Charts of the Week

Current economic trends from 19 to 22 April 2022: economic sentiment, turnover based on fiscal verification of invoices, slovenian industrial producer prices and other charts

After the value of the sentiment indicator had fallen sharply in March, it rose slightly in April and was also higher year-on-year. The situation in the international environment (war in Ukraine, rising prices, and supply chain bottlenecks) affected confidence in manufacturing and among consumers, which was lower year-on-year. According to data on fiscal verification of invoices, turnover in the first half of April was much higher in nominal terms than a year ago due to lockdown in this period last year. The growth of Slovenian industrial producer prices accelerated in March and amounted to 17.9% year-on-year; prices went up in all industrial groups. Year-on-year growth of the number of persons in employment remained high in February; it was highest in accommodation and food service activities and in construction. Given the shortage of domestic labour, the number of foreign citizens in employment is increasing, with their share particularly high in construction, transportation and storage, and administrative and support service activities. Average wages in the public sector remained lower year-on-year for the fourth month in a row in February due to the cessation of epidemic-related allowances in the middle of last year. Year-on-year wage growth in the private sector (4.2%) was similar to the previous month and lower than in the final months of 2021, with the strongest growth in accommodation and food service activities, but also high in construction, and transportation and storage, which could already be due to labour shortages.

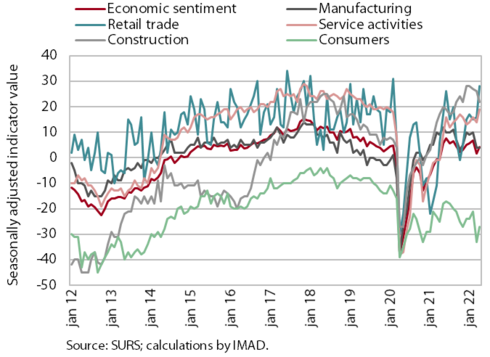

Economic sentiment, April 2022

After falling sharply in March, the value of the sentiment indicator rose again slightly in April and was also higher year-on-year. Confidence was significantly higher year-on-year in retail trade (by 22 p.p.) and in service activities (by 20 p.p.) and slightly higher in construction (by 5 p.p.). Year-on-year, confidence was slightly lower among consumers and in manufacturing (by 2 and 5 p.p. respectively). Confidence among consumers is most affected by rising prices and uncertainty about further price increases, which in turn affects expectations about the future financial situation of households, while confidence in manufacturing is strongly influenced by the situation in the international environment, most recently by the bottlenecks in the supply of raw materials, rising commodity and energy prices, and the Russian-Ukrainian war.

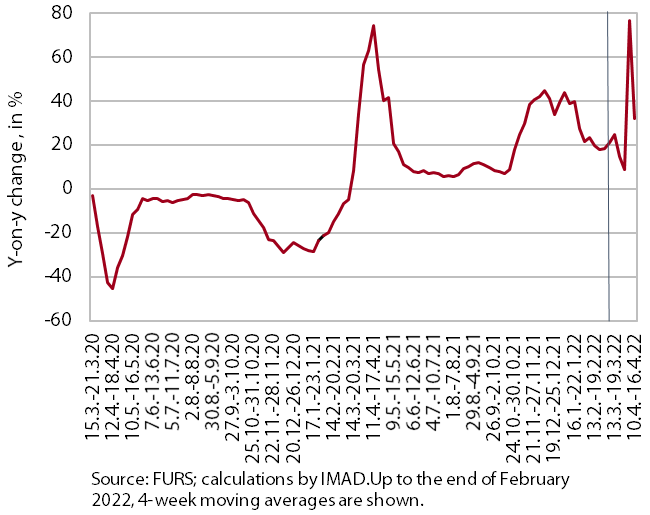

Turnover based on fiscal verification of invoices, in nominal terms, 3–16 April 2022

According to data on the fiscal verification of invoices, total turnover between 3 and 16 April 2022 was 50% higher year-on-year in nominal terms and 24% higher than in the same period of 2019. Year-on-year growth was much higher than the previous two weeks due to last year's low base as a result of the lockdown (between 1 and 11 April). It increased sharply in all three main trade segments (retail trade, wholesale trade and sale of motor vehicles). Growth was still high for activities that were almost completely shut down until the end of April last year (especially tourism-related services).

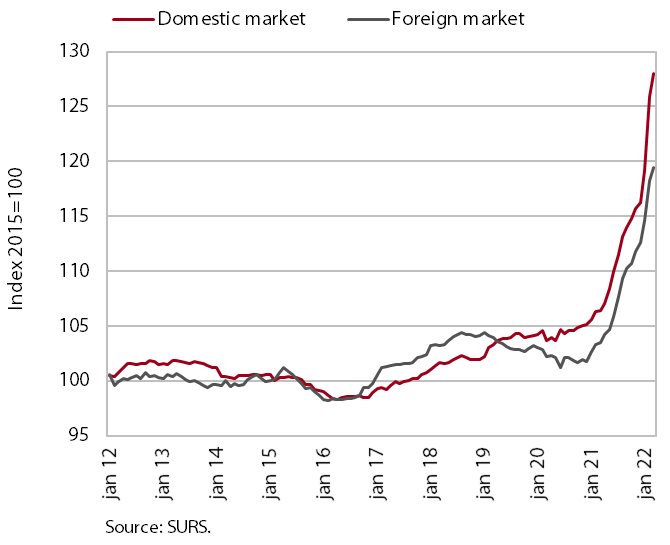

Slovenian industrial producer prices, March 2022

Growth of Slovenian industrial producer prices increased in March, reaching 17.9% year-on-year. Prices increased year-on-year in all industrial groups. Growth was slightly stronger in the domestic market, where prices were about one fifth higher on average. Overall price growth continues to be driven mainly by intermediate goods, whose prices were 23.8% higher year-on-year. The strongest year-on-year increase was still recorded by energy prices, which rose by almost 55%, but their contribution to overall growth was lower due to their lower weight compared to intermediate goods. Capital goods prices increased by about 10% year-on-year in the first quarter of this year. Consumer goods prices continued to rise gradually, increasing by 7.1% year-on-year in March. Prices for the group of non-durable goods grew somewhat more strongly, by 7.4%, while prices for durable consumer goods rose by 6% year-on-year.

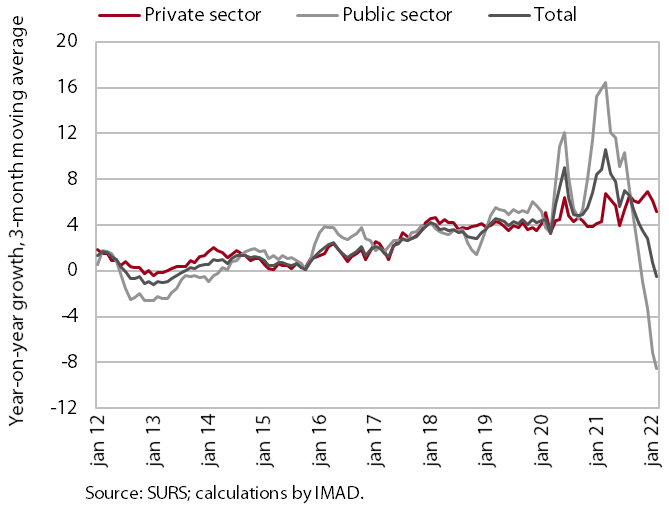

Wages, February 2022

In February, average wages in the public sector were 8.4% lower year-on-year, while they were 4.2% higher in the private sector (-1.0% overall). Due to the cessation of epidemic-related allowances, year-on-year wage growth in the public sector slowed significantly in the second half of last year and turned negative year-on-year last November. Year-on-year growth in the private sector in February was similar to the previous month and lower than in the last few months of 2021, partly due to a relatively high base year-on-year (given a large increase in the minimum wage and the impact of the methodology used to calculate average wages). Growth was by far the highest in accommodation and food service activities and it was also high in construction, and transportation and storage, which could already be the consequence of labour shortages.

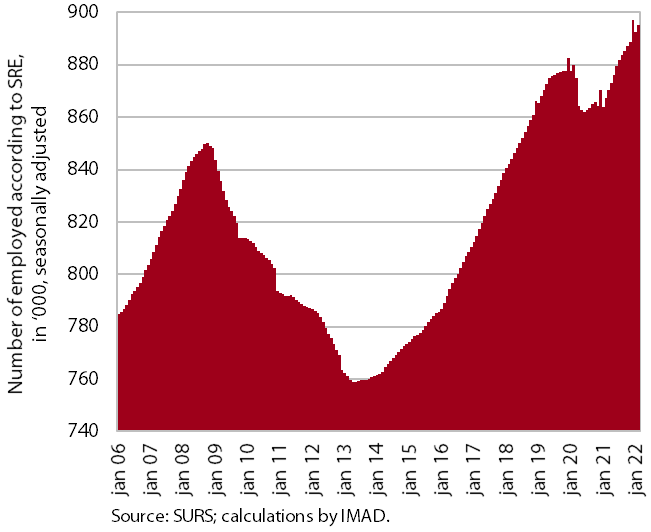

Labour market, February 2022

In February, the year-on-year growth in the number of persons in employment remained high (3.2%). It was the strongest in accommodation and food service activities and in construction. In the latter, the number of persons in employment was significantly higher than before the epidemic, while in the former it remained slightly below the level of two years ago. Amid economic recovery, growth in the number of persons in employment still depended largely on the employment of foreign workers, whose contribution to overall year-on-year growth was more than 50% in February. The share of foreigners among all persons in employment is also increasing, up 1.2 p.p. to 12.8% last year. This is largely related to the shortage of domestic labour, which is most pronounced in construction and administrative and support service activities (mainly due to a high job vacancy rate). The activities with the largest share of foreigners are construction (45%), transportation and storage (31%) and administrative and support service activities (24%).