Charts of the Week

Current economic trends from 15 to 19 November 2021: turnover based on fiscal verification of invoices, Slovenian industrial producer prices, construction and other charts

Employment, which is at a historically high level, continued to rise in September, with the highest year-on-year increases in human health and social work activities and construction. Construction activity increased in September, while it remained similar to the previous quarter on average in the third quarter. Construction price growth, driven by rising commodity prices and labour shortages, slowed somewhat in September, but still remains high. High commodity prices also have a significant impact on the year-on-year growth of Slovenian industrial producer prices, which continues to strengthen. Turnover based on fiscal verification of invoices was almost a third higher in the first half of November than a year earlier, mainly due to higher turnover growth in retail trade in the week leading up to the introduction of tighter business and trade restrictions. The current account surplus, which remains high, is declining, mainly due to a lower surplus in trade in goods, with September seeing the lowest 12-month surplus in at least four years.

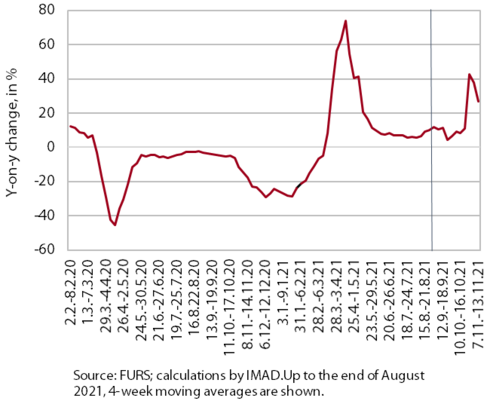

Turnover based on fiscal verification of invoices, October–November 2021

According to data on the fiscal verification of invoices, total turnover between 31 October and 13 November was 32% higher year-on-year and 11% higher than in the same period of 2019. Year-on-year growth strengthened compared to the previous two weeks, mainly due to higher turnover in the week leading up to the introduction of stricter business and trade restrictions (introduced on 8 November). Growth was particularly strong in retail trade, up by a third year-on-year in the mentioned week and by a quarter compared to the same period in 2019. Year-on-year growth in most sectors of the economy moderated in the week of 7–13 November (compared to the previous week), but remained very high, especially in those sectors that were almost completely shut down during this period last year (accommodation and food service activities, travel agencies and arts, entertainment and recreation).

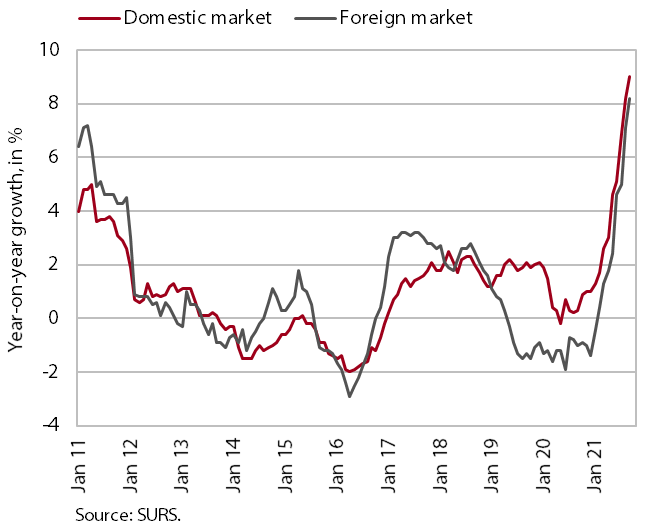

Slovenian industrial producer prices, October 2021

The year-on-year growth in Slovenian industrial producer prices (9.2%) increased in October, but it was somewhat less pronounced than in the previous months. Price growth in the domestic market is similar to that in foreign markets. Overall growth continues to be driven mainly by commodity and capital goods prices, which rose by 14.2% and 8.8% year-on-year, respectively, in October. Growth in energy prices fell by about a quarter, to 6.2%, compared to September, reflecting lower year-on-year price growth in foreign markets (38.4%). Growth in consumer goods prices was still relatively moderate (1.9%), but has been gradually strengthening. Prices of durable goods rose somewhat more markedly (3%), mainly due to higher growth in the domestic market, where they were more than 5% higher year-on-year (the highest increase in the last ten years).

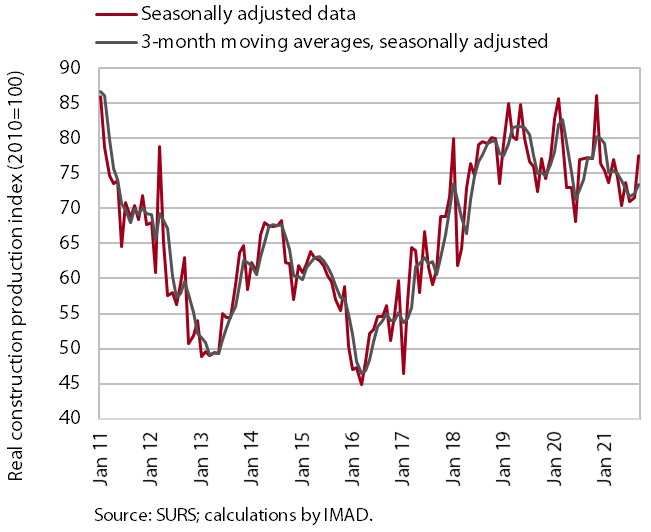

Construction, September 2021

Construction activity increased in September but remained similar to the previous quarter on average in the third quarter and was lower than a year ago. At the monthly level, the value of construction output increased by 8.5%. On average, it remained at a similar level in the third quarter as in the second quarter and was 4.8% lower than a year ago. With strong monthly fluctuations, activity in specialised construction has been stagnant for three years at the highest level since 2011, while activity in civil engineering works has picked up somewhat this year after stagnating in 2019 and 2020. The situation is similar in residential construction, where activity has increased even more this year. The decline in non-residential construction activity that began last year has intensified this year. The stock of contracts, which increased in the first half of the year and exceeded last year's level, remains very volatile. It fell sharply in August and has been below the previous year's level since then.

Construction price growth, driven by rising commodity prices and labour shortages, slowed somewhat in September, but still remains high. The implicit deflator of the value of completed construction works (used to measure prices in the construction sector) was 7% in September, which is one percentage point lower than in August.

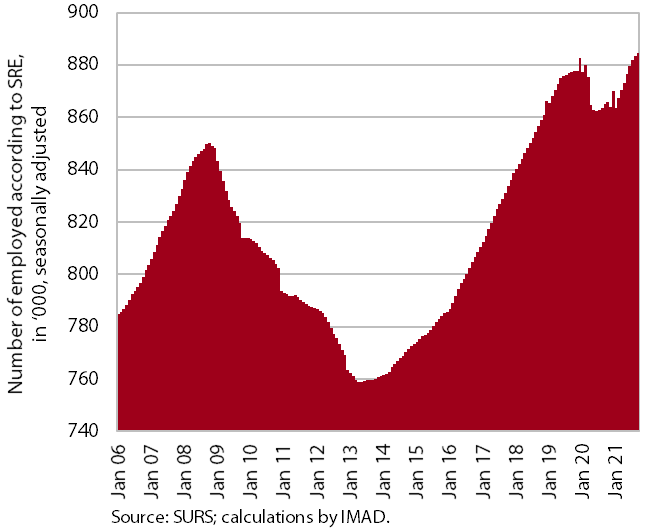

Labour market, September 2021

The historically high level of employment further increased in September. In the first nine months, the number of employed persons was 0.9% higher than in the same period last year. Employment growth was higher for the self-employed (1.4%) than for employees (0.7%), although the decline in the number of self-employed last year was much smaller than for employees. In September, the highest year-on-year increases were again recorded in construction and human health and social work activities. Employment growth was also high in the accommodation and food service activities, reflecting a relatively quick recovery after last year’s sharp decline, but the number of employed persons remained below September 2019 levels. The containment measures also had a strong impact on the arts, entertainment and recreation where the number of employed people also remained lower this September than in the same period of 2019.

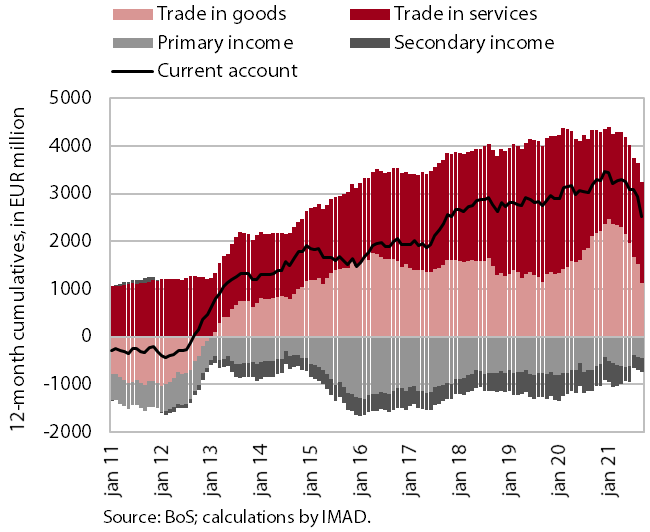

Current account of the balance of payments, September 2021

The current account surplus was again lower year-on-year in the third quarter. With deterioration in the terms of trade and higher real growth in imports than exports, this was again largely due to a lower trade surplus. The surplus in trade in services was higher year-on-year, mainly due to a larger surplus in administrative and support service activities and travel services. Net outflows of primary income were lower year-on-year in the third quarter, mainly due to lower net payments of dividends and profits to foreign investors and lower net payments of interest on external debt. Net outflows of secondary income were also lower year-on-year, mainly due to higher private sector transfers (net payments of non-life insurance premiums and other transfers). The 12-month current account surplus on the balance of payments stood at EUR 2.5 billion in September (5% of estimated GDP).