%), albeit somewhat less than on average in April and May (10.7%). In the private sector, both the wage bill and the number of persons employed already rose somewhat in May compared with April, while the increase in June was even stronger. The pronounced year-on-year wage growth (in the second quarter, by 6.4% on average) was significantly influenced by the methodology according to which employers report the number of wage recipients and the level of wages paid. With many employed persons being temporarily laid off, the amount of wages paid from employers’ resources decreased significantly. The number of employed persons who received these wages declined even more. The average gross wage per employee therefore rose significantly. In the public sector, the methodological effect of temporary layoffs was significantly smaller. The stronger wage growth in the second quarter (12%) was attributable to the payment of allowances for performing hazardous work and for higher workloads and the payment of the bonus for work in high-risk conditions (according to the collective agreement) in April and May. In June, the payment of these allowances ceased, which was reflected in lower year-on-year wage growth.

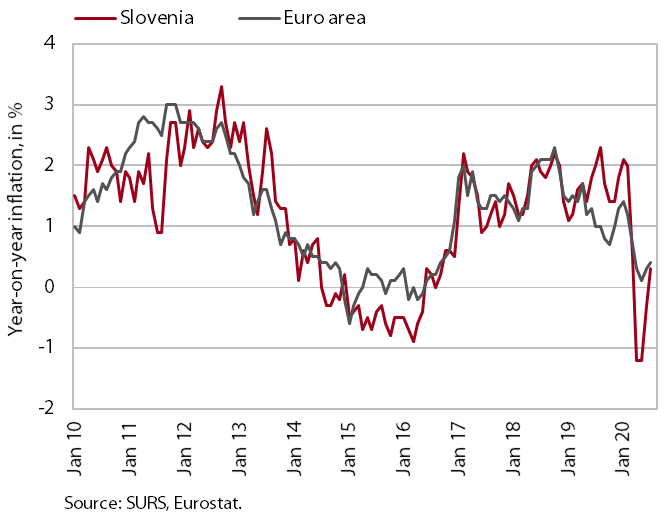

Consumer prices, July 2020

After a decline in the second quarter, consumer prices recorded year-on-year growth again in July. This was however significantly weaker than before the outbreak of the epidemic, mainly due to a fall in energy prices, which were still almost 9% lower year on year in July particularly due to low oil prices and the adjustment of excise duties. Total growth was mainly attributable to service and food prices, which were rising at 2% and 3% rates respectively. In July, prices of non-energy industrial goods, durable goods in particular, also rose slightly according to our estimate. The decline in prices of semi-durable goods also slowed significantly, as the seasonal decline in clothing and footwear prices in July was less pronounced than in the previous year.

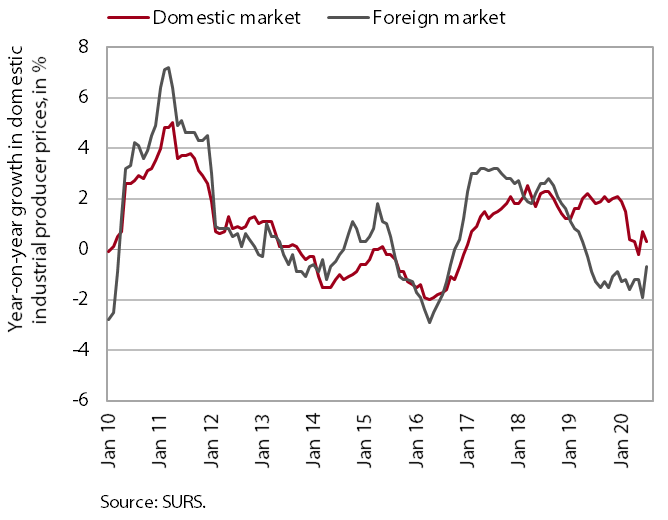

Slovenian industrial producer prices, July 2020

The total year-in-year fall in Slovenian industrial producer prices decreased in July. The smaller fall is largely related to strong monthly growth in capital goods prices on foreign markets. Prices in other industrial groups on foreign markets were again lower year on year. Price growth on the domestic market eased in July, which was mostly attributable to lower prices in the industrial group intermediate goods, while prices of energy, capital goods and consumer goods continued to rise at relatively high rates.