Charts of the Week

Current economic trends from 16 to 20 December 2019: current account, labour market, wages, Slovenian industrial producer prices...

The growth of employment and the decline in unemployment continue, but at a less intense pace than last year. The deterioration of economic sentiment seen for several months stopped in December, mainly due to the improvement in trade. The current account surplus remains high, largely on account of a higher trade surplus in services. Growth in property prices is somewhat lower than last year, primarily owing to noticeably weaker growth in Ljubljana. Growth in Slovenian industrial producer prices remains low; while being somewhat higher on the domestic market, it remains negative abroad.

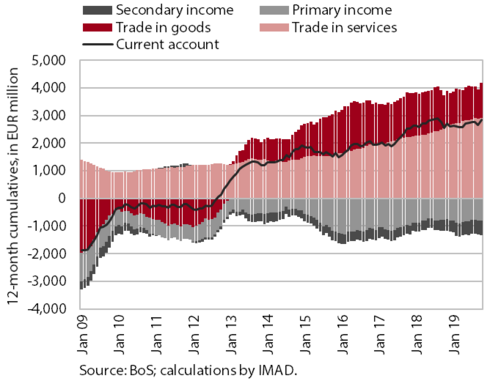

Current account, October 2019

In October, the current account surplus increased; it was higher year on year in the last twelve months (at 5.9% of estimated GDP). The higher surplus in comparison with the previous 12-month period was mostly due to a higher surplus in trade in transport, construction and processing services. The surplus in goods trade was also higher, which is attributable to volume factors since the terms of trade remained unchanged. On the other hand, the net outflows of primary and secondary incomes increased further owing to higher payments of dividends to foreign investors (primary income) and higher VAT- and GNI-based contributions to the EU budget (secondary income).

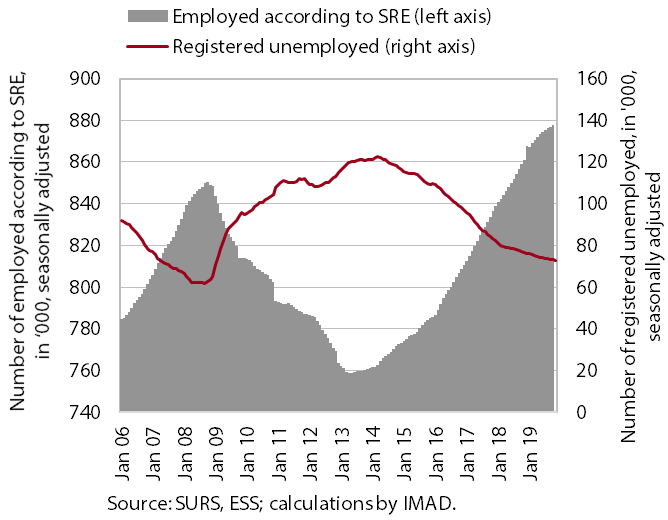

Labour market, October– November 2019

The growth of employment and the decline in unemployment are less intense than last year. The number of persons employed increased 2.6% year on year in the ten months to October (the most in construction, transportation and storage, and accommodation and food service activities), less than in the same period last year. Labour shortages accompanied by the still high labour demand are reflected in a further increase in the hiring of foreigners. Their contribution to total employment growth remains significant (more than 70%). The number of registered unemployed persons continues to decrease, albeit more slowly than at the beginning of the year. At the end of November it amounted to 72,395, which is 4.9% less than one year before.

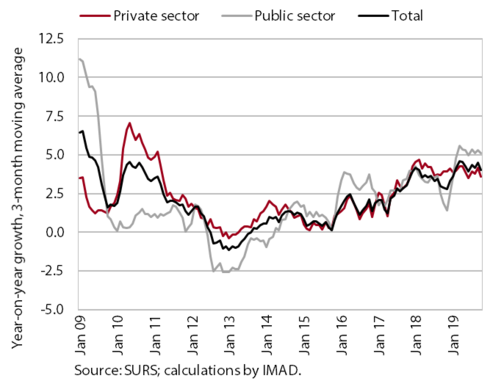

Wages, October 2019

Wage growth is higher this year than last due to wage rises in the government sector. In the first ten months, year-on-year wage growth was 4.3%, compared with 3.4% in the same period last year. Higher wage growth is mainly due to higher growth in the general government sector on account of the agreed wage rises and promotions and, partly, the increase in the minimum wage. Somewhat more moderate growth also continues in the private sector, where wages increased the most in administrative and support service activities (such as security and investigation activities), accommodation and food service activities, and trade.

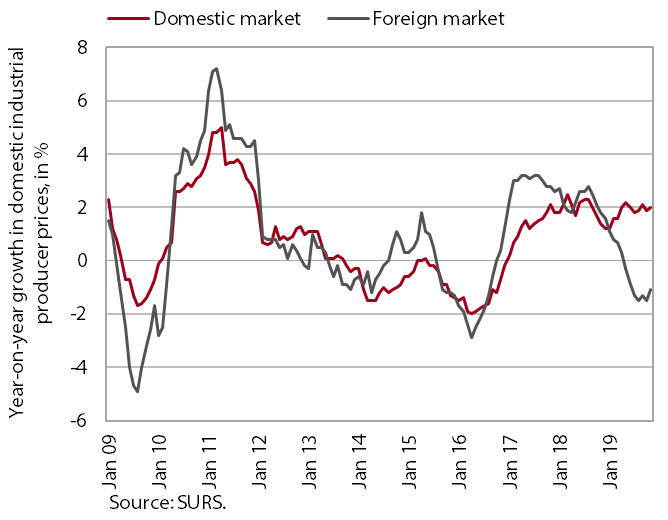

Slovenian industrial producer prices, November 2019

The total year-on-year growth of Slovenian industrial producer prices rose somewhat in November, but remained modest. The decline on foreign markets was less pronounced than in previous months, primarily owing to a somewhat smaller decline in raw material prices, which account for almost half of the index value. Price growth on the domestic market remains around 2%, still largely as a consequence of strong growth in energy prices (on account of higher prices in the supply of electricity, gas and steam, where year-on-year growth totals 15%). Year-on-year growth in non-durable consumer goods is hovering around 2%. Growth in investment goods is stable as well.

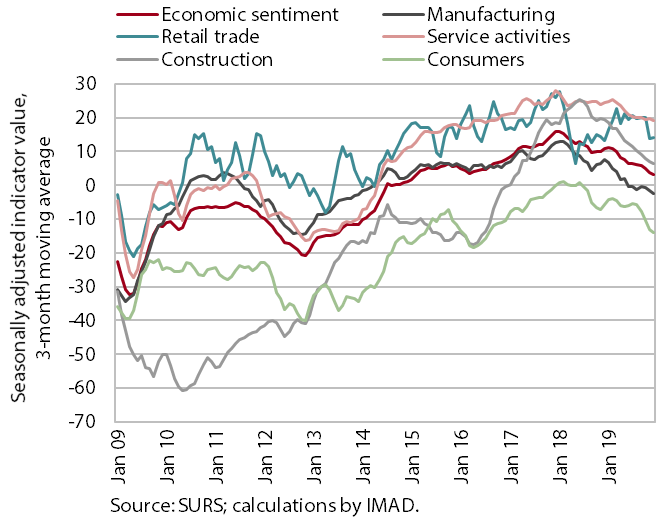

Economic sentiment, December 2019

Economic sentiment stopped deteriorating at the end of the year. After four consecutive months of decline, confidence improved somewhat in December. This is a consequence of noticeably higher confidence in retail trade, where the assessments of current sales improved significantly. Other confidence indicators were stable in the last quarter, although lower than at the beginning of the year.

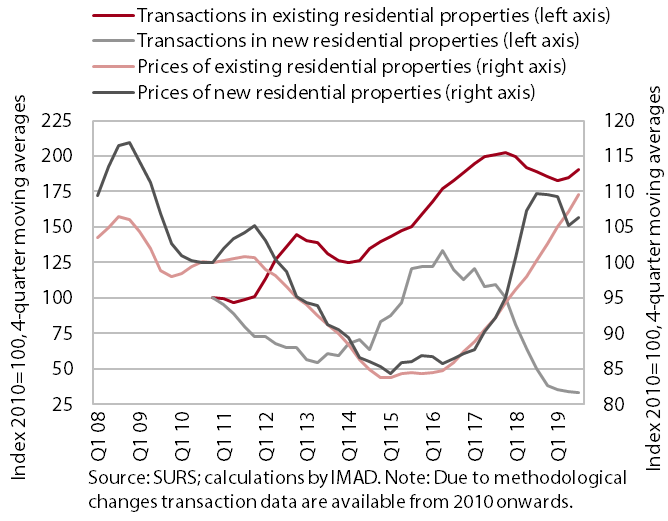

Real estate, 3th quarter of 2019

The average residential property prices increased further in the third quarter; the number of transactions rose as well, following a decline in the previous year. In the first nine months, prices were up 7.5% year on year on average (last year, 9.8% in the year as a whole). This year’s price growth is attributable to a higher number of transactions. Prices of existing family houses and existing flats outside Ljubljana increased the most. The average price of existing flats in Ljubljana, having been rising at above-average rates in the last four years, is only slightly higher this year than last. The average price of new residential properties, which accounted for only 2.2% of all transactions, was lower than one year before after two years of strong growth.