Charts of the Week

Current economic trends from 16 to 20 November 2020: fiscal verification of invoices, electricity consumption, traffic of electronically tolled vehicles, labour market, wages and slovenian industrial producer prices

According to November's data on fiscally verified invoices, the direct economic consequences of the renewed restrictions on business operations could be considerable but less intense than in the spring wave of the epidemic. This is also indicated by data on weekly electricity consumption, freight traffic on Slovenian motorways and unemployment in the middle of November.

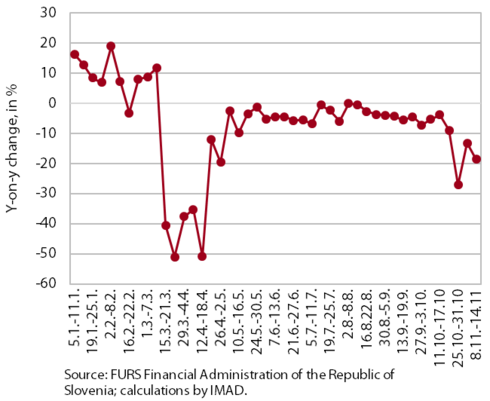

Fiscal verification of invoices, November 2020

According to data on fiscally verified invoices, turnover declined in the first two weeks of November, although significantly less than in the spring. It was approximately 15% lower y-o-y, but the decline was much smaller than at the end of March (more than 50%). Turnover fell the most in gambling and betting activities, arts and entertainment activities, travel agencies, and accommodation. A sharp decline was also recorded in food and beverage service activities, but it was smaller than in the spring. The markedly smaller total decline than in the spring was mainly attributable to retail trade and in the sale and repair of motor vehicles.

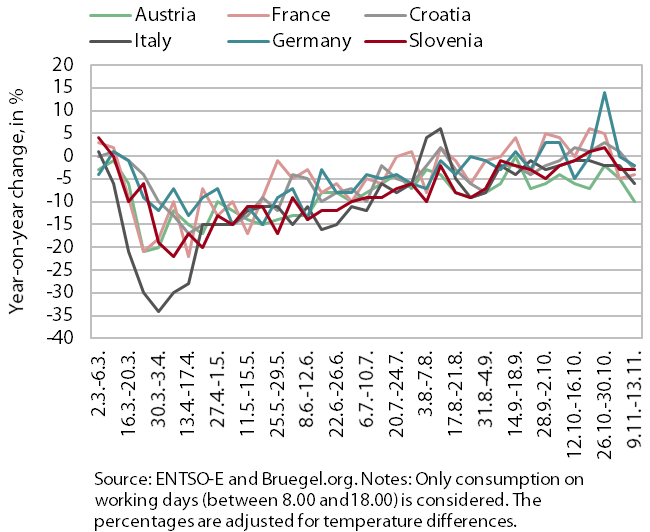

Electricity consumption, November 2020

In mid-November, the y-o-y decline in weekly electricity consumption remained smaller than in the spring wave of the epidemic, despite a number of containment measures. In the second week of November, electricity consumption was, as in the first, 3% lower y-o-y (in the middle of April, around 20% lower). In the majority of main trading partners, the y-o-y decline deepened in the second week of November relative to the previous week but remained smaller than in the spring. The largest decline was recorded in Austria (–10%, a week earlier –5%) and Italy (–6%, a week earlier –2%). In others, it was smaller. In Germany and Croatia, where consumption was mostly higher than last year in recent weeks, the decline amounted to –2% and –3% respectively. In France, it remained roughly the same as in the first week of November (–4%).

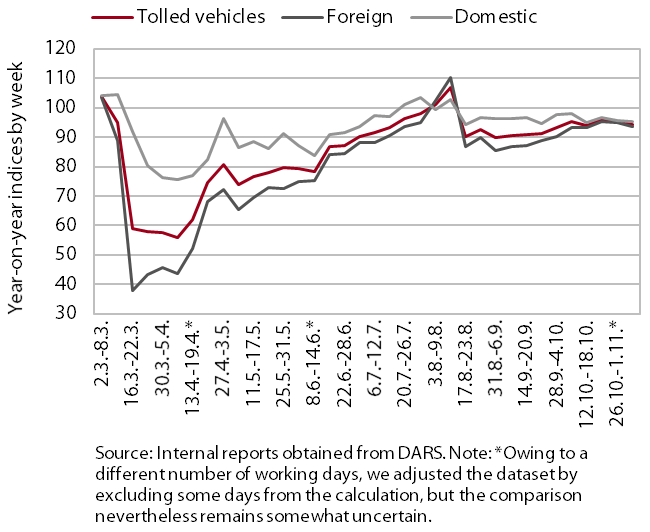

Traffic of electronically tolled vehicles on Slovenian motorways, November 2020

In the middle of November, freight traffic on Slovenian motorways increased somewhat and was only slightly lower than before the first wave of the epidemic. After a sharp fall following the declaration of the epidemic in March, it increased more markedly from mid-June to mid-August. Then it fell again and remained around 10% below last year’s level until the beginning of October, when it rose again slightly. In the week between 9 and 15 November, it was 2% lower than last year. In foreign hauliers, it was 4% lower, while in domestic hauliers it was at the same level as last year.

Labour market, September – November 2020

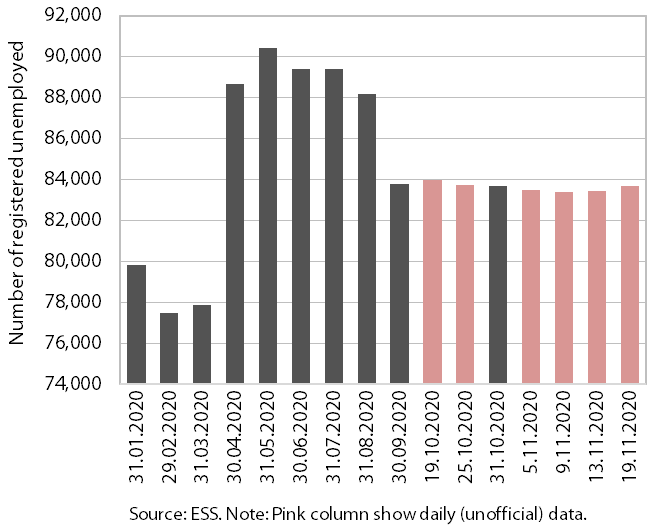

In the middle of November, the number of registered unemployed remained at almost the same level as in the previous two months, despite the renewed restrictions on business operations since mid-October. On 19 November, 83,677 persons were unemployed according to ESS unofficial (daily) data (around 16% more than in the same period last year). The maintenance of the number at a similar level, amid partial adaptation of businesses and consumers to a different way of operation, is to a great extent due to the extension of intervention measures to preserve jobs.

In September, the number of employed persons lagged slightly less behind last year’s level y-o-y (1.4%) than in previous months. Activities with the largest declines remain administrative and support service activities, accommodation and food service activities and manufacturing (-11.1%, –6% and –3.5% respectively).

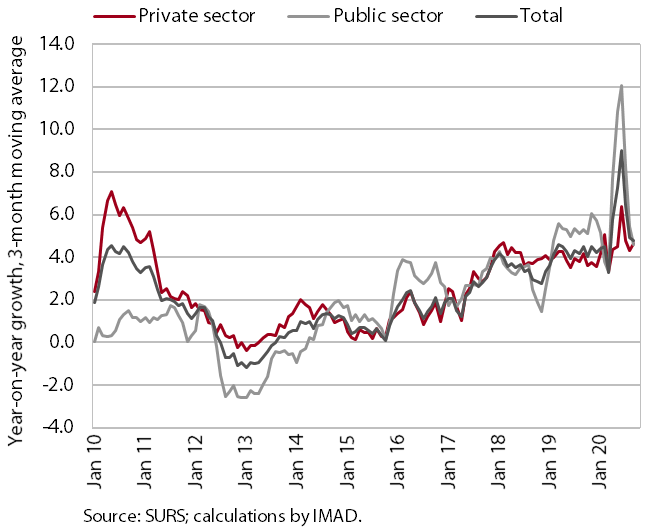

Wages, September 2020

In September, the average gross wage remained more of less the same as in previous months; y-o-y, it was up 5.1 %. The y-o-y wage growth since April was to a great extent related to the methodology for the collection of earning statistics, which were affected by the placement of a relatively large number of workers on temporary layoff. As a result, the number of wage recipients fell sharply, as did, albeit somewhat less, the amount of wages funded from employers’ resources, which pushed the average wage per employee upwards. The effect of the temporary layoff measure on wage growth was larger in the private than in the public sector. In the public sector, the stronger y-o-y wage growth in April and May (14.5%, on average) mainly reflected the extraordinary payment of allowances for hazardous working conditions and additional workloads and the payment of the bonus for work in crisis conditions (in accordance with the collective agreement). Since June, extraordinary bonuses have no longer been paid, which is reflected in lower y-o-y wage growth in the public sector – in September, it was at 4.5%.

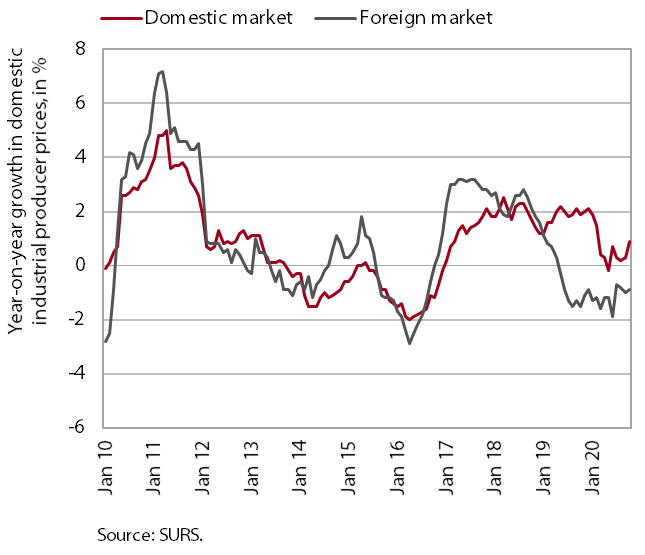

Slovenian industrial producer prices, October 2020

After a decline since the outbreak of the epidemic, Slovenian industrial producer prices remained unchanged y-o-y in October. The otherwise moderate price growth on the domestic market strengthened slightly (in all industrial groups except intermediate goods). The relatively strong growth of energy prices continued (4.8%). The growth of prices of non-durable goods for final consumption (3.0%) was also higher following the slowdown in the previous three months. The y-o-y decline in Slovenian producer prices on foreign markets remained at around 1%. Unlike on the domestic market, prices of energy and non-durable consumer goods recorded the largest y-o-y declines (–6.2% and –2.7% respectively). The y-o-y decline in Slovenian industrial producer prices outside the euro area strengthened, while in the euro area it remained more or less unchanged.