Charts of the Week

Current economic trends from 19 to 23 October 2020: economic sentiment, electricity consumption, traffic of electronically tolled vehicles, slovenian industrial producer prices and wages

Economic sentiment deteriorated in October under the impact of the renewed spread of the epidemic and the measures for its containment. Confidence fell especially among consumers and in sectors that are more closely linked to the adopted measures (trade, services). Confidence and expectations in manufacturing and construction did not deteriorate, but confidence remained significantly lower than in the same period of last year. In mid-October, electricity consumption was 3% lower and freight traffic on motorways around 6% lower year on year.

The methodology for calculating the average wage, according to which only the part funded by the employer is recorded as wage (the measure of co-financing temporary layoffs) and the payment of bonuses during the epidemic are contributing to strong growth in the average wage.

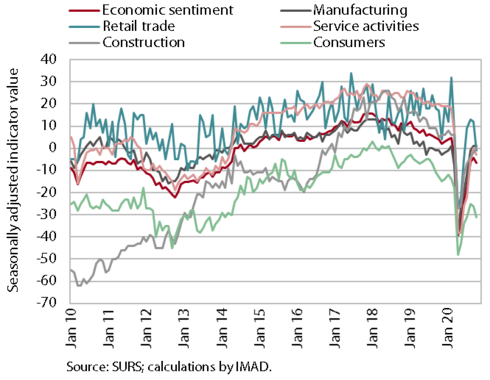

Economic sentiment, October 2020

After several months of improvement, economic sentiment worsened in October. Due to a renewed spread of the epidemic and the adoption of new containment measures, the economic sentiment indicator fell in October. Confidence declined the most in retail trade. It also fell in service activities and among consumers. In manufacturing, the confidence indicator remained close to the previous month’s level; business expectations regarding production volume and exports also remained unchanged. The confidence indicator in construction improved further (mainly due to increased orders in the construction of civil-engineering works), but, like other confidence indicators, it was significantly lower year on year.

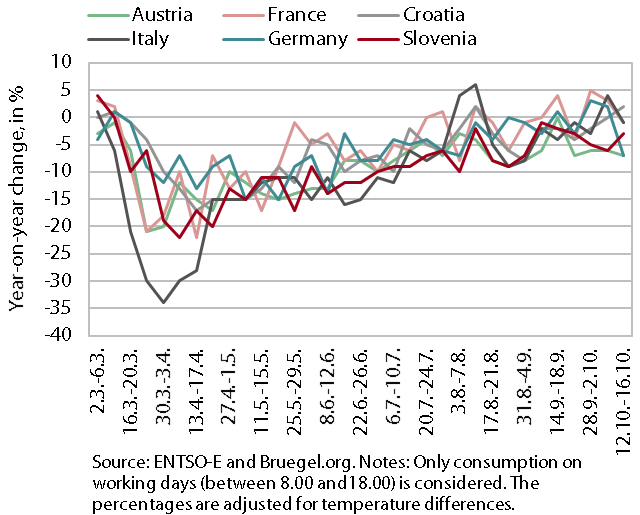

Electricity consumption, October 2020

The year-on-year decline in weekly electricity consumption decreased somewhat in mid-October. In the second week of October, electricity consumption was 3% lower year on year (one week earlier, 6% lower). Among Slovenia’s main trading partners, Austria and Germany recorded the largest year-on-year decline (-7%). In France and Italy, the decline was smaller (-1%), while consumption in Croatia was 2% higher than in the same period of last year.

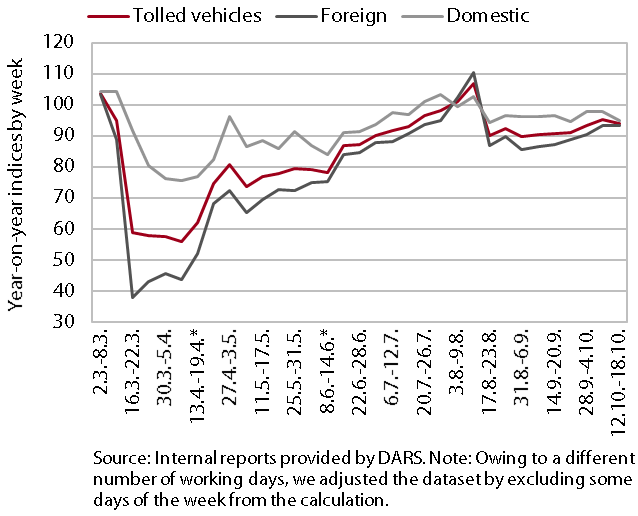

Traffic of electronically tolled vehicles on Slovenian motorways, October 2020

Freight traffic on Slovenian motorways increased somewhat in the first half of October but remained lower than before the epidemic. After a sharp fall following the declaration of the epidemic, it was rising more noticeably from mid-June to mid-August. Then it fell again and remained around 10% below the comparable last year’s level until the beginning of October, when it increased again slightly. In mid-October, it lagged behind the comparable last year’s figure by 6% (the number of kilometres travelled by foreign hauliers by 7% and the number of kilometres travelled by domestic hauliers by 5%).

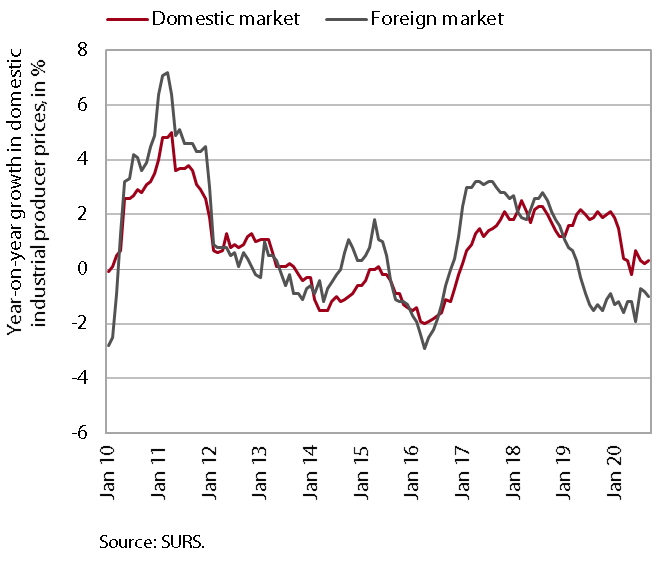

Slovenian industrial producer prices, September 2020

Slovenian industrial producer prices remained lower year on year in September. Prices in countries outside the euro area are declining faster year on year, but the decline in euro area prices has slowed in recent months. Price growth on the domestic market remains modest. Year on year, prices of energy (electricity) are rising at the fastest pace, but their growth is gradually easing. Consumer goods prices also continue to increase year on year (1.6%), this time particularly in the segment of non-durable goods, which is also related to uncertainty about the course of the epidemic. Industrial producer prices in the group of intermediate goods remain lower year on year amid moderate economic activity.

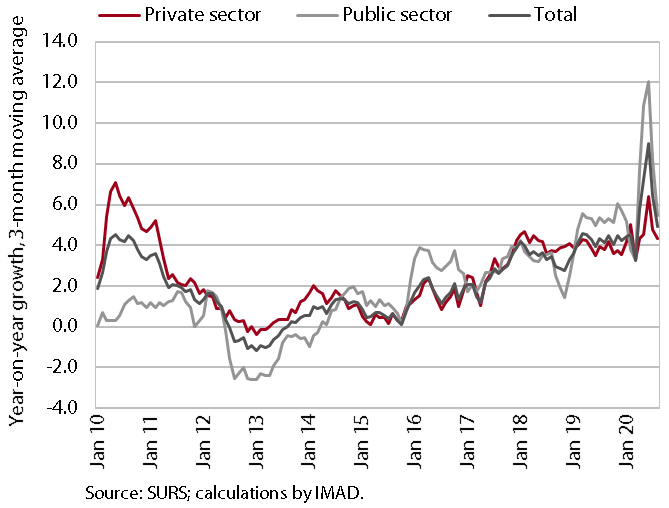

Wages, August 2020

In August, the average gross wage remained more of less the same as in the preceding two months; year on year, it was up 5%. The year-on-year wage growth since April is to a great extent related to the methodology for the collection of earnings statistics, which were significantly affected by the placement of a relatively high number of workers on temporary layoff. As a result of the layoffs, the number of wage recipients fell sharply, as did, albeit somewhat less, the amount of wages funded from employers’ resources. This pushed the average wage upwards. The effect of the temporary layoff measure on wage growth was larger in the private than in the public sector. In the public sector, the stronger year-on-year wage growth in April and May (14.5%, on average) mainly reflected the extraordinary payment of allowances for dangerous working conditions and additional workloads and the payment of the bonus for work in crisis conditions (in accordance with the collective agreement). Since June, extraordinary bonuses have no longer been paid, which is reflected in lower year-on-year wage growth in the public sector – in August, it was at 4.4%.